Rare Earths: China's Raw Material Dominance – Can Recycling, Research and New Mines Break Free from Raw Material Dependence? – Image: Xpert.Digital

Rare Earths: Germany's Path to Strategic Raw Material Autonomy – Challenges, Research and Political Options (Reading time: 49 min / No advertising / No paywall)

The strategic importance of rare earth elements for Germany

Rare earth elements (REEs) are a group of chemical elements that play a key role in numerous modern technologies due to their unique physical and chemical properties. Their strategic importance for industrialized nations like Germany has grown exponentially in recent decades, particularly in the context of digitalization, the energy transition, and security-relevant applications. However, the increasing concentration of global supply chains, especially China's dominance, has revealed significant economic and geopolitical risks. This article analyzes the complex issue of rare earth elements from a German perspective, highlights dependence on China, assesses current research and development approaches for new solutions, and outlines strategic options for Germany to achieve greater long-term independence in the supply of these critical raw materials.

Definition, properties and classification of rare earth elements (REEs)

The rare earth elements comprise 17 metals from the periodic table: the 15 lanthanides (lanthanum (La), cerium (Ce), praseodymium (Pr), neodymium (Nd), promethium (Pm), samarium (Sm), europium (Eu), gadolinium (Gd), terbium (Tb), dysprosium (Dy), holmium (Ho), erbium (Er), thulium (Tm), ytterbium (Yb), lutetium (Lu)), as well as scandium (Sc) and yttrium (Y). These metals are extracted from ores. Their unique physical and chemical properties, such as high reactivity (especially with oxygen), flammability, and specific magnetic and spectroscopic characteristics, make them highly sought-after raw materials.

A distinction is usually made between light rare earth elements (LSEE), which include, for example, lanthanum, cerium, praseodymium, and neodymium, and heavy rare earth elements (HSEE), such as terbium and dysprosium. This distinction is relevant because LSEE are significantly more abundant than HSEE in most deposits.

The term "rare earth elements" is somewhat misleading, as these elements are not necessarily rare from a geological perspective. Neodymium, for example, is more common than lead, and thulium is more abundant than gold or platinum. The real challenge, and thus the "rarity" in an economic sense, lies rather in the low concentrations at which they occur in many deposits, and above all in the extremely complex and costly process of their separation and processing. Rare earth elements always occur in nature in combination with each other and with other minerals; their isolation requires a multitude of chemical steps and specific expertise. This technological and economic hurdle, not geological availability per se, is the core of the supply problem.

Below is a table summarizing the rare earth elements:

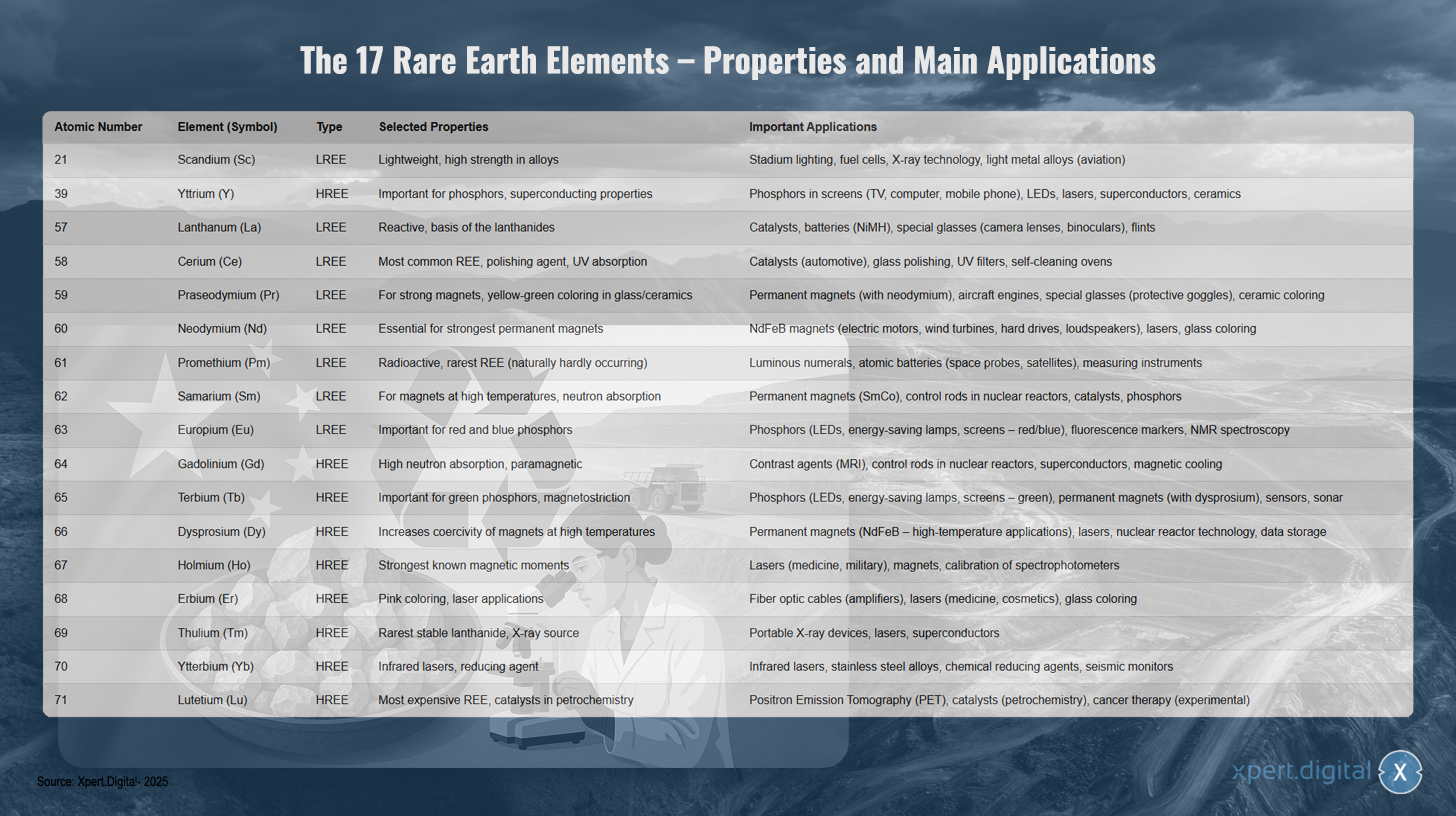

The 17 rare earth elements – properties and main applications

The 17 rare earth elements – properties and main applications – Image: Xpert.Digital

The 17 rare earth elements comprise both light and heavy rare earth metals, each with unique properties and diverse applications. Scandium (atomic number 21) is a light element with high strength in alloys and is used in stadium lighting, fuel cells, X-ray technology, and lightweight alloys for the aerospace industry. Yttrium (39) is one of the heavy rare earth elements and is important for phosphors and superconducting properties, which is why it is used in phosphors for displays, LEDs, lasers, superconductors, and ceramics.

Lanthanum (57) is highly reactive and forms the basis of the lanthanides. It is used in catalysts, batteries, specialty glasses, and flints. Cerium (58) is the most abundant rare-earth metal and serves as a polishing agent with UV absorption in catalysts, glass polish, UV filters, and self-cleaning furnaces. Praseodymium (59) enables strong magnets and produces a yellow-green color in glass and ceramics, making it suitable for use in permanent magnets, aircraft engines, and specialty glasses.

Neodymium (60) is essential for the strongest permanent magnets and is used in NdFeB magnets for electric motors, wind turbines, hard drives, and loudspeakers. Promethium (61) is radioactive and the rarest naturally occurring rare-earth metal, used in luminous displays, nuclear batteries, and measuring instruments. Samarium (62) is suitable for magnets at high temperatures and for neutron absorption in permanent magnets, control rods of nuclear reactors, and catalysts.

Europium (63) is important for red and blue phosphors in LEDs, energy-saving lamps, and displays. Gadolinium (64) exhibits high neutron absorption and paramagnetic properties, which is why it is used as a contrast agent in MRI, in control rods, and in superconductors. Terbium (65) is important for green phosphors and magnetostriction in LEDs, permanent magnets, and sensors.

Dysprosium (66) increases the coercive field strength of magnets at high temperatures and is used in high-temperature permanent magnets and lasers. Holmium (67) possesses the strongest known magnetic moments and is used in medical and military lasers. Erbium (68) produces a pink color and is used in fiber optic cables, medical lasers, and for coloring glass.

Thulium (69) is the rarest stable lanthanide and serves as an X-ray source in portable X-ray machines and lasers. Ytterbium (70) is used for infrared lasers and as a reducing agent in stainless steel alloys. Lutetium (71) is the most expensive rare-earth metal and is used in positron emission tomography, petrochemical catalysts, and experimentally in cancer therapy.

Key applications and growing relevance for future technologies

Rare earth elements have become indispensable in a wide range of high-tech applications due to their exceptional properties and play a central role in the technological development and competitiveness of modern economies. Their importance is constantly increasing with the progress of digitalization and the global energy transition.

Key areas of application include:

- Permanent magnets: Neodymium-iron-boron (NdFeB) magnets are the strongest known permanent magnets and are essential for high-performance and compact electric motors in electric vehicles, hybrid cars, e-bikes, robots, and industrial equipment. They are equally indispensable in wind turbine generators (especially gearless offshore turbines), hard disk drives, loudspeakers, and headphones. Dysprosium and terbium are often added to maintain the performance of these magnets at high temperatures.

- Catalysts: Cerium is used in automotive catalysts to reduce harmful exhaust emissions. Lanthanum and other rare earth elements are used in catalysts for petroleum refining (fluid catalytic cracking) and other chemical processes.

- Batteries: Lanthanum is an important component of nickel-metal hydride (NiMH) batteries, which are used in hybrid vehicles and portable electronics.

- Phosphors: Europium (for red and blue) and terbium (for green) are crucial for the color quality and efficiency of light-emitting diodes (LEDs), energy-saving lamps, flat panel displays (LCD, OLED), and other display technologies. Yttrium is also used in phosphors.

- Optics and lasers: Lanthanum improves the optical properties of specialty glasses for camera lenses, telescopes, and binoculars. Erbium is used in fiber optic cables for signal amplification. Neodymium, ytterbium, holmium, and erbium are important components in various types of lasers used in medicine, industry, and communications.

- Other high-tech applications include polishing agents (cerium oxide for precision optics and semiconductors), special ceramics (yttrium to improve high-temperature resistance), medical imaging (gadolinium as a contrast agent in MRIs), sensors, superconductors, and applications in the defense and aerospace industry (precision optics, navigation systems, drone and rocket control).

Rare earth elements (REEs) are of vital importance to key German industries such as the automotive sector (especially during the transition to electromobility), mechanical and plant engineering, renewable energies (primarily wind power), and the electronics and medical technology sectors. Progressive digitalization and the ambitious goals of the energy transition are leading to a projected significant increase in global demand for REEs in the coming years and decades. For example, the demand for REEs for permanent magnets could increase tenfold by 2050. The criticality of many rare earth elements stems not only from potential supply bottlenecks or the geographical concentration of production, but also from the lack of direct and equivalent substitutes for many of their high-performance applications. Although research into replacement materials is being conducted intensively, REEs are technologically difficult to replace in many areas due to their unique electronic and magnetic properties, or can only be replaced at the cost of reduced performance. This technological “lock-in” situation exacerbates the dependency problem and underlines the urgency of both increasing security of supply and developing alternative technological solutions.

Germany's critical dependence on China for rare earths: New strategies for technological sovereignty

Given the strategic importance of rare earth elements and the complex challenges associated with ensuring their security of supply, a thorough analysis of the current situation and future options for Germany is essential. This article aims to comprehensively examine the rare earth issue, analyze Germany's specific dependence on China, present the current state of research regarding new solutions, and, based on this, outline strategic opportunities for Germany to guarantee a long-term and sustainable supply of these critical raw materials and strengthen its own technological sovereignty.

Global supply landscape and Germany's dependence

The global supply of rare earth elements is characterized by an exceptionally high concentration in both deposits and extraction, as well as, and even more so, in processing. This concentration, particularly China's dominance, poses a significant strategic challenge and a potential risk for industrialized nations like Germany.

Global deposits, extraction and processing – China's dominant role

Although rare earth elements, as mentioned earlier, are not geologically extremely rare, economically viable concentrations are found in relatively few locations worldwide. The largest known reserves are in China, which is estimated to possess around 44 million tons of rare earth oxides (SEOs). Other significant reserves are located in Vietnam (approx. 22 million tons), Brazil and Russia (approx. 21 million tons each), India (approx. 6.9 million tons), Australia (approx. 4 million tons), and the USA (approx. 1.8 million tons). Greenland also has significant deposits.

China has played a leading role in global mine production for decades. In 2021, China's share of global mining output was approximately 61-64%, and it is estimated to reach around 70% in 2023. The USA, Myanmar, and Australia are other important producers, but with significantly smaller market shares. Historically, the USA was the largest producer until the late 1980s, before China massively expanded its production from the turn of the millennium and began to dominate the market.

China's dominance is even more pronounced in the refining and processing of rare earth elements. Here, China controls approximately 90% of global capacity. This means that even rare earth concentrates mined in other countries (e.g., the USA or Australia) often have to be transported to China for separation and refining. This step – the separation of the chemically very similar rare earth elements from each other and from accompanying elements – is technologically demanding and capital-intensive.

China's dominance is not solely attributable to its rich geological resources, but is the result of a long-term industrial strategy. In the past, this often involved accepting lower environmental standards and using state subsidies to achieve and maintain a dominant market position. This frequently led to production in Western countries becoming unprofitable, resulting in the closure of mines and processing plants. In recent years, China has consolidated its rare earth industry, employing export quotas and tariffs (historically and potentially in the future) as control mechanisms and increasingly focusing on the production of higher-value products and value creation within its own borders. A significant step was the ban imposed at the end of 2023 on the export of rare earth processing technologies for magnets, further cementing its technological dependence.

Another important distinction concerns light (LSEE) and heavy (HSEE) rare earth elements. While LSEE such as lanthanum and cerium are relatively abundant and mined outside of China, the supply of certain critical HSEE elements, essential for high-performance applications such as permanent magnets (e.g., dysprosium, terbium), is almost entirely dependent on China and neighboring Myanmar. This specific dependency for HSEE elements, which are often found in ion adsorption stones whose mining is particularly environmentally problematic, represents a critical point in the global supply chain.

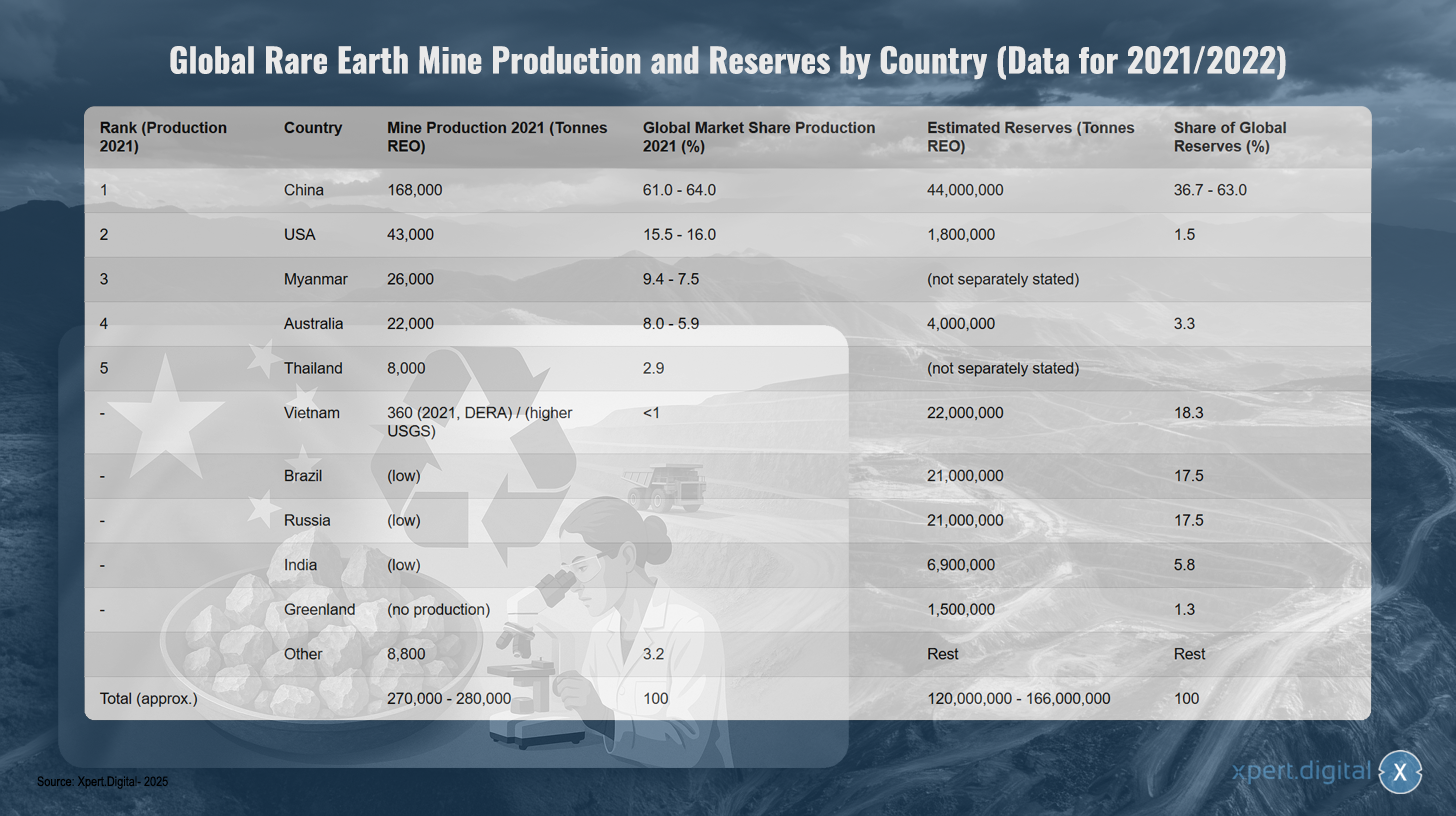

Global rare earth mine production and reserves by country (based on data for 2021/2022)

Global rare earth mine production and reserves by country (based on 2021/2022 data) – Image: Xpert.Digital

Note: Figures may vary slightly depending on the source and year of data collection. SEO = Rare earth oxides. Reserve figures for China vary considerably across sources.

Global rare earth mineral (SEM) mine production is dominated by China, which accounted for approximately 61-64% of global production in 2021, with 168,000 tons. The United States ranked second with 43,000 tons (15.5-16% market share), followed by Myanmar with 26,000 tons (9.4-7.5%) and Australia with 22,000 tons (8.0-5.9%). Thailand produced 8,000 tons (2.9% market share). Vietnam had low production of approximately 360 tons in 2021, according to DERA, although the USGS reports higher figures. Other countries, such as Brazil, Russia, and India, currently have low production. Total global production amounted to approximately 270,000-280,000 tons.

The picture is different when looking at reserves: China has an estimated 44 million tons of SEO (36.7-63% of global reserves), Vietnam 22 million tons (18.3%), Brazil and Russia 21 million tons each (17.5% each). India has 6.9 million tons (5.8%), Australia 4 million tons (3.3%), and the USA 1.8 million tons (1.5%). Greenland has 1.5 million tons of reserves (1.3%), but is not currently producing. Total global reserves are estimated at 120-166 million tons of SEO.

Analysis of Germany's and the EU's import dependence on China

China's dominance in the global rare earth element (REE) supply chain leads to a significant import dependency for Germany and the entire European Union. Recent data from the Federal Statistical Office shows that in 2024, Germany imported approximately 3,400 tons of rare earth elements directly from China, representing 65.5% of its total REE imports. For the EU as a whole, the share of direct imports from China in 2024 was 46.3% (6,000 tons), followed by Russia with 28.4% and Malaysia with 19.9%.

The dependence is particularly critical for specific rare earth elements needed for high-performance magnets, such as neodymium, praseodymium, and samarium. These were almost entirely imported from China in 2024. The situation is similar for processed products. For example, 84% of the rare earth metals imported into Germany and approximately 85-94% of the NdFeB magnets produced worldwide and imported into Germany originate from China.

This dependency has significant macroeconomic implications. It is estimated that in 2022, around 22% of the gross value added of the manufacturing sector in Germany (equivalent to €161 billion) depended on the availability of rare earth elements. Particularly affected sectors include other vehicle manufacturing (67% of value added dependent on rare earth elements), motor vehicle manufacturing (65%), and the manufacture of electronic and optical products (55%).

It is important to note that statistically recording the origin of rare earth elements can potentially underestimate the true dependence on China. If only the final country of shipment is recorded, processing sites in third countries can obscure the original Chinese provenance of the raw rare earth elements. For example, Austria and Estonia act as processors for German imports, and Malaysia is a major supplier to the EU. However, since China dominates global refining, it is highly likely that a large proportion of the raw materials processed in these countries originally come from China. Official import statistics may therefore not reflect the full extent of the interconnectedness with Chinese sources.

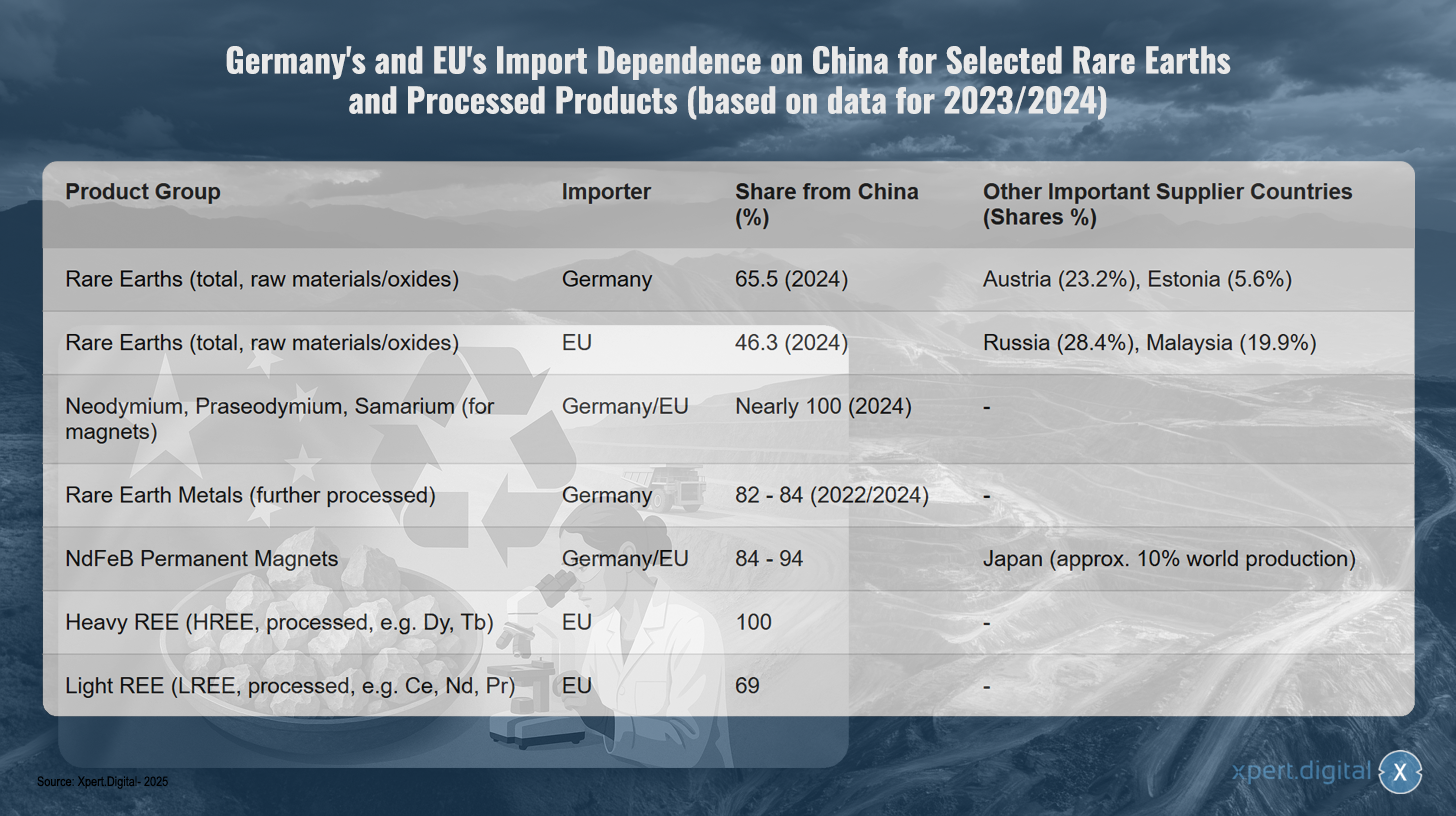

Import dependence of Germany and the EU on China for selected rare earths and processed products (based on data for 2023/2024)

Germany's and the EU's import dependence on China for selected rare earths and processed products (based on data for 2023/2024) – Image: Xpert.Digital

Note: The figures are based on the most recent available data, mostly for 2023/2024. Exact percentages may vary slightly depending on the data source and survey methodology.

Germany and the European Union are significantly dependent on China for rare earth elements and processed products, as recent data from 2023 and 2024 demonstrate. Germany sources 65.5 percent of its raw materials and oxides of rare earth elements from China, while the EU is slightly less dependent at 46.3 percent. Germany's other major suppliers are Austria (23.2 percent) and Estonia (5.6 percent). The EU diversifies more, also sourcing 28.4 percent from Russia and 19.9 percent from Malaysia.

The dependency is particularly critical for specialized products. Neodymium, praseodymium, and samarium, which are essential for magnet production, come almost entirely from China. For further processed rare-earth metals, Germany's import share from China ranges between 82 and 84 percent. The situation is similarly dramatic for NdFeB permanent magnets, with both Germany and the EU sourcing 84 to 94 percent of their imports from China. Japan plays a significant role as the only alternative, accounting for approximately ten percent of global production.

The dependence reaches its peak with heavy rare earth elements, as the EU imports 100 percent of its processed heavy rare earth elements, such as dysprosium and terbium, from China. For light rare earth elements like cerium, neodymium, and praseodymium, 69 percent of EU imports also come from China.

Economic and geopolitical risks of dependency

The high concentration of the SEE supply chain on China poses significant economic and geopolitical risks for Germany and the EU. In the past, China has repeatedly used its dominant market position to influence prices and employ supplies as a political tool.

A well-known example is the throttling of SEE exports to Japan in 2010 during a territorial dispute. More recent developments, such as China's imposition of export controls on certain SEE metals and magnets in April 2025, have again highlighted the vulnerability of Western industries. These measures led to significant price increases on the global market outside of China—dysprosium oxide, for example, cost up to US$300 per kilogram—and threatened to cause production stoppages in the German automotive industry within four to six weeks, as stockpiles rapidly dwindled.

Such supply disruptions or drastic price increases jeopardize the competitiveness of key German industries, particularly in the fields of electromobility, renewable energies, and high technology, and can severely hinder the achievement of ambitious energy and transport transition goals as well as digitalization. This dependency is multidimensional: it affects not only raw material extraction but, even more critically, refining and the production of intermediate products such as permanent magnets. Even if raw SEE were available from other sources, the necessary processing capacities outside of China to convert them into the required high-purity metals or alloys are often lacking. This means that diversifying mine production alone will not resolve the core dependency in the middle part of the value chain. Therefore, developing domestic European refining and processing capacities is just as critical a bottleneck as raw material extraction itself.

Ecological and social implications of global SEE extraction and processing

The extraction and processing of rare earth elements is associated with significant environmental and social problems, often concentrated in the mining and production countries. Mining frequently leads to massive environmental destruction, including soil erosion, contamination of water resources through the use of chemicals (e.g., acids, alkalis) and heavy metals, air pollution from dust and toxic gases, and the destruction of natural life forms and loss of biodiversity. Water and energy consumption are also very high in these processes.

A particular problem is the frequent occurrence of radioactive trace elements such as thorium and uranium in rare earth elements (REEs). The processing of REEs generates considerable quantities of residues – it is estimated that the production of one ton of REEs produces around 2,000 tons of waste rock and processing residues, including up to 1.4 tons of radioactive waste. Improper storage of these residues, as in the case of the enormous tailings lake at the Bayan Obo mine in China, leads to long-term contamination of soil and groundwater.

The social impacts in the mining regions are also severe. These include significant health risks for workers and the local population, for example, from dust exposure (pneumoconiosis in Baotou) or contact with toxic substances. Displacement of communities, land conflicts, and human rights violations are common. Corruption and inadequate safety measures are particularly prevalent in countries with low environmental and social standards.

In the past, China has accepted lower environmental standards and often tolerated the associated problems in order to achieve market dominance. More recently, there are indications that China is attempting to outsource the most environmentally damaging parts of production to neighboring countries such as Myanmar. While this shifting of environmental and social costs has reduced production costs for Western industries in the short term, it has led to ethical dilemmas and an externalization of the true costs of SEE production in the long term. A sustainable supply strategy for Germany and Europe must consider and internalize these aspects, rather than simply shifting the problems geographically. The development and implementation of domestic European extraction and processing capacities must therefore be carried out in compliance with the highest environmental and social standards, which in turn affects the economic viability of such projects.

🎯🎯🎯 Benefit from Xpert.Digital's extensive, five-fold expertise in one comprehensive service package | BD, R&D, XR, PR & Digital Visibility Optimization

Benefit from Xpert.Digital's extensive, five-fold expertise in a comprehensive service package | R&D, XR, PR & Digital Visibility Optimization - Image: Xpert.Digital

Xpert.Digital possesses in-depth knowledge across various industries. This allows us to develop tailored strategies precisely aligned with the requirements and challenges of your specific market segment. By continuously analyzing market trends and monitoring industry developments, we can act proactively and offer innovative solutions. The combination of experience and expertise generates added value and provides our clients with a decisive competitive advantage.

More information here:

Europe's way out of the rare earth trap: How recycling and substitution break raw material dependency

Research and development approaches to reduce dependency

Given the critical dependence on rare earth elements and the associated risks, intensive research and development (R&D) efforts are essential to find alternative solutions and strengthen the long-term security of supply for Germany and Europe. R&D activities focus primarily on three areas: substitution and efficiency improvements, recycling and the circular economy, and the development and sustainable extraction of new primary and secondary raw material sources.

Substitution and efficiency

The substitution of rare earth elements (REEs) with other materials or the use of technologies that do not require REEs at all is a key research approach. In parallel, efforts are aimed at using REEs more efficiently in order to reduce the specific requirement per application unit.

Replacement materials for magnets

Permanent magnets, especially NdFeB magnets, are one of the main applications for SEE and a critical bottleneck. Research here focuses on several alternative material classes:

- Iron nitride (FeN) magnets: These are considered a promising SEE-free alternative. The US company Niron Magnetics is driving the commercialization of FeN magnets and is building a production facility in Minnesota, USA, supported by government funding. ARPA-E in the USA is also funding research projects on FeN magnets.

- Manganese-based magnets: Alloys such as manganese-bismuth (MnBi) and manganese-aluminum (MnAl) are being intensively researched. The Ames Laboratory in the USA has developed MnBi magnets that exhibit particularly good properties at high temperatures and are already being tested in motors in cooperation with industrial partners. Research activities on MnBi are also taking place in Europe, for example at Austrian and German institutes, focusing on optimized synthesis processes such as high-pressure torsion (HPT) and thermomagnetic annealing.

- High-entropy alloys (HEA): This class of materials is also being investigated for its potential for magnetic applications, but is often still in an earlier stage of research.

- "Gap magnets": The goal is to develop magnets that bridge the performance and cost gap between inexpensive ferrite magnets and high-performance SEE magnets. MnBi is considered a potential candidate in this regard.

The development of SEE-free magnets is a global race. While the USA is already taking concrete steps towards pilot production and commercialization, particularly with FeN and MnBi magnets, Europe must intensify its efforts to avoid falling behind technologically and to prevent a new dependency, this time on the USA, for SEE-free magnet technologies.

Alternative materials for catalysts

Cerium, a light rare earth element (REE), plays an important role in three-way catalytic converters (TWCs) for automotive exhaust gas purification. Research in this area focuses less on the complete replacement of cerium, as it is one of the more common and inexpensive REEs, and more on reducing the use of the more expensive and critical platinum group metals (PGMs) such as platinum, palladium, and rhodium.

- Approaches include the development of copper-based catalysts that can significantly reduce the PGM content.

- Research to optimize cerium oxide nanoparticles aims to increase their efficiency in catalysts and thus potentially reduce material usage.

- TU Darmstadt is researching the oxygen dependence of cerium-based phosphors, which may also be relevant for understanding cerium chemistry in catalysts.

In the field of automotive catalysts, the primary driver for substitution research is less the availability of cerium than the cost and criticality of proton pumps (PGMs). The substitution of cerium itself tends to be less of a focus than, for example, the replacement of heavy SEEs in magnets.

Replacement materials for phosphors

Europium, terbium, and yttrium are crucial for the color quality and efficiency of LEDs and displays. Research is searching for SEE-free alternatives

- Quantum dots (QDs): Semiconductor nanocrystals (e.g., based on cadmium, indium, perovskite, or copper indium sulfide) can emit light with high efficiency in specific colors and are being investigated as a promising alternative to SEE phosphors in displays and lighting. However, challenges include the toxicity of some QD materials (especially cadmium-containing ones), their long-term stability under operating conditions, and the cost of mass production.

- Organic light-emitting diodes (OLEDs): These are already an established SEE-free technology for displays, but continuous materials research is taking place to improve efficiency, lifespan and cost.

- New phosphorus materials: Research is being conducted on new inorganic phosphorus materials that either do without critical energy elements (CEEs) entirely or reduce the proportion of critical CEEs. Often, however, this involves optimizing existing systems (e.g., by doping with less critical elements or improving quantum efficiency) rather than a complete replacement.

Although progress has been made with alternative phosphor materials such as QDs, the complete elimination of SEE-based phosphors, especially in applications requiring the highest color quality and efficiency, remains a significant challenge. The trend often leans towards increasing efficiency and reducing the SEE content rather than complete replacement with entirely new materials.

Reducing SEE requirements through material efficiency and design changes

Besides substitution, reducing the specific SEE requirement per application is an important lever.

- As part of the flagship project “Criticality of Rare Earths”, Fraunhofer Institutes have developed technologies to significantly reduce the need for neodymium and dysprosium in permanent magnets through optimized manufacturing processes (e.g., near-net-shape manufacturing to avoid material losses), alternative magnetic materials and recycling-friendly design of electric motors – potentially to one fifth of today's value.

- Constructive optimizations of electric drives, such as improved cooling, can lower the operating temperature and thus reduce the need for high-temperature stabilizing elements such as dysprosium.

- In general, the development of products that require fewer critical raw materials from the outset is an important aspect of resource efficiency.

Material efficiency and design innovations often represent more pragmatic and economically viable solutions in the short to medium term than complete substitution with entirely new materials, the development of which is lengthy, costly, and risky. However, these incremental improvements can, in aggregate, make a significant contribution to reducing criticality.

Recycling and circular economy

Recycling rare earth elements from old products and production waste is another crucial pillar for reducing import dependency and conserving primary resources.

Current recycling technologies and their economic viability

For the recycling of SEE, especially from permanent magnets (e.g. NdFeB) and batteries, various technological approaches exist:

- Hydrometallurgical processes: In this process, metals are selectively extracted from a solution, often after prior digestion of the materials with acids. This is an established method in ore processing and is, in principle, applicable to many magnetic compositions.

- Pyrometallurgical processes: In these processes, materials are melted at high temperatures, allowing the SEE to accumulate in the slag. These processes do not produce wastewater and potentially have fewer process steps than hydrometallurgical routes.

- Gas phase extraction and electrochemical processes: These are further approaches to the separation and recovery of SEE.

- Hydrogen embrittlement (Hydrogen Processing of Magnet Scrap, HPMS): In this process, NdFeB magnets are exposed to hydrogen, which leads to their embrittlement and disintegration into a powder. This powder can then be used directly to manufacture new magnets (material recycling) or for further chemical processing.

However, the economic viability of SEE recycling often remains a major hurdle. It depends heavily on current prices for primary SEE, the concentration of valuable elements (especially heavy SEE such as dysprosium) in the waste stream, and the costs of collection, dismantling, and processing. For many end-of-life products, such as smartphones, the amount of SEE used is so small that recycling is often not profitable. Consequently, SEE recycling rates in Europe are currently in the low single-digit percentage range or even lower.

The main problems are:

- Low and inefficient collection rates: Many products containing SEE do not enter official recycling streams.

- Complex disassembly: SEE components are often permanently integrated into products and difficult to access. Manual disassembly is time-consuming and costly.

- Heterogeneous material flows: The composition of electronic waste and other waste fractions varies greatly, which makes the development of standardized recycling processes difficult.

- High purity requirements: For reuse in high-performance applications, the recycled SEE often needs to have very high purity levels, which increases the cost of processing.

The economic viability of SEE recycling faces a chicken-and-egg problem: low collected volumes and technologically complex, not yet fully mature processes make recycling expensive, which in turn inhibits investment in larger plants and further research. Without economies of scale, technological breakthroughs in the automation of dismantling and separation, and supporting regulatory frameworks (e.g., binding recycling quotas, requirements for recyclable product design – “Design for Recycling”), establishing a comprehensive and economically viable SEE recycling industry remains a major challenge.

Progress and challenges in building a European recycling infrastructure

Despite the challenges, there is visible progress in building a European recycling infrastructure for SEE (stratified renewable energy). Within the framework of the Critical Raw Materials Act (CRMA), the EU has set the ambitious goal of meeting at least 25% of its annual demand for strategic raw materials through recycling by 2030.

Several pilot plants and initial commercial initiatives have been established or are in the planning stages in Europe:

- Heraeus Remmoy (Bitterfeld, Germany): In May 2024, it commissioned Europe's largest recycling plant for rare-earth magnets. The plant has an initial processing capacity of 600 tons of scrap magnets per year, which can be increased to up to 1,200 tons in the medium term. The technology used is expected to reduce CO2 emissions by 80% compared to primary extraction.

- Carester/Caremag (Lacq, France): Plans to build a large-scale plant for the refining and recycling of rare earth elements (REEs), scheduled to begin operation at the end of 2026. The plant is planned to process 2,000 tons of scrap magnets and 5,000 tons of primary REE concentrates per year, with a focus on the recovery of light and heavy REEs such as neodymium, praseodymium, dysprosium, and terbium. The project has been classified as a strategic project by the European Commission.

- Mkango Resources / HyProMag: Develops recycling plants in the UK (via HyProMag Ltd) and is planning a plant in Pulawy, Poland (via Mkango Polska), which has also been recognized as a strategic EU project. These projects often utilize the HPMS process.

- LIFE INSPIREE (Italy): An EU-funded project aiming to recover up to 700 tonnes of SEE (neodymium, palladium, dysprosium) annually from electronic waste magnets on an industrial scale. The long-term goal (by 2040) is a capacity of over 20,000 tonnes per year.

These initiatives demonstrate that efforts are being made at both the research and industrial levels to establish a circular economy for rare earth and solar waste (REE) in Europe. However, building a comprehensive, diversified, and economically viable European REE recycling infrastructure is a lengthy process. It requires substantial and continuous investment in technology development, collection and logistics systems, and overcoming scaling challenges from pilot plants (often TRL 6-7) to full-scale industrial applications. Against this backdrop, the recycling targets set by the EU must be considered highly ambitious.

German and European research projects and their results/potential (as of 2024/2025)

The research landscape in Germany and Europe is very active in the field of SEE recycling and substitution, supported by research institutions and by national and European funding programs.

- Fraunhofer Society: Various institutes make important contributions.

- The Fraunhofer Institute for Recycling and Resource Strategy (IWKS) is a leader in the development of recycling technologies for NdFeB magnets. Projects such as FUNMAG (recycling magnets for e-mobility) and RecyPer (production of defined magnet types from mixed waste magnet streams) utilize and optimize processes like hydrogen embrittlement (HPMS). Recycling magnets from wind turbines is also a key research focus.

- The Fraunhofer Institute for Interfacial Engineering and Biotechnology (IGB) is researching biotechnological processes for the recovery of SEE.

- The completed Fraunhofer flagship project “Criticality of Rare Earths” laid important foundations for substitution, efficiency improvement and recycling.

- Helmholtz Association:

- The Helmholtz Institute Freiberg for Resource Technology (HIF) at HZDR is also very active. The BioKollekt project is developing biotechnological methods (e.g., using peptides) for the selective extraction of metals, including SEE, from complex material streams such as electronic waste. The Renare project (part of the H2Giga flagship project) is investigating the recycling of critical raw materials, including SEE, from electrolyzers using innovative flotation and liquid-liquid particle extraction processes.

- EU-funded projects:

- SUSMAGPRO (completed November 2023) was a pioneering project to establish a European recycling supply chain for SEE magnets. It successfully demonstrated the production and use of recycled magnets in loudspeakers and electric motors.

- REEsilience (running until 2026) builds on the results of SUSMAGPRO and aims to establish a resilient European supply chain for SEE magnets, including through the development of software tools to optimize the use of secondary materials and improved alloy manufacturing and powder processing technologies.

- GREENE and HARMONY are newer EU projects that started in 2024. GREENE focuses on reducing the SEE content in magnets through innovative microstructure redesign. HARMONY aims to establish a pilot recycling loop for permanent magnets from various applications (wind turbines, electric motors, electronic waste).

- Other relevant projects include REMANENCE (completed, recovery of NdFeB magnets), SecREEts (extraction of SEE from phosphate rock in fertilizer production) and the completed EURARE project, which laid the foundations for a European SEE industry and assessed European deposits.

- Other stakeholders: The Öko-Institut regularly produces studies and develops strategic plans for sustainable resource management of SEE, with recycling playing a central role.

The research landscape in Germany and Europe is dynamic and addresses the entire value chain, from substitution and recycling to alternative extraction methods. A clear development is evident, moving from basic research to application-oriented pilot projects and initial commercial approaches. The networking of excellent research institutions with industry, as well as targeted funding through national and European programs, are crucial drivers in this process. However, the greatest challenge remains the successful transfer of research results into broad industrial applications and their scaling to economically viable processes (overcoming the "valley of death" for innovation). Demonstrating technical feasibility at a relevant level (high Technology Readiness Levels, TRLs) is just as important as developing viable business models.

Development and sustainable extraction of new resources

In addition to substitution and recycling, the development of new primary and secondary raw material sources is an important building block for diversifying the SEE supply.

Potential of European SEE deposits

Europe possesses geologically significant, but so far largely untapped, SEE deposits.

- Sweden: The Per Geijer deposit near Kiruna, being explored by the state-owned mining company LKAB, is considered Europe's largest known deposit, containing over 1 million tons of rare earth oxides. LKAB plans to begin mining in 2027, although full production capacity is not expected to be reached for another 10-15 years. The ore at Per Geijer contains approximately 0.2% rare earth oxides (REEs) in addition to iron and phosphate. Another important Swedish deposit is Norra Kärr, which is particularly rich in heavy REEs.

- Norway: The fen carbonatite complex in southern Norway is considered the potentially largest rare earth element (REE) deposit in Europe. Estimates suggest a total REE deposit of 8.8 million tonnes, of which approximately 1.5 million tonnes are magnetically relevant. The company Rare Earths Norway (REN) is exploring the area and considers mining realistic from 2030 onwards, which could potentially cover 10% of European demand.

- Finland: The Sokli phosphate mine in Lapland also has potential for the extraction of SEE as a by-product.

- Greenland: Deposits such as Kvanefjeld, Kringlerne, and Sarfartoq possess significant SEE resources. However, development is fraught with major challenges, including high infrastructure costs, extreme climatic conditions, a shortage of skilled workers, and complex permitting processes.

- Other occurrences: Smaller or less well-studied occurrences also exist in Germany (e.g. Storkwitz in Saxony, which is considered uneconomical, and Bavarian clays with low concentrations), Greece and Spain.

However, developing these European deposits faces significant hurdles. These include often high investment and operating costs compared to established producers like China, lengthy and complex permitting processes (often 10-15 years), strict environmental regulations (particularly regarding radioactive trace materials such as thorium and uranium), and the need to gain public acceptance for mining projects. While these deposits could contribute to diversification in the long term, they do not offer a short-term solution to current dependencies. A bridging strategy that relies on recycling, substitution, and diversifying existing import sources is therefore essential.

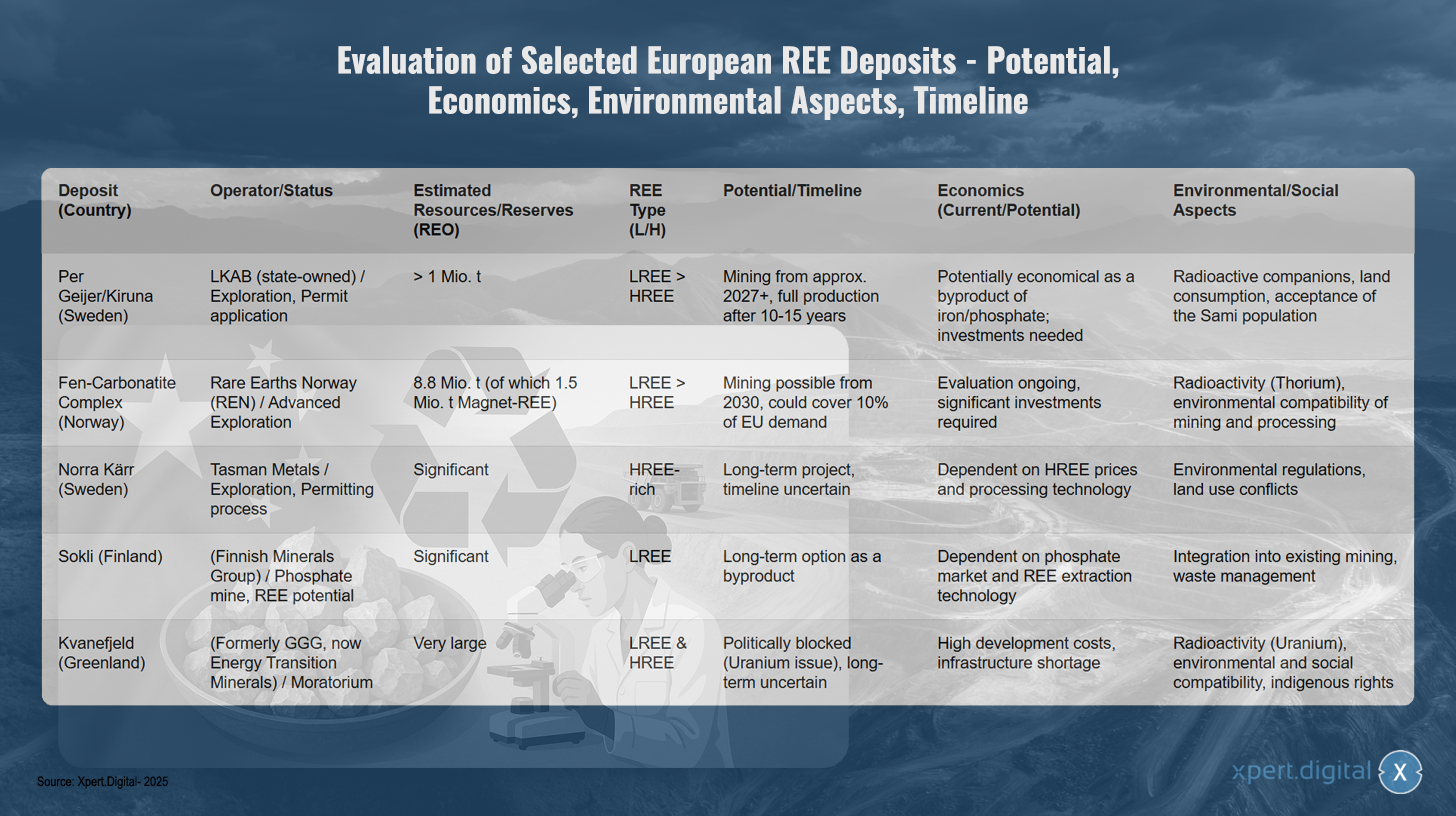

Evaluation of selected European SEE deposits – potential, economic viability, environmental aspects, timeline

Evaluation of selected European SEE deposits – potential, economic viability, environmental aspects, timeline – Image: Xpert.Digital

The evaluation of selected European rare earth deposits reveals varying stages of development and potential. The Swedish Per Geijer/Kiruna deposit is operated by the state-owned LKAB and is currently in the exploration phase with a permit application pending. With estimated resources exceeding one million tons of rare earth elements (SE) and a higher proportion of light rare earths, mining could begin as early as 2027, although full production would not be reached for another 10-15 years. While the deposit is potentially economically viable as a by-product of iron and phosphate mining, it requires substantial investment. Challenges include radioactive traces, land use, and gaining acceptance from the Sami population.

The Norwegian fen carbonatite complex is being developed by Rare Earths Norway and is in advanced exploration. With estimated resources of 8.8 million tonnes, including 1.5 million tonnes of magnetic sea-sea ore, mining could be possible from 2030 onwards, potentially covering ten percent of EU demand. The economic assessment is still underway, and significant investment is required. Environmental concerns include radioactivity from thorium and the environmental impact of mining and processing.

Tasman Metals' Norra Kärr project in Sweden is rich in heavy rare earth elements and is currently undergoing the permitting process. As a long-term project with an uncertain timeline, its economic viability depends on HSEE prices and processing technology. Environmental regulations and land-use conflicts present further challenges.

The Finnish Sokli deposit, owned by Finnish Minerals Group, offers low-emission renewable (LEE) phosphate potential with significant low-emission renewable (LSEE) deposits. As a long-term option for by-products, its economic viability depends on the phosphate market and LEE extraction technology. Integration into existing mining operations and waste management are key considerations.

The Kvanefjeld deposit in Greenland, formerly owned by GGG and now by Energy Transition Minerals, contains very large reserves of both light and heavy rare earth elements. However, the project is politically blocked by a moratorium due to the problematic nature of uranium. High development costs, a lack of infrastructure, radioactivity from uranium, as well as environmental, social, and indigenous legal issues make long-term development uncertain.

Research into alternative extraction methods

In parallel with the exploration of conventional deposits, intensive research is being conducted into alternative ways of extracting SEE from secondary sources and using novel methods.

- Industrial waste as a source of raw materials (Urban/Industrial Mining):

- Coal (fly) ash: In the USA, significant concentrations of heavy SEEs have been identified in coal ash from the Powder River Basin. In the UK, a project funded by Innovate UK (Mormair and Materials Processing Institute, October 2024 – August 2025) is underway to recover neodymium, praseodymium, and scandium from coal fly ash using a pilot-scale combination of chemical looping reactors and carbochlorination. Extraction from coal fly ash using ionic liquids is also being investigated.

- Red mud (bauxite residue): As a byproduct of aluminum production, red mud is generated in large quantities and also contains SEE (especially cerium, lanthanum, neodymium, and scandium). The completed EU project REDMUD focused on the complete utilization of bauxite residues, including SEE recovery. However, the concentrations are often low, and extraction is complex.

- Phosphorus gypsum (fertilizer production): The EU project SecREEts has successfully demonstrated pilot-scale processes for extracting SEE (Nd, Pr, Dy) from the process streams of phosphate fertilizer production. This approach is considered particularly sustainable because it is based on already mined material and does not generate new mining waste.

- Biotechnological processes:

- Bioleaching and biomineralization: The use of specific microorganisms (bacteria, fungi) or their metabolic products (e.g., organic acids, enzymes, peptides) for the selective dissolution (bioleaching) or binding (biosorption, biomineralization) of metals from ores or waste streams is a promising field of research. The Helmholtz Institute Freiberg (HIF) at the HZDR (BioKollekt project), for example, is working on the use of peptides for the selective binding of rare earth elements (REEs) from electronic waste. At LMU Munich, the use of lanthanide-dependent bacteria for the extraction of REEs from industrial waste and mining waters is being investigated, with the bacterial strain SolV showing promising results. The bioleaching of magnetic waste is also being studied.

- Phytomining: This involves utilizing plants that accumulate metals from the soil. The metals can then be extracted by harvesting and incinerating the plant biomass. However, this process is still in a very early stage of research, and its economic viability for SEE (soil-based renewable energy) has not yet been proven.

- Technology Readiness Level (TRL): Many of these alternative extraction methods are still in early research or pilot phases (TRL 3-6). Scalability to industrial scale and economic competitiveness are often not yet achieved and require further intensive research and development.

Developing alternative sources of renewable energy from waste streams and using biotechnological processes is very promising in terms of sustainability and potentially lower environmental impact compared to primary mining. These approaches could make a significant contribution to the circular economy and reduce dependence on newly extracted raw materials. However, the path to industrial maturity and economic viability for these technologies is still long and requires substantial and long-term investments in research, development, and scaling. They therefore represent more of a medium- to long-term option.

Development of more environmentally friendly separation and refining processes

Conventional separation of SEE, mostly using solvent extraction, is an energy-intensive process that requires large quantities of chemicals (acids, organic solvents) and generates environmentally harmful waste. Therefore, research into more environmentally friendly and efficient separation methods is of great importance, not only for primary raw materials but also for recycling.

- Ionic liquids (ILs) and deep eutectic solvents (DES): These are being intensively researched as "green" solvent alternatives. They are characterized by low vapor pressure, non-flammability, and often high selectivity for certain metals. Research in this area is being conducted, among other places, at the University of Rostock. A special issue of the journal Minerals was dedicated to this topic in 2023/2024, with strong European participation.

- Challenges and TRL: Despite promising laboratory results, the cost of ILs/DES, their long-term stability under process conditions, efficient solvent recovery, and process scalability remain major challenges. Many of these approaches are still at laboratory or, at best, pilot scale (TRL often < 6). Although intensive research has been conducted for years, there have been no widespread commercial breakthroughs in the SEE industry to date.

The development of new, more environmentally friendly and cost-efficient separation processes is a crucial key to significantly improving the environmental footprint of the entire SEE value chain (from both primary and secondary sources). This is a core area for technological innovation that would enable a truly sustainable European SEE supply. Without advances in separation technology, building an independent European value chain will remain difficult, even if primary or secondary raw materials were available.

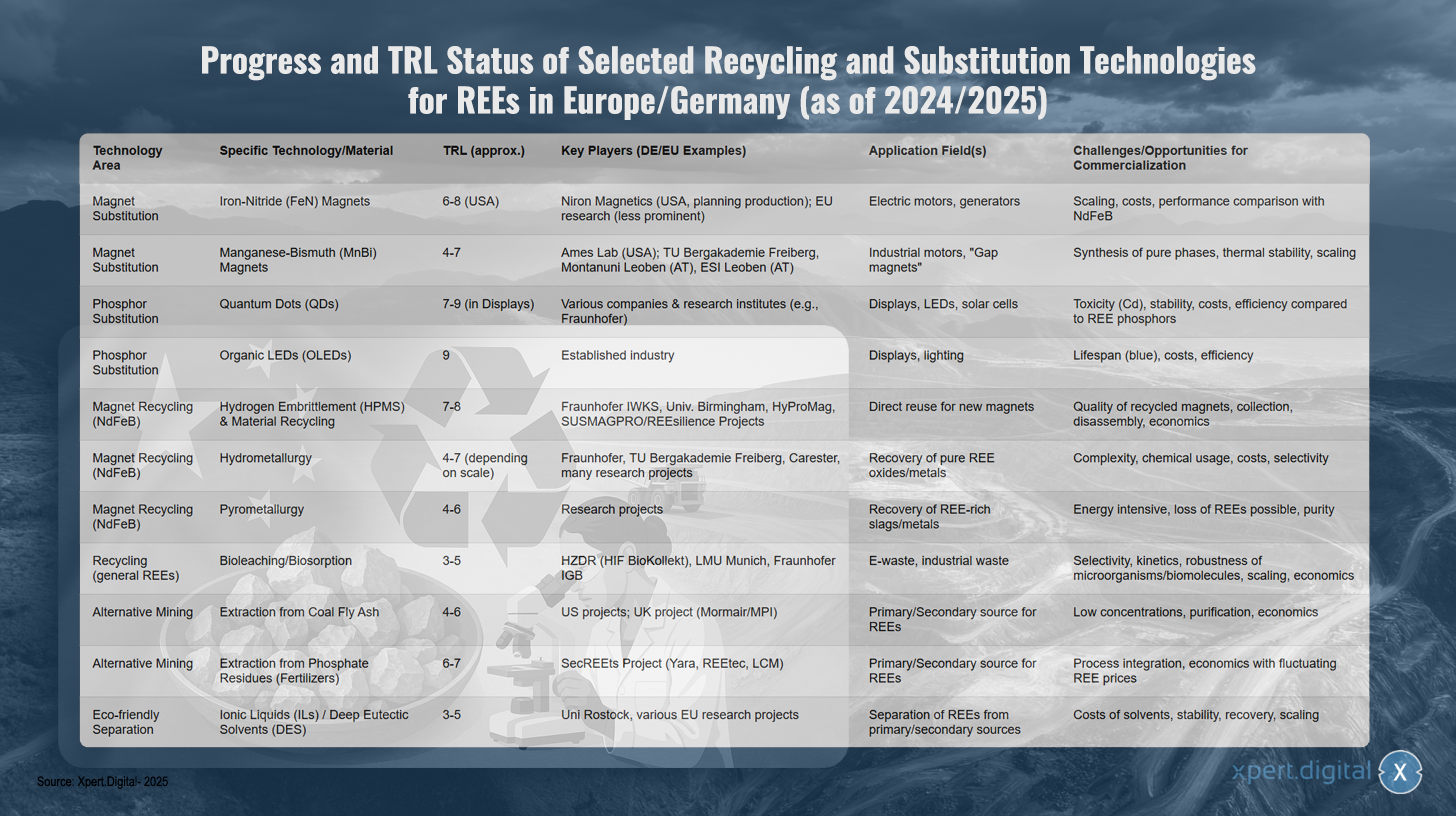

Progress and TRL status of selected recycling and substitution technologies for SEE in Europe/Germany (as of 2024/2025)

Progress and TRL status of selected recycling and substitution technologies for SEE in Europe/Germany (as of 2024/2025) – Image: Xpert.Digital

TRL (Technology Readiness Level): 1-3 Basic research, 4-6 Validation/demonstration in the laboratory/relevant environment, 7-9 Prototype/system demonstration in an operational environment, commercial application.

The European and German research landscape is showing significant progress in recycling and substitution technologies for rare earth elements, with various approaches reaching different levels of maturity. In the field of magnet substitution, iron-nitride magnets are developing with a technology maturity level of 6-8, particularly in the USA through Niron Magnetics, while EU research is less prominent. This technology targets applications in electric motors and generators but faces challenges in scaling, cost, and performance comparison with conventional NdFeB magnets.

Manganese-bismuth magnets, with a TRL of 4-7, are in an early stage of development. Besides the Ames Lab in the USA, German and Austrian institutions such as the TU Bergakademie Freiberg and the Montanuniversität Leoben are also conducting research. The main application areas are industrial motors and so-called "gap magnets," while the synthesis of pure phases, thermal stability, and scalability represent the key challenges.

In phosphor substitution, quantum dots have already reached a high maturity level of 7-9 in display applications, with the participation of various companies and research institutes such as Fraunhofer. Despite promising applications in displays, LEDs, and solar cells, challenges remain regarding toxicity, stability, and efficiency compared to SEE phosphors. Organic LEDs, with a TRL of 9, have already reached market maturity and are an established industry in displays and lighting, but they continue to struggle with lifetime issues for blue LEDs, as well as cost and efficiency concerns.

The recycling of NdFeB magnets shows several promising approaches. Hydrogen embrittlement combined with material recycling has achieved a TRL of 7-8, with German institutions such as the Fraunhofer IWKS, together with international partners and EU projects like HyProMag and SUSMAGPRO/REEsilience, leading the way. This technology enables the direct reuse of NdFeB magnets for new magnets but faces challenges regarding the quality of recycled magnets, collection, dismantling, and economic viability.

Hydrometallurgical processes with a TRL of 4-7 are being developed by Fraunhofer, the TU Bergakademie Freiberg, and companies like Carester, and aim to recover pure SEE oxides and metals. The complexity of the processes, the use of chemicals, costs, and selectivity issues remain key challenges. Pyrometallurgical approaches, with a TRL of 4-6, are still in the research phase and struggle with energy intensity, potential SEE losses, and purity problems.

Innovative biological processes such as bioleaching and biosorption are being researched for e-waste and industrial waste by institutions like HZDR, LMU Munich, and Fraunhofer IGB, with a TRL of 3-5. Challenges lie in the selectivity, kinetics, robustness of the microorganisms, and economic scalability.

Alternative extraction methods also show potential. Extraction from coal fly ash with a TRL of 4-6 is being pursued mainly in US and UK projects, while extraction from phosphate residues from fertilizer production in the SecREEts project with partners such as Yara and REEtec has achieved a TRL of 6-7. Both approaches struggle with low concentrations and economic viability issues.

Environmentally friendly separation technologies using ionic liquids and deep eutectic solvents are still in the early stages of research, with a TRL of 3-5. The University of Rostock and various EU projects are involved in this field. The challenges lie in the cost of the solvents, their stability, recovery, and scalability for industrial applications.

Our recommendation: 🌍 Limitless reach 🔗 Connected 🌐 Multilingual 💪 Sales power: 💡 Authentic with strategy 🚀 Innovation meets 🧠 Intuition

From local to global: SMEs conquer the world market with a clever strategy - Image: Xpert.Digital

In an era where a company's digital presence determines its success, the challenge lies in creating an authentic, personalized, and far-reaching presence. Xpert.Digital offers an innovative solution that positions itself as the intersection of an industry hub, a blog, and a brand ambassador. It combines the advantages of communication and sales channels in a single platform and enables publication in 18 different languages. Cooperation with partner portals and the ability to publish articles on Google News and a press distribution list with approximately 8,000 journalists and readers maximize the reach and visibility of the content. This represents a crucial factor in external sales and marketing (SMarketing).

More information here:

Rare earths as Germany's Achilles' heel: Why Germany must act now to secure its resource sovereignty

Strategic options for Germany towards long-term independence

To reduce its significant dependence on rare earth elements, particularly on China, and to ensure long-term security of supply, Germany has a number of strategic options available at the national and European levels. These include policy decisions, the development of resilient value chains, the intensification of international cooperation, and the targeted strengthening of its own technological leadership.

National and European policymaking

The political framework is crucial to initiating and supporting the necessary transformations in raw material supply.

German Raw Materials Strategy and National Circular Economy Strategy (NKWS)

The German raw materials strategy, last updated in 2020, aims to support companies in securing a safe and sustainable supply of raw materials. Key pillars include diversifying sources of supply, promoting recycling and material efficiency, strengthening domestic raw material extraction (where possible and practical), and supporting German companies in international competition. The strategy specifically emphasizes the importance of research and development for substitution and more efficient recycling processes for critical raw materials such as sessile and reticulous (SRE) raw materials.

The National Circular Economy Strategy (NKWS), adopted by the German Federal Government in December 2024, sets important complementary priorities in this area. Its key objectives relevant to the Sustainable Development Economy (SEE) include:

- Reduction of primary raw material consumption: In the long term, per capita consumption of primary raw materials in Germany should be significantly reduced.

- Closing material cycles: The share of secondary raw materials in material use should be significantly increased; the EU aims for a doubling by 2030, a goal that the NKWS (National Centre for Recycled Materials) adopts.

- Strengthening raw material independence: The explicit goal is to cover 25% of the demand for strategic raw materials such as rare earths or lithium by recycling by 2030, which is in line with the EU Critical Raw Materials Act.

The implementation of these strategies to date is viewed critically. Experts point to a gap between the stated goals and their actual implementation, particularly regarding the provision of sufficient funding, the acceleration of approval processes for domestic projects, and the lack of investment from industry as long as global market prices for unseaworthy renewable energy (SEE) remain comparatively low. A lack of strategic thinking and concrete, binding measures is criticized. The Nationally Renewable Energy Strategy (NKWS) is a newer approach whose effectiveness remains to be proven. There is a clear conflict of objectives between the long-term need for strategic planning and short-term economic considerations, a conflict that must be overcome through political steering.

EU Critical Raw Materials Act (CRMA)

The EU Critical Raw Materials Act (CRMA), which entered into force in May 2024, forms the central European legal framework for strengthening the security of supply of critical and strategic raw materials. Its core targets for 2030 are ambitious:

- At least 10% of the EU's annual demand for strategic raw materials should come from domestic production.

- At least 40% should be further processed in the EU.

- At least 25% should be covered by recycling within the EU.

- Dependence on a single third country for a strategic raw material should be limited to a maximum of 65%.

A key component of CRMA is the identification and promotion of so-called strategic projects. These can benefit from accelerated permitting processes (a maximum of 27 months for mining projects, 15 months for processing and recycling projects) and financial support. In March 2025, an initial list of 47 such projects was published, primarily concerning battery raw materials, but also including rare earth projects (e.g., the Kiruna mining project in Sweden and recycling initiatives such as the Pulawy project in Poland). For implementation in Germany, national contact points for these projects must be designated (deadline: February 2025), with the Federal Ministry for Economic Affairs and Climate Action (BMWK) and the German Mineral Resources Agency (DERA) playing a coordinating role.

The CRMA has received mixed reviews. On the one hand, it is seen as an important and necessary step towards addressing resource dependency. On the other hand, there are doubts about the technical and environmental feasibility of the ambitious targets, particularly for rare earth elements, within the set timeframe. The often very long permitting processes for mining projects (10-15 years) stand in stark contrast to the deadlines targeted by the CRMA. Furthermore, public opposition to new mining or processing projects in Europe could slow down implementation. The success of the CRMA will depend crucially on its consistent implementation by the member states, the mobilization of substantial private investment, and the resolution of conflicting objectives, such as those between rapid permitting and high environmental standards.

Funding programs and initiatives

To support the strategic goals, there is a wide range of funding programs at the German and European levels:

- Germany: The Federal Ministry for Climate Action, Environment, Energy, Mobility, Innovation and Technology (BMK) and the Federal Ministry of Education and Research (BMBF) offer various programs that address research, development, and innovation in the areas of critical raw materials, resource efficiency, and the circular economy. These include the newly launched Raw Materials Fund, the STARK program (Strengthening the Dynamics of Transformation and Innovation in the Mining Regions and at Coal-Fired Power Plant Sites), and untied financial loans (UFK guarantees) to secure projects abroad.

- EU: Programmes such as Horizon Europe, InvestEU and LIFE offer funding opportunities for research, innovation and the implementation of technologies in the areas of SEE substitution, recycling and sustainable extraction. The Innovation Fund can provide funding for recycling capacities.

- Initiatives: The European Raw Materials Alliance (ERMA) plays a key role in identifying and promoting investment projects along the entire SEE value chain in Europe. ERMA has set the goal that by 2030, 20% of Europe's demand for SEE magnets could be met by EU-grown production, for which investments of around €1.7 billion have been identified. Resource efficiency programs such as ProgRess in Germany also contribute to raising awareness and initiating measures.

Although numerous funding instruments exist, their effective coordination, accessibility, particularly for small and medium-sized enterprises (SMEs), and sufficient financial resources relative to the scale of the challenge are crucial for their effectiveness. Fragmentation of the funding landscape and bureaucratic hurdles could diminish the intended impact and delay the urgently needed rapid capacity building.

Overview of EU and German political strategies and funding programs relevant to rare earths (selection)

Overview of EU and German political strategies and funding programs relevant to rare earths (selection) – Image: Xpert.Digital

The European Union and Germany have developed various policy strategies and funding programs that are particularly relevant for rare earth elements. The EU Critical Raw Materials Act (CRMA) aims to achieve domestic production of 10 percent of the required raw materials by 2030, processing of 40 percent domestically, and recycling of 25 percent, while limiting dependence on a single third country to a maximum of 65 percent. Funding is provided for strategic projects in the areas of mining, processing, and recycling, as well as research and innovation.

The German Federal Government's raw materials strategy, led by the Federal Ministry for Climate Action, Environment, Energy, Mobility, Innovation and Technology (BMK), focuses on diversification, recycling, and domestic extraction where feasible, as well as research and development for substitution. Measures for diversification, research and development for recycling and substitution, and the assessment of domestic potential are supported. The National Circular Economy Strategy of the Federal Ministry for the Environment, Nature Conservation, Nuclear Safety and Consumer Protection (BMUV) and the BMWK aims to cover 25 percent of the demand for strategic raw materials through recycling and to reduce primary raw material consumption. Funding is provided for the development of recycling capacities, design for recycling, and research and development of recycling technologies.

The German Raw Materials Fund, a joint initiative of the Federal Ministry for Economic Affairs and Energy (BMWi) and the German Development Bank (KfW), aims to contribute to security of raw material supply and reduce dependencies by supporting projects for the extraction, processing, and recycling of critical and strategic raw materials both domestically and internationally. The BMWi's STARK funding program supports the transformation of coal-mining regions and promotes the production and recovery of critical raw materials for key components.

At the European level, Horizon Europe strengthens the scientific and technological foundations and promotes innovation, particularly research and innovation in substitution, recycling, sustainable extraction, and new materials. The European Raw Materials Alliance (ERMA), a joint initiative of EIT RawMaterials and the EU, works to build resilient EU value chains for raw materials and identifies and supports investment projects in the mining, processing, and recycling of rare earth elements. The German BMBF's "SME Innovative: Resource Efficiency and Circular Economy" program strengthens research and development in small and medium-sized enterprises and promotes the efficient supply and use of critical raw materials, innovative recycling processes, and circular products.

Building resilient value chains in Germany and Europe

Building resilient, locally sourced rare earth value chains in Europe is a key element in reducing dependence on China. This requires efforts across all stages, from raw material extraction and processing to the manufacture of end products and recycling.

Opportunities and challenges in building domestic processing and refining capacities

A critical bottleneck in the current European SEE landscape is the lack of significant capacity for separating raw SEE into high-purity single oxides and for subsequent metal production. Even if Europe were to increase its primary or secondary raw material production, these would often have to be exported to China for further processing, which would only shift the dependency.

- Necessity: The development of European separation plants and metallurgicals is essential to achieve genuine vertical integration and strategic autonomy.

- Examples of approaches: In Estonia, Neo Performance Materials (Silmet) already operates a separation plant, which, however, relies on imported concentrates. In France, there are plans for a plant in La Rochelle, and the Caremag project in Lacq aims for integrated processing and recycling. There are also initiatives in Poland (Pulawy project).

- Economic viability: Building such plants is extremely capital-intensive. Investment costs are high, and European producers would have to compete with established and often state-subsidized Chinese companies. Long-term purchase agreements and stable pricing would be necessary to incentivize investment.

- Technological hurdles: Specific know-how is required for the complex separation processes. Furthermore, environmentally friendly and energy-efficient processes must be developed and scaled up to meet high European environmental standards.

- LSEE vs. HSEE: The development of processing capacities for heavy SEE (HSEE) requires special attention, as the dependence on China (including the processing of raw materials from Myanmar) is almost 100% and these elements are critical for high-performance magnets.

Building a complete European SEE value chain is a generational project that is hardly feasible without massive government start-up funding, long-term political commitments, and close cooperation between public and private stakeholders. Focusing solely on domestic mining, without simultaneously developing processing, metal production, and magnet manufacturing capacities, would not fundamentally resolve the strategic dependency.

“Design for Recycling” as a long-term strategy

Another important long-term strategy is the design of products containing rare earth elements in line with the principles of a circular economy (“Design for Recycling”, DfR).

- Objectives: Products should be designed in such a way that components containing rare earth elements (e.g., magnets in electric motors) can be easily identified, disassembled, and recycled by type at the end of the product's life. This would significantly increase the efficiency and cost-effectiveness of recycling.

- Tools: The introduction of digital product passports, containing detailed information on material composition and disassembly instructions, is seen as an important tool for creating the necessary transparency for effective recycling. Standardization efforts are also relevant here.

- Challenges: Implementing DfR principles is complex, especially in globalized supply chains with diverse manufacturers and product designs. Developing and enforcing binding standards is a major challenge.

Design for Recycling (DfR) is an essential strategy, but one with a very long-term impact. Its full effect on the availability of secondary raw materials will only be realized when products designed today according to DfR principles reach the end of their life cycle in 10, 15, or more years. In the short term, DfR cannot solve current supply problems, but it is indispensable for building a sustainable and resilient circular economy for secondary raw materials in the future.

International cooperation and diversification

Since complete self-sufficiency in rare earths for Germany and Europe is unrealistic in the short to medium term, international cooperation and the diversification of sources of supply play a central role in any resilience strategy.

Potential and sustainability assessment of raw material partnerships

Germany and the EU are intensifying their efforts to establish and expand raw material partnerships with various countries worldwide.

- Example countries and focus raw materials:

- Chile: Focus on lithium and copper, but also potential for other minerals. Cooperation agreements were reaffirmed in January 2023 and June 2024, with a focus on sustainable mining and scientific exchange.

- Mongolia: Partnership since 2011, strategic partnership since February 2024. Focus on copper and rare earth elements (neodymium, praseodymium). Support for the German-Mongolian University of Raw Materials and Technology.

- Australia: Energy and raw materials cooperation since 2017, with an increasing focus on climate protection and critical minerals. The "Australia-Germany Critical Minerals Supply Chains Study" aims to identify value creation potential.

- Canada: Strategic partnership in the area of critical raw materials.

- Other partners: Kazakhstan, Ukraine, Greenland, as well as various African (e.g. Namibia, Zambia, DR Congo) and South American countries (e.g. Argentina) are the focus of the EU for raw material partnerships.

- Goals of the partnerships: In addition to diversifying supply sources, the aim is also to support partner countries in sustainable raw material extraction, promote local value creation (e.g. by building processing capacities) and establish high environmental, social and governance (ESG) standards.

- Challenges and risks: Implementing such partnerships is complex. Compliance with ESG standards must be ensured, and greenwashing must be avoided. Many potential partner countries are politically unstable or exhibit governance deficiencies. Furthermore, there is intense competition, particularly with China, for access to raw materials and influence in these countries. Simply shifting dependence from one dominant actor (China) to several potentially unstable or Chinese-influenced actors does not fully resolve the fundamental issue of resilience. A very careful selection of partners and intelligently designed agreements are essential, creating genuine win-win benefits rather than merely pursuing one-sided interests.

Geopolitical implications and long-term stability

The supply of critical raw materials such as rare earths has long since become a central area of geopolitical conflict.

- Instrumentalization of raw material supplies: The risk that raw material supplies will be used as a political tool in international conflicts is real and has already led to significant market distortions in the past.

- The need for a coherent European strategy: Given this geopolitical dimension, a purely economically or technologically driven raw materials policy is insufficient. A coherent European foreign trade, security, and development policy is needed that integrates raw material aspects. Securing the supply of SEE (separately renewable energy resources) is therefore inextricably linked to strengthening European sovereignty and shaping resilient international relations. This requires close coordination within the EU and with like-minded international partners.

Strengthening technological leadership

The development and application of its own advanced technologies in the field of substitution, recycling and sustainable extraction of rare earths offers Germany the chance to reduce its dependence and at the same time unlock new economic potential.

Germany's innovation potential in substitution, recycling and sustainable extraction

Germany has a strong and broad research landscape in the field of materials science, chemistry and process engineering, both at universities and at non-university research institutions (e.g. Fraunhofer Society, Helmholtz Association, Leibniz Association) and in industry.

- Areas of strength: As detailed in Section III, there are promising research approaches in Germany and Europe for the development of SEE-free magnets, more efficient catalysts and phosphors, innovative recycling processes (e.g. HPMS, hydrometallurgical and biotechnological approaches) and for the recovery of SEE from alternative sources.

- Technology transfer challenge: A key challenge is to translate excellent research results into industrial applications and marketable products more quickly and effectively (transfer research). A gap often exists between basic research/pilot projects and commercial scaling.

- Global competition: Germany and Europe are engaged in intense global competition for technological leadership, particularly with the USA and China, which are also investing heavily in these areas. To succeed, targeted and substantial support for key technologies, the development of pilot plants, and the creation of leading markets for sustainable and innovative products are essential.

Economic impact of the transition to REE-free technologies for key industries

The shift to technologies that require fewer or no rare earth elements has complex economic implications:

- Cost-benefit analysis: In the short term, substituting SEE may be associated with higher costs or potential performance losses in certain applications. In the long term, however, significant economic advantages can arise from eliminating expensive and price-volatile SEE, reducing supply chain risks, and opening up new markets for innovative products.

- Investment and adaptation needs: German industry, particularly in the key sectors of automotive manufacturing, renewable energies, and electronics, faces significant investment and adaptation needs to convert its production processes and products to low- or zero-renewable energy alternatives. This affects not only end products but also entire supply chains.

- Opportunities for "First Movers": German companies that adopt innovative, sustainable technologies that are independent of critical raw materials early on can secure competitive advantages as "first movers" and tap into new, promising markets. However, this requires a willingness to take risks and a long-term strategic focus.

The switch to REE-free or more REE-efficient technologies is therefore not only a question of security of supply, but also a strategic decision for the future competitiveness of German industry in global future markets.

Synthesis and recommendations for action for Germany

The analysis of the rare earth issue has highlighted Germany's and Europe's profound dependence on global, particularly Chinese, supply chains and the associated economic and geopolitical risks. At the same time, promising research approaches and strategic options are emerging to reduce this dependence and increase long-term security of supply. However, achieving greater independence is a complex undertaking that requires a coherent strategy and consistent action from both policymakers and industry.

Assessment of risks, opportunities and conflicting objectives

The supply of rare earth elements is of paramount strategic importance to Germany, as these raw materials are indispensable for key technologies in the energy transition, digitalization, and for important industries such as automotive manufacturing. The current global supply structure, dominated by China in both extraction and, in particular, processing, poses significant risks due to price volatility, supply bottlenecks, and the potential instrumentalization of raw material supplies for geopolitical purposes. These risks are further exacerbated by rising global demand.

The chances of reducing this dependency lie in a multi-pronged approach:

- Substitution and efficiency: Research into substitute materials and SEE-free technologies, especially for magnets, as well as increasing material efficiency, offer medium- to long-term potential for reducing specific SEE requirements.