Success with SME sales alliances in EU defense logistics: Sales partnerships for major projects with EU high-tech – Image: Xpert.Digital

Automated warehouses, smart trains: How high-tech alliances are addressing NATO's weaknesses

The forgotten superpower: Why logistics determines Europe's security – and who benefits now

SMEs as innovation drivers: Europe's defense logistics on the move through strategic sales alliances ### Europe's new defense: Why small companies are now the unsung heroes ### From rail to AI: How SMEs want to revolutionize Europe's military logistics

Related to this:

The new paradigm – Europe's defense capability in transition

The turning point as a catalyst for a new industrial strategy

Geopolitical context

The geopolitical landscape of Europe has fundamentally changed in recent years. The annexation of Crimea in 2014 and, in particular, Russia's large-scale war of aggression against Ukraine since February 2022 mark a watershed moment, described in Germany as a "turning point." These events have shaken the decades-long prevalence of a stable peace order on the continent and have once again placed the need for a robust and credible collective defense capability at the heart of European security policy. Faced with increasing geopolitical tensions, the European Union has placed defense at the top of its agenda and is striving to strengthen its defense industry to make it more responsive, innovative, and resilient. The return to national and collective defense is no longer a theoretical scenario but a strategic necessity with profound implications for armed forces, industrial policy, and technological development across Europe.

NATO's eastern flank as a strategic focus

The strategic focus of this realignment is unmistakably on NATO's eastern flank. From the Baltic Sea in the north to the Black Sea in the south, the alliance has massively reinforced its presence to ensure a credible deterrent against potential aggressors. Following the Russian invasion of Ukraine, the existing multinational battle groups in the Baltic states and Poland were supplemented by four more in Bulgaria, Hungary, Romania, and Slovakia. At the 2022 NATO summit in Madrid, it was also decided that these units could be expanded to brigade strength if necessary. However, this military presence is only effective if it is supported by superior logistical capability. The strategic challenge lies in being able to rapidly move and supply massive reinforcements—plans envision the deployment of up to 800,000 NATO troops within 180 days—to and through the eastern flank in the event of a crisis. Initiatives such as the Eastern Flank Deterrence Line, launched by the US and its allies, underscore this focus. It prioritizes ground-based capabilities and the interoperability of weapon systems to build a robust defense line. This is complemented by regional efforts such as the Baltic Defense Line, a joint project between Estonia, Latvia, and Lithuania to construct defense installations, and Poland's East Shield program, which also aims to fortify the border. These initiatives require not only weapon systems but, above all, sophisticated cross-border logistics for materiel, ammunition, and supplies.

The European answer: A new industrial strategy for the defense sector

In response to the changing security landscape, the European Union has initiated a paradigm shift in its defense policy. The objective is clearly defined: Member States should invest more, better, jointly, and at the European level in their defense. This requires building a responsive and resilient European Technological and Industrial Defence Base (EDTIB) capable of meeting the needs of European armed forces and ensuring technological sovereignty. Key strategic documents and initiatives point the way. The "Strategic Compass for Security and Defence" defines the EU's ambitions and emphasizes the need to act more quickly and decisively. The "Readiness 2030" White Paper, expected in 2025, is intended to set further crucial directions for increasing the EU's defense readiness. Programs such as the European Defence Fund (EDF), with a budget of almost €8 billion for the period 2021-2027, and the resulting European Defence Industry Programme (EDIP) are designed to promote collaborative research, development, and procurement of defense equipment. These initiatives aim to overcome the fragmentation of the European defence market and to make industrial cooperation the norm.

Logistics as a decisive factor (“Logistics win wars”)

In this new strategic environment, logistics moves into the spotlight. The old military adage that amateurs talk about tactics, but professionals talk about logistics, is gaining renewed urgency. Without superior, resilient, and rapid logistics, neither credible deterrence nor successful defense operations are conceivable. The ability to get troops and equipment to the right place at the right time is becoming the decisive factor. Due to its geographical location and economic strength, Germany plays a key role as a central logistical hub for NATO and EU operations. Supporting allied forces during deployment through German territory (Host Nation Support) has become a core task of the Bundeswehr (German Armed Forces). The efficiency and speed of these logistical processes are a direct indicator of the defense capability of the entire alliance. The challenge lies in creating a logistics chain that not only functions in peacetime but also remains robust and adaptable under conditions of crisis or conflict.

Related to this:

The indispensable but ambivalent role of SMEs in the European defence ecosystem

Definition and economic importance of SMEs

Small and medium-sized enterprises (SMEs) form the backbone of the European economy. According to the European Commission's definition, a company qualifies as an SME if it employs fewer than 250 people and has either an annual turnover of no more than €50 million or an annual balance sheet total of no more than €43 million. In the European Union, the approximately 23 million SMEs represent over 99% of all businesses and employ around 100 million people. They are therefore not only a crucial factor for growth and prosperity, but also key drivers of Europe's green and digital transformation. Their importance is so fundamental that EU policy follows the principle of "Think Small First," which states that the needs of SMEs should be given priority in policy decisions.

SMEs as recognized innovation drivers in the defense sector

Particularly in the high-tech defense sector, the role of SMEs as indispensable players is increasingly recognized. They are considered "key drivers of innovation," especially with regard to disruptive technologies that are crucial for Europe's future defense capabilities. While large defense companies are often tied to long development cycles for complex weapon systems, SMEs, and especially startups, are characterized by their agility, high flexibility, and specialization. They are often leaders in future-oriented fields such as artificial intelligence (AI), quantum technology, cyber defense, robotics, and unmanned systems. Their inherent strengths enable them to respond more quickly to new requirements and meet specific customer needs. SMEs can often adapt their production more rapidly and are characterized by a more innovation-friendly corporate culture marked by strong employee loyalty and high motivation. This ability to develop innovative solutions quickly makes them an indispensable component of the European Technological and Industrial Defense Base (EDTIB).

The harsh reality: Structural underrepresentation and systemic barriers

Despite this political recognition and their evident innovative capacity, SMEs in the European defense sector face a harsh reality: they are structurally and massively underrepresented. The discrepancy between their potential and their actual participation in public defense contracts is striking. One study shows that in Germany in 2014, SMEs accounted for only 3.2% of industry revenue, while their share of the overall economy was 35.5%. A similar picture emerges at the EU level, where SMEs represented only 6.1% of revenue in a sample of public defense contracts, but accounted for 29% of the total public sector revenue. These figures demonstrate that the "barracks gate" appears to be far more open for large, established companies than for innovative SMEs and start-ups.

Analysis of access barriers

The reasons for this marginalization are systemic in nature and create high barriers to market entry and growth for SMEs in the defense sector.

Financing hurdles: One of the biggest challenges is access to capital. Many banks and private investors are hesitant to invest in defense companies. This is due, on the one hand, to strict ESG (Environmental, Social, Governance) guidelines, which often critically assess defense investments, and on the other hand, to risk aversion in a market with long development cycles and uncertain purchase guarantees. This hits SMEs particularly hard, as they rely on external financing for innovation and scaling.

Bureaucratic and regulatory complexity: Procurement procedures in the defense sector are often extremely complex, lengthy, and subject to stringent formal requirements. Legal technicalities and the need to provide extensive economic and technical documentation overwhelm the administrative capacities of many SMEs. While measures such as the EU directive to simplify the transfer of defense goods are intended to alleviate this, the fundamental complexity of procurement processes remains a significant barrier.

Market fragmentation and the dominance of systems integrators: The European defense industry has grown historically and is fragmented nationally. It is dominated by a small number of large systems integrators that act as prime contractors for the armed forces. SMEs are often relegated to the role of a second- or third-tier supplier. This dependency leads to margin pressure and limits their ability to directly market their own innovations. The massive increase in defense spending risks further cementing this dominance if the funds are primarily distributed through the large integrators.

Skills shortage: Particularly in high-tech fields crucial for future defense, such as AI, quantum computing, and cybersecurity, there is an acute shortage of qualified specialists. SMEs are competing with the civilian tech industry for the best talent and are often at a disadvantage.

A profound paradox is evident: While policymakers declare the innovative capacity of SMEs essential for Europe's strategic autonomy and technological superiority, the actual structures of the defense market systematically favor established large corporations. The political commitments to promoting SMEs, as formulated in strategy papers, stand in stark contrast to the reality of procurement practices. The systemic requirements—high capital demands, complex compliance regulations, and lengthy, resource-intensive tendering processes—are de facto tailored to the capacities of large corporations.

Without a fundamental reform of procurement processes and the creation of targeted, accessible pathways for SMEs, the "turning point" risks failing to deliver its transformative power for small and medium-sized enterprises (SMEs). The new, massive financial resources, for example from the European Defence Fund, would then primarily flow to the large system integrators. While SMEs would participate as subcontractors, their structural dependency would become entrenched, and their full innovative potential would be stifled by the rigid, hierarchical structures of large corporations. Against this backdrop, the formation of strategic sales alliances for SMEs becomes not only a growth strategy but an existential necessity to compensate for these structural disadvantages and effectively bring their innovative strength to market.

Hub for Security and Defense - Advice and Information

Hub for Security and Defense - Image: Xpert.Digital

The Security and Defence Hub offers expert advice and up-to-date information to effectively support companies and organizations in strengthening their role in European security and defence policy. Working closely with the SME Connect Defence Working Group, it particularly promotes small and medium-sized enterprises (SMEs) that wish to further develop their innovative capacity and competitiveness in the defence sector. As a central point of contact, the Hub thus creates a crucial bridge between SMEs and European defence strategy.

Related to this:

Public-Private Partnership (PPP) defense alliances: Key to success in complex security landscapes

Strategic cooperation as the key to success – sales alliances for SMEs

Models of B2B cooperation in the defense context

Definition of B2B relationships

The business-to-business (B2B) sector, which describes business relationships between companies, differs fundamentally from the business-to-consumer (B2C) market. While B2C transactions are often short-term, emotionally driven, and focused on individual purchases, B2B business is characterized by greater complexity, larger order volumes, and a long-term, partnership-oriented approach. This is especially true for the defense sector. Here, business relationships are based on detailed contract negotiations, deep technical understanding, and a high degree of trust, as security-critical products and services are involved. So-called "relationship marketing," i.e., the cultivation of long-term and stable business relationships, is of central importance in this environment.

Related to this:

Analysis of forms of cooperation

To succeed in this demanding B2B environment, especially for SMEs, collaborations are essential. Several models exist, each offering specific advantages and disadvantages:

Strategic alliances: This is the most flexible form of cooperation. Two or more companies agree to a long-term collaboration to achieve common goals, while retaining their full legal and economic independence. The focus is on pooling resources (e.g., technology, knowledge), sharing risks (e.g., in developing new products), and jointly accessing new markets. Since no new legal entity is created and often no capital investment is required, this form is particularly attractive for SMEs to collaborate on a project basis and in an agile manner. However, the lower level of contractual commitment can also be a disadvantage in the event of disagreements.

Joint Ventures (JVs): In a joint venture, two or more parent companies establish a legally independent subsidiary, over which they jointly exercise control. This form is far more binding and suitable for large, capital-intensive, and long-term projects, such as the joint development and production of a new weapons system. Costs, risks, and profits are shared, which reduces the entrepreneurial risk for each partner. A key advantage is the ability to jointly create and own new intellectual property. Disadvantages include the high coordination effort, potential conflicts arising from differing corporate cultures, and lower flexibility compared to a strategic alliance.

Consortia: A consortium is a purpose-driven association of companies, typically formed for the duration of a specific project, for example, to submit a joint bid for a major public tender. The partners remain legally independent but act externally as a single entity. Unlike a strategic alliance, which is often broader in scope, a consortium is not intended to be permanent and dissolves upon project completion. It is a pragmatic solution for pooling the expertise and resources required for a large contract.

Platform-based ecosystems: This most modern form of cooperation is based on digital platforms that connect a multitude of actors – SMEs, large companies, suppliers, customers, and service providers – in a digital network. They not only enable transactions but also promote collaboration and standardized data exchange.

Sales models in detail

Different sales strategies can be pursued within these forms of cooperation:

Direct sales: The company sells its products or services directly to the end customer, in the defense sector typically to the Ministry of Defense or a procurement agency. The advantages lie in the direct customer relationship, full control over the sales process, and higher margins. However, for SMEs, this approach is often hardly feasible due to the immense resource expenditure required for sales, marketing, and handling complex tenders.

Indirect sales via partner networks: Here, sales are conducted through third parties, such as distributors, resellers, or – most commonly in the defense sector – large system integrators who incorporate the SME's product into their overall system. The decisive advantage for SMEs is scalability and cost efficiency. They can access established sales networks, certifications, and the partner's market knowledge without having to build their own expensive sales organization. The disadvantage is a lower profit margin and significant dependence on the partner, who controls the interface with the end customer. For many specialized SMEs in the defense sector, however, this is the only viable route to market.

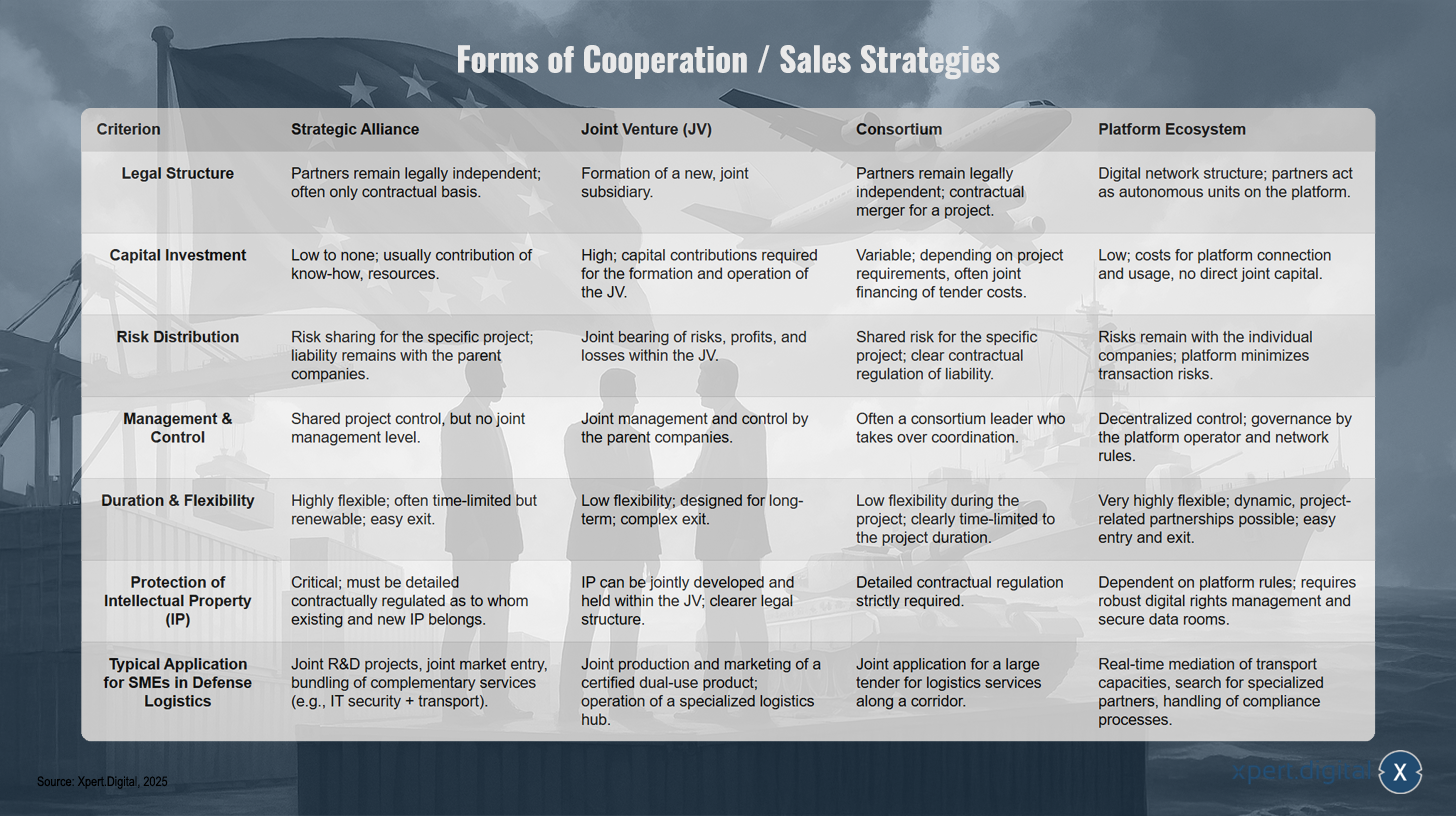

The following table provides a comparative analysis of cooperation models and is intended to serve as a strategic tool for decision-makers in SMEs to identify the most suitable form of cooperation for their specific situation.

Different sales strategies can be pursued within these forms of cooperation – Image: Xpert.Digital

In the world of corporate cooperation, various forms of collaboration exist, differing significantly in their legal, financial, and organizational aspects. Strategic alliances offer companies a flexible way to jointly implement projects without relinquishing their legal independence. This primarily involves the sharing of know-how and resources, keeping risks manageable and ensuring that the parent companies retain their liability.

A more intensive form of cooperation is the joint venture, in which a completely new joint company is founded. Here, the partners invest substantial capital and share risks, profits, and losses equally. Management is carried out by a joint executive team, which increases commitment and accountability.

Consortia are particularly suitable for time-limited projects where partners remain legally independent but collaborate on a specific task. Typically, there is a consortium leader who handles the coordination.

Platform ecosystems represent a modern form of cooperation. They enable highly flexible digital network structures in which companies operate as autonomous entities. Transaction risks are minimized, and companies can dynamically enter into partnerships.

The choice of cooperation model depends on strategic goals, resources, and risk tolerance. For small and medium-sized enterprises in sensitive sectors such as defense logistics, these models offer various opportunities – from joint research projects to the real-time brokering of transport capacities.

Success factors and risk management in defense alliances

The success of cooperation in the defense sector depends on a multitude of factors that go far beyond the purely technical or economic compatibility of the partners.

“Soft” success factors

Trust is the foundation of any successful alliance. In a sector where sensitive information and technologies are exchanged, open, honest, and regular communication is essential. Dishonesty or misunderstandings can quickly destroy a partnership. Equally important is the compatibility of strategic goals and corporate cultures. If partners have different visions for the future of the collaboration or if their working methods differ fundamentally, conflicts are inevitable. Therefore, a thorough evaluation of potential partners beforehand is crucial.

“Hard” success factors: The foundation of cooperation

In addition to the cultural aspects, the legal and technical framework must be precisely and robustly designed:

Contract drafting: A detailed and legally sound contract is the backbone of any alliance. It must regulate all essential aspects: the precise contributions and responsibilities of each partner, the distribution of costs and profits, clear liability rules, and, above all, well-defined processes for decision-making and conflict resolution. An often neglected but critical point is exit clauses, which stipulate the conditions under which and the consequences of a partner leaving the alliance. Given the complexity and the increased liability risk, which can be particularly existential for SMEs, policymakers are calling for support for these businesses, for example, through the provision of model contracts or the creation of project-based joint ventures with government participation to mitigate the risk for SMEs.

Intellectual Property (IP) Protection: For innovative SMEs, their intellectual property – patents, designs, software code, know-how – is their most valuable asset. In a collaboration, there is a risk of this knowledge being unintentionally transferred. Therefore, the collaboration agreement must precisely define which IP each partner contributes ("background IP") and who owns the IP newly created within the framework of the collaboration ("foreground IP"). Clear rules for the use, licensing, and protection of these rights must be established to avoid future disputes.

Cybersecurity in the supply chain: An alliance inevitably increases the digital attack surface. A cyberattack on one partner can quickly spread to the entire network. The entire alliance is only as secure as its weakest link. Therefore, adherence to common, high cybersecurity standards is non-negotiable. This requires a joint risk assessment, the implementation of compatible security systems (e.g., according to ISO 27001), and regular joint exercises to defend against cyberattacks.

Compliance and regulations: The defense sector is extremely heavily regulated. Companies must adhere to a multitude of national and international regulations. These include strict export control laws for defense and dual-use goods, which require approval from authorities such as the German Federal Office for Economic Affairs and Export Control (BAFA). When collaborating with US partners or accessing the US market, further complex regulations such as ITAR (International Traffic in Arms Regulations) or the Cybersecurity Maturity Model Certification (CMMC) come into play. All partners in an alliance must ensure compliance with these rules, as violations can lead to severe penalties and exclusion from future contracts.

The power of indirect distribution: Partner networks as a growth engine

SMEs and system houses

The relationship between innovative SMEs and large system integrators is often symbiotic, but rarely symmetrical. SMEs provide specialized technologies and agility, while system integrators offer market access, the financial resources for large projects, experience in complex certification processes, and the capability for system integration. For many SMEs, partnering with a system integrator is the only way to integrate their products into major defense programs. However, this dependency carries the risk of intense price and margin pressure, as well as the loss of direct customer relationships. A successful SME must actively manage this relationship, leverage its technological uniqueness as negotiating leverage, and strive to avoid dependence on a single large customer.

SME-to-SME alliances

A strategic alternative to simply acting as a supplier is the formation of alliances between several SMEs. By pooling their capabilities, complementary companies can jointly offer more complex and comprehensive solutions. For example, a consortium consisting of a logistics software specialist, a provider of secure communication technology, and a transport company can create an integrated logistics package that is more attractive to a public sector client than the individual services. Such alliances increase competitive advantage and enable SMEs to act as more equal partners.

Lead generation and market opportunity creation

A key advantage of partnerships is improved access to information and market opportunities. Partner networks act as multipliers. Through collaboration, an SME gains insight into its partners' networks, learns earlier about new requirements and potential tenders, and can jointly develop offerings that it could never have managed alone. Consulting and networking services, such as those promoted by government agencies or industry associations, can play a vital role in bringing the right partners together.

For SMEs in the defense sector, a distribution alliance is therefore more than just one of many strategic options; it is a strategic imperative to compensate for the inherent structural disadvantages of the market. However, the success of these alliances is not guaranteed. It depends on extremely careful and proactive risk management, which plays a far less significant role in civilian markets. The selection of a partner must therefore go far beyond assessing technological or market complementarity. A crucial selection criterion must be the potential partner's compliance and security maturity. An alliance with a partner that is weak in the areas of intellectual property, cybersecurity, or export control can quickly become an existential threat for an SME. This makes the due diligence phase before entering into a partnership considerably more complex and critical than in any other sector.

The technological and logistical implementation – From corridors to digital platforms

The backbone of the deployment: LogHub networks and strategic corridors

The PESCO project “Network of Logistic Hubs”

To enable the rapid and efficient deployment of armed forces across Europe, the "Network of Logistic Hubs in Europe and Support to Operations" project was launched within the framework of the EU's Permanent Structured Cooperation (PESCO). The core idea is the establishment of a Europe-wide network of military logistics centers (LogHubs). These are national logistics facilities that, as part of the network, offer permanent or temporary logistics services such as warehousing, transshipment, maintenance, and refueling to other participating nations. The goal is to create a robust logistical "spine" along strategic deployment routes, reducing response times, increasing capacities, and enhancing the sustainability of military operations, from exercises to real-world scenarios.

Related to this:

Function and control

The coordination of this complex network takes place on two levels. Each participating nation establishes a national access point (nAP), which serves as an interface for requests and offers. The central coordination of the entire network, i.e., the coordination of material and movement flows, is carried out by the Joint Coordination Centre (JCC), located at the Bundeswehr Logistics Center in Wilhelmshaven and established specifically for this PESCO project. Importantly, the network is explicitly designed not as a competitor to existing NATO structures, but as a complementary and interconnected system. It is also open to the participation of third countries such as Canada, the United Kingdom, and Norway, which underscores its strategic importance.

Role of the NATO Joint Support and Enabling Command (JSEC)

The operational framework for military mobility in Europe is provided by NATO's Joint Support and Enabling Command (JSEC), headquartered in Ulm, Germany. As an operational command under the direct command of the Supreme Allied Commander Europe (SACEUR), JSEC is responsible for ensuring and securing the rapid and seamless movement of troops and equipment across national borders. JSEC thus acts as the primary strategic "customer" and user of the capabilities provided by the PESCO LogHub network. The creation of "military Schengen corridors" to minimize bureaucratic hurdles is one of the key objectives pursued by JSEC.

Opportunities for SMEs

The development of this logistics infrastructure opens up diverse business opportunities for small and medium-sized enterprises (SMEs). They can position themselves as highly specialized service providers for the individual LogHubs. Possible niches include, for example, the development and implementation of secure IT and warehouse management systems, the provision of specialized maintenance and repair services for specific weapon systems, the supply of innovative surveillance and security technology for the hubs, or the flexible provision of civilian transport capacities within the framework of dual-use concepts.

Dual-use logistics: The intelligent integration of civilian and military capabilities

Definition and advantages

Dual-use logistics refers to the use of goods, technologies, and processes that can be employed for both civilian and military purposes. This approach offers enormous strategic advantages. By accessing the capacities of the civilian logistics market—from freight forwarders and warehouses to IT systems—armed forces can make their own logistics more flexible, resilient, and cost-efficient. Studies indicate potential cost savings of up to 20 percent. Particularly during peak loads, such as those that occur during large troop movements or in crisis situations, the involvement of civilian partners enables a massive expansion of available capacities. At the same time, this collaboration leads to a significant technology transfer: Civilian logistics benefits from the military's high cybersecurity standards, while the military can learn from the efficiency- and automation-oriented processes of the civilian sector.

Related to this:

Challenges and Regulation

The use of dual-use goods and services is subject to strict legal controls to prevent their misuse for undesirable purposes. The EU Dual-Use Regulation and national laws, such as the German Foreign Trade and Payments Act, precisely regulate the export of such goods and technologies. Companies operating in this sector must ensure full compliance and generally require export licenses from the Federal Office for Economic Affairs and Export Control (BAFA). This regulatory complexity presents a significant challenge, particularly for SMEs.

Intermodality and interoperability as a core problem

Maximizing deployment speed requires seamless intermodal transport chains that intelligently link modes of transport such as road, rail, ship, and air freight. However, this encounters significant obstacles, particularly in cross-border transport within Europe, due to a lack of technical and procedural interoperability.

Deep Dive Rail Transport

Rail transport is ideally suited for transporting heavy military equipment over long distances, but in Europe it suffers from historically developed fragmentation. The biggest obstacles to smooth military rail transport are:

Different track gauges: While most of Europe uses the standard gauge of 1,435 mm, the Iberian Peninsula and the successor states of the Soviet Union (including Ukraine and Belarus, bordering NATO's eastern flank) use a broad gauge of 1,520/1,668 mm. This necessitates time-consuming and costly transshipment of goods or gauge-changing of wagons at borders.

Different power and signaling systems: The diversity of operating and safety systems is even more significant. In Europe, there are four different power systems (e.g., 15 kV AC in Germany, 3 kV DC in Poland) and over 20 different national train protection systems (e.g., PZB in Germany, TVM in France). This forces locomotives to stop and often change systems at almost every border.

Technological solutions exist and are increasingly being implemented. The European Train Control System (ETCS) is being introduced as a uniform digital standard for train protection throughout Europe and is intended to replace the national, isolated systems in the long term. Modern multi-system locomotives are capable of operating under different power and signaling systems, thus significantly reducing waiting times at borders. For the problem of different track gauges, there are automatic gauge-changing systems (e.g., the systems from Talgo or Rafil/DB AG) that allow specially equipped wagons to adjust their track gauge while slowly passing through the system. SMEs can play a crucial role in this area as highly innovative suppliers of components for ETCS, software for multi-system locomotives, or mechatronic systems for gauge-changing facilities.

Technological revolution in buffer storage: System terminals and automated high-bay warehouses (HBS)

Problem of traditional container storage

The LogHubs and terminals along the deployment corridors serve as buffer storage and transshipment points. However, traditional container terminals, where containers are stacked flat and only a few layers high, are space-intensive and inefficient. Accessing a specific container located at the bottom or in the middle of a stack often requires the time-consuming restacking of several other containers ("unproductive movements"). For military logistics, where rapid access to specific equipment is crucial, this is a significant disadvantage.

The HBS concept

Automated high-bay storage (HBS) systems offer a revolutionary solution for container storage. Instead of stacking containers, they are stored in a huge, steel racking system that can be up to 11 or more levels high. Storage and retrieval are fully automated by stacker cranes and shuttles controlled by intelligent software.

Analysis of the decisive advantages for military logistics

This technology offers a quantum leap for the requirements of defense logistics:

100% direct access: The crucial advantage is that every single container is directly accessible at any time without having to move any other container. This allows for a drastic acceleration in the provision of specific military supplies – be it ammunition, spare parts, or medical supplies.

Efficiency and speed: HBS systems reduce truck handling times by up to 20 percent and almost completely eliminate unproductive container movements. This significantly increases a terminal's throughput.

Safety and sustainability: Fully automated and purely electric operation minimizes the risk of accidents involving personnel, reduces noise, and eliminates local emissions. The large roof areas of the facilities are ideally suited for the installation of photovoltaic systems, enabling the terminals to cover part of their own energy needs.

Space efficiency: An HBS requires significantly less floor space than a conventional warehouse with the same capacity. This is a crucial advantage in strategically important but often space-constrained areas such as ports or military logistics centers.

Suppliers and SME potential

Leading providers of this technology include companies such as BOXBAY (a joint venture between DP World and SMS group), Amova (which has already implemented a warehouse for the Swiss Army), and Konecranes. This presents diverse opportunities for SMEs, either as highly specialized suppliers for HBS manufacturers (e.g., in the areas of sensors, control technology, mechatronics, and steel construction) or as developers and providers of complementary software solutions, such as for warehouse management, IT security, or the integration of the HBS into overarching military logistics networks.

Building a robust physical logistics infrastructure in the form of log hubs and strategic corridors is therefore only one side of the coin. The full potential of this infrastructure can only be unlocked if the technological and procedural bottlenecks that impede traffic flow are systematically eliminated. This requires a holistic approach: investments in physical infrastructure must be synchronized with investments in technological enablers that solve interoperability problems along the route (ETCS, gauge-changing facilities) and efficiency problems at the hubs (automated HBS). For SMEs, this means that the most lucrative market opportunities often lie not in operating large-scale logistics, but in developing and providing these highly specialized technological bottleneck solvers. A sales alliance between an SME specializing in rail technology and an SME specializing in HBS software, for example, could offer a highly innovative, integrated solution for modernizing a log hub, thereby securing a decisive competitive advantage.

🎯🎯🎯 Benefit from Xpert.Digital's extensive, five-fold expertise in one comprehensive service package | BD, R&D, XR, PR & Digital Visibility Optimization

Benefit from Xpert.Digital's extensive, five-fold expertise in a comprehensive service package | R&D, XR, PR & Digital Visibility Optimization - Image: Xpert.Digital

Xpert.Digital possesses in-depth knowledge across various industries. This allows us to develop tailored strategies precisely aligned with the requirements and challenges of your specific market segment. By continuously analyzing market trends and monitoring industry developments, we can act proactively and offer innovative solutions. The combination of experience and expertise generates added value and provides our clients with a decisive competitive advantage.

More information here:

Platform power and smart supply chains: The key to national security

The digital dimension – platform economy and artificial intelligence

The ecosystem of the future: Platform-based sales partnerships

From analog to digital collaboration

Traditional collaboration in the defense and logistics industries is often characterized by isolated IT systems, manual processes, and paper-based communication. This lack of digital continuity hinders efficiency, slows responsiveness, and complicates inter-company cooperation, ultimately stifling innovation. To meet the complex demands of modern defense logistics, a paradigm shift toward networked, digital ecosystems is necessary.

Conception of a digital B2B ecosystem

The vision is a central, cloud-based B2B platform that acts as the digital nervous system for European defense logistics. Such a platform functions as a "digital marketplace" and "collaboration space," connecting all relevant stakeholders – armed forces as the end users, logistics service providers, transport companies, maintenance firms, suppliers, and systems integrators. It enables the real-time exchange of demand and capacity information, thus creating unprecedented transparency across the entire supply chain.

Core functions of the platform

Such a platform would rest on three pillars:

Transaction focus: The platform facilitates logistics contracts, from tendering and awarding to tracking and invoicing. An SME could offer its available transport capacity, and a military entity could find the most suitable and available service provider in real time.

Networking focus: It offers a secure digital space where companies can form consortia and alliances for specific projects. The platform would facilitate partner searches and support cross-company collaboration through standardized communication and project management tools.

Data focus: Similar to initiatives like Catena-X in the automotive industry, the platform would be based on creating shared data spaces and standardized interfaces. This enables the secure and seamless exchange of critical data, be it technical specifications, transport documents, customs data, or compliance certificates. A "digital twin" of the logistics chain could thus be created, enabling comprehensive monitoring and control.

Advantages for SMEs

For small and medium-sized enterprises, participation in such an ecosystem would be a fundamental game-changer:

Transparency and market access: SMEs could present their specialized skills and capacities to a wide range of potential clients and partners, thereby drastically increasing their visibility in the market.

Efficiency: The administrative effort involved in preparing offers, processing orders and providing compliance documentation would be significantly reduced through digitized and standardized processes.

Automation: The platform could automate processes such as lead generation, the creation of offers based on standardized parameters, and invoicing, freeing up valuable resources for SMEs.

Artificial intelligence as a strategic enabler in defense logistics

Artificial intelligence (AI) is the key technology for transforming a networked platform into an intelligent, proactive ecosystem. AI goes beyond simply automating rules; it uses algorithms that can learn from data, recognize patterns, and adapt to new situations.

Related to this:

AI for process automation and optimization

Integrating AI modules into the logistics platform's workflows enables the automation of complex tasks. AI can automatically classify incoming documents (e.g., waybills, customs documents) and extract relevant data, dynamically prioritize transport requests, and detect supply chain anomalies (e.g., unexpected delays) in real time. This relieves human dispatchers of routine tasks, allowing them to focus on resolving critical issues.

AI in Supply Chain Optimization

The greatest potential of AI lies in the strategic optimization of the entire supply chain:

Predictive analytics: By analyzing historical and current data, AI systems can make precise predictions. They can anticipate peak demand for certain supplies, identify potential supply chain bottlenecks early on (e.g., by evaluating geopolitical news and weather data), and predict the optimal time for vehicle and infrastructure maintenance (predictive maintenance) before a failure occurs.

Dynamic route planning: AI algorithms can calculate and adjust the most efficient transport routes in real time. They take into account a multitude of variables, including current traffic and weather conditions, the availability of rest and refueling facilities, as well as specifically military factors such as the current threat level, convoy regulations, and the load-bearing capacity of bridges.

Autonomous control: The long-term vision is a largely autonomously controlled supply chain. An AI system could independently react to disruptions by rerouting shipments, activating alternative suppliers, or dynamically shifting inventory levels to ensure security of supply at all times.

Opportunities for SMEs through AI

Here, too, immense opportunities open up for agile SMEs. Instead of trying to compete with the large tech companies in developing basic AI models, they can concentrate on developing and offering highly specialized niche AI solutions. Examples include algorithms for optimizing the loading of military transport vehicles, taking into account center of gravity and unloading sequence; AI-based tools for detecting cyberattacks on logistics networks; or predictive analytics models for the maintenance of specific weapon systems. Through such specialized contributions, SMEs can position themselves as indispensable technology partners in the digital supply chain.

Physical logistics is fragmented and plagued by technical hurdles, while traditional collaboration is complex and fraught with high costs and risks. A digital, AI-powered logistics platform can address these fundamental problems. It creates a unified digital space where standardized data flows, resolving interoperability issues at the information level. It efficiently processes transactions, reducing costs and facilitating collaboration within alliances. Artificial intelligence adds the crucial layer of "intelligence" to this system. It enables not only networking but also proactive, optimized, and data-driven decision-making.

The future of distribution alliances therefore no longer lies solely in bilateral agreements, but in active participation in such a digital ecosystem. For SMEs, the ability to connect to this platform and exchange data securely and efficiently will become a core strategic competency. This raises a crucial question for Europe: Who develops, operates, and controls this critical digital infrastructure? To prevent the dominance of a few large players and to create a fair, transparent marketplace that grants access, especially to SMEs, an open, EU-funded initiative – similar to projects like Gaia-X or Catena-X – would be of paramount strategic importance.

Related to this:

Technological niches as a competitive advantage: New approaches in defense logistics

Strategic recommendations for SMEs, policymakers and established industry players

To fully leverage the potential of small and medium-sized enterprises (SMEs) as drivers of innovation in European defense logistics, concerted efforts from all stakeholders are needed. The formation of strategic sales alliances is a key lever, but their success depends on the right framework conditions.

For SMEs

Strategic positioning: SMEs should focus on technological niches where they can fully leverage their agility and innovative strength. This includes, in particular, future-oriented fields such as specialized AI applications, cybersecurity solutions for logistics networks, innovative components for rail interoperability, or software for automated warehouse systems.

Proactive partner search: Instead of passively waiting for inquiries from large corporations, SMEs should actively seek complementary partners – be it other SMEs to form powerful consortia or system integrators where their technology offers clear added value. Building trust and personal networks is crucial here.

Investing in "readiness": The ability to meet the high demands of the defense sector must be understood as a strategic competitive advantage. This includes investments in internal cybersecurity, the implementation of quality management systems (e.g., ISO 9001), and building expertise in export control and other compliance regulations.

Utilizing funding instruments: SMEs must actively utilize the diverse funding and networking opportunities offered by the EU and national governments. While this requires an initial investment, it can provide the crucial impetus for market entry or growth.

For politics (EU and national)

Procurement reform: Tendering procedures urgently need to be simplified, accelerated, and made more accessible to SMEs. This includes dividing large projects into smaller lots, reducing bureaucratic hurdles, and giving greater consideration to innovation potential instead of solely relying on the references of established suppliers.

Targeted support: Instruments such as the European Defence Fund (EDF) and, in particular, the EU Defence Innovation Scheme (EUDIS) must be consistently aligned with the needs of SMEs and provided with robust funding. Access to these funds must be low-threshold and unbureaucratic.

Promoting digital ecosystems: Policymakers should actively promote and shape the development of an open, standardized, and secure digital logistics platform for the European defense sector. This will create a fair marketplace and prevent the emergence of monopolistic structures.

Improving financing conditions: A clear political stance on the ESG classification of investments in the security and defense industry is essential to facilitate SMEs' access to private venture capital and bank loans. Cooperation between public development banks such as the EIB and KfW and commercial banks must be further expanded.

For system houses and large companies

Building fair partnerships: Large system integrators should view SMEs not merely as interchangeable suppliers, but as strategic innovation partners. This requires transparent contract models, a fair distribution of risk, and recognition of the SMEs' intellectual property.

Creating open system architectures: Instead of closed, proprietary systems, large companies should create open interfaces (APIs) that make it easier for innovative SMEs to connect and integrate their solutions and technologies.

Taking on mentoring roles: System integrators can leverage their immense experience to support their SME partners in complex certification and compliance processes. This creates a win-win situation, as it makes the entire supply chain more resilient and efficient.

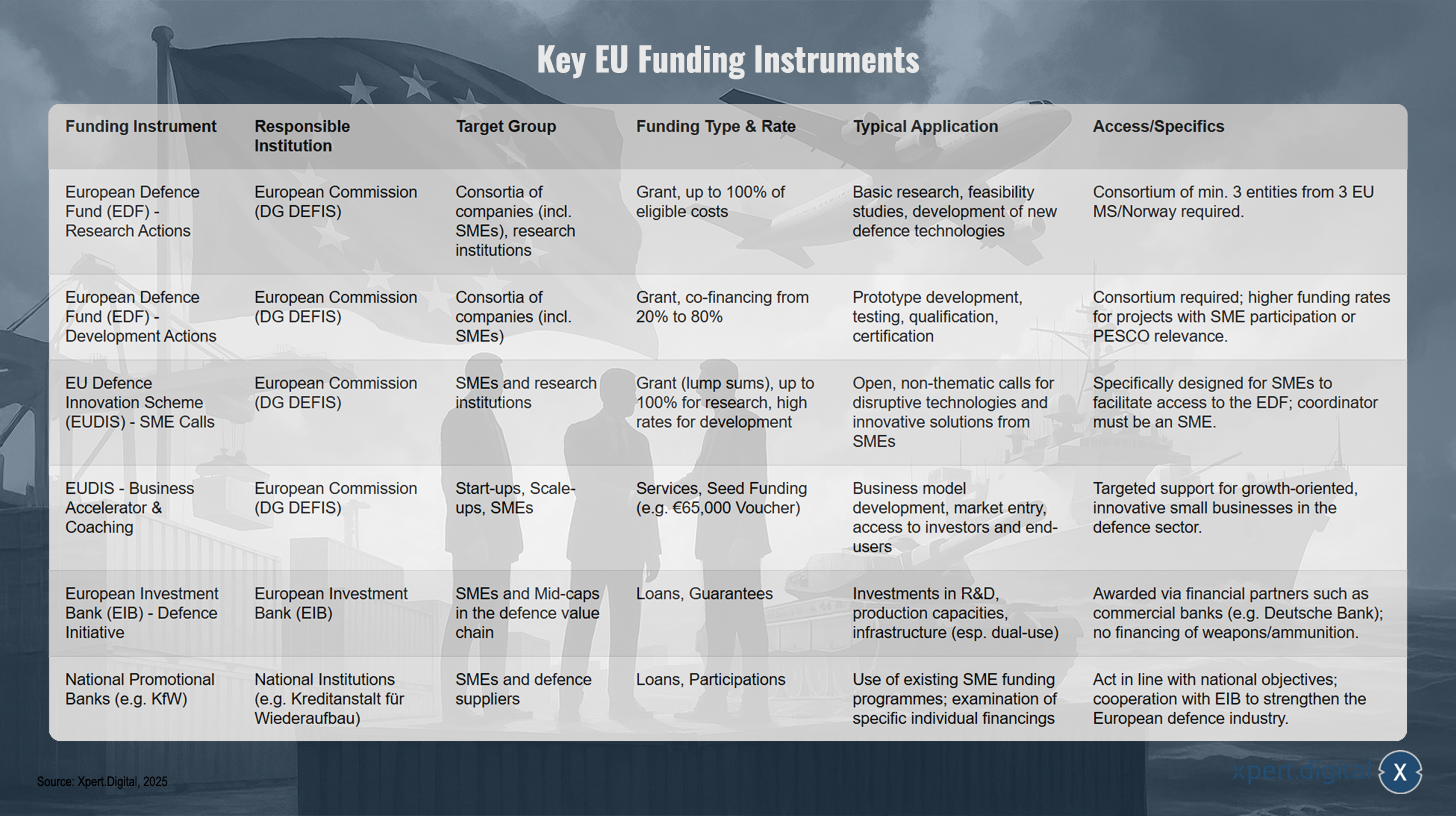

The following table provides SMEs with a practical overview of the most important EU funding instruments to facilitate their entry into the complex funding landscape.

Key EU funding instruments

Key EU funding instruments – Image: Xpert.Digital

The European Union offers various funding instruments for defense technology and innovation, specifically tailored to different stakeholders and needs. The European Defence Fund (EDF) comprises two main areas: research actions and development actions. Research actions cover up to 100% of eligible costs for basic research and feasibility studies, requiring collaboration between at least three institutions from three EU Member States or Norway. Development actions focus on prototype development, testing, and certification, with co-financing rates ranging from 20% to 80%.

The EU Defence Innovation Scheme (EUDIS) specifically targets small and medium-sized enterprises (SMEs). It offers open calls for proposals for disruptive technologies and innovative solutions, with SMEs acting as coordinators. Additionally, there is a business accelerator with coaching services and seed funding to support growth-oriented companies in the defence sector.

In addition, financing instruments such as the European Investment Bank (EIB) Defence Initiative are available, providing loans and guarantees for investments in research, development, and production capacities. National development banks like KfW complete the range of support instruments and enable specific individual financing for SMEs and defense suppliers.

Towards an integrated, agile and resilient defense logistics ecosystem

The “turning point” requires more than just increased defense spending. It demands a fundamental shift in how Europe designs, develops, and maintains its defense capabilities. The central thesis of this article is that the future of effective European defense logistics depends on the successful integration of highly innovative small and medium-sized enterprises (SMEs). The key to this integration lies in the formation of strategic, digitally supported distribution alliances.

The vision is a networked European defense logistics ecosystem in which physical infrastructure – such as the PESCO LogHub network and strategic deployment corridors – is seamlessly linked with technological enablers like automated high-bay warehouses and interoperable rail systems. This system is controlled and optimized by a digital nervous system: an AI-powered collaboration platform that creates real-time transparency and enables agile, cross-company cooperation.

In such an ecosystem, SMEs can fully leverage their strengths. They are no longer merely dependent suppliers, but agile, networked, and indispensable partners, contributing specialized technologies and services where they create the greatest added value. The alliances they forge are no longer simply bilateral, rigid contracts, but dynamic, project-based collaborations within a digital marketplace. Realizing this vision is a monumental task that must overcome technological, political, and cultural hurdles. However, it is essential to achieving the speed, resilience, and efficiency required to guarantee national and collective defense in the 21st century.

Consulting - Planning - Implementation

Markus Becker

I would be happy to serve as your personal advisor.

Head of Business Development

Chairman SME Connect Defense Working Group

Consulting - Planning - Implementation

Konrad Wolfenstein

I would be happy to serve as your personal advisor.

You can contact me at wolfenstein∂xpert.digital or

Just call me on +49 7348 4088 965 .