The quiet decline of the Chinese auto industry – The paradox of growth – Image: Xpert.Digital

China's automotive industry: Behind the success headlines lurks a crisis

Structural problems are shaking China's automotive industry despite impressive sales figures

The Chinese automotive industry is currently undergoing an unprecedented transformation, casting its seemingly unstoppable success story of recent years in a completely new light. While sales figures still appear impressive on the surface, they mask an industry plagued by fundamental structural problems and whose future is highly uncertain.

The paradox of growth

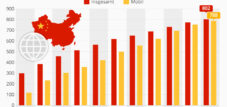

China has become the world's largest automotive market in recent years, simultaneously overtaking Japan as the world's largest car exporter. The figures speak for themselves: in 2024, over 31 million vehicles were produced and sold in China, with electric vehicles accounting for more than 40 percent. The dominance of Chinese brands is particularly impressive, as they have increased their market share in the domestic market to over 65 percent.

But behind these impressive figures lies a different reality. The rapid expansion of the Chinese automotive industry was driven by government subsidies, regional ambitions, and the political will to play a leading role in electromobility. Every province wanted its own electric vehicle brand, and large technology companies like Xiaomi and Huawei pushed into the market. The result was an explosive increase in the number of manufacturers: there are currently around 100-150 active Chinese car brands, with a total of approximately 300 brands registered.

Related to this:

The crisis of overcapacities

The core of the current problems lies in the massive overcapacity of the Chinese automotive industry. The country's production capacity is around 50 million vehicles annually, while domestic demand is only about 30 million. This overcapacity of 20 million vehicles is equivalent to more than the entire annual car production of Europe.

Factory capacity utilization is at only 49.5 percent, and there are 3.5 million unsold cars in storage. This situation is forcing manufacturers to drastically reduce their prices in order to keep the production lines running – a vicious cycle that is putting the entire industry under enormous pressure.

The brutal price war

The price war in the Chinese automotive industry reached a new level in May 2025 when BYD, the market leader in electric vehicles, slashed prices on 22 models by up to 34 percent. The small Seagull hatchback is now available for the equivalent of just €6,700, while the Seal dual-motor hybrid is offered with a 34 percent discount.

This price offensive triggered a chain reaction, forcing other manufacturers like Geely, Chery, and Changan to follow suit. The consequences were dramatic: BYD lost over $20 billion in market capitalization in just two weeks, and the average return in the industry plummeted from 4.3 percent in 2024 to 3.9 percent in the first quarter of 2025.

What's unique about this price war is that it's hitting the lower price segments, where profit margins are already minimal or nonexistent. There's growing concern that even established brands could collapse under this pressure, as many companies have financed their rise through debt.

The problem of hidden debt

Another serious problem is the lack of transparency in the financing practices of many Chinese automakers. BYD's case illustrates the complexity of their true debt situation. According to an analysis by GMT Research, BYD's real debt is around €44 billion, while only €3.3 billion is officially reported. This discrepancy arises from delayed payments to suppliers and other creative financing methods.

In 2023, BYD took an average of 275 days to pay its suppliers. Chinese automakers pay their suppliers on average after 182 days, while Western manufacturers typically pay after one to one and a half months. This practice effectively turns suppliers into banks and obscures the true debt of automakers.

Related to this:

Manipulated sales figures

A particularly problematic aspect of the crisis is the systematic manipulation of sales figures through so-called "zero-kilometer used cars." Manufacturers sell new cars to financing companies or dealers to meet their sales targets. These cars then end up on the market as "used cars" with zero kilometers and discounts of up to 40 percent.

The Chinese Ministry of Commerce has summoned managers from BYD, Dongfeng, and other manufacturers over alleged manipulation of sales figures through used car channels. Videos of dusty new cars sitting in vast parking lots—officially registered but never driven—are circulating on platforms like Weibo.

Related to this:

The wave of bankruptcies begins

The first victims of the crisis are already visible. Luxury electric car manufacturer HiPhi had to file for bankruptcy after the company was unable to pay its bills since April 2024. Other companies, such as Hozon, which had big plans for 2024 with its Neta brand, suffered a similar fate, falling far short of expectations.

Even established startups like Nio, Xpeng, and Li Auto are under enormous pressure. Despite record deliveries in the next quarter, Nio reported a growing net loss of $700 million. A Chinese automotive analyst predicts that the probability of Nio, Xpeng, and Li Auto surviving independently for the next three years is zero.

The challenge of economies of scale

A fundamental problem for many Chinese automakers is their small size. Experts agree that electric vehicle manufacturers selling fewer than two million vehicles per year will not survive, as economies of scale are too small and research and development costs too high. Of the original 300 new electric vehicle companies, only 100 survived, and today fewer than 50 companies exist, of which only 40 actually sell cars each year.

Impact on the supplier industry

The crisis is also affecting the automotive supply industry, which is suffering from delayed payments by car manufacturers. The Chinese government has responded by requiring 17 major automakers, including BYD, Geely, and Chery, to limit their payment terms to 60 days. This measure demonstrates the seriousness of the situation and shows that even the government recognizes the need for action.

Failed consolidation attempts

The Chinese government has recognized the urgent need for industry consolidation. However, an attempt to merge the two state-owned automakers, Changan and Dongfeng, failed spectacularly. The planned merger would have created China's largest car company, but it was called off due to resistance within the companies and complex legal issues with international joint venture partners.

The role of the international market

Given domestic overcapacity, Chinese automakers are increasingly reliant on exports. In 2024, China exported 5.86 million vehicles, an increase of 19.3 percent. However, they are also encountering resistance here: The EU has imposed tariffs of up to 45 percent on Chinese electric cars, and the US has practically closed the market completely.

The Chinese government responded to these trade restrictions by urging its automakers to slow their expansion in Europe and refrain from seeking new production sites. This measure demonstrates how limited the options have become for Chinese automakers.

German manufacturers as losers

Ironically, German car manufacturers are also affected by the crisis in China, even though they are not directly part of the Chinese industry. Their market share for electric vehicles in China fell to just five percent in 2024. Volkswagen, BMW, and Mercedes experienced significant declines, with Porsche being particularly hard hit, seeing a drop in registrations of over 50 percent.

Future forecasts

The outlook for the Chinese automotive industry is bleak. Experts predict that of the more than 100 currently active Chinese car brands, only about seven major automakers will survive. BYD will likely emerge as an integrated, state-backed champion, but for many other manufacturers, it remains to be seen whether they have more to offer than registered but unused vehicles.

The situation reminds many observers of the collapse of the real estate company Evergrande, which left behind derelict buildings and millions of unoccupied housing units. The parallels are obvious: exaggerated growth ambitions, government subsidies, inflated balance sheets, and ultimately a systemic crisis.

Lessons Learned for the Global Automotive Industry

The crisis in the Chinese automotive industry offers important lessons for the global automotive sector. It shows that even seemingly unstoppable growth markets have their limits and that government subsidies and political ambitions alone are not enough to create sustainable business models.

The transformation to electromobility requires not only technological innovation, but also sound financing, realistic business models, and the ability to thrive in an increasingly competitive market. The Chinese experience shows that while electromobility is the future of the automotive industry, the path to it is fraught with considerable risks.

The coming years will show which Chinese automakers will survive the crisis and which will succumb to the pressure. For the surviving companies, consolidation could have positive effects, leading to a healthier market structure and more sustainable business models. For many others, however, the only hope remains a takeover by stronger competitors or government bailouts.

Related to this:

Your global marketing and business development partner

☑️ Our business language is English or German

☑️ NEW: Correspondence in your native language!

Konrad Wolfenstein

I and my team are happy to be available to you as your personal advisor.

You can contact me by filling out the contact form here wolfenstein@xpert.digital:or simply call me at +49 7348 4088 965. My email address is

I'm looking forward to our joint project.