Germany's underappreciated superpower: Smart Factory – Why our factories are the best launchpad for the AI future

Xpert Pre-Release

Available in 27 languages 📢

Prefer Xpert.Digital on GoogleⓘPublished on: August 7, 2025 / Updated on: August 7, 2025 – Author: Konrad Wolfenstein

Germany's underappreciated superpower: Smart Factory – Why our factories are the best launchpad for the AI future – Image: Xpert.Digital

California - Germany: Tech giant versus industrial giant – Who will really win the race for the future?

How industrial foundations determine dominance in the digital age – A comparative analysis of Germany and California

### Silicon Valley's Achilles Heel: Why Tech Giants Suddenly Have a Problem Germany Can Solve ### Germany's Industrial Heart as a Data Refinery: The Hidden Strategy for Our Survival in the Tech Race ###

The digital economy—information technology (IT), cloud services, and artificial intelligence (AI)—is fundamentally dependent on a robust physical, manufacturing industrial base for its value creation and monetization. We compare the economic models of Germany, characterized by a strong industrial sector, and California, whose economy is driven by a dominant technology sector. Our article confirms the strategic importance of the industrial foundation but nuances the initial assumption of a one-sided dependency and instead develops a model of profound symbiosis in which both sectors benefit from and are mutually dependent.

The quantitative economic structures of both regions are confirmed: Germany relies on a manufacturing sector that contributes around 18.2% to nominal gross value added, while California's technology sector accounts for 17–19% of gross domestic product (GDP), with a significantly smaller traditional manufacturing sector of about 11%. A crucial finding, however, is the deconstruction of the Californian "tech sector," which reveals that a substantial portion of its value added and employment stems from high-tech manufacturing, particularly in semiconductors, computer hardware, and biomedical engineering. The comparison is therefore less one of "industry versus IT" and more one of "traditional heavy industry versus advanced high-tech industry.".

This article identifies strategic weaknesses in both models. Germany's Achilles' heel is an acute and worsening shortage of skilled IT professionals, which is projected to grow to over 660,000 unfilled positions by 2040. This lack of human capital represents the biggest obstacle to the proclaimed rapid catch-up in the digital sphere. Added to this is a relative lag in venture capital investment. California, on the other hand, faces enormous challenges with its physical infrastructure. The exponentially growing energy and water demands of hyperscale and AI data centers are colliding with an already strained supply network and ambitious climate regulations, creating the risk of bottlenecks and "stranded assets.".

The central strategic conclusion is that Germany and the European Union (EU) possess a unique, yet untapped, advantage. Their dense, highly specialized industrial base is not merely a market for digital services, but a strategic asset—a “data refinery” and “problem laboratory” of inestimable value. It provides the ideal foundation for developing proprietary, domain-specific AI solutions that can outperform generic applications and represent a new, high-margin digital export commodity.

To realize this potential, an aggressive, unified, and well-funded strategy is required. The recommendations focus on three core areas:

- Completion of the digital single market: Radical dismantling of the remaining national barriers to enable European digital companies to scale in a home market of 440 million consumers.

- Human capital offensive: A massive, EU-wide coordinated “Digital Skills Pact” for the retraining, further education and recruitment of IT professionals to overcome the most critical obstacle to growth.

- Promoting industrial-digital ecosystems: Targeted use of policy instruments such as the EU Chips Act to finance deep integration between industrial giants and AI start-ups, thereby accelerating the development of "Industrial-Digital Champions".

Ultimately, the question of whether a factory can survive without the cloud will not determine future economic dominance, but rather which economy most effectively manages the symbiosis between physical production and digital intelligence. For Europe, the opportunity lies in understanding its industrial strength not as a relic of the past, but as an anchor and launching pad for the digital future.

Suitable for:

The symbiotic machine: Deconstruction of the interdependence of physical production and the digital economy

The premise that the digital economy is fundamentally dependent on manufacturing is rooted in a traditional understanding of value creation. While this model captures an important part of economic reality, it falls short of describing the complex, bidirectional relationships that define the 21st century. A deeper analysis reveals not a one-sided dependency, but a symbiotic machine in which the physical and digital worlds are inextricably intertwined and mutually reinforcing.

Rethinking value creation: From supply-side production to demand-side networks

Classical economics, particularly supply-side economics, posits that the production of goods and services is the primary engine of economic growth. In this model, a factory creates value by producing tangible goods. The supply of these goods is the fundamental economic activity that generates demand and creates wealth. This paradigm describes value creation in the industrial age and forms the conceptual basis for the claim that a factory is a more fundamental economic entity than a data center.

The digital economy, however, operates according to a different, complementary logic, one strongly influenced by demand-side principles and, in particular, network effects. Unlike the linear value chain of a factory, the value of a digital platform or service increases exponentially with the number of its users. A social network with one billion users is not only twice as valuable as one with 500 million; its value is many times greater, as the number of potential connections and interactions increases dramatically. This phenomenon creates a self-reinforcing cycle: more users attract more users, making the platform more valuable for everyone and creating extremely strong competitive advantages (so-called "moats"). Digital platforms like Amazon, Google, or Uber create value not primarily through the ownership of physical means of production, but through the orchestration of networks and the facilitation of transactions between different user groups. Here, the user base itself—the demand side—becomes the most valuable asset.

The comparison of these two models reveals a false dichotomy. The most successful economic models of our time are hybrid in nature. Digital services generate their enormous value creation through demand-side network effects, but they ultimately require a supply-side economy to flourish. The logic can be traced step by step:

- The initial thesis postulates a dependence of IT on industry.

- However, the analysis of the platform economy shows that digital platforms create value through network effects seemingly independently of physical production, which contradicts the thesis.

- The crucial question, however, is: What do these platforms provide? E-commerce platforms like Amazon need physical goods to sell. Cloud services like AWS or Microsoft Azure require businesses—including, and especially, manufacturing companies—to demand their computing power and storage capacity to optimize their own processes. AI applications need real-world data and problems from industry to train on and generate economically relevant value.

It follows that the relationship is not a one-way street, but a symbiotic cycle. The physical economy provides the "what"—the goods, the services, the data, the problems. The digital economy provides a highly efficient "how"—the marketplaces, the optimization algorithms, the communication infrastructure. Value is created on both sides: Industry becomes more efficient and innovative, while the digital economy provides the platforms for monetizing these efficiency and innovation gains.

The digitalization of industry: A symbiotic, not a parasitic relationship

Digitalization is no longer an external service that industry merely consumes; it has become an integral part of the production process itself. Under the banner of "Industry 4.0," physical manufacturing and digital intelligence are merging into a cyber-physical system that fundamentally changes the way value is created.

The integration of digital technologies such as AI, the Internet of Things (IoT), and robotics is driving efficiency, resilience, and sustainability in manufacturing. Companies are using AI-powered predictive maintenance to forecast machine failures and reduce downtime by 15–30%, potentially extending equipment lifespan by 20%. Digital services enable manufacturers to create entirely new value propositions, such as responsive customer portals with real-time pricing and inventory information, or personalized buying experiences that extend far beyond the physical product.

Scientific studies support this symbiotic relationship. Research from China reveals a complex, U-shaped development in which digitalization initially disrupts existing structures but ultimately significantly promotes the collaborative agglomeration of the manufacturing and service sectors. This suggests a profound integration process, not a simple customer-supplier relationship. Further studies confirm that the digital economy is a key driver of high-quality manufacturing development and accelerates the modernization of industrial structures.

These findings lead to a strategic reassessment of the role of a strong industrial base. It is not merely a consumer of generic cloud services from American hyperscalers. Rather, it represents a unique, valuable pool of data and complex problems that can serve as the foundation for developing specialized, proprietary digital and AI-powered solutions. These solutions are defensible and globally competitive. The logic behind this is compelling:

- The initial premise views the industry as a mere "customer" that monetizes the cloud.

- However, research shows that digital tools create value within manufacturing.

- The most valuable AI and digital services are often those that are trained on specific, high-quality data to solve complex, domain-specific problems.

- Germany's world-leading automotive, mechanical engineering and chemical industries generate vast amounts of unique operational data and present complex optimization challenges.

Consequently, this industrial base is not just a market, but a strategic asset—a “data refinery” and a “problem-solving laboratory.” It offers the perfect conditions for developing and training industrial AI that could outperform generic solutions. This creates a new level of high-margin, exportable digital products firmly rooted in physical expertise. This perspective reverses the dependency narrative: the most valuable future of the digital sector may depend on deep integration with the industrial sector, not just on serving it.

The physical requirements of the digital world

The idea of a “virtual” or “intangible” economy is a misleading oversimplification. The digital world is rooted in a profoundly physical reality, with an immense and ever-increasing demand for energy, water, land, and critical raw materials. Data centers, which form the backbone of cloud computing and AI, are industrial facilities of enormous scale.

Hyperscale data centers require electrical connection capacity of 20 to over 100 megawatts (MW)—enough to power a small town. AI-specific facilities, which rely on energy-intensive graphics processing units (GPUs), drive this demand even higher. Enormous quantities of water are needed to cool these massive server farms; a single large data center can consume millions of liters daily. The construction and operation of these facilities requires a robust and highly available infrastructure: high-performance power grids, dedicated substations, redundant fiber optic networks, and good transportation connections. Furthermore, the digital economy itself depends on a physical supply chain for its hardware, from servers and network components to critical microelectronic building blocks. The security of these supply chains is inextricably linked to the stability of the national defense industrial base (DIB) and access to critical minerals.

The claim that data centers can be built "anywhere," while production facilities are tied to complex location factors, proves to be a fallacy upon closer examination. In fact, the location requirements for cutting-edge digital and industrial infrastructure are converging. A step-by-step comparison of the criteria for hyperscale data centers and modern semiconductor factories (fabs) makes this clear:

- The initial hypothesis suggests a fundamental flexibility in the construction of data centers.

- However, the analysis of data center location choices reveals an intense focus on the availability of massive, stable and increasingly green energy, water access and fiber optic connectivity as crucial criteria.

- The analysis of site selection for semiconductor factories reveals an almost identical list of priorities: abundant energy and water, a highly skilled workforce, and a stable infrastructure.

This convergence means that regions are entering into direct competition for the same scarce fundamental resources—both for expanding their digital and advanced industrial capacities. A region's ability to deliver this infrastructure at scale becomes the primary bottleneck for both development paths. This undermines the notion that data centers are inherently more flexible in their choice of location and highlights the importance of integrated infrastructure and industrial policies.

🎯🎯🎯 Benefit from Xpert.Digital's extensive, five-fold expertise in a comprehensive service package | BD, R&D, XR, PR & Digital Visibility Optimization

Benefit from Xpert.Digital's extensive, fivefold expertise in a comprehensive service package | R&D, XR, PR & Digital Visibility Optimization - Image: Xpert.Digital

Xpert.Digital has in-depth knowledge of various industries. This allows us to develop tailor-made strategies that are tailored precisely to the requirements and challenges of your specific market segment. By continually analyzing market trends and following industry developments, we can act with foresight and offer innovative solutions. Through the combination of experience and knowledge, we generate added value and give our customers a decisive competitive advantage.

More about it here:

Digitalization meets industry: What distinguishes German and Californian models

Two titans, two models: A comparative economic analysis of Germany and California

The comparison of the economic models of Germany and California forms the empirical core of the initial thesis. A detailed, data-driven analysis confirms the structural differences, but also reveals crucial nuances that challenge the prevailing narrative of "industry versus IT" and lead to a more differentiated strategic assessment.

Macroeconomic overview: The initial situation

At first glance, the macroeconomic data seem to support the thesis of two fundamentally different economic structures. Germany, the largest economy in Europe, and California, the largest subnational economy in the world, are of similar size, but exhibit different growth profiles and sectoral focuses.

Germany

Nominal gross domestic product (GDP) amounted to approximately €4.12 trillion in 2023. The German economy experienced a period of stagnation in 2023 and 2024, with price-adjusted declines of -0.3% and -0.2%, respectively. This development reflects the challenges faced by a highly export-oriented and energy-intensive industrialized nation in a globally uncertain environment.

California

California's gross domestic product (GDP) reached approximately $3.9 trillion in 2023 and was projected to reach $4.1 trillion in 2024. This would place California, were it an independent state, as the fourth or fifth largest economy in the world. The economy of the "Golden State" is largely driven by the dynamism of its technology sector.

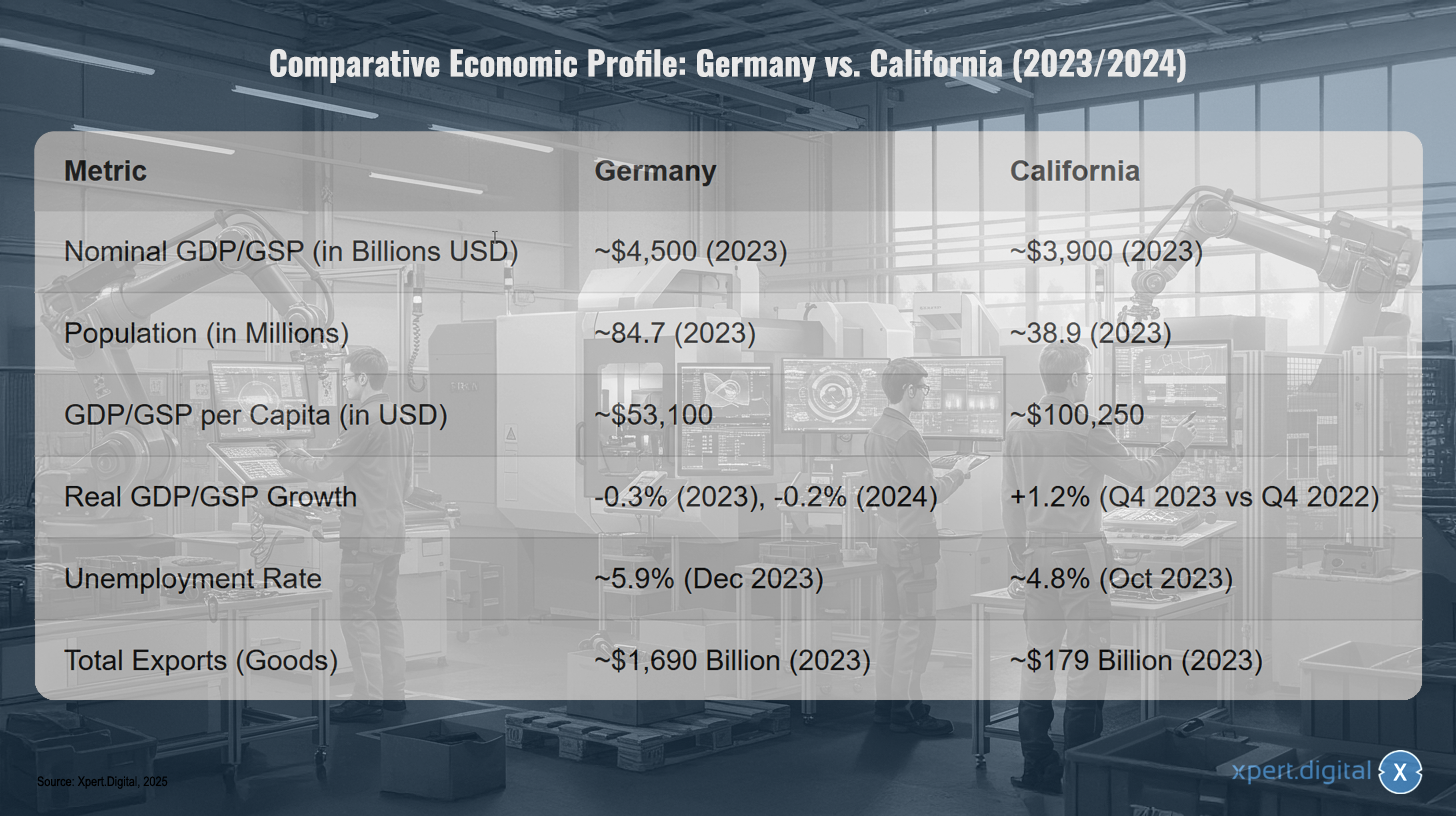

Comparative economic profile: Germany vs. California (2023/2024)

Comparative economic profile: Germany vs. California (2023/2024) – Image: Xpert.Digital

Note: Currency conversions are based on average exchange rates for the relevant period. The data serves to illustrate the order of magnitude.

The comparative economic profile of Germany and California for 2023/2024 shows that Germany has a nominal gross domestic product (GDP) of approximately US$4.5 trillion, while California's is around US$3.9 trillion. Germany's population is approximately 84.7 million, compared to California's 38.9 million. GDP per capita in Germany, at approximately US$53,100, is significantly lower than in California, where it is around US$100,250. Real GDP growth in Germany is negative, at -0.3% in 2023 and a projected -0.2% for 2024, whereas California recorded growth of 1.2% in the fourth quarter of 2023 compared to the fourth quarter of 2022. The unemployment rate in Germany was approximately 5.9% in December 2023, while in California it was around 4.8% in October 2023. Regarding total goods exports, Germany reached a value of approximately US$1.69 trillion, which is significantly higher than California's US$179 billion in 2023.

Germany's industrial powerhouse: The foundation of value

The strength of Germany's manufacturing sector is undisputed and forms the backbone of the national economy. The claim that it accounts for almost 20% of GDP is largely confirmed by the data and underscores the country's exceptional industrial depth by global standards.

A precise analysis of the Federal Statistical Office's data for 2023 yields a nominal GDP of €4,121.15 billion. The nominal gross value added (GVA) of the manufacturing sector amounted to €749.36 billion in the same year. This results in a GVA share of the manufacturing sector in total GDP of 18.2%. This figure is very close to the number cited in the inquiry and is remarkably high compared to other highly industrialized nations such as France (approx. 10.6%) or the USA (approx. 17.5%). Other sources indicate the share of "industry" as high as 24.2%, which, however, typically also includes sectors such as energy supply and construction.

The sector's dominance is also evident in absolute figures: manufacturing companies generated around €2.9 trillion in revenue in 2024. Its structure is dominated by four key industries: the automotive, mechanical engineering, chemical, and electrical engineering sectors. Globally operating corporations such as Volkswagen, BASF, and Siemens are flagships of this industrial strength. At the same time, the sector, particularly mechanical engineering, is heavily comprised of small and medium-sized enterprises (SMEs), ensuring a broad and resilient industrial base. However, recent economic developments also reveal the vulnerability of this model: price-adjusted gross value added in the manufacturing sector declined slightly by 0.4% in 2023 and more significantly by 3.0% in 2024, indicating weak global demand, high energy prices, and structural challenges.

Suitable for:

The Californian tech giant: Deconstruction of the digital economy

California's economy is undeniably dominated by the technology sector. The figures of 17–19% of GDP cited in the inquiry are supported by several sources. An analysis by the California Chamber of Commerce puts the tech sector's direct contribution at $623.4 billion, or 19% of GDP, in 2022; including multiplier effects, this figure rises to nearly $1 trillion, or 30% of the state's economic output. Other sources cite a direct economic impact of $542.5 billion, equivalent to 16.7% of the economy. This immense financial power is also reflected in the market capitalization of the largest technology companies in Silicon Valley, which reached a record $14.3 trillion in February 2024.

At the same time, the manufacturing sector's share of the Californian economy is estimated at 11%, which seems to confirm the thesis of a less industrialized economy compared to Germany. However, this simple comparison is strategically misleading, as it overlooks a crucial component of the Californian economy. Analyzing the composition of the Californian "tech sector" leads to a fundamental reassessment:

The common perception establishes a clear separation between Germany (industry) and California (IT/software).

A detailed report by the California Chamber of Commerce, however, breaks down the "Tech Sector" into eight subsectors. These include, as expected, software, IT, and entertainment, but also "High-Tech Manufacturing" (semiconductors, computer and communications hardware, biomedical devices) and "Aeronautics & Space.".

Within this broad tech sector, high-tech manufacturing is the largest subsector in terms of employment, with 426,500 jobs. The goods-producing industries within the tech sector alone contribute $201.4 billion to California's GSP.

These facts necessitate a revision of the original comparison. A significant part of California's technological dominance stems from its highly advanced industrial base. The state is not deindustrialized; it possesses a different kind of industry. The relevant comparison is therefore not "industry versus IT," but rather "traditional German heavy industry versus advanced Californian high-tech industry." This nuance is crucial for the strategic assessment of the future viability of both models.

A direct comparison of the IT sector

A direct comparison of the pure IT and communications (ICT) sectors confirms California's overwhelming leadership position and highlights the scale of the challenge for Germany and the EU to close this gap.

Germany

The ICT sector's share of GDP is estimated at approximately 4.5% to 4.8%. The total German ICT market is projected to reach a volume of €235.8 billion by 2025. This underscores the growing, but still relatively small, role of the IT sector compared to the overall economy.

California

As previously explained, the broad tech sector is dominant, accounting for 17–19%. Even when focusing on a narrower definition, such as the "information" sector, which primarily encompasses software, publishing, and data processing, this sector alone contributes 14% to California's GSP. Relative to the respective economic sizes, the core IT sector in California is therefore about three times more significant than in Germany.

These figures illustrate that the “rapid catch-up process” for Germany in the IT sector, as postulated by the initial thesis, would require a tremendous effort to overcome the existing gap in terms of size, innovation strength and market capitalization.

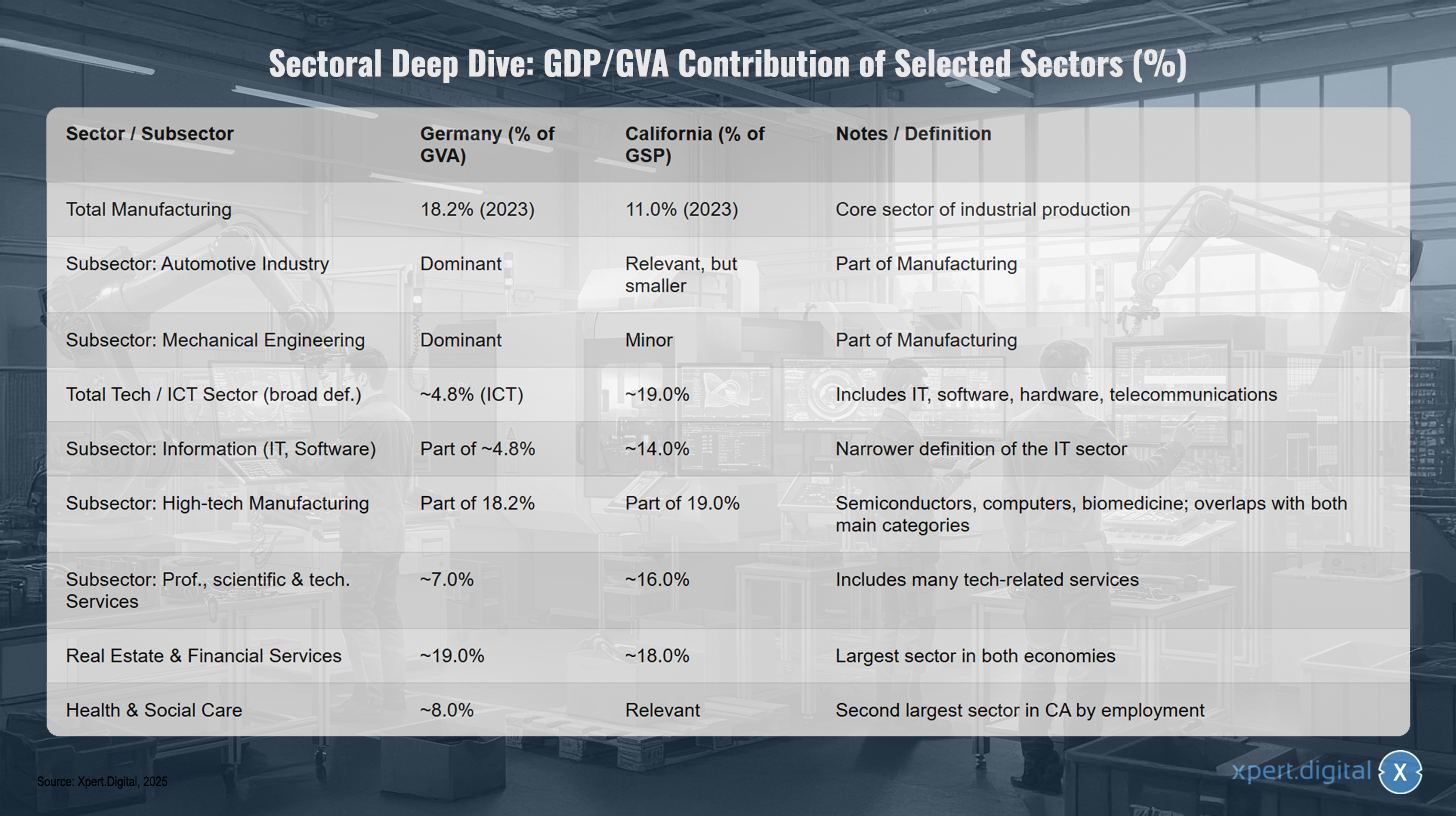

Sectoral in-depth analysis: GDP/GVA contribution of selected sectors (%)

Sectoral in-depth analysis: GDP/GVA contribution of selected sectors (%) – Image: Xpert.Digital

The sectoral analysis shows the contribution of selected sectors to gross domestic product (GDP) and gross value added (GVA) in Germany and California. The manufacturing sector accounts for 18.2% (2023) in Germany and 11.0% (2023) in California, thus representing a core sector of industrial production. Within this sector, the automotive industry is dominant in Germany, while it is relevant but smaller in California. Mechanical engineering is also dominant in Germany but less significant in California. The entire technology and ICT sector comprises approximately 4.8% (ICT) in Germany and about 19.0% in California, encompassing IT, software, hardware, and telecommunications. The information sector, which includes IT and software, accounts for roughly 14.0% in California and is part of the approximately 4.8% in Germany. High-tech manufacturing, which includes semiconductors, computers, and biomedicine, is part of the manufacturing sector in both regions. Professional, scientific, and technical services contribute approximately 7.0% to the economy in Germany and about 16.0% in California, encompassing many technology-related services. Real estate and financial services are the largest sector in both economies, accounting for roughly 19.0% in Germany and about 18.0% in California. Health and social services represent approximately 8.0% of the economy in Germany and are a significant, second-largest sector by employment in California.

Foundations and Fortifications: The Strategic Value of an Industrial Base in the Digital Age

The analysis of the two economic models goes beyond purely quantitative comparisons and requires an assessment of their strategic robustness. The assumptions regarding resilience, agility in infrastructure development, and the strength of the respective ecosystems must be critically examined. This reveals that traditional industrial strengths can offer new, often unexpected strategic advantages in the digital age.

Speed versus substance: The infrastructure dilemma

The claim that data centers can demonstrably be built faster than production facilities is superficially correct, but it overlooks the real strategic challenge. The physical construction of the buildings is no longer the critical path in the development of hyperscale infrastructure. Rather, it is the lengthy processes for securing the necessary utilities—energy and water—that dictate the timeline and are becoming the primary bottleneck for the growth of the digital economy.

The pure construction process can be significantly accelerated through modular and prefabricated approaches. A modular data center can be operational in just 3–6 months, whereas a traditional on-site construction takes 12–24 months. This initially supports the assumption of greater agility. However, the entire project timeframe, from site selection to commissioning a large data center, typically spans 3 to 6 years. The critical time factors are the permitting processes and connecting to the utility infrastructure, each of which can take 6 to 18 months or longer. A hyperscale data center requires an immense and highly reliable power supply of over 100 MW, often its own substation, access to high-capacity water pipes for cooling, and redundant fiber optic connections. Providing this infrastructure is a complex and time-consuming undertaking that extends far beyond the actual construction.

As already explained in section 2.3, these requirements converge with those of modern industrial plants. An advanced semiconductor factory has a comparably enormous demand for stable energy and highly purified water. This leads to a reassessment of location advantages. Germany's established industrial areas could represent a significant "brownfield" advantage. The logic is as follows:

The theory assumes that building a data center is an isolated task.

The analysis shows that the main limitation is the supply infrastructure.

Germany has a decades-long history of developing and maintaining heavy industrial zones with massive energy and water infrastructure. These sites are already dedicated to industrial use and have established, high-performance grid connections. This represents an often overlooked but strategically valuable asset.

California, on the other hand, is implementing far-reaching climate protection laws (e.g., SB 253, SB 261) that require companies to submit comprehensive emissions reports and implement reductions. Data centers are massive energy consumers, with a carbon intensity that averages 50% higher than the national average for all economic activities.

This creates a strategic asymmetry: Germany's existing industrial infrastructure could accelerate the construction of data centers by alleviating the biggest bottleneck – the power supply. At the same time, California's regulatory environment, coupled with grid constraints, could become a significant obstacle to the expansion of energy-intensive AI data centers. This poses the risk of "stranded assets" if the decarbonization of the power grid cannot keep pace with the growing energy demands of the AI industry, and presents a strategic opportunity for regions with more robust and available energy infrastructure.

Ecosystem dependencies: Capital, talent, and regulation

Success in both the digital and industrial sectors depends on a complex ecosystem of capital, talent, and a supportive regulatory framework. This is where the most significant differences and the greatest challenges for Germany's efforts to catch up become apparent.

Venture capital

California, and the Bay Area in particular, is the undisputed global center for venture capital (VC). An estimated 35% of all US venture capital is concentrated there. American VCs tend to be more active and specialized than their European counterparts, which are more geographically fragmented. This massive capital pool is a crucial factor in the ability to rapidly scale technological innovations and create global market leaders. Germany and Europe have a significant structural disadvantage in this regard.

Human capital (Germany's Achilles heel)

While Germany's dual vocational training system provides an excellent foundation for qualified specialists in the industrial sector, the country is suffering from a dramatic and worsening shortage of IT professionals. Forecasts from the industry association Bitkom indicate a gap of over 150,000 unfilled IT positions by 2024. Long-term projections are even more alarming: by 2040, this gap could grow to 663,000 IT specialists. This lack of human capital is arguably the most critical bottleneck and fundamentally undermines the notion that Germany can "quickly" catch up in the IT sector. Without a massive and successful effort in education, retraining, and immigration, the crucial foundation for a thriving digital ecosystem is lacking.

Regulatory environment

Here, the picture is partially reversed. Companies in California face high operating costs, rising wages, and a complex regulatory environment that is often perceived as burdensome. In particular, stringent climate regulations and high energy costs make the location less competitive for manufacturing companies compared to other US states. While Germany and the EU also offer a highly regulated environment, their political stability and integrated social market economy can also provide advantages for long-term, capital-intensive investments.

In summary, California possesses an unparalleled ecosystem for the rapid scaling of software and platform innovations, based on capital and a deep talent pool. Germany has a strong industrial ecosystem, but its lack of digital human capital poses an existential threat to its digital ambitions.

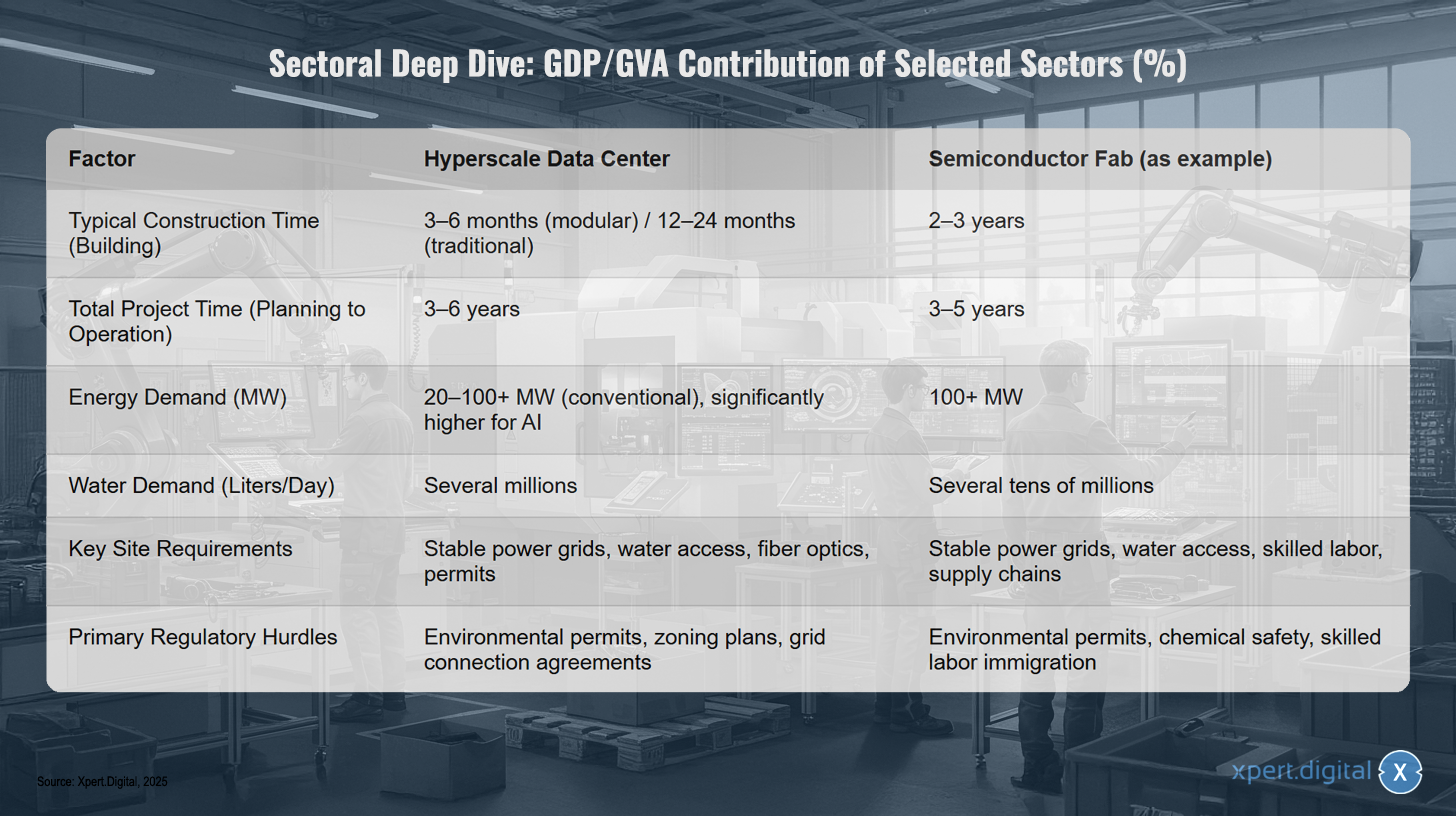

Comparison of infrastructure development: Data centers vs. advanced manufacturing

Infrastructure development comparison: Data centers vs. advanced manufacturing – Image: Xpert.Digital

A comparison of infrastructure development reveals significant differences between hyperscale data centers and advanced semiconductor fabrication plants. Construction time for a hyperscale data center using modular construction typically ranges from three to six months, while traditional buildings can take up to 12 to 24 months. The total project time from planning to operation is approximately three to six years. In contrast, the construction of a semiconductor fabrication plant typically takes two to three years, with a total project time of three to five years. Regarding energy consumption, conventional data centers require 20 to over 100 megawatts; for artificial intelligence applications, consumption is significantly higher, while semiconductor fabrication plants generally require more than 100 megawatts. Water consumption for data centers is several million liters per day, compared to tens of millions of liters daily for semiconductor fabrication plants. Key site requirements for data centers include stable power grids, water access, fiber optic connections, and regulatory approvals. For semiconductor fabrication plants, in addition to stable power and water supplies, qualified personnel and intact supply chains are crucial. The primary regulatory challenges for data centers include environmental permits, zoning plans, and grid connection contracts, while semiconductor factories must also consider chemical safety and the immigration of skilled workers.

🔄📈 B2B trading platforms support – strategic planning and support for exports and the global economy with Xpert.Digital 💡

B2B trading platforms - Strategic planning and support with Xpert.Digital - Image: Xpert.Digital

Business-to-business (B2B) trading platforms have become a critical part of global trade dynamics and thus a driving force for exports and global economic development. These platforms offer significant benefits to companies of all sizes, particularly SMEs – small and medium-sized businesses – which are often considered the backbone of the German economy. In a world where digital technologies are becoming increasingly prominent, the ability to adapt and integrate is crucial to success in global competition.

More about it here:

Europe in the fast lane: Strategies for digital and industrial sovereignty

The way forward: A strategic blueprint for Europe's digital and industrial sovereignty

The comparative analysis highlights the need for a coherent and ambitious strategy for Germany and the European Union. The mere existence of a strong industrial base is no guarantee of future prosperity. It must be actively leveraged to shape the digital transformation and achieve a sovereign position in global competition. This requires targeted policy measures that address the identified weaknesses and capitalize on Europe's unique strengths.

Suitable for:

The EU's digital ambition: A fragmented reality

With the proclamation of the "Digital Decade," the European Union has formulated a clear strategic ambition. The goals include strengthening digital skills, building a secure and sustainable digital infrastructure, digitally transforming businesses, and digitizing public services. The annual progress report, "State of the Digital Decade," serves as a monitoring tool. However, the 2025 report has been described as a "wake-up call" due to insufficient progress and significant disparities between member states.

A central motive behind these efforts is the pursuit of "digital sovereignty." This refers to Europe's ability to act in the digital space according to its own rules and values, without being dependent on external actors. This dependency is a reality today: the EU is heavily reliant on US and Chinese suppliers for strategic technologies such as AI, cloud infrastructure, and semiconductors. This dependency is increasingly perceived as a risk to Europe's strategic autonomy, especially as digital infrastructures and services become ever more critical to the functioning of the economy and society.

The biggest obstacle to digital sovereignty and competitiveness is the ongoing fragmentation of the single market. Although the EU single market, with over 440 million consumers, theoretically offers enormous potential, national differences in regulation, standards, and administrative practices prevent digital companies from scaling as quickly and smoothly as their counterparts in the US or China. The cost of this incomplete digital transformation in Europe was estimated at €315 billion for 2021, with the potential to rise to €1.3 trillion by 2033. Completing the digital single market is therefore not a technical imperative, but a strategic necessity of the highest order.

Politics in action: Evaluation of the EU's instruments (Chips Act, AI Act)

In response to these challenges, the EU has developed an impressive set of regulatory and investment tools in recent years. Two of the most prominent examples are the EU Chips Act and the EU AI Act.

EU Chips Act

This law is a direct response to the semiconductor shortage and the strategic dependence of the sector. The goal is ambitious: to double the EU's share of the global semiconductor market to 20% by 2030. To achieve this, over €43 billion in public and private investment is to be mobilized to promote research, design, and, above all, new production facilities ("fabs") in Europe. Critics point out, however, that even this sum is modest compared to investment programs in the US and Asia, and that the 20% target is considered highly unlikely. Nevertheless, the law has already triggered a wave of investment announcements and placed the sector's strategic importance on the political agenda.

EU AI Act

With this law, the EU has created the world's first comprehensive regulation for artificial intelligence. The approach is risk-based and aims to promote trustworthy, safe, and human-centered AI. While the EU is setting a global standard (the "Brussels Effect"), some industry stakeholders are concerned that the regulation could slow innovation and impair European competitiveness in the global AI race. The challenge lies in reconciling the protection of fundamental rights with the need for agility and innovation.

Germany's AI strategy

At the national level, Germany complements EU initiatives with its own AI strategy, which has a budget of €5 billion until 2025 and focuses on strengthening research, technology transfer to industry, and talent development. However, recent reports from the OECD and other institutions reveal a discrepancy between ambition and reality. Germany lags behind in AI adoption within its European partner countries, lacks its own leading AI frontier model, and remains heavily dependent on foreign providers.

Strategic recommendations: Shaping a unified industrial-digital future

To effectively leverage Europe's industrial strength and achieve genuine digital sovereignty, it is not enough to rely solely on regulation or to fund individual flagship projects. What is needed is an integrated, bold strategy that addresses the key levers.

Completion of the digital single market for services

This is the most urgent task. The European Commission and the Member States must systematically dismantle the remaining national barriers to digital services. This includes areas such as the harmonization of consumer protection rules, the cross-border recognition of digital identities, and the harmonization of tax regulations for digital businesses. Only a truly seamless single market with 440 million consumers will give European startups and scale-ups the chance to achieve the size and speed necessary for global competition.

A European “Digital Skills Pact”

The IT skills shortage so clearly visible in Germany is a Europe-wide problem and the single biggest obstacle to growth. It requires a massive, coordinated effort – a "pact" between the EU, member states, businesses, and educational institutions. This pact must set ambitious targets for retraining and further education of the existing workforce, radically modernize IT education in schools, and make Europe an attractive destination for global IT talent, including through simplified immigration rules and competitive framework conditions. Without addressing the staffing issue, all other investments will remain ineffective.

Promotion of industrial-digital ecosystems

Policymakers should not only focus on building generic digital infrastructure, but also actively promote deep integration between the industrial base and the digital innovation landscape. Instruments such as the Chips Act or Important Projects of Common European Interest (IPCEI) should prioritize funding for projects at the intersection of industry and AI. The goal must be to create "Industrial-Digital Champions" that leverage the unique datasets and challenges of European industry to develop world-leading, domain-specific AI solutions (see section 2.2).

Pooling and alignment of investment capital

The European venture capital landscape is fragmented and undercapitalized compared to the US. The EU should use its financial instruments (e.g., through the European Investment Bank) to promote the creation of pan-European, privately managed umbrella funds. These funds must be capable of raising the large financing rounds required to scale technology companies in their growth phase. A more unified strategy is needed to channel public and private capital more effectively and create European venture capital funds that can compete globally.

By consistently implementing these four strategic pillars, Europe can transform its industrial strength from a passive market for external digital providers into an active driver for a sovereign and competitive digital future.

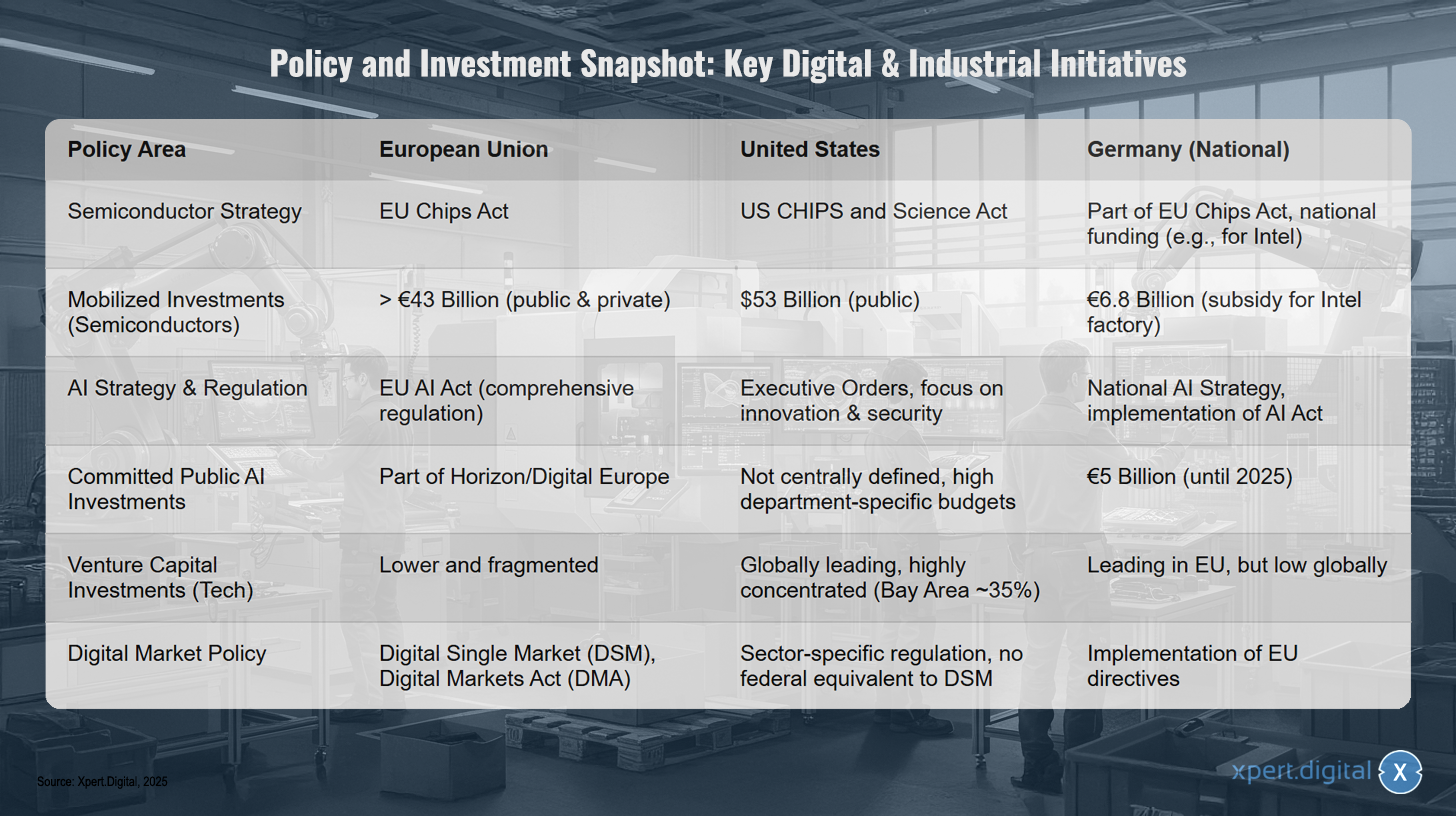

Policy and Investment Snapshot: Key Digital & Industrial Initiatives

Policy and investment snapshot: Key digital & industrial initiatives – Image: Xpert.Digital

The policy and investment snapshot highlights key digital and industrial initiatives in the European Union, the United States, and Germany. In the area of semiconductor strategy, the European Union has responded with the EU Chips Act and mobilized investments of over €43 billion (public and private), while the US is implementing the US Chips and Science Act with $53 billion in public funding. Germany is part of the EU Chips Act and is providing national funding to companies such as Intel with €6.8 billion. Regarding AI strategy and regulation, the EU is pursuing comprehensive regulation with the EU AI Act, the US is relying on executive orders focused on innovation and safety, and Germany is working on implementing the AI Act with a national AI strategy. Public AI investments in the EU are part of Horizon and Digital Europe, while in the US they are not centrally determined but are substantial depending on the specific government department, with Germany committing €5 billion by 2025. In terms of venture capital investments in the tech sector, the EU, with Germany leading the way within Europe, but its global participation is low. The US is the global leader, with a strong concentration in the Bay Area, while the EU's participation is lower and more fragmented. Regarding digital market policy, the EU pursues the Digital Single Market (DSM) and the Digital Markets Act (DMA), while the US has sector-specific regulations but no federal equivalent to the DSM, and Germany implements EU directives.

Your global marketing and business development partner

☑️ Our business language is English or German

☑️ NEW: Correspondence in your national language!

Konrad Wolfenstein

I would be happy to serve you and my team as a personal advisor.

You can contact me by filling out the contact form or simply call me on +49 7348 4088 965 (Munich) . My email address is: wolfenstein ∂ xpert.digital

I'm looking forward to our joint project.