The US is not our friend! EU pincers: The bitter truth about the transatlantic alliance

Xpert Pre-Release

Available in 27 languages 📢

Prefer Xpert.Digital on GoogleⓘPublished on: July 3, 2026 / Updated on: July 3, 2026 – Author: Konrad Wolfenstein

The US is not our friend! EU pincers: The bitter truth about the transatlantic alliance – Image: Xpert.Digital

Economic sovereignty: Why Europe urgently needs to emancipate itself from US power

Europe regulates, America collects: The transatlantic relationship was one of the cornerstones of the Western economic order

Between strategic partnership and costly dependence: Why Europe urgently needs to wake up to its relationship with the USA

For decades, the transatlantic partnership has been considered the unshakable foundation of the Western world. The division of labor seemed simple and profitable: the US guaranteed military security and provided technological impetus, while Europe shone with its industrial strength and a vast, high-spending domestic market. But those days are over. Beneath the surface of shared values and diplomatic platitudes, a profound structural asymmetry has developed, increasingly threatening European prosperity and political sovereignty.

Today, the picture is sobering: While Europe is massively dependent on American structures in key areas such as energy, digitalization, financial markets, and security, US corporations are reaping the strategic and economic benefits. From expensive liquefied natural gas (LNG) and dominant cloud infrastructures to the global power of the dollar, the US consistently uses its geopolitical leverage to further its national interests. Europe, on the other hand, is becoming bogged down in piecemeal regulation instead of building its own globally competitive counterweight.

For Germany, a leading export-oriented industrial nation, this development is becoming a matter of survival. The following article offers a sharp, unbiased analysis of how a once equal partnership has transformed into an asymmetrical relationship of dependency – and what Europe must now do to avoid becoming a mere recipient of orders and a sales outlet for American power politics.

Europe pays, American corporations profit, Washington sets the rules: Why the transatlantic partnership is closer than ever economically, but is becoming increasingly costly for the European Union strategically

The transatlantic relationship is one of the cornerstones of the Western economic order. For decades, this partnership was considered a model of success: The United States offered security stability, technological dynamism, deep capital markets, and a vast domestic market. Europe, in turn, contributed industrial strength, export quality, institutional stability, and markets with strong purchasing power. For a long time, this division of labor seemed productive and mutually beneficial. However, in recent years, the nature of this relationship has shifted. What was once a partnership between relatively balanced centers of power has increasingly become an asymmetrical relationship in which the US leverages its economic, technological, energy, and security advantages far more consistently than the European Union leverages its own strengths.

The central question, therefore, is not whether the US is "exploiting" Europe in a moral or even criminal sense. The more precise question is whether a structural asymmetry has become entrenched in the transatlantic relationship, in which the US disproportionately benefits while Europe bears a growing share of the economic costs, strategic risks, and political adjustment burdens. From an economic perspective, there is much to suggest that this is indeed the case. The US is acting within its national interests. The real problem, therefore, lies less in American toughness than in European openness without an equivalent counterweight, in European fragmentation without a coherent industrial strategy, and in a security architecture that systematically limits economic sovereignty.

A factual, strategic analysis must avoid two errors. The first error lies in anti-American oversimplification. Europe is not powerless, and the US is not the sole cause of European weaknesses. The second error lies in the romanticized view of the transatlantic partnership. References to shared values do not replace a sober assessment of financial flows, technological dependencies, location decisions, and industrial policy consequences. Anyone wishing to make a strategic judgment must consider both aspects simultaneously: The US remains indispensable for Europe, but this very indispensability has long since become a cost factor itself.

More information here:

The new asymmetry in the transatlantic relationship

Economic relations between the EU and the US are extremely close. The United States is one of the most important markets for European goods exports. At the same time, Europe is a highly profitable sales, investment, and regulatory environment for American companies. At first glance, this appears to be a reciprocal arrangement. However, a closer look reveals a qualitative shift: the US controls the key areas with the higher strategic return. These include energy exports during times of crisis, digital platforms, cloud infrastructures, semiconductor and AI ecosystems, international financial flows, reserve currency advantages, military security guarantees, and the ability to enforce trade and sanctions policies extraterritorially.

Europe, on the other hand, possesses a vast single market, core industrial competencies, and regulatory power. However, these strengths are only partially translated into strategic leverage. The single market remains fragmented in many areas, such as capital markets, digital services, defense, energy infrastructure, and innovation financing. Furthermore, regulatory strength is no substitute for industrial leadership. Those who set the rules without controlling the leading platforms, chips, cloud systems, or commodity chains ultimately remain in a defensive position. The EU tends toward precisely this pattern: it attempts to regulate foreign power without having built up a corresponding level of counter-power.

Furthermore, there is a difference in the timing of political responses. The US acts more quickly, coherently, and strategically with greater clarity when economic advantages or geopolitical interests are at stake. The EU, on the other hand, must coordinate the interests of 27 member states, differing budgetary situations, divergent industrial structures, and national election cycles. In practice, this means that while Washington uses pressure immediately, Brussels often reacts late, in stages, and with a focus on compromise. It is precisely this slowness that makes Europe predictable and therefore exploitable from the perspective of a strategically acting partner.

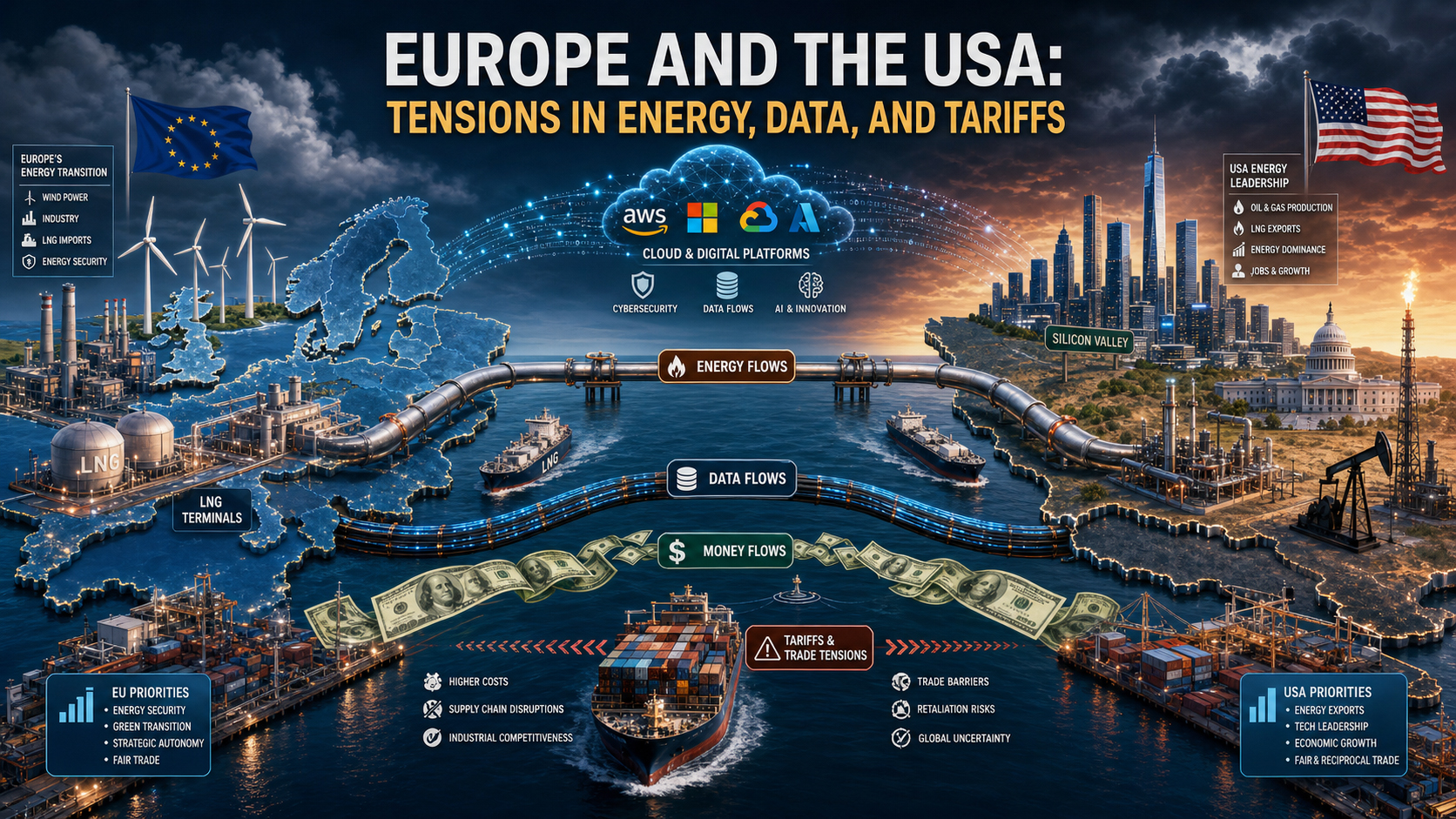

Energy policy: From Russian to American dependence

Few areas illustrate this new asymmetry as clearly as energy policy. After the break in Russian gas supplies, Europe had to quickly find replacements. Liquefied natural gas (LNG) from the US became a central pillar of European energy security. In the short term, this was rational and often the only option. Without additional LNG deliveries, the risk of supply shortages, price shocks, and production shutdowns in parts of Europe would have been considerably greater. In this sense, the US not only profited but also filled a functional gap.

But this very crisis aid has created a new structural vulnerability. Energy is not merely a commodity, but a strategic production factor. Whoever supplies Europe's industry with expensive liquefied natural gas (LNG) influences not only heating costs and electricity prices, but also investment decisions, location calculations, and the international cost position of energy-intensive sectors. US energy exporters benefit from persistently high European demand, while European companies suffer from higher energy prices than many of their US competitors. This disparity is particularly pronounced in the chemical, basic materials, metal processing, fertilizer production, glass manufacturing, and parts of the logistics sector.

The economic implications run deeper than the question of individual gas prices. Europe's industrial policy model has long relied on a combination of technological expertise, skilled workers, infrastructure quality, and a comparatively competitive energy supply. This model has been damaged. If energy remains more expensive than in the US for years, not only will operating costs rise, but investments, research capacities, and production chains will shift. What appears today as a temporary disadvantage could lead tomorrow to permanent deindustrialization or at least to the relocation of important value-added stages. In this sense, the new LNG dependency is not merely a procurement issue, but a structural problem in industrial economics.

Added to this is the power-political leverage. In this relationship, the US is not only a supplier of energy but also Europe's security anchor. This dual role alters every negotiation. When the same partner provides military protection, foreign policy leadership, and crucial energy exports, Europe incurs implicit loyalty costs. Even in the absence of formal blackmail, the possibility of asymmetric countermeasures shapes the behavior of the weaker side. Strategically relevant is not only what is actually threatened, but also what is conceivable and therefore anticipated. In such situations, Europe avoids confrontations that a more autonomous actor would be more likely to risk.

This does not mean that Europe should forgo US LNG. Rather, the realistic conclusion is that an energy partnership without a diversification strategy leads to a new form of dependency. Those who withdraw from a geopolitically motivated monopoly only to enter into another have not addressed the core of the problem. Europe's task, therefore, is not to morally question American deliveries, but to systematically reduce its own vulnerability through more sources of supply, greater storage capacity, improved grids, stronger electricity integration, an accelerated expansion of flexible generation, and a technology-neutral industrial policy.

Digital value creation: Europe regulates, America profits

The asymmetry in the digital sphere is even more pronounced than in energy policy. The US dominates the digital infrastructures, platforms, operating systems, cloud architectures, software standards, and AI ecosystems upon which a growing share of European value creation is built. Europe is not a technological no-man's-land in this system, but in strategically crucial areas, it is often a customer, not a supplier. This distribution of roles has immense economic consequences because digital markets tend toward high returns to scale, network effects, and winner-takes-most dynamics. Those who set standards early and scale globally occupy markets permanently. Those who regulate later can limit abuse, but can hardly change the fundamental value creation architecture.

The EU has primarily responded to this situation with regulation. The General Data Protection Regulation (GDPR), the Digital Markets Act, the Digital Services Act, and the AI Act demonstrate that Europe certainly possesses normative and regulatory influence. However, this strength is ambivalent. On the one hand, it protects citizens, competition, and the rule of law. On the other hand, it masks an industrial policy weakness: Europe primarily regulates companies that are predominantly not based in Europe. As a result, profits, data returns, economies of scale, and capital market effects continue to flow largely to the USA. Europe bears the regulatory burden, market liberalization risks, and adaptation costs, while American corporations continue to siphon off the crucial digital rents despite penalties and restrictions.

This is particularly critical for cloud and data infrastructures. Companies, public administrations, research institutions, and increasingly also industrial control and analysis processes in Europe run on systems from US-dominated providers. This does not automatically mean a loss of control in every single case. However, it does mean a structural dependency in a layer that is central to future productivity. Those who have only limited control over data storage, computing power, developer ecosystems, and AI tools will lose sovereignty in innovation, cybersecurity, business models, and the industrial upgrading of digital processes in the medium and long term.

This dependency generates several economic effects simultaneously. First, license, subscription, consulting, and platform revenues regularly flow out of Europe. Second, market power shifts to those ecosystems that control the interfaces between companies, customers, and data. Third, economies of scale in favor of American providers are amplified because European demand further finances their global dominance. Fourth, lock-in effects emerge: the more deeply European companies are integrated into US clouds, software stacks, and AI tools, the more expensive a later switch becomes. From a company perspective, this is often rational, but from a broader European perspective, it is problematic.

The real strategic point is this: In digital policy, Europe too often confuses consumer protection with sovereignty. Protection is important, but it doesn't replace an industrial counter-model. A continent can protect its citizens from market power and simultaneously remain economically dependent on that very market power. This is precisely the EU's paradoxical situation. It is strong in regulation but weak in platforms; visible in its norms but weak in capital markets; sensitive to data but dependent on infrastructure. The US is exploiting this situation not illegitimately, but systemically. They own the companies that Europe needs, and Europe has so far failed to build enough of the companies that the US, conversely, needs.

Trade and customs policy: Market opening on a European level, power politics on an American level

In goods trade, the transatlantic relationship appears less one-sided at first glance. For many years, the EU has enjoyed a significant trade surplus with the US. Germany, in particular, has benefited disproportionately from access to the US market, especially in the automotive, mechanical engineering, chemical, pharmaceutical, and high-value industrial goods sectors. Therefore, someone focusing solely on goods trade might argue that Europe is not a victim of American dominance, but rather a winner in this relationship.

This view, however, is incomplete. First, the trade surplus in goods is only one part of the overall relationship. In the services sector, particularly in digital services, intellectual property, software, platforms, and financial services, the balance is significantly more favorable for the US. Second, the central question is not simply who achieves what balance in an annual statistic, but who sets the rules of the game. This is precisely where the power imbalance lies. In recent years, the US has repeatedly demonstrated its ability to strategically combine tariffs, threats of sanctions, subsidy regimes, and security policy arguments to exert economic pressure on its partners.

The European response to this often remains defensive. Firstly, because individual member states have different levels of exposure. Secondly, because the EU is understandably reluctant to escalate tensions. An export-oriented economic system suffers particularly from trade wars. But this restraint comes at a price: it signals predictability without deterrence. If Washington knows that Brussels will only retaliate in a limited way or with considerable delay, the balance of power in negotiations shifts. Then even a formally cooperative relationship becomes characterized by an implicit imbalance.

This is particularly evident in sectors with high political symbolic value. Automobiles, steel, aluminum, semiconductors, and green industries are not merely commodities, but sectors of power. The US protects and promotes these sectors with a directness that was long foreign to Europe. Programs like the Inflation Reduction Act have demonstrated how effectively tax incentives, subsidies, local content requirements, and predictable investment conditions can attract capital. Europe responded with debates about state aid law, exemptions, and European funds—in other words, once again more slowly and with greater complexity. For investors, the signal is clear: The US acts strategically in a unified manner, while Europe reacts in a rules-based and fragmented way.

This is particularly critical for Germany. For decades, the German model has been geared towards open markets, stable rules, and a high degree of international division of labor. However, when the global economy becomes increasingly shaped by industrial power politics, a model based on reciprocal rules loses its robustness, especially as key partners increasingly act selectively according to their own national strategies. Openness then turns from an advantage into a risk if it is not combined with domestic mechanisms for protection, support, and response.

Our US expertise in business development, sales and marketing

Our US expertise in business development, sales and marketing - Image: Xpert.Digital

Industry focus areas: B2B, digitalization (from AI to XR), mechanical engineering, logistics, renewable energies and industry

More information here:

A thematic hub offering insights and expertise:

- Knowledge platform covering global and regional economies, innovation and industry-specific trends

- A collection of analyses, insights, and background information from our key areas of focus

- A place for expertise and information on current developments in business and technology

- A hub for companies seeking information on markets, digitalization, and industry innovations

Dollar and Power: How the US Financial Order Weakens Europe

Financial power and the dollar order: The silent return of American dominance

Countervailing power instead of decoupling: A realpolitik plan for Europe

Perhaps the least visible, but economically most profound, asymmetry lies in the financial architecture. With the dollar, the US possesses the world's central reserve and settlement currency. This gives them advantages that extend far beyond foreign trade. They can more easily finance deficits, issue government bonds on a large scale, attract capital from around the world, and conduct their monetary policy with global reach. The consequences of American interest rate decisions, dollar movements, and financial sanctions are felt worldwide, including in Europe. Conversely, Europe's ability to exert similar leverage against the US is very limited.

This financial power generates a kind of structural additional return for the US. International investors, including those from Europe, help finance American deficits because US Treasury bonds are considered a safe haven and the depth of the American capital market is virtually unrivaled. The US thus benefits from a confidence premium that translates into lower financing costs, greater investment flexibility, and increased resilience to crises. Europe, on the other hand, while possessing substantial savings, lacks a similarly integrated and attractive capital market. Consequently, capital from Europe often finds its way into American assets, companies, and innovation ecosystems, rather than flowing into European scaling, infrastructure, or technological sovereignty.

This poses a double problem for the EU. First, it lacks a fully developed capital markets union that could channel private savings more efficiently into productive European investments. Second, the dominance of American financial markets intensifies the pull in favor of the US. Young European growth companies often find it easier to secure large funding rounds, higher valuations, and a more liquid exit market there. This is not a minor detail, but a core issue of strategic competitiveness. Research alone cannot create industrial leadership if scaling capital, anchor investors, and stock market depth are concentrated in other jurisdictions.

The dollar system also functions as a geopolitical instrument. Sanctions, payment restrictions, and the indirect coercion to comply with US rules also affect European companies. Even if Europe had different political preferences, its companies are often effectively forced to adapt to the framework of American financial power. Strategically speaking, this is a restriction of European sovereignty that goes far deeper than a single trade dispute. It concerns the question of who, in a crisis, can define the freedom of action for economic actors.

Security as an economic lever

The US military role in protecting Europe cannot be separated from economic analysis. Security is not an external framework for the economy, but rather a factor of production itself. Supply chains, investments, energy infrastructure, sea lanes, and financial flows all depend on stability. As long as the US provides the crucial portion of nuclear deterrence, vital intelligence capabilities, strategic projection, and logistical support within the transatlantic alliance, Washington inevitably wields considerable indirect influence over Europe's room for maneuver.

This doesn't mean the US threatens Europe with security withdrawal on a daily basis. Power often operates more subtly. The mere expectation that security policy disruptions would massively increase economic costs disciplines political options. If Europe knows that an open break with Washington on trade, technology, or security issues triggers high risks, its willingness to confront decreases. This is precisely how security becomes an economic lever, even without an explicit link in every single issue.

The result is a classic junior partner problem. Europe can speak in terms of strategic autonomy, but in core areas remains bound to a guarantor of security whose economic policy decisions it cannot control. This does not diminish the real value of American security guarantees. However, it explains why Europe often acts less autonomously than its economic size would suggest. A country that relies on protection negotiates differently economically than a completely independent power.

This dimension is particularly sensitive in Germany. For decades, the Federal Republic has benefited enormously from the American security architecture. This enabled restraint in domestic defense spending and a strongly export-oriented economic model. With the return of hard geopolitics, this comfortable situation will become more expensive. Europe must now simultaneously invest more in security, bear higher energy costs, manage digital dependencies, and secure its industrial competitiveness. In this situation, the US has the advantage that Europe can hardly postpone many of these burdens under the pressure of external uncertainty.

The underlying cause of the problem: Europe's own design flaws

However justified the criticism of the US's asymmetric advantages may be, it would be wrong to externalize the responsibility to Washington. The deeper cause lies in Europe's incomplete integration and its strategic inconsistency. The EU is an economic giant, but in key areas of the future, it is not a unified power actor. This applies to energy, defense, capital markets, data spaces, innovation promotion, securing raw materials, and industrial scaling. Progress has been made in all these areas, but there is no sufficiently robust overall architecture.

A key problem is the discrepancy between the size of the single market and political fragmentation. Europe possesses sufficient demand, talent, capital, and industrial expertise to be a global leader in significantly more sectors. However, national regulations, differing tax systems, heterogeneous funding landscapes, fragmented capital markets, and lengthy approval processes often prevent this strength from being fully realized. The result is a paradoxical situation: Europe succeeds in formulating complex rules for global companies, but not to the same extent in creating its own large corporations in future-oriented sectors.

Another problem is the cultural separation of competition and industrial policy. Europe has long prided itself on organizing markets in an open, competitive, and legally secure manner. This remains a major competitive advantage. However, in a world where states are once again actively projecting industrial power, this is no longer sufficient. When other actors support their companies with capital market advantages, strategic procurement programs, energy policies, tax incentives, and geopolitical backing, then strict adherence to rules is no longer an ideal of neutrality, but potentially a disadvantage. Europe recognized this shift late and often reacts half-heartedly to this day.

Ultimately, what is lacking is a convincing political narrative that explains economic sovereignty not as isolationism, but as a prerequisite for open action. Many European debates oscillate between market romanticism and fantasies of autarky. Neither is helpful. Strategic sovereignty means neither protectionism for its own sake nor the illusion of complete independence. It means not being vulnerable to blackmail in critical sectors and possessing one's own choices in key areas of the future. European policy should be guided precisely by this definition.

Germany's particular vulnerability

Germany is at the heart of this problem. Hardly any other large EU country is simultaneously so export-oriented, so energy-intensively industrialized, so deeply embedded in security policy, and so heavily dependent on international value chains. The German business model was extraordinarily successful under the conditions of the old globalization. It combined relatively inexpensive energy, high product quality, technical specialization, global sales markets, and stable geopolitical integration. Several of these prerequisites have since eroded.

Access to the US market remains essential for Germany. At the same time, its vulnerability to American tariff decisions, industrial policy incentives, and currency fluctuations is increasing. Added to this is the technological dependence on US platforms and cloud systems, which now also affects medium-sized industrial companies. What once seemed purely an issue for the internet economy now extends deep into production control, data analysis, sales, marketing, collaboration, and AI applications. German SMEs frequently use American tools without this necessarily creating a problem at the company level. However, at a systemic level, this adds up to a loss of digital independence.

The combination of energy price disadvantages and investment competition is particularly problematic. When companies choose between a highly subsidized, energy-cheaper, and more capital market-oriented US location and a regulatory-complex European environment, incentives shift. Even if only individual investments relocate, this sends signals to entire industries. For Germany, the danger lies less in an abrupt industrial collapse than in a gradual erosion: fewer new business locations, lower reinvestments, more cautious scaling, slower digitalization, and a gradual loss of vertical integration.

Precisely for this reason, it is insufficient to interpret the transatlantic relationship categorically as a threat or an alliance without alternatives. Germany must learn to deal with the US simultaneously as a partner, competitor, and center of power. This multifaceted role demands more strategic pragmatism than the German debate often allows. Economic policy can no longer assume that open markets automatically produce fair outcomes. In a geopolitically charged economy, those actors who consistently combine economic, technological, and security policy levers often prevail.

Recommendations for action for Europe and Germany

This diagnosis does not lead to an anti-American agenda, but rather to a strategy of risk reduction and counter-power development. Europe does not need to be defined in opposition to the US, but it must be able to represent its own interests independently, even when these interests do not align with those of Washington. Several priorities are crucial for this.

First, Europe needs a realistic energy and industrial base. This includes diversified gas sources, a more robust electricity infrastructure, accelerated permitting processes, flexible reserve capacities, increased storage, and an industrial energy policy that considers security of supply and competitiveness together. Expanding renewable energy remains crucial, but it is not enough on its own if grids, storage facilities, backup capacities, and industry-friendly electricity prices do not grow accordingly.

Secondly, the EU must expand its digital policy to include a genuine infrastructure dimension. Regulation remains necessary, but it must be complemented by building European cloud and computing capacities, interoperable data spaces, sovereign AI models, public procurement for European technologies, and better financing for scaling. Not every digital service needs to originate in Europe. But persistent one-sidedness in critical sectors must not become the accepted norm.

Thirdly, Europe urgently needs deeper capital markets. A functioning capital markets union is not a technical side issue, but a prerequisite for strategic competitiveness. If European savings systematically migrate to non-European investment regions, the capital needed for domestic innovation leaps will be lacking. More venture capital, better exit opportunities, less regulatory fragmentation, and stronger institutional investors would help transform research into marketable products.

Fourth, trade policy must become more resilient. Open markets remain in Europe's interest, but openness without reciprocity is naive. Europe should more consistently employ instruments for a swift response to economic pressure, discriminatory subsidies, and extraterritorial coercion. The goal is not escalation, but credibility. Those who can never credibly retaliate practically invite their power-political partners to test the limits.

Fifth, burden-sharing in security policy is also economic policy. A Europe that invests more in its own defense capabilities, the resilience of critical infrastructure, and security technology expertise not only strengthens its military position but also expands its economic bargaining power. Strategic autonomy begins not with grand pronouncements but with real capabilities.

Sixth, Germany needs a more active role as an industrial policy coordinator within Europe. The Federal Republic should not only balance its interests bilaterally with Washington, but should instead forge targeted European coalitions for energy, digitalization, procurement, capital market integration, and industrial standards. The biggest mistake would be to pursue national go-it-alone approaches, especially since the structural asymmetry results precisely from European fragmentation.

Strategic classification

The US does not disproportionately exploit Europe because it unfairly operates outside the rules. It does so because it systematically translates its strengths as a power center of a large economy, a dominant technology sector, a leading currency, a deep capital market, and a guarantor of security into economic advantages. For too long, Europe has countered this with a mixture of normative self-assurance, regulatory platitudes, and strategic slowness. This combination is the root cause of Europe's weakness.

Anyone who concludes from this that Europe must decouple from the US is drawing the wrong conclusion. Equally wrong would be the opposite assertion, that the existing asymmetries are merely an expression of efficient division of labor. The truth is rather this: the transatlantic partnership remains indispensable for Europe, but it will only remain viable if it becomes less one-sided. Partnership without a counterweight inevitably leads to dependency in the long run. And while dependency may provide stability in times of crisis, in the long term it increases the cost of growth, innovation, and political maneuvering.

Europe faces a strategic decision. It can accept the new asymmetry in its relationship with the US as an inevitable consequence of geopolitical uncertainty and limit itself to mitigating the damage. Or it can understand the current situation as a wake-up call to finally develop the economic, technological, and security capabilities that will transform the partnership back into a relationship of near-equal balance. From an economic perspective, everything points to the second option.

The crucial insight is this: The problem is not American strength. The problem is European strength, which is too rarely organized strategically. As long as Europe fails to translate its market size, industrial base, scientific expertise, and savings more effectively into its own power resources, it will remain an indispensable partner for the US, but also a space from which disproportionate returns, influence, and strategic advantages can be extracted. Anyone who wants to change this dynamic doesn't need to think anti-American. They need to finally start thinking strategically in a European way.

Your global marketing and business development partner

☑️ Our business language is English or German

☑️ NEW: Correspondence in your native language!

Konrad Wolfenstein

I and my team are happy to be available to you as your personal advisor.

You can contact me by filling out the contact form here [email protected]:or simply call me at +49 7348 4088 965. My email address is

I'm looking forward to our joint project.

☑️ SME support in strategy, consulting, planning and implementation

☑️ Creation or realignment of the digital strategy and digitization

☑️ Expansion and optimization of international sales processes

☑️ Global & Digital B2B trading platforms

☑️ Pioneer Business Development / Marketing / PR / Trade Fairs

🎯🎯🎯 Data-driven B2B industry hub as a quasi-in-house solution

The quasi-in-house solution: How Xpert.Digital closes operational gaps in B2B marketing and sales – Smart Content-Driven Business - Image: Xpert.Digital

Xpert.Digital is a data-driven B2B industry hub led by Konrad Wolfenstein . The company acts as an external, quasi-in-house solution for industrial partners, closing operational gaps in marketing, content, and sales – without requiring additional resources on the client side.

More information here: