Container shock 2.0: and exploding freight rates: How the Middle East conflict is making everything more expensive

Xpert Pre-Release

Available in 27 languages 📢

Prefer Xpert.Digital on GoogleⓘPublished on: April 2, 2026 / Updated on: April 2, 2026 – Author: Konrad Wolfenstein

Container shock 2.0: and exploding freight rates: How the Middle East conflict is making everything more expensive – Image: Xpert.Digital

Trump, Iran and sea freight: A highly dangerous mix for the economy

The end of "just-in-time": Why companies are now radically restructuring their logistics

Record fleet meets chaos: The price paradox of global shipping

Global shipping is currently a geopolitical powder keg. Just as international supply chains seemed to have stabilized after the historic turmoil of the Covid years, the next massive shock is already rolling through the global economy. The escalating Middle East conflict, ongoing Houthi attacks in the Red Sea, and geopolitical rhetoric are effectively transforming the Bab al-Mandab strait into a highly dangerous restricted zone. The dramatic consequence: thousands of container ships are forced to take the weeks-long detour around the Cape of Good Hope. Transit times are exploding, containers are piling up in the wrong places, and freight rates are skyrocketing. This reveals a dangerous paradox: although more ships than ever before are in operation worldwide, there is suddenly an acute shortage of capacity. Sea freight costs are no longer simply the result of supply and demand – they have become an incorruptible, real-time seismograph of a vulnerable, globalized world. For businesses, consumers, and the already fragile inflation trend, this means: Anyone still hoping for "business as usual" has not understood the seriousness of the situation.

Freight rates in crisis mode: How the new Middle East conflict is shaking up the global maritime economy

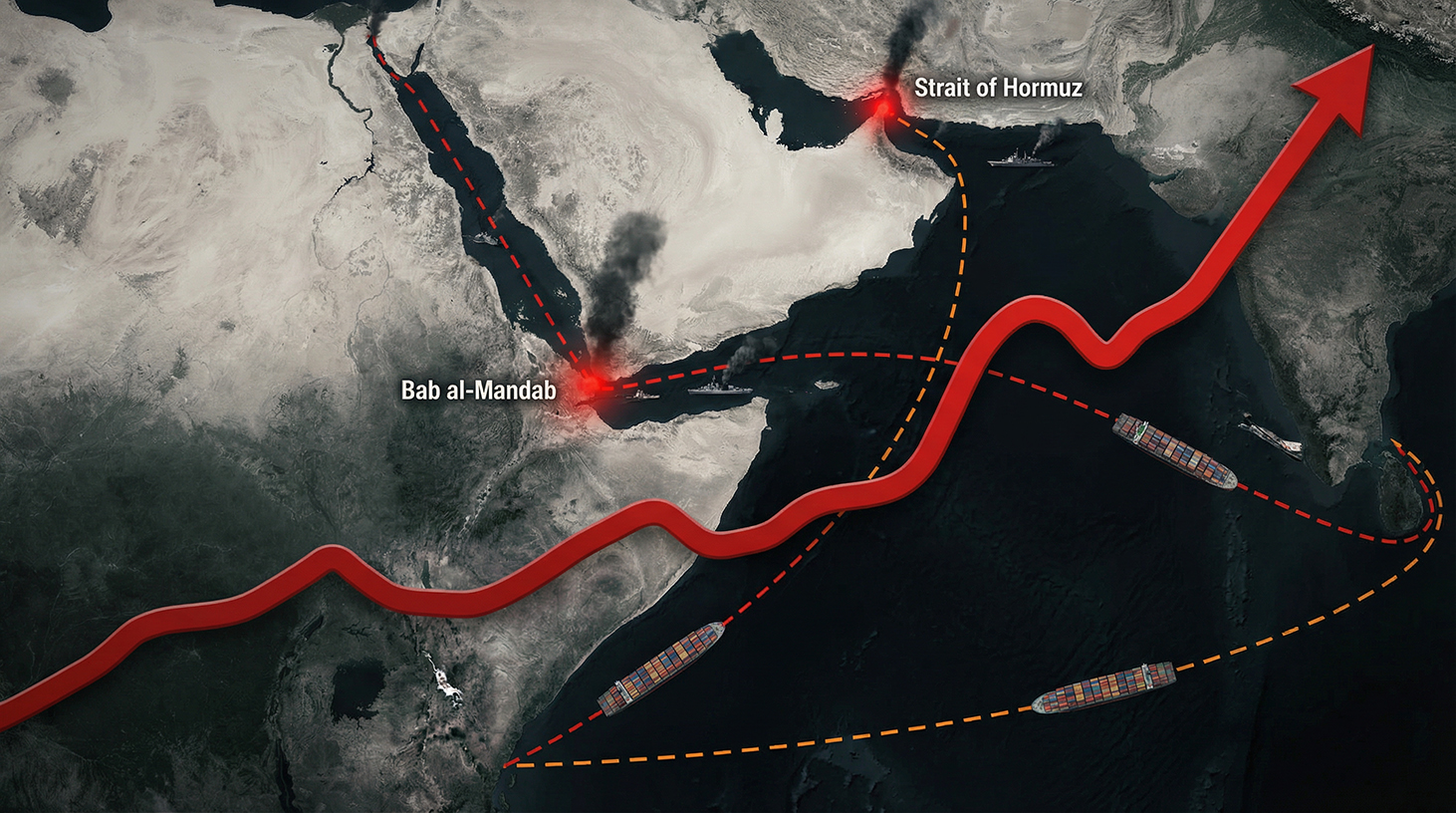

1. A new bottleneck of globalization: Why Bab al-Mandab has suddenly become a key issue in global economic policy

There are moments when abstract geography suddenly becomes harsh reality for economies, businesses, and consumers. Bab al-Mandab, the narrow strait only about 30 kilometers wide between Yemen on the Arabian Peninsula and Djibouti or Eritrea in Africa, is precisely such a point. This passage connects the Red Sea with the Gulf of Aden – and thus the route from the Mediterranean via the Suez Canal towards the Indian Ocean and the Far East. A significant portion of global container and oil tanker traffic travels along this route, including supply chains to Europe and large parts of Africa.

With the Iran-Iraq War, the escalating Houthi attacks on merchant ships in the Red Sea, and the growing threat of Bab al-Mandab becoming a de facto temporary exclusion zone, this crucial waterway has moved into the spotlight of geopolitical attention. Initial Houthi missile attacks on Israel, threats to block shipping, and the expansion of hostilities at sea have transformed a regional escalation into a global supply chain crisis. While the Strait of Hormuz has been recognized as a strategic hotspot for decades, Bab al-Mandab is now emerging as Iran's "second waterway"—and thus as another lever to exert pressure on the global economy.

For shipping companies, shippers, and national economies, this means increased uncertainty, significantly longer transit times, and a sharp rise in freight rates. Any serious threat to the route through the Suez, Red Sea, and Bab al-Mandab straits forces carriers to divert ships extensively – usually around the Cape of Good Hope in southern Africa. This lengthens the Asia-Europe sea route by up to two weeks, consumes additional bunkering budgets, and ties up ship and container capacity.

2. Trump, Kharg Island and the escalation spiral: How political threats drive freight rates

In this already tense situation, political statements act as catalysts. When US President Donald Trump publicly threatens to "bomb Iran back to the Stone Age" and explicitly targets the Iranian oil hub of Kharg Island, it abruptly shifts the risk perception of market participants. Kharg Island is the most important export port for Iranian crude oil; an attack on this island, or even just a credible threat, increases the risk of a counter-reaction from Tehran – for example, in the form of a blockade of the Strait of Hormuz or indirectly through actors allied with Iran, such as the Houthis in Yemen.

Market participants in maritime transport react to such signals much faster than traditional political processes would suggest. Shipping companies adjust routes, insurers add risk premiums, charter rates rise, and shippers begin to secure capacity as a precaution. This dynamic often drives up freight rates even before actual military action. This is precisely what can be observed in the current Iran crisis: even before a complete blockade of Hormuz or Bab al-Mandab occurs, the risks are reflected in surcharges on sea freight prices.

This has two economic effects. First, direct transport costs increase for companies whose supply chains run through these regions. Second, the volatility of rates increases, making planning and calculation more difficult. For many importers and exporters, logistics costs thus become a kind of political risk premium – in addition to energy prices, interest rates, and currency fluctuations. In short, freight rates are no longer just an expression of supply and demand in the container capacity markets, but increasingly an early indicator of geopolitical tensions.

3. From oversupply to scarcity: How the post-Covid surplus is turning into a new capacity crisis

Just a few years ago, the world of container shipping looked completely different. Following the Covid boom of 2020/2021, massive fleet orders were placed to profit from the then exorbitantly high rates. As demand normalized, a persistent oversupply of shipping capacity threatened from 2023/2024 onwards, significantly driving down freight rates. Shipping companies faced shrinking margins, overcapacity, and, in some cases, falling charter rates.

The current escalation in the Middle East, and especially the situation in the Red Sea, has reversed this picture in just a few months. Detours around the Cape of Good Hope lengthen shipping routes, shift turnaround times, and thus drain available capacity from the market. Even if the nominally global container fleet continues to grow, a significant portion of this capacity is no longer available to the market to the same extent because ships are at sea for longer periods and the same transport volumes require more ship and container time.

The effect is paradoxical: A record fleet meets chaotic routes – and instead of falling prices, shippers experience rising rates and recurring bottlenecks in slot availability on certain trade lanes. Traffic between Asia and Europe is particularly affected, but routes from the Middle East to Europe and North America are also feeling the scarcity. At the same time, disruptions are occurring in the global repositioning of empty containers because established flow patterns are disrupted. This can lead to temporary undersupply at European ports, while elsewhere containers are plentiful but, due to route changes, cannot reach their destinations in time.

4. What's happening at the ports: congestion, slot shortages, and operational uncertainty

The geopolitical crisis is manifesting itself not only in abstract price indices, but very concretely at the quays of major container ports. Diverted ships are arriving in European and Asian ports in a concentrated period, leading to temporary peak loads. While previously there was a relatively stable schedule throughout the year, there are now more frequent waves of ship arrivals followed by periods of low capacity. This irregularity complicates operational planning for port operators, terminal service providers, and hinterland transport companies.

For freight forwarders and shippers, this means: a shortage of slots on inland waterway vessels, overloaded rail connections, and bottlenecks in truck capacity in the port hinterland. Every delay in the unloading and loading process is compounded in the supply chain. A one-day delay at sea can cause a two- or three-day delay in downstream transport if the planned train or truck schedules can no longer be maintained. This not only increases direct transport costs but also indirect costs due to inventory build-up, safety stocks, and penalties for late delivery.

Added to this is the need to mitigate operational risks. Shipping companies and terminals are strengthening security measures and coordinating more closely with naval operations and international missions to protect merchant shipping. This security architecture incurs additional costs, which are ultimately also reflected in freight rates. At the same time, port operators must adapt to short-notice route decisions by carriers: If a ship decides to sail through the Red Sea after all or is rerouted to the Cape route at short notice, arrival times, berth assignments, and shift schedules can change within a few days.

5. Freight rates on the rise: figures, trends and price peaks

Specific freight rates are highly volatile depending on the route and time, but the trend is clear: Since the escalation in the Red Sea and the increasing threat to Bab al-Mandab, the indices for container freight from Asia to Europe, as well as on some transatlantic routes, show a clear upward trend. After a period of relatively low rates due to excess capacity, rates have reached a level in many routes that, while still below the historical peaks seen during the Covid pandemic, is already noticeably painful for many importers and exporters.

Spot rates, in particular, have risen sharply, while longer-term contracts have sometimes been limited in time or include escalation clauses. Shippers who rely heavily on spot bookings often currently pay a significant risk premium, while companies with proactively negotiated annual contracts still benefit from more favorable conditions – provided their contractual partners do not invoke force majeure or hardship clauses.

In parallel, insurance premiums for war zones and high-risk areas are rising in certain regions. This is particularly true for ships that continue to navigate the Red Sea and the Strait of Hormuz. These additional costs are often passed on to shippers, directly or indirectly. Freight rates are thus increasingly taking on a dual function: they reflect not only transport costs but also geopolitical risk premiums. For many companies, logistics costs are becoming a variable factor, more dependent on foreign policy developments than on their own planning.

6. Energy, inflation, consumption: How sea freight rates impact the real economy

Sea freight is the backbone of global trade. A significant proportion of globally traded goods – from everyday products to machinery and electronics, and even raw materials – are transported by ship. Rising freight rates therefore act like an invisible tax surcharge on international trade. The higher the transport costs, the greater the pressure on producers, retailers, and ultimately, consumer prices.

Goods with a low value per unit volume, such as mass-produced goods, textiles, or simple consumer goods, are particularly sensitive to price fluctuations. Here, transport costs represent a comparatively high percentage of the final price. If sea freight for a container becomes significantly more expensive, this cannot be absorbed into margins for such products without impacting profit margins. Manufacturers and retailers are then faced with a choice: raise prices, adjust product ranges, or reduce the flow of certain goods. As a consequence, the range of products available in stores can decrease, while certain product groups become more expensive.

Another factor is energy prices. An escalation surrounding Kharg Island and a potential disruption to Iranian oil exports would have a direct impact on oil and, consequently, fuel prices. Higher bunker prices immediately affect the operating costs of shipping companies, which in turn respond with fuel surcharges (BAF – Bunker Adjustment Factor). These surcharges are added to the base freight rates and can have a significant impact during sharp price fluctuations.

Rising sea freight rates and energy prices thus act as a dual driver of inflation. Firstly, through higher production and logistics costs, and secondly, through increased energy costs in industry, transportation, and private households. This makes it more difficult for central banks and fiscal policymakers to stabilize inflation expectations, especially since geopolitical shocks are difficult to predict and cannot be neutralized by traditional monetary policy instruments.

7. Supply chains under stress: From just-in-time to risk management

The current crisis is yet another blow to the just-in-time supply chain model, perfected over decades. The Covid pandemic and the Suez Canal congestion caused by the Ever Given had already demonstrated the vulnerability of highly optimized supply chains geared towards minimal inventory levels. The now persistent threat along key maritime trade routes is forcing companies to fundamentally rethink their logistics strategies.

A key trend is the return to higher safety stock levels. Instead of relying on minimal inventory, many companies are again building up buffer stocks to protect themselves against delays at sea. This ties up capital, increases storage costs, and requires more professional forecasting and inventory management systems. At the same time, the geographical diversification of suppliers is becoming more important: companies are trying to reduce dependence on individual regions or transit routes by developing alternative sources of supply in other parts of the world.

Another area of adaptation concerns contract design with logistics service providers. Where previously pure price orientation dominated, the resilience component is now moving more into the foreground. Companies are paying closer attention to capacity commitments, flexibility clauses, alternative routes, and service-level agreements that guarantee a certain level of transport capability even in crisis situations. For shipping companies and freight forwarders, this means that they are no longer perceived solely as capacity providers, but increasingly as partners in joint risk management.

Your container high-bay warehouse and container terminal experts

Container high-bay warehouses and container terminals: The logistical interplay – expert advice and solutions - Creative image: Xpert.Digital

This innovative technology promises to fundamentally change container logistics. Instead of stacking containers horizontally as before, they will be stored vertically in multi-story steel racking structures. This not only allows for a drastic increase in storage capacity within the same area, but also revolutionizes all processes at the container terminal.

More information here:

Who really benefits from the freight rate boom? A look at the winners and losers

8. Power shifts in the shipping market: Who benefits from the crisis – and who doesn't?

Rising freight rates appear at first glance to be an advantage for shipping companies. Those offering cargo space can command higher prices and improve their profits. However, the reality is more complex. Large liner shipping companies with global networks, strong capital bases, and considerable negotiating power with shippers are undoubtedly in a position of relative strength. They can adjust routes more flexibly, have easier access to insurance and naval escorts, and better opportunities to pass on additional costs through their pricing.

Smaller carriers or niche providers, on the other hand, are finding it more difficult. Their insurance and financing costs are rising disproportionately, and they often lack the same flexibility in fleet management. In some segments, market concentration could therefore increase further, because only financially robust providers are able to survive prolonged periods of crisis. For shippers, this poses the risk of a shrinking competitive landscape, which could strengthen the negotiating power of shipping companies in the long term.

Alliances and partnerships between shipping companies are also gaining importance. Joint route planning, slot sharing, and coordinated capacity management allow for the sharing of risks and costs. Nevertheless, the market remains subject to strong cyclical fluctuations: A relaxation of the geopolitical situation could put freight rates under renewed pressure within months and bring the issue of overcapacity back onto the agenda. This makes it more difficult for investors and corporate strategists to develop reliable long-term scenarios for the profitability of the ocean freight industry.

9. Political responses: Naval presence, sanctions and trade agreements

The threat to sea lanes in the Middle East is no longer just a concern for shipping companies and insurers, but a matter of international politics. Several states and alliances have deployed naval forces to the region to protect merchant ships, repel attacks, and prevent escalation toward complete blockades. This military presence is costly, but many governments consider it necessary to safeguard the functioning of global trade.

In parallel, a political debate is underway regarding sanctions, embargoes, and potential negotiations with Iran and other actors in the region. Trump's threats against Tehran, particularly concerning Kharg Island, are increasing the pressure on European and Asian states to define their own position: Should they adopt a hard line or pursue de-escalation and diplomatic channels to ensure the security of maritime lanes?

At the trade policy level, the current situation is also being used as an argument to promote the diversification of trade flows. Regional trade agreements that encourage nearshoring and friendshoring are gaining in attractiveness. As geopolitical tensions increase at critical sea lanes, the incentive to move production and procurement structures closer to sales markets in order to reduce dependence on a few routes grows. This trend is not short-term crisis management, but could change the architecture of global trade in the long term.

10. Europe in the crosshairs: Particular vulnerability due to Suez, the Red Sea and Hormuz

Europe is particularly affected by current developments. A large proportion of imports from Asia – from consumer goods and components to industrial intermediates – arrive via the Suez Canal and the Red Sea. Alternative routes via the Cape of Good Hope not only significantly increase transit times but also shift the cost structure. For Europe's export-oriented economies, this is a double burden: they suffer both as importers of intermediate goods and as exporters whose products lose competitiveness due to higher logistics costs.

Large port cities like Rotterdam, Antwerp-Bruges, Hamburg, and other North and Baltic Sea ports, which serve as hubs for the European single market, are particularly vulnerable. Disruptions in maritime transport directly impact hinterland transport by rail, inland waterway, and truck, and can put domestic logistics systems under pressure. For companies in Germany, France, the Benelux countries, and other EU member states, the resilience of their maritime transport chains is therefore becoming a key factor in determining their attractiveness as a business location.

Furthermore, Europe is vulnerable in terms of energy policy. An escalation over Iranian oil exports and the Strait of Hormuz would drive up global oil prices and thus also energy import costs for the EU. This would further weaken the competitive position of European companies, especially since they already face higher energy prices and stricter climate regulations compared to some competitors in North America or parts of Asia.

11. Winners and losers: Who benefits from the current situation

As paradoxical as it may sound, every crisis also creates winners. In the context of rising sea freight rates and unstable shipping lanes, those who can offer alternative logistics solutions or are able to sell additional services related to risk management, consulting, and digital transparency benefit most. Providers of multimodal transport, such as rail-sea freight via alternative routes, can expect increased demand, provided they have sufficient capacity.

Logistics and supply chain consultancies are experiencing increased demand for scenario analyses, resilience strategies, and network optimization. At the same time, providers of digital platforms that offer real-time data on ship movements, delays, and rate trends are gaining importance. Companies are willing to pay for transparent, up-to-date information because it allows them to better inform their decisions regarding orders, inventory management, and transport bookings.

On the other side, however, there are numerous losers. Small and medium-sized importers with limited bargaining power, who rely on spot rates, suffer disproportionately. They often cannot fully pass on rising logistics costs to their customers and see their margins shrink. The same applies to export sectors whose business models depend heavily on price competitiveness. For them, a prolonged period of high sea freight rates can become an existential threat if they do not react in time and adapt their business models.

12. Strategic options for companies: What to do now

Against this backdrop, many companies are faced with the question of how to react to the current situation while simultaneously preparing for future shocks. A short-term "wait and see" strategy is risky given the complex geopolitical landscape. The Iran war, the Houthi attacks in the Red Sea, and the threats against Kharg Island demonstrate that political escalations can quickly impact global markets.

Meaningful strategic areas of action can be categorized into three groups:

First: logistics and supply chain structure. Companies should examine their networks to identify dependencies on individual routes and shipping bottlenecks. Where possible, alternative routes, ports, or modes of transport should be established – even if these appear more expensive in the short term. The option of being able to diversify in a crisis is a kind of insurance premium.

Secondly: Contract policy and partnerships. Instead of focusing solely on the lowest price, shippers should develop more collaborative models with shipping companies, freight forwarders, and logistics providers. This can include long-term capacity guarantees, flexible routing options, or joint investments in digital transparency solutions. Those who act as reliable partners during a crisis have a better chance of securing space on ships in extremely tight markets.

Thirdly: Financial and operational resilience. Higher safety stocks, additional storage capacity, and investments in inventory management and risk management systems help to cushion shocks. At the same time, working capital should be managed in such a way that temporary capital commitments due to inventory build-up can be absorbed. Companies that discuss potential financing needs with their banks early on reduce the risk of later liquidity shortages.

13. Long-term perspective: Will freight rates remain permanently higher?

A key question from a macroeconomic perspective is whether we are at the beginning of a permanently higher freight rate era or whether this is a temporary overreaction that will subside once tensions in the Middle East ease. Historically, ocean freight rates exhibit distinct cycles: periods of extremely high prices have often been followed by long periods of relative weakness, particularly when massive investments were made in fleet expansion during boom times.

At the same time, there are indications that geopolitical risks will remain a persistent variable in the price structure. The increasing rivalry between major powers, regional conflicts, and the strategic importance of energy and commodity routes suggest that maritime bottlenecks such as the Strait of Hormuz and Bab al-Mandab will continue to be a focus of attention. Other potential disruptive factors include extreme weather events, cyberattacks on port and logistics systems, and regulatory interventions related to climate policies.

The most likely outlook is therefore not a linear development, but a pattern of wave-like movements: phases of relative relaxation with moderate rates, followed by abrupt upward spikes during new crises. For companies, this means they must optimize their logistics and procurement strategies for uncertainty, instead of assuming a return to a stable, predictable normal state.

14. The psychological factor: How perception determines prices

Besides hard facts like capacity, route lengths, and insurance premiums, psychology also plays a role. Markets react not only to actual events but also to expectations, rumors, and political signals. The media coverage of threats, such as those made by Trump against Iran, reinforces the feeling of a fragile situation among many market participants. Reactions like panic bookings, overly cautious rerouting, or excessive security requirements can exacerbate actual disruptions and thus drive freight rates even higher.

At the same time, it can be observed that market participants have learned from previous crises. Since Covid, many companies have developed crisis plans, simulated alternative scenarios, and professionalized their information channels. Today, they react in a more nuanced and less reflexive way than they did a few years ago. This can help to cushion extreme price spikes by enabling supply and demand to react more rationally to new information.

However, even a more rational market reaction doesn't change the fact that geopolitical shocks create real price pressure. The psychological factor then acts more as an amplifier or dampener, not as a fundamental trendsetter. For political actors, this means that words should be chosen more carefully – because loud threats can incur real economic costs even before a shot has been fired.

15. Freight rates as a seismograph of a vulnerable global economy

The current development of sea freight rates in the context of the Iran-Iraq War, the threat to Bab al-Mandab and the Strait of Hormuz, and the threats against Kharg Island demonstrates how closely intertwined geopolitics and economics have become. What was once perceived as a distant crisis region now impacts supermarket prices, industrial costs, and inflation rates in developed economies within just a few weeks.

Freight rates act like a seismograph: they spike as soon as tensions increase at strategic points of conflict, signaling where the next tectonic shift in the global economy might occur. Companies that take these signals seriously can develop risk reduction strategies in a timely manner – for example, through diversification, resilience building, and more collaborative relationships with their logistics providers. Those who continue with "business as usual," however, risk being caught off guard by the next wave of rising rates and disrupted supply chains.

From an economic perspective, one thing is clear: the era of extremely cheap, seemingly limitless sea freight is over. This isn't necessarily because capacities are physically limited, but because the political and security dimensions of sea routes have permanently gained in importance. Whether the global economy can manage this transition to "expensive security" depends not only on investments in fleets, ports, and digital systems, but above all on the ability of international politics to limit escalation spirals like the current conflict with Iran. As long as this fails, freight rates will continue to reflect a vulnerable globalization, prone to crises.

Your global marketing and business development partner

☑️ Our business language is English or German

☑️ NEW: Correspondence in your native language!

Konrad Wolfenstein

I and my team are happy to be available to you as your personal advisor.

You can contact me by filling out the contact form here or simply call me at +49 7348 4088 965. My email address is : [email protected]

I'm looking forward to our joint project.

☑️ SME support in strategy, consulting, planning and implementation

☑️ Creation or realignment of the digital strategy and digitization

☑️ Expansion and optimization of international sales processes

☑️ Global & Digital B2B trading platforms

☑️ Pioneer Business Development / Marketing / PR / Trade Fairs

🎯🎯🎯 Data-driven B2B industry hub as a quasi-in-house solution

The quasi-in-house solution: How Xpert.Digital closes operational gaps in B2B marketing and sales – Smart Content-Driven Business - Image: Xpert.Digital

Xpert.Digital is a data-driven B2B industry hub led by Konrad Wolfenstein . The company acts as an external, quasi-in-house solution for industrial partners, closing operational gaps in marketing, content, and sales – without requiring additional resources on the client side.

More information here:

📈🔵 Market knowledge vs. marketing knowledge: Why SMEs block their own growth 💡

Market vs. Marketing Knowledge: Why SMEs Block Their Own Growth - Image: Xpert.Digital

A persistent, pragmatic misconception exists among small and medium-sized enterprises (SMEs): that those who know their customers and the market also know how marketing works. However, this very equation is increasingly becoming a strategic trap for many SMEs.

The following article analyzes the often overlooked tension between operational market knowledge (looking in the rearview mirror) and strategic marketing knowledge (the high beam for future market share). Learn why a sole focus on sales targets leads to interchangeability in the long run and how SMEs can mature from "short-distance runners" to distinctive brands by consciously separating and realigning these two disciplines. Because those who understand marketing merely as "colorful pictures for sales" surrender 95 percent of tomorrow's potential customers to the competition without a fight.

More information here: