Labor migration: Between short-term necessity and long-term miscalculation? Why AI will radically change the demand for skilled workers

Xpert Pre-Release

Available in 27 languages 📢

Prefer Xpert.Digital on GoogleⓘPublished on: February 25, 2026 / Updated on: February 25, 2026 – Author: Konrad Wolfenstein

Labor migration: Between short-term necessity and long-term miscalculation? Why AI will radically change the demand for skilled workers – Image: Xpert.Digital

Skilled worker shortage in Germany: Between economic lull and structural time bomb? Or artificial intelligence as a game changer?

Is a major job revolution looming? Why companies will suddenly be looking for completely different skills in 2026

At first glance, it seems like a long-awaited sigh of relief for the German economy: at the beginning of 2026, the fewest companies in five years reported a shortage of qualified employees. But anyone who believes the problem is solved is mistaken. This apparent easing of the situation is a dangerous illusion – merely a symptom of an economy mired in stagnation and recession. Beneath the calm economic surface, the demographic time bomb continues to tick unabated. With the impending retirement of the large baby boomer generation, a gap of millions of workers is foreseeably opening up in the labor market, pushing the system to its absolute limits.

But instead of relying solely on the traditional panacea of mass immigration, a new and far more powerful player is coming into focus: artificial intelligence. While policymakers continue to rely on immigration programs that are partly based on completely outdated needs assessments and promote ethically questionable brain drain in already crisis-ridden developing countries, a fundamentally new picture is emerging. Current forecasts suggest that generative AI could close over 90 percent of the demographic gap by 2030 through gigantic leaps in productivity.

This comprehensive analysis sheds light on the German labor market at a historic turning point. It reveals which sectors remain under extreme pressure despite the economic downturn, why our current migration policy urgently needs to be re-evaluated, and why Germany is facing a radical paradigm shift: The path out of the crisis does not primarily lead through recruitment agreements in the Global South, but rather through the consistent use of AI, skills development, and a new era of productivity.

In short:

AI as a game-changer for workforce forecasting: The AI chapter shows that generative AI could save around 3.9 billion working hours by 2030 – which would close over 90 percent of the demographic gap of 4.2 billion hours. Current forecasts of skilled labor demand are considered potentially obsolete because they barely factor in the productivity effect of AI.

Brain drain and ethical responsibility: The immigration chapter deals extensively with the brain drain from developing countries, especially in healthcare (WHO Code, Philippines, Africa), the Rosa Luxemburg Foundation's criticism of the Triple Win program, and the question of whether it is cynical to poach skilled workers today when AI will foreseeably reduce the need.

Societal costs and realignment: The conclusion argues for a paradigm shift – away from the fixation on immigration as a panacea, towards AI and productivity as the primary lever for securing skilled workers.

The deceptive calm before the demographic storm

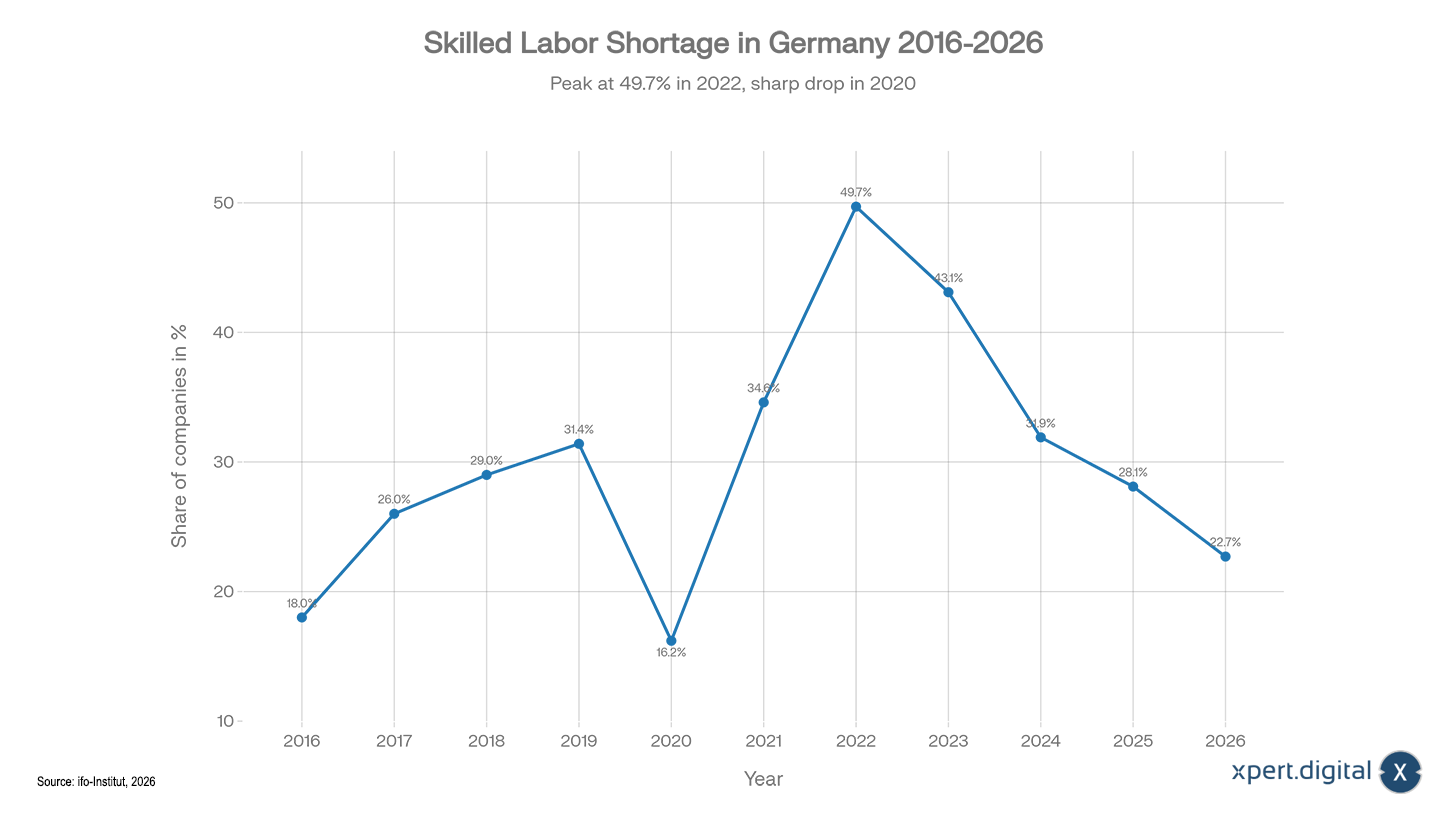

At first glance, the figures seem like a sign of relief: at the beginning of 2026, only 22.7 percent of German companies reported a shortage of skilled workers, the lowest figure in five years. In October 2025, this figure was still at 25.8 percent, and in the summer of 2022, it was almost 50 percent. But anyone who interprets this decline as a trend reversal is making an analytical error. This easing of the situation primarily reflects an economy that has been mired in recession, or at best stagnation, for three years now. It is not a sign that Germany has solved its skilled worker problem. On the contrary: the structural drivers of the shortage remain undiminished, and the moment the economy picks up speed again, they will return with full force.

This analysis paints a comprehensive picture of the current situation on the German labor market. It is based on the latest data from the ifo Institute, the Institute for Employment Research, the DIHK Skilled Workforce Report 2025/2026, as well as surveys by the German Economic Institute and other research institutions. The analysis focuses on the following questions: How should the current easing of the situation be interpreted? Which sectors remain under pressure? What role do demographics, digitalization, and immigration play? And which political and corporate strategies actually promise to be effective?

Decline in the skilled worker shortage – The deceptive calm before the demographic storm? – Image: Xpert.Digital

The economy as a painkiller: Why the numbers are misleading

The German economy has been experiencing one of its longest periods of weakness since the end of World War II since the end of 2022. Gross domestic product grew by only 0.2 percent in 2025, and various institutes forecast growth of between 1.1 and 1.4 percent for 2026. The unemployment rate climbed to an annual average of 6.3 percent in 2025 and is expected to remain at this level or decline only marginally in 2026. The number of employed persons stagnated in 2025 and is projected to fall in 2026 for the first time since the COVID-19 pandemic year of 2020, by approximately 18,000 to 20,000 people, according to IAB forecasts.

In such an environment, the pressure on skilled workers naturally decreases. When companies produce less, invest less, and hire fewer people, they also report fewer staffing shortages. The DIHK Skilled Workers Report 2025/2026 confirms precisely this: 36 percent of the nearly 22,000 companies surveyed reported difficulties filling vacancies, a decrease of seven percentage points compared to the previous year. At the same time, the proportion of companies that currently have no staffing needs at all rose from 44 to 48 percent. The weak economy thus has an effect on both sides of the equation: less demand leads to fewer reported shortages. This is not a solution, but rather an anesthetic.

Particularly revealing is the look at the skills gap, i.e., the number of jobs that cannot be filled with suitably qualified unemployed individuals. In the second quarter of 2025, this gap shrank by 17.9 percent compared to the same quarter of the previous year. For the first time since June 2021, there were even more qualified unemployed people than job vacancies in March 2025: 1.24 million compared to only 1.15 million open positions. Nevertheless, in June 2025, there was still a nationwide shortage of around 391,000 qualified workers. The gap has therefore narrowed, but it is by no means closed. In a period of economic weakness, this is an alarming signal, because this gap will widen considerably again during an economic recovery.

The industry landscape: Where the bottleneck remains and where it eases

An aggregated view of the skills shortage obscures the significant differences between individual economic sectors. The ifo Business Climate Survey from January 2026 provides a more nuanced picture, revealing the heterogeneity of the problem.

The situation remains most strained in the service sector. Roughly one in four service providers complains of staff shortages. By far the hardest hit are legal and tax consultancies and auditing firms, where 58.4 percent of companies report difficulties finding qualified personnel. In the summer of 2025, this figure was even higher at 72.7 percent. Temporary staffing agencies are also significantly overaffected, at 56.6 percent. This finding has deeper implications: Legal and tax consultancies are among the sectors that handle the bureaucratic red tape of the German economy. The fact that skilled workers are particularly scarce in this area indirectly and considerably exacerbates regulatory costs for all other companies.

The most noticeable change is in the transport and logistics sector. Here, the proportion of affected companies fell from 42.7 to 30.6 percent. This decline is likely due, on the one hand, to the weak order situation in logistics, and on the other hand, to increasing digitalization in scheduling and planning. However, industry experts warn against interpreting this as a sign that the situation is over: The bottleneck is shifting from quantitative to qualitative shortcomings. The demand is less for general workers and increasingly for specialists in IT, telematics, e-mobility, and data-driven logistics management.

In the industrial sector, 16.6 percent of companies report a shortage of skilled workers, half a percentage point less than in October 2025. Within the manufacturing sector, there are significant differences: mechanical engineering reports a shortage of around 19 percent, while the automotive sector and manufacturers of electrical equipment are considerably lower at just under 10 percent. The low figure in the automotive industry is not a sign of health, but rather a consequence of massive restructuring involving job cuts and hiring freezes. In an industry undergoing the most significant transformation in its history, a low shortage of skilled workers is paradoxically a symptom of a crisis.

The trade sector is experiencing a slight easing of the situation, with around 18 percent of companies affected. Retail trade is more severely impacted at 21.6 percent than wholesale trade at 16.2 percent. The construction industry, however, remains at a high level at 30.4 percent. This is due to the still-pending infrastructure projects and the physically demanding working conditions, which make the sector unattractive to young applicants.

The healthcare sector deserves particular attention. According to calculations by the German Economic Institute, it has the greatest shortage of skilled workers of all industries. In 2024, an average of around 46,000 qualified positions remained unfilled, especially for physiotherapists, nurses, and dental assistants. These shortages are immediately noticeable in everyday life: long waiting times for doctor's appointments, bed closures in nursing homes, and the overburdening of existing staff.

The demographic turning point: When the baby boomers leave

Beneath the economic surface lurks the real challenge: demographic change. Germany is reaching a critical turning point in these years that will shape labor market policy for decades to come.

The figures are clear: By 2036, around 19.5 million baby boomers will leave the labor market. At the same time, only about 12.5 million younger workers will enter the workforce. This creates a calculated gap of seven million people. The large birth cohorts between 1954 and 1969, in which over 1.1 million children were born annually in West Germany, are gradually reaching retirement age. The largest cohort, 1964, with 1.4 million live births, is at the heart of this exodus.

The Institute for Employment Research (IAB) has predicted a historic turning point for 2026: For the first time, Germany's potential labor force will decline in absolute terms, by approximately 35,000 to 40,000 people. This decrease may seem small at first glance, but it marks the beginning of a structural downward trend. The retirement of the baby boomers can no longer be compensated for by immigration and increased labor force participation. Enzo Weber, head of the IAB's forecasting research department, puts it clearly: The opportunities for job creation are severely limited compared to previous record increases.

The consequences extend far beyond the labor market. In 2022, there were just under 30 people over 67 for every 100 people of working age; by 2040, this number will be around 41. This so-called old-age dependency ratio is fundamentally shifting the financial basis of social security systems. Fewer working people will bear the costs of a growing number of pensioners, those requiring care, and patients. The German Economic Institute warns that the shortage of skilled workers could reach three million by 2030, while the skills gap could already exceed 700,000 by 2027.

The situation is particularly dire in the nursing sector. The Federal Statistical Office anticipates a need for approximately 180,000 additional nursing staff by 2049. Depending on the scenario, between 280,000 and 690,000 additional professional nurses could be required. The labor market reserve in professional nursing, which stood at 2.0 percent in 2025, will halve to 1.0 percent by 2027 and amount to only 0.5 percent by 2030. This means that in just a few years, there will be virtually no unused personnel reserves left in the nursing sector.

Artificial intelligence as a game changer: Why AI will radically change the demand for skilled workers

Artificial intelligence is not just another factor in the skilled worker debate; it has the potential to completely upend the entire calculation of demand. What is currently estimated as a skills gap of hundreds of thousands could take on a completely different dimension in just a few years, once AI-supported automation and productivity gains have reached their full potential. This realization has far-reaching consequences: The currently calculated demand forecasts, on which political decisions are based, could soon become obsolete.

The figures are impressive. According to OECD estimates, AI could theoretically automate up to 58 percent of individual tasks. A McKinsey study puts the proportion of potentially automatable working hours in Germany at around 18 percent by 2030. In practice, AI is currently changing primarily the nature of work, rather than the quantity. Qualification profiles are beginning to shift: There is an increasing demand for mixed skills that combine technical understanding with analytical thinking, communication, and creativity. The classic assumption from earlier waves of automation, that highly qualified individuals are less threatened by substitution, is being partially overturned by generative AI. Jobs in the middle and upper qualification ranges, such as in administration, accounting, or reporting, are coming under pressure to transform.

The decisive factor lies in the impact on productivity. Already, 82 percent of companies using AI in Germany report measurable productivity increases, averaging 13 percent per year. A study by the Cologne Institute for Economic Research (IW Köln) sees the potential for automation to increase productivity in Germany by up to 3.3 percent annually until 2030. Particularly noteworthy is the following calculation: the use of generative AI could save 3.9 billion working hours annually by 2030. This would close over 90 percent of the demographically driven gap, which the German Economic Institute (IW) estimates at 4.2 billion working hours. If this projection proves even remotely accurate, it would fundamentally alter the entire calculation of skilled labor needs. The currently projected gaps of 700,000 or even three million missing skilled workers are based on models that barely, if at all, factor in the AI productivity boost.

The impact on the IT sector itself is already measurable. The shortage of skilled IT professionals at IT service providers has fallen to 21.3 percent, down from around 50 percent two years ago. This is likely due not only to economic factors but also to the fact that AI-supported tools are massively increasing productivity in software development, data analysis, and IT administration. At the same time, one in twelve companies is specifically using AI to counteract the IT skills shortage. Around 27 percent of companies expect AI to lead to job cuts, and 16 percent anticipate that AI will make positions redundant that cannot be filled anyway. However, 42 percent expect AI to create an additional need for IT specialists within their companies. This shows that AI doesn't simply eliminate jobs but rather shifts the qualification requirements.

In a comprehensive research report, the IAB (Institute for Employment Research) simulated the employment effects of AI over a 15-year period. The result is remarkable: In the AI scenario, the total number of jobs remains at a similar level to that without AI. However, behind this stability lie massive shifts. In some sectors, such as IT service providers, the demand for labor increases by around 110,000 people, while it decreases by around 120,000 in business service providers. According to the IAB researchers, an AI-related reduction in the number of employed persons is not necessarily linked to a deterioration of the labor market situation: Scarce human resources could be used more efficiently in the long term, thus offering the potential to reduce labor shortages in other sectors.

This has a key implication for political planning: the speed of AI adoption will determine the true extent of the skills shortage in the coming years. Anyone currently sizing migration programs based on demand forecasts that assume a static level of productivity risks massive mismanagement. The German Academy of Science and Engineering (acatech) concludes that, under the criteria of human-centered work design with and through AI, the demographically driven net shortage of skilled workers could be significantly lower than currently assumed. This does not mean that AI will completely solve the skills shortage, but it does mean that current projections are subject to considerable uncertainty and will become increasingly less valid with each technological advancement.

Klaus Wohlrabe, deputy head of the ifo Center for Macroeconomics and Surveys, sums up the connection: The weak economic development plays a role in the current easing of the situation, but at the same time, technological change, especially artificial intelligence, is increasingly transforming the labor market. This transformation is only just beginning. If Germany creates the right framework for the adoption of AI, this could prove to be a more effective strategy against the skills shortage than any ambitious migration policy.

Our EU and German expertise in business development, sales and marketing

Our EU and German expertise in business development, sales and marketing - Image: Xpert.Digital

Industry focus areas: B2B, digitalization (from AI to XR), mechanical engineering, logistics, renewable energies and industry

More information here:

A thematic hub offering insights and expertise:

- Knowledge platform covering global and regional economies, innovation and industry-specific trends

- A collection of analyses, insights, and background information from our key areas of focus

- A place for expertise and information on current developments in business and technology

- A hub for companies seeking information on markets, digitalization, and industry innovations

Organized theft? The inconvenient truth about Germany's poaching of skilled workers

Immigration: Between short-term necessity and long-term miscalculation

The big miscalculation: Why AI is overtaking Germany's immigration strategy – technology instead of migration and the overlooked way out of the skilled worker crisis

Skilled immigration has developed dynamically since the Skilled Immigration Act came into force in March 2020. Labor migration has more than doubled since then: In June 2025, 420,000 employees subject to social security contributions held a residence or settlement permit based on their employment, compared to just over 200,000 in 2020. Roughly half of them came to Germany with an EU Blue Card. The number of Blue Card holders rose to around 164,000, representing an increase of 114 percent since 2020.

The 2023 amendment to the law brought further simplifications. Recognized skilled workers are now permitted to work in all qualified professions, the salary thresholds for the Blue Card have been significantly lowered, and its scope has been extended to include equivalent qualifications such as master craftsman, technician, and certified specialist. The new Opportunities Card also allows individuals to enter Germany to search for work even without a concrete job offer.

However, the migration strategy urgently needs to be reassessed in light of technological developments. If AI-supported automation can indeed close the demographic working-hours gap by over 90 percent, as calculations by the Cologne Institute for Economic Research (IW Köln) suggest, then the question arises whether the currently politically communicated need for hundreds of thousands of skilled workers per year is still justified in the medium and long term. A migration program based on demand forecasts that systematically underestimate the impact of AI does not produce solutions, but rather new problems: integration conflicts, cultural tensions, overburdened social systems, and a growing labor supply in sectors where demand is currently declining due to automation.

Even more serious is the ethical dimension. The systematic recruitment of skilled workers from developing and emerging countries has consequences that receive too little attention in the German debate. This so-called brain drain deprives the countries of origin of precisely those qualified individuals who are most urgently needed there. Research provides clear evidence: In most developing countries, especially in sub-Saharan Africa and Central America, the extent of the brain drain significantly exceeds economically efficient levels, resulting in substantial fiscal losses and serious depletion of human capital.

The healthcare sector provides a particularly striking example of this dilemma. According to the WHO, 57 countries, 36 of which are in sub-Saharan Africa, currently face a critical shortage of healthcare professionals. In some of these countries, there are fewer than 2.28 healthcare professionals per thousand inhabitants. At the same time, the WHO estimates that up to 10 million healthcare professionals are needed worldwide to achieve universal healthcare by 2030, with the shortage particularly affecting Africa and Southeast Asia. When Germany specifically recruits nurses, doctors, and therapists from these very regions to fill its own healthcare gaps, it exacerbates the crisis in the already fragile healthcare systems of the countries of origin. The Rosa Luxemburg Foundation refers to this as an organized theft of skilled workers, especially in the case of recruitment from Indian states like Kerala under the Triple Win program.

In 2010, the WHO adopted a global code of conduct for the international recruitment of health professionals, which sets out ethical principles and specifically recommends refraining from active recruitment in countries with critical shortages of healthcare workers. While the German government participated in the negotiations and signed this code, its implementation is voluntary and not legally binding. In practice, active recruitment continues, even in countries whose healthcare systems are under enormous strain. Germany has entered into placement agreements with countries such as the Philippines, Tunisia, Colombia, and India. In the Philippines, which specifically trains nurses for the global market, this leads, despite the export strategy, to a situation where rural areas remain underserved and the most qualified professionals leave the country. Criticism is growing within the Philippines itself: this brain drain is destabilizing the country's healthcare system.

This ethical dilemma becomes even more pressing in light of AI. If Germany is able to significantly reduce its demand for skilled workers through consistent AI adoption and automation, then the recruitment of skilled workers from the Global South loses a substantial part of its legitimacy. It would be cynical to recruit caregivers from Ghana, nurses from the Philippines, or IT specialists from India today when it is foreseeable that AI-supported diagnostics, robotic assistance in care, and automated administrative processes will significantly reduce the demand within a few years. The countries of origin bear the training costs, lose their best talent, and ultimately face exacerbated healthcare crises in their own countries, while the receiving industrialized nations could potentially have met the demand through technological innovation.

Added to this are the societal costs of immigration, which are often externalized in economic analyses. Integrating skilled workers from culturally distant regions of origin is complex, costly, and fraught with potential conflict. Language barriers, differing values, divergent work cultures, and the strain on social infrastructure in the host communities are real factors that do not appear in the simplistic needs assessments of labor market economists. If, in the end, a significant number of the recruited skilled workers are employed in professions that will disappear in the medium term due to automation or undergo fundamental changes, new integration problems will arise instead of solutions.

Demand already exceeds the available quota in some sectors. For example, in December 2025, the Federal Employment Agency had to reject approximately 18,000 applications for labor market permits under the Western Balkans Regulation, as the quota, which had been doubled to 50,000 annually, was already exhausted. At the same time, Germany is competing internationally for skilled workers with other industrialized nations that are also facing demographic pressure. This competition is driving up recruitment efforts globally and further exacerbating the brain drain from the regions of origin.

Immigration alone cannot fully compensate for the demographic decline. The IAB (Institute for Employment Research) calculates that, despite positive net migration, the potential labor force will decline in absolute terms for the first time in 2026. At the same time, there is a risk that a strategy primarily focused on immigration will reduce the pressure for reforms in automation, digitalization, and productivity improvement. If cheap labor is available from abroad, the incentive for companies to invest in AI and automation decreases. This would be disastrous in the long term, as it would cause Germany to fall further behind in international productivity competition.

A responsible skilled labor policy must therefore continuously adapt immigration strategies to technological realities. Forecasts that currently indicate a need for hundreds of thousands of additional workers per year must be regularly reviewed for their validity as AI penetration progresses. Clinging to outdated demand models that ignore technological change would not only be economically inefficient but would also exacerbate social tensions in receiving countries and development deficits in countries of origin. The most intelligent way to secure skilled workers is not to maximize recruitment from abroad, but to maximize the use of technological potential within the country.

Qualification and further training: The underestimated lever

In addition to immigration, the qualification of the existing workforce is a key aspect of the skilled worker strategy. In 2022, the German Federal Government adopted a cross-departmental skilled worker strategy with five areas of action: modernized training, targeted professional development, higher labor force participation, improved job quality, and modernized immigration.

The National Continuing Education Strategy plays a key role in the field of continuing education. It aims to create a new culture of professional development and enable employees to prepare for the demands of a changing world of work. Instruments such as the Qualification Opportunities Act, the planned part-time educational leave, and the qualification allowance are intended to lower the financial barriers to continuing education measures. The Federal Employment Agency's educational target plan for 2026 particularly emphasizes qualification-oriented continuing education and partial qualifications as instruments for securing skilled workers.

The need is evident in the figures: Among companies experiencing staffing difficulties, the most frequent candidates are those with dual vocational training, sought by 56 percent of the affected businesses. Employees with advanced vocational qualifications are lacking in 40 percent of cases, often in the high-tech sector. At the same time, companies are demanding, as the most important prerequisite for securing skilled workers, a reduction in bureaucracy for their employees (61 percent), followed by strengthening vocational training (44 percent) and fewer legal restrictions on working hours (41 percent).

A particular pressure to act arises from the looming loss of company-specific knowledge. When experienced professionals from the baby boomer generation retire, they take with them tacit knowledge that is not documented and is difficult to replace through new hires. The DIHK report shows that 23 percent of companies fear this loss of knowledge as a concrete consequence of the skills shortage. Systematic knowledge management and intergenerational tandem models, in which older employees specifically pass on their know-how to younger colleagues, will therefore become increasingly important.

Industry undergoing structural change: Transformation and skilled workers

Germany's industrial base is undergoing one of the most profound transformations since reunification. The combination of decarbonization, digitalization, and a restructuring of global supply chains is impacting an economy simultaneously grappling with skills shortages and economic weakness.

According to IAB forecasts, significant job losses are expected in the manufacturing sector, while hundreds of thousands of new jobs are being created in areas such as the public sector, education, and healthcare. This sectoral shift reflects structural change: Germany is moving from a strongly export-oriented industrial economy to a more service-based economy. Employment subject to social security contributions is growing only through part-time positions, while full-time employment is declining.

The automotive sector is a prime example of this contradictory dynamic. Its low skills shortage of just under 10 percent reflects a massive reduction in jobs associated with the transformation to electromobility. By summer 2025, the figure had fallen from 20.9 to 14.5 percent, a consequence of ongoing restructuring. The workers being laid off often possess highly specialized qualifications in combustion engine manufacturing, skills no longer required in the new world of electric and software architectures. This creates a mismatch problem: workers are available, but their skills do not meet the new qualification requirements.

Mechanical engineering, traditionally one of the strongest pillars of the German economy, is reporting an above-average shortage of skilled workers, at around 19 percent. In this sector, which is heavily dependent on exports and innovation, a lack of skilled workers can directly impact competitiveness. Engineers, mechatronics technicians, and specialists with digital skills who can bridge the gap between traditional mechanical engineering expertise and networked production are particularly in demand.

The economic costs: Growth slowdown, skills shortage

The effects of the skilled worker shortage extend far beyond individual companies. The DIHK Skilled Worker Report 2025/2026 shows that 83 percent of companies expect negative consequences in the coming years. Rising labor costs are the primary concern, predicted by 63 percent of businesses. The skilled worker shortage is driving up wages in shortage occupations, further increasing labor costs already burdened by high social security contributions. The increased workload for existing employees follows in second place, cited by 55 percent. Overtime, more intensive work schedules, and higher performance pressure are the result, which in turn increases sick leave and employee turnover, exacerbating the skilled worker shortage: a vicious cycle.

Equally serious is the anticipated restriction of the supply of goods and services, which 36 percent of companies expect. When a nursing home closes beds due to staff shortages, when a craft business turns down orders because it can't find skilled workers, or when a machine manufacturer can't meet delivery deadlines because of a lack of engineers, then the skilled worker shortage manifests itself as a real loss of prosperity.

The situation is particularly dire for small and medium-sized enterprises (SMEs). According to a report by the German Chamber of Industry and Commerce (DIHK), more than 40 percent of SMEs are now affected by the shortage of skilled workers. SMEs, often described as the backbone of the German economy, frequently lack the resources of large corporations to compete for scarce skilled workers with competitive salaries, employer branding campaigns, or international recruitment strategies. For smaller businesses, especially in rural areas, finding staff is becoming an existential challenge.

The STEM sector: Between relaxation and anxiety about the future

A surprising finding at first glance is the significant decline in the shortage of skilled workers in STEM professions (science, technology, engineering, and mathematics). In the fields of science, geography, and computer science, the number of unfilled positions fell by 59.2 percent in March 2025 compared to the same month of the previous year. The collapse in job openings for qualified IT professionals, coupled with rising unemployment, is a clear economic phenomenon.

However, experts warn against drawing hasty conclusions. The current STEM skills shortages are temporary, and the long-term prospects remain high. Digital transformation, the expansion of renewable energies, infrastructure modernization, and the growing importance of AI and cybersecurity will cause the demand for STEM qualifications to rise sharply again in the medium term. The IW report on artificial intelligence as a competitive factor predicts that the current skills gap could increase to more than 700,000 people by 2027, with STEM professions being particularly affected.

According to the DIHK report, future-oriented areas such as digitalization, e-mobility, the energy transition, and infrastructure expansion are particularly affected by the shortages. The transformative agenda that Germany is pursuing, from the electrification of transport and the development of a hydrogen economy to broadband expansion, is simply not feasible without a sufficient number of STEM professionals.

Political levers and entrepreneurial responses

Securing skilled workers requires a package of measures that operate at various levels. With its skilled worker strategy, the Federal Government is pursuing a five-pronged approach, ranging from modernized training and targeted professional development to increasing labor force participation, improved job quality, and modernized immigration.

There is still considerable potential for improvement in labor force participation. While Germany has significantly increased the female employment rate in recent decades, the high rate of part-time work among women limits their effective contribution to the total volume of work. The labor force participation of older workers can also be increased. According to the IAB projection, around 52 percent of men aged 65 to 69 will be part of the potential labor force by 2030, compared to almost 30 percent in 2020. Incentives for working longer, flexible transitions into retirement, and the abolition of early retirement mechanisms could reinforce this trend.

At the company level, innovative recruitment strategies are becoming indispensable. The DIHK survey shows that companies are demanding less bureaucracy for their employees as the most important prerequisite. This desire reflects a key insight: the shortage of skilled workers is exacerbated by unnecessary administrative burdens because scarce working time is tied up in non-productive tasks. Every reporting and documentation requirement that is eliminated effectively frees up working capacity.

Flexible working hours are also demanded by 41 percent of companies. In a world where skilled workers have become a scarce commodity, working time arrangements are becoming a competitive factor. Companies that offer flexible models, from remote work and four-day weeks to individual working time accounts, have a better chance of attracting and retaining talent.

On the way to a skilled worker economy: A new paradigm

The analysis of current data leads to a clear conclusion: Germany is not experiencing a period of easing in its skilled worker shortage, but rather a cyclical lull within a long-term structural problem. The figures from the ifo Institute for the beginning of 2026 are not a reason to sound the all-clear, but rather the result of an economy that has been weak for three years.

If the economy recovers as predicted in 2026 and 2027, the pressure on skilled workers will return with full force, but this time it will meet a shrinking potential labor force. The demographic shift of 2026, in which the potential labor force declines in absolute terms for the first time, marks the beginning of a new era. Germany will have to learn to manage with a structurally limited labor supply.

This development necessitates a paradigm shift in economic policy. The previous growth strategy, which relied on a steadily increasing labor supply, is reaching its limits. Instead, productivity strategies are needed: more output per capita through automation, digitalization, and improved skills. Demographic pressure can become an opportunity if it forces the long-overdue modernization of administration, infrastructure, and production processes.

The aging population coincides with profound technological change, and this combination will further shift the demand for specific skills. Those who invest in this equation—whether companies in the further training of their workforce, governments in educational infrastructure, or individuals in their own professional development—will determine the winners and losers of this transformation. The economic lull of 2026 should not be used for complacency, but rather as a window of opportunity for investments that will pay off in just a few years.

Your global marketing and business development partner

☑️ Our business language is English or German

☑️ NEW: Correspondence in your native language!

Konrad Wolfenstein

I and my team are happy to be available to you as your personal advisor.

You can contact me by filling out the contact form here or simply call me at +49 7348 4088 965. My email address is: [email protected]

I'm looking forward to our joint project.