Coil storage – more than just steel coils: The smart slitting strip storage system as the key to fully automated slitting strip production and logistics – Image: Xpert.Digital

How modern coil storage reduces years of delivery time for transformers

Weighing tons and extremely sensitive: The true bottleneck of the global energy transition

Delivery times of up to 5 years: Why the global transformer boom needs a new logistics system

The world is facing an unprecedented wave of electrification. Driven by the energy transition, the rapid expansion of data centers for artificial intelligence, and the urgently needed modernization of outdated power grids, global demand for transformers is exploding. But while demand is growing exponentially and delivery times are increasing to up to five years, a massive bottleneck is emerging in manufacturers' factories: intralogistics. The heart of every transformer – the so-called grain-oriented electrical steel (slit strip) – presents manufacturing companies with enormous challenges. The strips, wound into coils, weigh up to five tons, yet are so delicate that even the smallest scratches or pressure marks lead to measurable energy losses and thus to costly scrap. Anyone still managing this balancing act between heavy loads and millimeter precision manually or semi-automatically not only loses valuable time but also risks the profitability of their entire production. The solution lies in fully automated cantilever high-bay warehouses that handle the heaviest loads with maximum process reliability. The following article shows why smart heavy-duty intralogistics is no longer just an option, but the crucial strategic lever to meet the enormous demand of the future.

Fully automated intralogistics in transformer manufacturing

When the energy transition hinges on the warehouse – Why no transformer in the world can function without precise slit strip logistics

The global transformer market is experiencing exceptional growth, fueled by several megatrends simultaneously. The market was valued at approximately US$63.8 billion in 2024 and is projected to reach US$122.7 billion by 2034 – representing a compound annual growth rate (CAGR) of over 6.6 percent. Other market analysts anticipate even more dynamic growth: Fortune Business Insights forecasts a market size of US$137.72 billion by 2032, corresponding to a CAGR of nearly 10 percent.

Drivers of this development include the modernization of global power grids, the integration of renewable energies, the expansion of electrification, and the massively increased industrial electricity demand. Added to this are the demand peaks caused by the worldwide boom in data centers, fueled by rapidly growing artificial intelligence, and Russia's war against Ukraine, which has reassessed security of supply in Europe and triggered massive investments in grid infrastructure.

For Germany alone, an analysis by the University of Wuppertal, commissioned by BDEW and ZVEI, has determined that more than 500,000 new transformers will be needed by 2045 – just for the conversion from medium to low voltage, representing almost 80 percent of the current stock. For the conversion from high to medium voltage, more than 5,000 units, around 70 percent of the existing stock, will need to be newly constructed, upgraded, or replaced. The entire grid expansion in Germany by 2045 will require investments of an estimated €328 billion for transmission networks alone and a further €323 billion at the distribution network level.

These figures reveal a systemic challenge: Demand is growing exponentially, while the production capacities of transformer manufacturers are not keeping pace. Average delivery times for power transformers, which were six to eight months in 2021, have increased to three to four years – and for large-scale installations in parts of Europe, to as much as five years. Transformer prices in some segments have reached 2.6 times their pre-pandemic levels. Therefore, anyone producing transformers today is doing so under immense pressure to meet expectations and with virtually guaranteed full capacity utilization for years to come.

The heart of every transformer: Grain-oriented electrical steel and its special requirements

To understand why intralogistics in transformer manufacturing places such exceptional demands on the process, one must understand the key raw material: grain-oriented electrical steel, also known as transformer steel or slit strip. This material is an iron-silicon alloy with a silicon content typically ranging from 1 to 4.5 percent by weight. Its defining characteristic is that a complex rolling and annealing process aligns the iron crystals in a preferred direction – the so-called grain orientation.

This grain orientation is the decisive technological advantage. Grain-oriented electrical steel exhibits significantly higher magnetic conductivity than non-grain-oriented variants, and the remagnetization losses are considerably lower. In practice, this means that transformer cores made of this material operate more efficiently, generate less heat, and allow for more compact designs. The relevant standard is DIN EN 10107 for grain-oriented electrical steel. Measured by its economic importance, this material is the most significant soft magnetic material overall – with a global annual production of approximately 10 million tons.

The raw material is rolled into thin sheets of 0.1 to 1 millimeter – the thinner, the lower the energy losses during subsequent transformer operation. These extreme wall thicknesses, combined with their high weight, make the material exceptionally challenging to handle. The strips are wound onto coils without a spool, meaning they lack a load-bearing inner tube. Laying them on the outer shell would inevitably cause deformations and surface damage that would permanently impair the material's magnetic properties. Every dent, every pressure mark, every scratch on the material can lead to measurable losses in the finished transformer.

thyssenkrupp Materials Processing Europe offers slit strip from 0.20 millimeters thick, achieving burrs of less than 0.020 millimeters – less than ten percent of the material thickness. These precision requirements continue throughout the entire value chain: from the rolling mill to the slitting center and on to the transformer plant, which uses the material for winding the transformer cores. Once damaged, strip is generally irreparable – it is scrap and therefore a direct economic loss.

The logistical challenge: weighing tons, fragile, and with diverse dimensions

Anyone handling slit strip for transformers faces a seemingly contradictory combination of requirements: the material weighs many tons yet is highly sensitive. Coils for transformer manufacturing can reach weights of up to five tons. At the same time, the strips are available in a wide variety of widths, thicknesses, and diameters – each dimension corresponding to different specifications for different transformer types.

In a modern transformer core cutting center, a single coil measuring 1.4 meters in length and 1.1 meters in diameter is split into up to 14 smaller coils of varying dimensions. These 14 subsequent coils must then be identified, sorted, temporarily stored, and made available at the right time for the correct production step. Managing this process manually or semi-automatically risks mix-ups, damage, and, above all, production interruptions—in a market environment where delivery times of three to five years for transformers dramatically increase the cost of any delay in the manufacturing process.

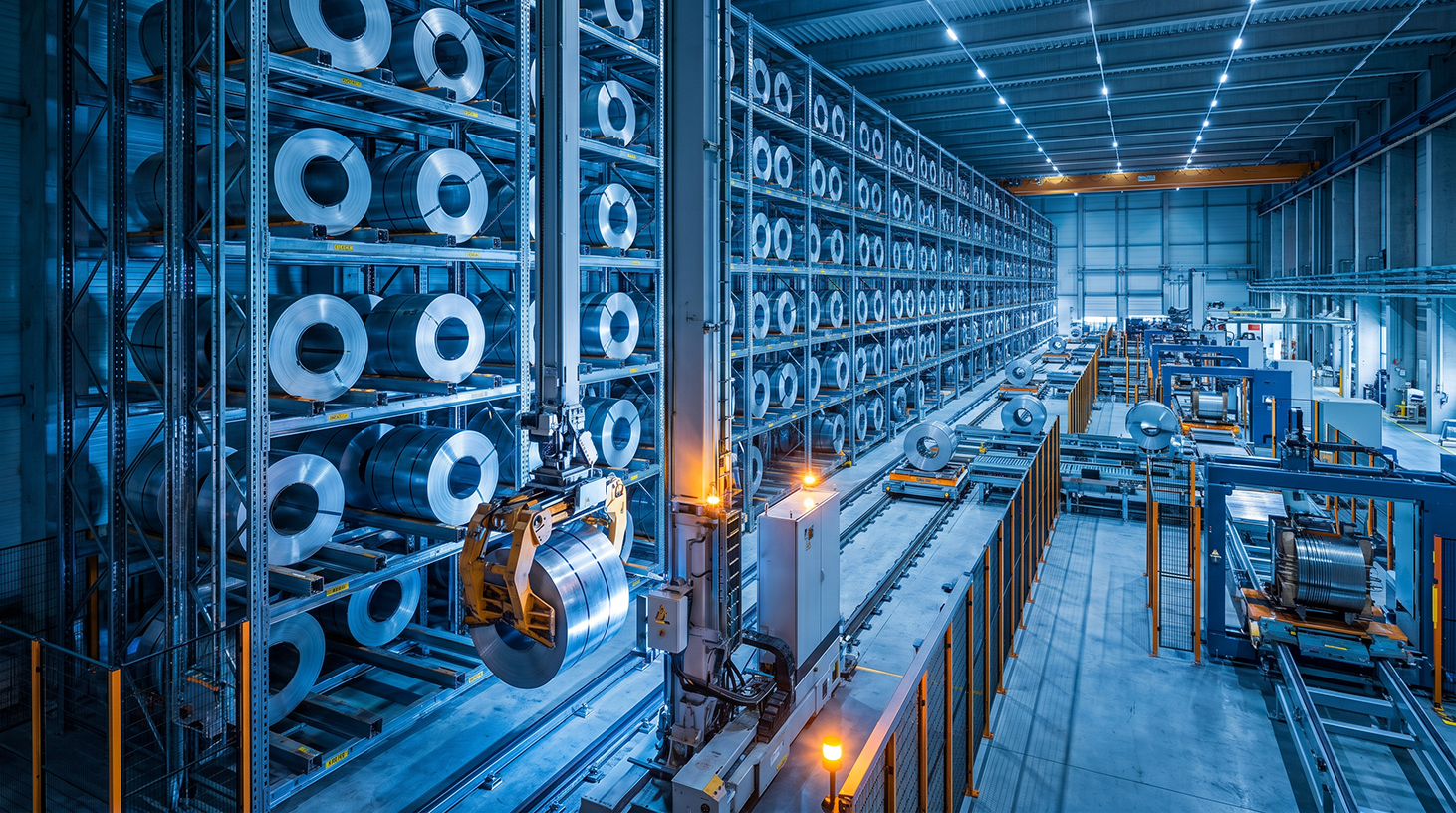

The specific storage challenge for slit strips without an inner mandrel has been technically solved: The strip must be supported on cantilever arms – meaning it is supported from the inside, without any pressure on the sensitive outer sheath. This sounds simple, but places high demands on the precision of the handling systems. Storage and retrieval machines must not only move loads weighing many tons, but do so with millimeter accuracy – at travel speeds of up to 2.5 meters per second. Storage must be possible from both sides of the high-bay warehouse, as must retrieval. Specially developed rotary-push forks solve this problem: They allow storage from both sides of the high-bay warehouse and, in combination with the lifting platform of the storage and retrieval machine, enable the coil to be gently lowered onto the cantilever arms.

In addition, correct sequencing is required. In transformer manufacturing, the order in which tapes are delivered to the production lines is not arbitrary. Different production lines require different material specifications at different times. The warehouse management system must therefore not only manage storage locations but also anticipate the entire production flow and proactively organize the material supply – a complex task that cannot be solved without sophisticated software at multiple control levels.

Fully automated solutions: How modern heavy-duty intralogistics is transforming production

The leading approach to this complex logistics task is the fully automated cantilever high-bay warehouse in combination with stacker cranes and transfer platforms. This system combination enables a continuous, automated material flow from the receipt of the delivered coils through intermediate storage to sequential provision at the production lines – and even the return storage of the smaller coils produced from a larger coil.

The specific reference project that exemplifies the technical capabilities of this solution class is a fully automated cantilever storage system for a transformer core cutting center in Tianjin, northern China. The plant, which upon completion will house one of the largest such machining centers in China, was equipped with a complete storage and material flow system. Its central component is a fully automated, 150-meter-long and 11-meter-high high-bay warehouse with seven levels, 1,500 coil storage locations, and 90 production buffer locations. Two stacker cranes handle storage and retrieval, while five upstream transfer platforms with outfeed pallet trucks connect to the production lines.

The warehouse management system operates on two control levels: An intelligent Level 2 system positions the coils freely within the high-bay racking, optimizing for short travel distances. The higher-level Level 3 system determines which coil is intended for which work step and coordinates the entire material flow with the overall production planning. The system is designed for redundancy – both stacker cranes can serve all input and output stations, so that the failure of one unit does not bring operations to a standstill. With travel speeds of up to 2.5 meters per second, each stacker crane achieves 18 double cycles per hour.

The fact that this manufacturer of intralogistics solutions for heavy-duty applications was commissioned a second time by the same Chinese customer – TBEA, the world's largest transformer manufacturer, whose production capacity ranks first in China and third worldwide – demonstrates the trust that such systems inspire in practice. Within three years, TBEA awarded a second contract for the construction of a fully automated storage and material flow system for steel coils, including a high-bay warehouse, designed to accommodate up to 32,000 steel coils in a twin plant.

Economics of Automation: Why Full Automation Is Not an Option, But a Necessity

The economic justification for fully automated intralogistics solutions in transformer manufacturing arises from the interplay of several factors which, in combination, develop an almost unstoppable logic.

Material value density is paramount. Grain-oriented electrical steel is a highly refined specialty product whose production requires several demanding rolling and annealing processes. A single production error due to incorrect material handling is costly – not only in terms of the direct material value, but also in the lost lead time of a production line that was waiting for precisely the right strip. In a market environment where fully booked transformer manufacturers must process every order as quickly as possible, every production interruption translates directly into lost revenue.

Secondly, space efficiency and area productivity play a crucial role. High-bay warehouses with seven or more levels utilize the full height of the building and, with a capacity of 1,500 or more storage locations, require a comparatively small footprint. Given today's typical industrial land prices – especially in urban areas and in China, where industrial land is limited and expensive – this space efficiency represents a significant economic advantage over manual, floor-based storage.

Thirdly, and increasingly dominantly, is the labor factor. According to a representative study by TMG Consultants, for which over 2,500 companies in the manufacturing industry were surveyed between March and July 2024, 94 percent of companies that have invested in automation solutions have already reported positive results. At the same time, the same study shows that 63 percent of the surveyed companies have not automated their intralogistics at all or only to a limited extent – an enormous potential for further automation. The shortage of skilled workers in the logistics sector is structural and is being exacerbated by demographic factors. Fully automated systems provide a solution by completely decoupling repetitive transport tasks from human labor.

Fourth: Process reliability and traceability. In transformer manufacturing, complete quality documentation is not optional, but mandatory. Every coil, its origin, its material properties, and its processing history must be fully traceable. A fully automated warehouse management system digitally and completely documents every step of the process – a manual system can only meet this requirement with a disproportionately high level of personnel effort, and never with the same reliability.

Fifthly, and finally: speed and throughput. With 18 double cycles per hour per storage and retrieval machine and a direct connection to the production lines via transfer platforms and buffer zones, a fully automated system enables just-in-time supply of production, which would only be approximately achievable with manual transport equipment such as forklifts – but with many times the personnel required and a significantly higher risk of accidents when handling loads weighing many tons.

LTW Intralogistics Solutions

LTW Intralogistics – Engineers of Flow - Image: LTW Intralogistics GmbH

LTW offers its customers not individual components, but integrated complete solutions. Consulting, planning, mechanical and electrotechnical components, control and automation technology, as well as software and service – everything is networked and precisely coordinated.

In-house production of key components is particularly advantageous. This allows for optimal control of quality, supply chains, and interfaces.

LTW stands for reliability, transparency, and collaborative partnership. Loyalty and honesty are firmly anchored in the company's philosophy – a handshake still means something here.

Related to this:

Niche market with power: How specialist suppliers are winning over the transformer industry

Technological depth: What distinguishes modern heavy-duty intralogistics

The complexity of fully automated intralogistics solutions for slit conveyor belts extends beyond the mechanics of stacker cranes and cantilever racks. The real differentiation lies in the systemic integration and the detailed engineering solutions, which only together enable the required level of process reliability.

A particularly illustrative detail is the transfer and pickup technology of the storage and retrieval machines. The specially developed rotary-push fork allows coils to be stored and retrieved on both sides of the high-bay warehouse – without having to reposition the storage and retrieval machine. The lifting platform of the storage and retrieval machine enables gentle vertical placement, while the rotary-push fork handles the horizontal transfer onto the cantilever arms. With loads of up to five tons, this mechanism must operate with millimeter-precise repeatability.

The cantilever racks themselves are tailored to the specific requirements of the slit strip. Cantilever arms are connected to the rack structure's uprights, creating the necessary storage levels that allow for easy storage and retrieval of even bulky materials of any length. The automated storage and retrieval (AS/RS) system is capable of moving items weighing up to 40 tons at speeds of up to 160 meters per minute. The contact surfaces of the cantilever arms are specially designed to prevent damage to the delicate silicon steel strip—typically through plastic or rubber pads that prevent pressure peaks.

The control architecture of fully automated systems is hierarchically structured and maps the decision-making logic at various levels. At the lowest level, the programmable logic controller (PLC) controls the individual actuators and drives. Above this is the material flow computer system (MFC), which orchestrates the coordinated movements of multiple devices and prevents collisions. The warehouse management system (WMS) at level two knows the complete inventory, its spatial arrangement, and its material properties. Finally, production planning at level three specifies orders and optimizes the sequence of material supply.

In addition, there is the safety technology: protective fences, light barriers at the processing lines, sliding doors, and a sophisticated zone safety concept securely separate the fully automated storage area from the manually accessible area. Modern systems also integrate condition monitoring of the mechanical components and enable predictive maintenance, which further increases the availability of the system.

Market dynamics and competition: A few specialists dominate a niche segment

The market for fully automated intralogistics solutions in the heavy-lift segment – particularly for coils and slit strips in transformer manufacturing – is a distinct niche segment with high barriers to entry and few truly high-performing suppliers. Only a handful of companies worldwide possess the combined expertise in heavy-lift handling, logistics software know-how, plant-specific engineering, and international project management.

Vollert Heavy Duty Solutions, based in Weinsberg (Baden-Württemberg), is one of the most prominent examples of a German specialist in this segment. The company, with a 100-year history, develops customized storage systems for heavy-duty applications ranging from 5 to 50 tons and has demonstrated its international expertise in transformer intralogistics with reference projects for TBEA in China. The company underwent insolvency proceedings in 2025 and relaunched on January 1, 2026, as Vollert Heavy Duty Solutions GmbH, with the Czech PKD Holding as its strategic partner. Managing Director Hans-Jörg Vollert continues to lead the family-owned business. The focus is now even more sharply on heavy-duty intralogistics solutions and shunting systems.

In the broader market environment, specialists such as AMOVA, which focuses on automated coil transporters (ACT) and high-bay warehouses for the steel industry, and CTI Systems, which offers high-bay warehouses with honeycomb and cantilever racks for coils and spools, are active. General intralogistics automation is served by broader providers such as Knapp, STILL, and others, who, however, are typically not present in the specific heavy-duty segment. Carl Stahl's handling system concept with the CSCH system pursues a different approach through certified load carrier systems.

The high barriers to market entry result from several factors. First, designing a fully automated heavy-duty storage system for sensitive slit strips requires a deep understanding of both logistics processes and material-specific requirements. Second, reference projects and proven reliability in practice are crucial selling points – an inexperienced supplier is rarely entrusted with a multi-million-dollar project. Third, international project execution, as in the case of the Chinese reference projects, requires the ability to integrate local partners while still assuming responsibility as the general contractor.

Global perspective: Asia as a high-growth core market

The geographical distribution of demand for fully automated intralogistics solutions in transformer manufacturing reflects global production structures. The Asia-Pacific region already dominated the global transformer market in 2024, accounting for 30.46 percent of the market share. China is by far the most important single market – both as a producer and as a consumer of transformers.

TBEA, the company mentioned above as a reference customer, is the most impressive example of Chinese transformer manufacturer scaling. With an annual production capacity of more than 80,000 MVA, the company is one of the world's largest transformer producers – and has therefore recognized the need to maintain its intralogistics at the same top level as its manufacturing processes. The awarding of a second contract to the same German specialist within three years sends a strong signal: once proven, these systems are consistently replicated.

A fundamental shift in demand is emerging for Europe, and Germany in particular. The investment requirements for the German electricity grid, exceeding €650 billion by 2045, will inevitably lead to an expansion of European transformer manufacturing. New production sites will need to be established – and each new site will require a high-performance intralogistics system from the outset. The demand raised by BDEW and ZVEI in October 2024 for the establishment of additional production sites in Germany with planning and investment security underscores this trend.

The Indian market is developing into another significant growth driver. TBEA already operates a manufacturing base in Gujarat for transformers, solar equipment, and cables. NLMK is building a new plant in India for the production of grain-oriented electrical steel with a capacity of 64,000 tons per year – and every new production plant for transformer core material sooner or later also generates demand for corresponding handling systems.

The bottleneck effect: When production fails due to logistics

An underestimated dimension of the global transformer supply crisis lies not only in manufacturing capacity, but also in the production efficiency of existing capacities. In a market where lead times of three to five years have become the norm, the question of whether a manufacturer can reduce these lead times to two or three years is of enormous commercial importance. The difference often lies in internal logistics efficiency.

A manually or semi-automatically organized slit strip storage system creates waiting times on the production lines if the required material is not provided on time or is in the wrong condition. It generates scrap if strips are damaged through improper handling. It creates planning uncertainty because inventory levels are not precisely known or correctly allocated. And it generates personnel costs, which, especially when dealing with loads weighing several tons, are also associated with significant occupational safety requirements.

A fully automated system systematically eliminates these sources of loss. The Level 2 warehouse management system knows each coil, its current storage location, its material properties, and its intended use. The Level 3 system proactively coordinates retrieval with production planning. Incorrect deliveries, which can occur in manual systems due to confusing visually similar coils, are prevented through automatic identification. The production lines are supplied just-in-time – neither too early, which leads to buffer problems, nor too late, which brings the line to a standstill.

For transformer manufacturers operating in a supply-driven market with long lead times, every increase in production efficiency translates directly into increased revenue: more finished transformers per year with the same production capacity, lower error rates and therefore less rework, and greater planning accuracy in order processing. Under these market conditions, investing in fully automated intralogistics is not a cost burden, but a strategic lever for increasing revenue.

Technology trends: Where is heavy-duty intralogistics headed?

The next stage of development in fully automated heavy-duty intralogistics lies in the deeper integration of artificial intelligence and data analytics. Where today's systems operate according to clearly defined rules and optimization algorithms, future systems will learn from operational data and continuously improve their decision-making logic.

Predictive maintenance is evolving from an add-on function to a core requirement. Storage and retrieval machines, which move loads weighing many tons with precision and at high speeds, are subject to considerable mechanical stress. Sensor systems that record vibrations, temperatures, and load changes and use this data to predict maintenance needs can prevent unplanned downtime – which is particularly costly in a fully automated, just-in-time production environment.

The integration of warehouse management systems with higher-level ERP systems is becoming tighter and faster. Where interfaces previously acted as bottlenecks, modern API architectures and cloud connections enable near real-time synchronous data exchange between production, logistics, and business management. The next step—directly connecting the warehouse management system to the ordering systems of coil suppliers—closes the gap between production logistics and procurement logistics.

Autonomous mobile robots (AMRs) for pre-transporting coils to the transfer points of the high-bay warehouse are increasingly complementing stationary systems. Driverless transport systems, which are not directly controlled by humans, take over transport within the production environment and further reduce the use of conventional forklifts. In the heavy-duty class up to five tons, which is typical for slit strips, the technical requirements for the use of AMRs can already be met today.

Strategic implications: What the market means for suppliers and customers

For transformer manufacturers investing in new production capacities today, the question of how internal material flow is organized is not a secondary detail, but a strategic decision with long-term consequences. Once installed, an intralogistics system shapes production processes for 15 to 25 years – during this time, product ranges will change, coil dimensions will adapt, and throughput requirements will increase. Flexibility and scalability are therefore just as important selection criteria as initial performance.

For providers of fully automated intralogistics solutions in the heavy-duty segment, the market situation described presents an exceptional growth opportunity. The structural boom in demand for transformers, combined with the growing awareness of the productivity levers of modern intralogistics and the relentless pressure of the skilled labor shortage, is generating a demand dynamic that extends beyond the normal economic cycle. Unlike cyclical investments in industrial goods, this trend is fundamentally anchored by the regulatory and infrastructural requirements of the energy transition.

The decisive differentiating factor in this market is proven expertise. A supplier who has demonstrably delivered and commissioned a fully automated cantilever warehouse for one of the world's largest transformer manufacturers – and who has successfully re-engaged the same customer three years later – stands on a different foundation than a competitor without comparable evidence. In a market where investments run into the millions and mistakes cannot be compensated for with contractual penalties, this kind of proven reliability is the strongest argument.

Fully automated intralogistics for transformer belts is not a niche topic limited to specialized circles. It is part of the answer to one of the most pressing questions of our time: How can we build enough transformers to enable the energy transition? The answer doesn't begin on the production line – it begins in the warehouse.

Consulting - Planning - Implementation

Konrad Wolfenstein

I would be happy to serve as your personal advisor.

You can contact me at wolfenstein∂xpert.digital or

Just call me on +49 7348 4088 965 .

Your intralogistics experts

Consulting, planning and implementation of complete solutions for high-bay warehouses and automated storage systems - Image: Xpert.Digital

More information here: