The Iran war, the global economic earthquake, and why China, Japan, South Korea, and Singapore are losing more than the rest of the world

Xpert Pre-Release

Available in 27 languages 📢

Prefer Xpert.Digital on GoogleⓘPublished on: March 30, 2026 / Updated on: March 30, 2026 – Author: Konrad Wolfenstein

The Iran war, the global economic upheaval, and why China, Japan, South Korea, and Singapore are losing more than the rest of the world – Image: Xpert.Digital

The global economy's bottleneck is closed: Why Asia's export crisis will affect us all

When oil becomes a weapon – how a sea bottleneck brings the entire global economy to its knees

The war between the US, Israel, and Iran has severed the lifeline of global energy supply and plunged the world economy into a historic state of emergency. With the de facto closure of the Strait of Hormuz at the end of February 2026, an unprecedented price shock has erupted on world markets, far exceeding the already exploding oil and gas prices. While Europe and the US grapple with the looming return of stagflation, Asian economic giants like Japan, South Korea, and China face an existential crisis. Disrupted supply chains, prohibitive logistics costs, and the threat of a production halt in the global semiconductor industry due to an acute helium shortage demonstrate that this conflict is no longer merely a geopolitical escalation in the Middle East, but rather the largest and most dangerous shock to the global economy in half a century.

And why Asia is losing more than the rest of the world combined

The war between the US, Israel, and Iran has sent a shockwave through the global economy since the end of February 2026, the intensity of which can hardly be overstated. What began in the Strait of Hormuz has, within a few weeks, escalated into a triple crisis of energy price shock, the threat of inflation, and a slump in growth – hitting a global economy already weakened by the trade war and the ongoing conflict in Ukraine at a particularly inopportune moment. Detailed analysis reveals that while Europe and the US are at the center of public debate, it is the Asian economies – above all China, Japan, South Korea, and Singapore – that are suffering the most severe structural damage.

The bottleneck of the world's energy supply

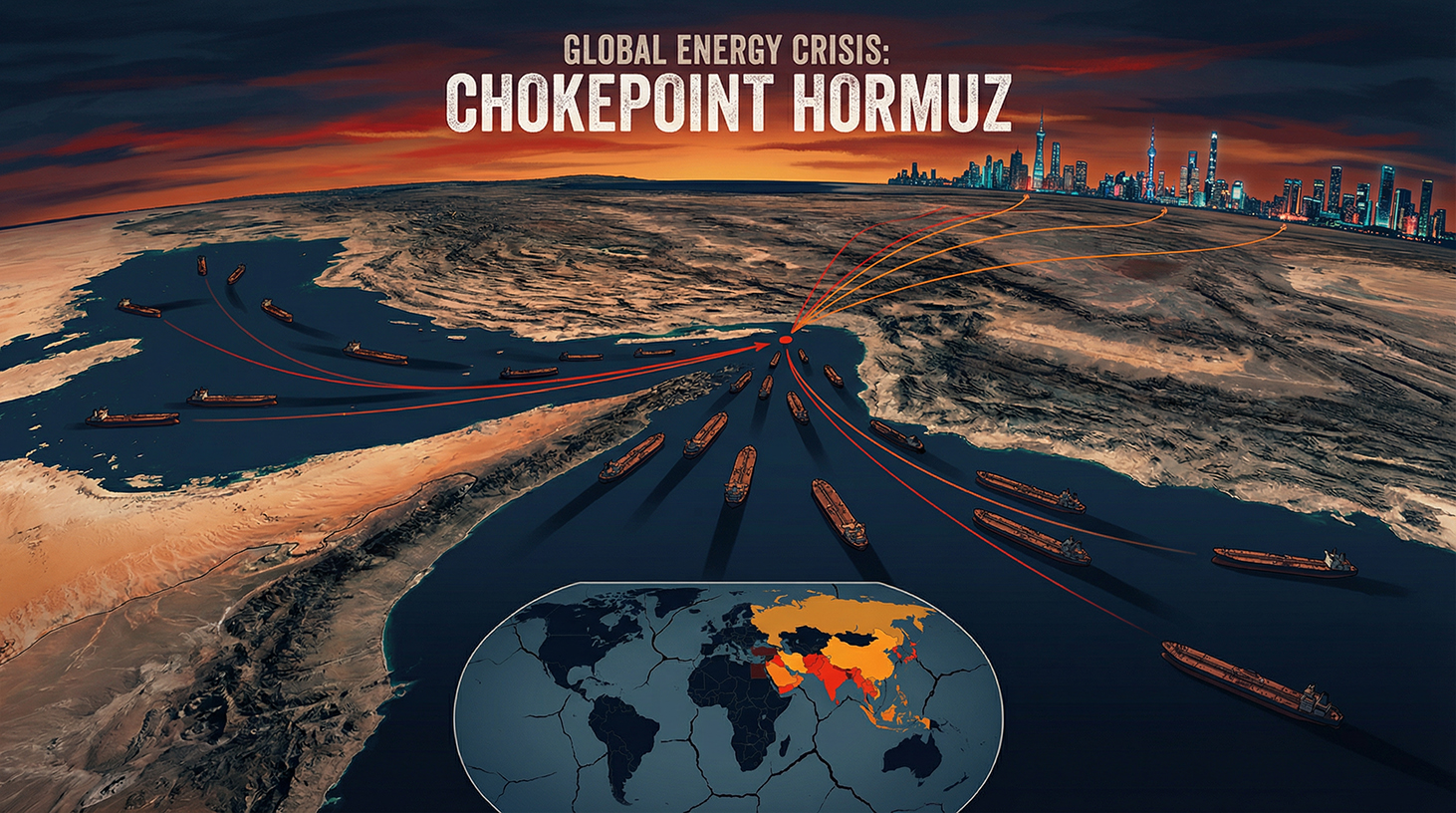

To understand the geopolitical significance of the current situation, one must first grasp the crucial strategic role the Strait of Hormuz plays in global energy supply. This narrow waterway between Iran and Oman connects the Persian Gulf with the Gulf of Oman and the Arabian Sea. It is the only sea route through which Saudi Arabia, the United Arab Emirates, Kuwait, Iraq, and Iran can ship their oil exports.

Approximately 20 percent of global oil and LNG trade passes through this strait daily. According to the US Energy Information Administration (EIA), around 13 million barrels of crude oil were expected to transit it daily by 2025 – a volume that could hardly be replaced by alternative routes. Even more significant, however, is a geographical fact that fully explains the current crisis: Over 80 percent of the energy transported through the Strait of Hormuz is destined for consumers in Asia – particularly China, India, Japan, and South Korea. Therefore, the blockade of this strait is not merely a regional trade dispute, but an attack on the energy heart of the Asian continent.

Qatar, the world's largest LNG exporter, supplies around 20 percent of the global liquefied natural gas market – and these deliveries also pass through the Strait of Hormuz. Furthermore, an attack on Qatar's globally significant LNG facility has, according to media reports, put 17 percent of its capacity out of operation for up to five years. For Asia, the primary consumer of these quantities, this is a catastrophe with long-lasting repercussions.

From attack to blockade – The escalation spiral

On February 28, 2026, the US and Israel launched coordinated attacks on Iran, killing, according to media reports, the regime's leadership. Iran responded with what has been considered its most potent asymmetric weapon for decades: the de facto closure of the Strait of Hormuz. Several ships in the region received radio messages from the Iranian Revolutionary Guard stating that no vessel was permitted to pass through the strait. During the second week of the war, not a single tanker transited the strait—approximately 500 oil and gas tankers were trapped.

Iranian counterattacks also damaged the oil and gas infrastructure of neighboring Arab states, including a major Saudi Arabian refinery and gas facilities in Qatar. The shockwave that swept through global energy markets from that moment on was immediately felt by Asian importers: In Japan, South Korea, and China, gas and oil prices rose more sharply on average than anywhere else in the world. Poorer Asian countries became embroiled in a veritable bidding war for scarce oil and gas supplies, which only wealthier nations like Japan and South Korea were able to win, at least for the time being, by paying exorbitant prices.

IEA chief Fatih Birol issued a stark warning about the greatest threat to energy security in the history of the modern global economy, stating that more than 40 power plants in nine countries had been severely damaged since the start of the war. This figure makes it clear that the damage is by no means limited to a single strait, but has affected the entire energy infrastructure of the region.

The oil price shock and its markets

The economic impact of the blockade immediately hit the energy markets. Before the outbreak of military operations at the end of February 2026, Brent crude oil was trading at around $73 per barrel. In the first trading days after the attacks began, the price of Brent rose by almost 19 percent to nearly $110, while the US benchmark West Texas Intermediate (WTI) broke the $100 mark for the first time since 2022. At its peak, Brent temporarily reached $120 per barrel.

Asian refinery companies were hit particularly hard by this price surge. Refining margins in Singapore – one of Asia's most important refining and trading hubs – skyrocketed to almost $30 per barrel, the highest level since 2022. The margin for jet fuel even exceeded $52 per barrel, doubling within just a few days. For refineries in Japan, South Korea, and India, which are technically designed to process heavy crude oil from Saudi Arabia, Kuwait, and Iraq, this resulted in a virtually insurmountable double burden: on the one hand, raw material shortages due to the blockade, and on the other, the technical impossibility of quickly substituting it with lighter US or West African oil.

The spectre of stagflation is returning

Economists of all stripes agree on one point: The combination of rising energy prices and declining growth carries the risk of stagflation – that dreaded economic scenario which paralyzed entire economies for years in the 1970s. Harvard economist Kenneth Rogoff painted a bleak overall picture: The Iran war, following the trade war and the ongoing war in Ukraine, represents the biggest shock to growth and prices to hit the global economy in five decades. The pressure on Europe and Asia is considerably worse than on the US and is intensifying in terms of both inflation and growth.

The Japanese business association Keidanren warned that Japan's industrial sector was facing increasing stagflation risks. Japan's composite Purchasing Managers' Index (PMI) fell from 53.9 to 52.5 – the weakest increase in three months. In South Korea, the benchmark KOSPI index plummeted by more than 12 percent on March 4, trading was temporarily suspended, and the Korean won also depreciated significantly. These market reactions demonstrate how immediately and brutally Asian financial markets responded to geopolitical developments.

China – The world power in a dilemma

China plays a profoundly contradictory role in this crisis. As the world's largest oil importer and simultaneously Iran's closest ally, Beijing is both the main victim and a covert beneficiary of the Hormuz blockade. Iraq, Saudi Arabia, the United Arab Emirates, and Oman together account for about 40 percent of China's crude oil imports. Roughly half of all Chinese oil imports pass through the Strait of Hormuz. Furthermore, Iranian oil accounts for about 12 to 13 percent of China's total oil imports – replaceable, but not without considerable effort and not in the short term.

Nevertheless, China has deliberately prepared for such a scenario. According to analysts' estimates, the People's Republic possesses strategic oil reserves of around 1.2 billion barrels – enough to cover demand for three to four months. China is the only country in the world that continues to receive Iranian oil through the blockade: since the start of the war, at least 11.7 to 12 million barrels of Iranian crude oil are believed to have been exported, all destined for China, as documented by satellite imagery from the analysis firms TankerTrackers and Kpler. Iran maintains this special route for China because Beijing has been purchasing 80 to 90 percent of all Iranian oil exports for years, making it a vital economic lifeline for the mullah regime.

Despite this preferential treatment, China faces structural challenges. Chinese refineries have been ordered to suspend diesel and gasoline exports to prevent domestic supply shortages. According to the analysis firm Kpler, tankers carrying a total of approximately 46 million barrels of oil are anchored off the coasts of Singapore and China – a buffer stock that can provide short-term relief but does not offer a long-term solution. Particularly noteworthy is the fact that, according to media reports, Iran was considering restricting passage through the Strait of Hormuz to ships whose cargo is settled in Chinese yuan. This would transform a military blockade into a monetary policy instrument – an attack on the petrodollar system that has formed the basis of global energy trade since 1974.

China's strategic response to the crisis is twofold. On the one hand, Beijing is desperately seeking alternatives to the Gulf region: Russia, already the largest supplier of crude oil, accounting for approximately 20 percent of Chinese oil imports, is to be further strengthened as an energy partner, according to the British Financial Times. On the other hand, China is focusing on deepening its financial ties with Iran in order to establish the yuan as an international reserve currency in energy trading. The infrastructure for this – the Cross-Border Interbank Payment System (CIPS) – already exists and could gain considerable global significance in the wake of the crisis.

The geopolitical dimension should not be underestimated. Some analysts see the US attack on Iran as a strategically motivated operation ultimately aimed at bringing China's energy supply under American control in the long term. Whether this thesis is accurate or exaggerated is difficult to definitively assess – but the structural consequence that a US-controlled or US-friendly Iran would fundamentally threaten Chinese energy security is undeniable. China is therefore monitoring the situation with a level of strategic attention that goes far beyond what can be explained economically.

Japan – 93 percent dependency as an existential risk

Japan represents one of the starkest contrasts in the current crisis: hardly any energy resources of its own, maximum dependence on the Gulf region. According to the Japanese Ministry of Economy, Trade and Industry, 93 percent of Japan's crude oil imports come from four Middle Eastern countries: the United Arab Emirates, Saudi Arabia, Kuwait, and Qatar. The vast majority of these shipments pass through the Strait of Hormuz. For Japan, the blockade of this route is therefore not an abstract trade policy challenge, but a direct threat to its basic industrial supply.

Japan's immediate response was to release strategic oil reserves. At the end of 2025, the combined state and private reserves covered domestic demand for 254 days. During the second week of the war, the government began releasing approximately 45 days' worth of these reserves to prevent price spikes and maintain stability in energy-intensive industries such as automotive, steel, and machinery manufacturing. Companies like Toyota, Mitsubishi, and Nippon Steel depend on a stable energy supply and cannot quickly develop alternative energy sources.

Prime Minister Takaichi announced that measures to limit gasoline prices would be considered, underscoring the government's concern about growing signs of lasting economic damage. The yen weakened by 0.6 percent since the start of the war, falling to 156.95 per US dollar and approaching the psychologically important 160 mark—a level that further increases import costs, as Japan pays its energy bills in dollars and a weak yen further reduces purchasing power.

The Bank of Japan (BOJ) faces a monetary policy dilemma of historic proportions. Even before the crisis, it had cautiously raised its key interest rate to 0.75 percent. Now, rising oil prices are forcing further interest rate hikes to combat inflation, while overly aggressive tightening risks pushing the already strained economy into recession. Seisaku Kameda, former chief economist of the BOJ, told Reuters that the BOJ has few options other than raising interest rates, as the oil shock is exacerbating inflationary pressures on an economy already under price pressure. Board member Kazuo Momma, for his part, warned that it is difficult to say whether the risks of inflation or recession outweigh the risks – with the practical consequence that the BOJ must reassess the situation at every meeting.

The economic calculations are sobering. The Nomura Research Institute estimates that a prolonged conflict would reduce Japan's real GDP by 0.18 percentage points and increase inflation by 0.31 percent. Takuya Hoshino, chief economist at the Dai-ichi Life Research Institute, calculated that, in a scenario with $130 per barrel, Japan's real GDP would fall by 0.58 percent in the first year and by 0.96 percent in the second year. Morgan Stanley MUFG Securities estimates that every 10 percent increase in oil prices reduces Japan's real GDP by about 0.1 percentage points. With oil prices rising by more than 40 percent above pre-war levels, the cumulative losses in growth for Japan are therefore substantial.

South Korea – Export nation on the brink

Few countries in the world are as dependent on energy imports from the Middle East as South Korea. The country obtains around 70 percent of its crude oil and 20 percent of its liquefied natural gas from the Gulf region – almost exclusively via the Strait of Hormuz. As the world's fourth-largest importer of crude oil, South Korea has virtually no domestic energy production and was therefore directly affected from the very first day of the blockade.

The South Korean government's response was marked by remarkable resolve. President Lee Jae-myung ordered a government-imposed cap on fuel prices for the first time in nearly three decades. Furthermore, through intensive diplomatic negotiations, Seoul secured an emergency shipment of more than six million barrels of crude oil from the United Arab Emirates – with two tankers calling at a UAE port via a route that bypassed the Strait of Hormuz. Another two million barrels came from a joint reserve that the UAE had stored in South Korea. The total amount is more than double South Korea's daily consumption – a scale that, while providing temporary stabilization, does not offer a solution to a prolonged blockade.

In parallel, the government decided on a radical energy policy reversal: Production limits for coal-fired power plants were lifted, and the utilization of nuclear power plants is to be increased to up to 80 percent. A total of 22.46 million barrels from strategic oil reserves are to be released gradually within three months, and the state-owned Korea National Oil Corporation must also import 3.35 million barrels from its own overseas projects by June. These measures illustrate the extent of the emergency: A democratic market economy is resorting to instruments of state resource management that would be unthinkable in normal times.

The consequences for South Korea's export sector are particularly worrying. The Hyundai Economic Research Institute has calculated that an average annual oil price of $80 reduces South Korean GDP growth by 0.1 percentage points; if it rises to $100, the decline could be 0.3 percentage points. The Korean central bank had calculated its most recent growth forecast based on an oil price of $64 – with prices remaining high, economists estimate that growth could be halved.

Added to this is a sector-specific threat whose magnitude can hardly be overestimated: the South Korean petrochemical and semiconductor industries. South Korea imports around 25 percent of its naphtha from the Middle East – an essential raw material for the petrochemical industry. Supply disruptions and price fluctuations in naphtha could force petrochemical companies to reduce production. Furthermore, other critical raw materials are affected: aluminum, sulfur, and – most seriously – helium.

Our China expertise in business development, sales and marketing

Our China expertise in business development, sales and marketing - Image: Xpert.Digital

Industry focus areas: B2B, digitalization (from AI to XR), mechanical engineering, logistics, renewable energies and industry

More information here:

A thematic hub offering insights and expertise:

- Knowledge platform covering global and regional economies, innovation and industry-specific trends

- A collection of analyses, insights, and background information from our key areas of focus

- A place for expertise and information on current developments in business and technology

- A hub for companies seeking information on markets, digitalization, and industry innovations

Singapore at its limit: Why the Hormuz blockade is hitting Asia's trading heart

The silent system shock: Helium, chips and the global supply chain

One of the most underestimated dimensions of the Iran war concerns a raw material that plays almost no role in public perception but is of strategic importance to the global economy of the 21st century: helium. Qatar is one of the world's most important helium suppliers, and this raw material is indispensable for semiconductor production – it is used to cool the high-precision manufacturing equipment and cannot be replaced by any other substance.

South Korea is home to the world's largest memory chip manufacturers, Samsung and SK Hynix. Taiwan is home to TSMC, the world's leading contract manufacturer of advanced semiconductors. Both locations rely on Qatari helium – and both now face the reality that deliveries from Qatar are significantly hampered by the combination of declining production and the Hormuz blockade. Jochen Stanzl, market expert at CMC Markets, succinctly summarized the danger: Taiwan and South Korea have helium reserves for approximately three months. After that, they would have to halt production because helium cannot be replaced for cooling the machinery. The worst-case scenario of such a disruption would be a global collapse of the semiconductor supply chain – with catastrophic consequences for the entire world economy.

South Korean industry representatives, following meetings with government officials, pointed out that the supply of helium and other raw materials such as neon – also essential in chip manufacturing – could be disrupted. In addition to material shortages, the industry fears that a prolonged conflict could lead to rising energy costs and delays in the region's planned AI data centers, which could dampen demand for chips. Samsung Electronics and SK Hynix saw their share prices fall by around four percent in a single trading day after the outbreak of war. This is because the Middle East war is driving up chip prices, as chip manufacturers are quickly passing on the sharply increased energy, material, and logistics costs to their customers.

Singapore – The threatened linchpin

Singapore occupies a unique position in Asian economic geography: The city-state is simultaneously one of Asia's most important refinery locations, the world's most important bunkering center, and a global transshipment hub for goods of all kinds. It is precisely this significance that makes Singapore one of the most exposed victims of the Hormuz crisis.

Since the end of February, prices for marine fuels – so-called bunker prices – have more than doubled in Singapore. Ships are having to wait longer than before for their fuel, as bunker fuel, which consists primarily of Gulf refinery products, has become scarce due to the blockade. Lynn Loo, head of the Global Centre for Maritime Decarbonisation in Singapore, warned of an impending bunker fuel supply crisis in Asia that could shake global trade to its core – potentially worse than during the coronavirus pandemic. Several bunker traders are holding back on large orders because extreme price fluctuations are making risk management virtually impossible.

Singapore's Prime Minister Lawrence Wong publicly stated that the government was closely monitoring the situation and examining the impact on the economy and consumers. He explicitly warned that if the Strait of Hormuz remained blocked much longer, the damage would not be limited to rising energy prices but would affect the entire economy. Singapore reviewed its GDP forecast immediately after the outbreak of war – a clear indication that the government anticipated significant losses in growth.

Singapore's structural vulnerability is particularly high. As a small city-state without its own energy production and with an economy entirely dependent on international trade and transit, Singapore can hardly build up any buffers. Singapore's strength – its openness and global interconnectedness – becomes a weakness in a crisis. Every delay in shipping movements, every price increase for bunker fuel, and every uncertainty about alternative routes strikes at the very core of the city-state's business model.

The broader South and Southeast Asian context

Beyond the four economies in focus, the entire Southeast Asian economic system is suffering. In Thailand, export growth figures for February fell far short of expectations: analysts had predicted an increase of 15.8 percent, but only 9.9 percent was achieved. The Ministry of Commerce in Bangkok warned of further export declines due to higher fuel prices and transportation costs. Vietnam canceled 23 domestic flights per week starting in April due to the threat of a kerosene shortage. The Philippines even considered temporary grounding of aircraft.

In India—another major player in the region—the private sector experienced its weakest growth in three years, as the country imports around 90 percent of its crude oil and almost half of its natural gas. Indian refineries reduced their capacity, further exacerbating the already strained fuel supply on the subcontinent. The overall picture for the region is sobering: Asia is not only the largest consumer of the affected energy flows, but also structurally the least able to switch to alternative supply routes at short notice. The supply routes of alternative providers—US shale oil, Russian Arctic oil, West African oil—are simply too long and technically incompatible with the types of refineries prevalent in the region.

The geostrategic reorganization: Russia, the Yuan, and new alliances

The crisis is accelerating geopolitical shifts that had been brewing for some time, but are now suddenly gaining momentum. Russia is the quiet winner in this situation: higher oil prices directly translate into higher export revenues for Moscow, while the Iranian crisis is simultaneously driving China further into the arms of its northern neighbor. Neil Beveridge, head of China energy research at the Bernstein research firm in Hong Kong, has already clearly identified one of the most important conclusions to be drawn from the crisis: the deepening of Chinese energy relations with Russia – in both crude oil and gas.

This creates a strategically advantageous situation for Russia: A war waged by the US and Israel indirectly strengthens Moscow's economic resilience and simultaneously deepens the Eurasian axis, which is central to Russia's long-term geopolitical strategy. China and Russia, already linked by their shared opposition to the Western order, will be further intertwined in energy policy as a result of the Iran crisis.

Furthermore, the crisis opens the door to a potential weakening of the petrodollar system. Should Iran actually realize its demand for yuan in exchange for passage of the Strait of Hormuz, and should China exploit this strategically, the Iran-Iraq War could be seen in the long term as a watershed moment, marking the first time the US dollar's share of global energy trade has been structurally diminished. This effect is limited in the short term, but of considerable long-term significance for the architecture of the global financial system.

Three crises, one global economy

The particular urgency of the current situation stems not only from the Iran war, but from the accumulation of several simultaneously acting stressors. Even before the outbreak of war, the Trump administration's trade war had significantly weakened global trade dynamics. According to calculations by Allianz Trade, global trade growth slowed from 2 percent in 2025 to just 0.6 percent in 2026. Global gross domestic product is projected to grow by only 2.5 percent in 2026 – significantly below the historical average.

This trade downturn is hitting Asia's export-oriented economies particularly hard. Japan, South Korea, Taiwan, and Singapore are fundamentally dependent on open global markets for their economic structure. A combination of rising input costs due to the energy price shock, falling global demand due to the trade war, and disrupted supply chains caused by the Hormuz blockade creates the worst possible environment for export-oriented industrial economies. The Kiel Institute for the World Economy warned early on that the simultaneity of these shocks could unleash a dynamic of its own that far exceeds the sum of its individual effects.

The logistics crisis: When the world's factory runs out of fuel

A study by the Supply Chain Intelligence Institute Austria (ASCII), the Complexity Science Hub (CSH), and TU Delft estimates the total economic damage to global trade caused by the Hormuz blockade at around €400 billion annually – solely due to supply chain disruptions, without including the impact on energy prices. For Asia, the world's manufacturing hub, this logistics crisis has a particular significance: when bunker fuel prices skyrocket in Singapore, when shipping companies have to reroute their services, when insurance costs for tankers rise sharply – then Asia's exports to the rest of the world become significantly more expensive.

Logistics companies like DHL reacted with contingency plans: freight rail lines between Abu Dhabi and the Saudi border, massive expansion of truck fleets, and air freight for critical components such as microchips. Where ships are stuck, trains or planes take over the cargo – at costs two to three times higher than under normal conditions. These additional costs ultimately end up with consumers worldwide in the form of higher prices for consumer goods, electronics, and industrial products.

Structural change in installments: The long-term consequences for Asia

Even a swift end to the war would not simply return Asia's energy and supply chain markets to their pre-war state. Experts agree that the war with Iran has permanently altered energy markets and fundamentally challenges the strategic planning foundations of Asian economies.

Japan, South Korea, and Taiwan will reassess their dependencies and accelerate diversification strategies. For South Korea, the crisis experience will most likely lead to a permanent revaluation of nuclear power in national energy policy—the pragmatic return to nuclear and coal as emergency measures restores political weight to the nuclear energy sector. For Japan, the shock is likely to accelerate the energy transition and lead to massive investments in energy storage technologies—less for environmental reasons than for sound strategic considerations.

China, in turn, will incorporate the lessons of the crisis into its long-term energy security strategy: greater diversification of import sources, deeper cooperation with Russia, expansion of alternative transport routes (rail links across Central Asia, pipeline systems, the Jask terminal in the Persian Gulf), and potentially accelerated internationalization of the yuan in energy trading. In just a few weeks, the crisis has accomplished what years of strategic planning have failed to do: it has ruthlessly exposed the fragility of Asia's existing energy supply architecture.

For the semiconductor industry, the backbone of the modern digital economy, the crisis will trigger a long-term acceleration of raw material diversification. Helium, neon, and other critical gases from the Gulf region will increasingly need to be substituted by alternative sources—particularly from Russia, the US, and Australia. Building national reserves of critical raw materials, which until now have been sourced just-in-time from a handful of sources, will become a national security priority.

Geopolitical uncertainty as a structural economic problem

Beyond the immediate price effects, the Iran war has created another, more serious layer of economic damage: massive uncertainty. Investments are being postponed, supply chains reassessed, and long-term planning put on hold. This uncertainty premium acts like a hidden tax on all global economic activity—it makes energy more expensive, complicates planning, and reduces investors' risk appetite. And it comes at a time when the global economy desperately needs stability and reliability after years of pandemic, inflation, and geopolitical turmoil.

Kenneth Rogoff aptly described Trump's economic policies as the destruction of established institutions and foundations of trust—something that had built up over years and could not be quickly restored. The Iran war adds an acute geopolitical dimension to this structural erosion. Even if the Strait of Hormuz were to reopen tomorrow, market confidence in the region's stability would remain permanently shaken. Shipping companies, insurers, and energy companies will price in higher risk premiums for years to come—and this effect will hit Asia, the main consumer of Gulf energy, proportionally the hardest.

A shock that was coming

In retrospect, the risk of such a scenario was known and widely discussed. Iran had invested heavily in asymmetric warfare capabilities in recent years – drones, naval weapons, and sea mines. For decades, the Strait of Hormuz had been considered the most vulnerable point in global energy supply in strategic planning exercises. What is new is not the threat itself, but its realization – and its simultaneous occurrence with other systemic shocks.

The global economy, and Asia in particular, must now learn to cope with a new reality: the era of cheap, secure energy from the Gulf may be drawing to a close. Those who dismiss this as a temporary crisis fail to grasp the magnitude of the structural transformation currently underway. What is happening is not just another conflict in the Middle East. It is a historic rupture—the greatest economic shock in five decades—and Asia stands at its most severe fault line.

Your global marketing and business development partner

☑️ Our business language is English or German

☑️ NEW: Correspondence in your native language!

Konrad Wolfenstein

I and my team are happy to be available to you as your personal advisor.

You can contact me by filling out the contact form here or simply call me at +49 7348 4088 965. My email address is: [email protected]

I'm looking forward to our joint project.

☑️ SME support in strategy, consulting, planning and implementation

☑️ Creation or realignment of the digital strategy and digitization

☑️ Expansion and optimization of international sales processes

☑️ Global & Digital B2B trading platforms

☑️ Pioneer Business Development / Marketing / PR / Trade Fairs

🎯🎯🎯 Data-driven B2B industry hub as a quasi-in-house solution

The quasi-in-house solution: How Xpert.Digital closes operational gaps in B2B marketing and sales – Smart Content-Driven Business - Image: Xpert.Digital

Xpert.Digital is a data-driven B2B industry hub led by Konrad Wolfenstein . The company acts as an external, quasi-in-house solution for industrial partners, closing operational gaps in marketing, content, and sales – without requiring additional resources on the client side.

More information here: