Weak Chinese domestic market: China's economic power between regional dynamics and global challenges – Image: Xpert.Digital

Export giant, consumption dwarf: China's economy is caught in a dangerous dilemma

China's unequal boom: Why 4 super-provinces are carrying the country while the rest lag behind

China's economy resembles a colossus with feet of clay, presenting a picture of stark contradictions. While record exports and a historic trade surplus solidify its position as a global economic power, a closer look reveals profound structural weaknesses at home. Chronically weak domestic consumption, far below the global average, makes the world's second-largest economy dangerously dependent on global demand. This dependence is exacerbated by massive regional inequality: only a handful of wealthy coastal provinces like Guangdong and Jiangsu act as engines of growth, while large swathes of the country, particularly in the west, lag far behind economically—with income disparities that dwarf even those in Germany. At the same time, Beijing grapples with a simmering housing crisis that threatens the banking system and a demographic time bomb in the form of a shrinking working-age population. Faced with these challenges, the government is attempting to counteract them with an ambitious strategy of "dual circulation" and massive investment in "killer technologies" to strengthen domestic demand and achieve technological independence. China's economic future thus stands at a crucial turning point that will shape not only the country itself but the entire global economy.

Related to this:

Regional economic drivers and the role of the leading provinces

In short: China's economy is characterized by a weak domestic market with low consumer demand and structural problems, while exports remain very strong and drive a large portion of economic growth. This means that China's economy is heavily dependent on foreign demand and international markets, as domestic consumption is significantly lower than in comparable countries.

The Chinese economy is largely driven by a few high-performing regions, while other areas lag significantly behind. The four eastern provinces of Guangdong, Jiangsu, Shandong, and Zhejiang alone generate nearly 35 percent of the national gross domestic product, demonstrating the enormous concentration of economic power in the coastal regions. Guangdong leads with a GDP of over 129 trillion yuan and, despite a growth rate of 4.1 percent in the first quarter of 2025, which fell short of the annual target, showed an improvement of 0.6 percentage points compared to the previous year.

Shanghai improved its ranking impressively by two places, moving from 11th to 9th nationwide. With a GDP of 1.273 trillion yuan in the first quarter, the metropolis achieved growth of 5.1 percent, exceeding its annual target by 0.1 percentage points. This development underscores the adaptability of economically strong regions and their ability to adjust to changing conditions.

However, the regional disparities are significant. Per capita income in Beijing reached 190,313 yuan, while in Gansu it was only 41,864 yuan – a difference of almost fivefold. These disparities are even greater than those between Germany's weakest and strongest states. The western provinces, including Tibet and Qinghai, together generated only 6.3 percent of the economic output, highlighting the uneven development.

Convergence between the regions is happening very slowly. Studies show that it could take half a century for the differences in economic performance between administrative districts to even be halved. These structural imbalances are further exacerbated by demographic trends, as younger workers concentrate in wealthy coastal cities and provinces, while central and western provinces struggle with outmigration and declining birth rates.

Related to this:

Export economy versus domestic market

China achieved a new record export volume in 2024, reaching the equivalent of €3.4 to €3.5 trillion, representing a 5.9 percent increase compared to the previous year. This export boom resulted in a historic trade surplus of US$992 billion. Exports are growing significantly faster than global trade overall, with Chinese manufactured goods exports increasing by over ten percent in volume.

At the same time, however, imports are stagnating with growth of only 1.1 percent, indicating weak domestic demand. This development highlights the dilemma of the Chinese economy: exports serve as its main pillar, while domestic consumption continues to falter. Trade data shows that China exports in large volumes, while the value per exported unit often declines – an indication of state-subsidized overcapacity.

Domestic consumption accounts for less than 40 percent of annual economic output, roughly 20 percentage points below the global average. Interestingly, consumption patterns vary geographically: while growth in consumption has stagnated in major cities like Shanghai, Beijing, Guangzhou, and Shenzhen, smaller cities exhibit higher levels of consumption. Shanghai recorded only 0.5 percent growth in consumption, while cities such as Wenzhou, Jinhua, Taizhou, and Quanzhou significantly exceeded the national average of five percent.

The government has recognized the need to diversify away from export dependence. The "dual circulation" strategy aims to stimulate domestic consumption and reduce export reliance. This policy reflects China's understanding that it cannot rely on trade as heavily in the next two decades as it did in the previous two.

🔄📈 B2B trading platform support – Strategic planning and support for export and the global economy with Xpert.Digital 💡

B2B trading platforms - Strategic planning and support with Xpert.Digital - Image: Xpert.Digital

Business-to-business (B2B) trading platforms have become a critical component of global trade dynamics and thus a driving force for exports and global economic development. These platforms offer significant advantages to companies of all sizes, especially SMEs—small and medium-sized enterprises—which are often considered the backbone of the German economy. In a world where digital technologies are increasingly prominent, the ability to adapt and integrate is crucial for success in global competition.

More information here:

China's economy at a crossroads: Export strength meets domestic crisis

Economic stability in global comparison

China's economy exhibits both strengths and significant weaknesses that affect its stability. The country met its 2024 growth target of five percent, with government stimulus boosting the economy at the end of the year. Economic growth accelerated to 5.4 percent in the fourth quarter and to 1.6 percent quarter-on-quarter.

Nevertheless, China faces structural challenges. The real estate crisis is significantly impacting the economy, as the real estate sector at its peak accounted for around a quarter of GDP, and housing comprised almost 80 percent of private assets. In June 2024, 40 banks filed for bankruptcy within a single week—an event China had not experienced for more than 30 years. China's shadow banking system manages assets between three and twelve trillion US dollars and is heavily invested in real estate projects.

Demographic trends pose a further risk to stability. China's population shrank in 2022, 2023, and 2024, with the working-age population already declining. The working-age population between 15 and 64 has peaked and is expected to decline sharply from 2030 onward. This will cause the labor force's contribution to GDP to become negative within a few years.

China's changed position is evident in international comparisons. The USA overtook China as Germany's most important trading partner in 2024, for the first time since 2016. Trade volume between Germany and China amounted to €246 billion, while with the USA it reached €255 billion. German exports to China fell by 7.6 percent in 2024, marking the second consecutive year of decline following an 8.8 percent drop in 2023.

Related to this:

New development strategies and technological orientation

China is pursuing an ambitious strategy for technological self-sufficiency, which was underscored in the Third Plenum Document of July 2024. The strategy focuses on building a modern industrial system driven by "new quality productive forces" in high-tech sectors such as semiconductors, artificial intelligence, aerospace, and biomedicine.

The concept of "dual circulation" forms the core of the new economic strategy. It envisions two economic cycles: an internal one, capable of satisfying Chinese demand and consumption on its own, and an external cycle that complementarily optimizes the internal cycle through imports and exports. This strategy aims for greater economic independence for China while simultaneously increasing its asymmetric dependence on foreign countries.

Eleven key high-tech zones have established a collaborative network to promote AI industrial innovation, including Beijing's Zhongguancun, Shanghai's High-Tech Zone, and zones in Shenzhen, Chengdu, and other cities. China is pursuing "killer technologies" to strengthen the existential dependence of international industrial value chains on China and to develop a deterrent against supply disruptions.

The Belt and Road Initiative complements this strategy by creating new trade routes and markets. The project enables China to utilize its substantial foreign exchange reserves for investment, develop new markets for industrial surplus capacity, and contributes to the internationalization of Chinese companies. Central to this is securing new transport routes for trade and diversifying energy sources as components of a strategy designed for long-term stability.

From export miracle to internal crisis: How regional differences are slowing China down

Despite impressive export successes, China's economy faces significant challenges. Youth unemployment is just under 19 percent, and for the first time in decades, Chinese workers believe that the younger generation may not fare as well as those currently in the workforce. Geopolitical tensions with the West are leading to substantial capital outflows and an exodus of global companies.

The housing crisis continues, with 400 million square meters of vacant living space and household debt amounting to 145 percent of disposable income. Despite government support programs exceeding 200 billion yuan and interest rate cuts by the People's Bank of China to 1.5 percent, the structural weakness persists.

China's official Gini coefficient in 2022 was 0.466, although independent studies suggest values above 0.6 – significantly higher than Germany's 0.29. This inequality is exacerbated by demographic trends, as central and western provinces face labor shortages and declining productivity.

Experts forecast GDP growth of 4.5 to 4.8 percent for 2025, which is below the official target of five percent. The government is increasingly focusing on stimulating consumption, with the term "consumption" being mentioned 31 times in official documents, compared to 21 times the previous year. A "special action plan" to vigorously boost consumption is intended to stimulate domestic demand.

China's economic development thus presents a complex picture: While a few coastal regions act as economic engines and achieve impressive export successes, the country struggles with structural problems such as the real estate crisis, demographic challenges, and weak domestic demand. The new strategy of "dual circulation" and the focus on technological self-sufficiency demonstrate a willingness to transform, but its success depends on overcoming these existing challenges.

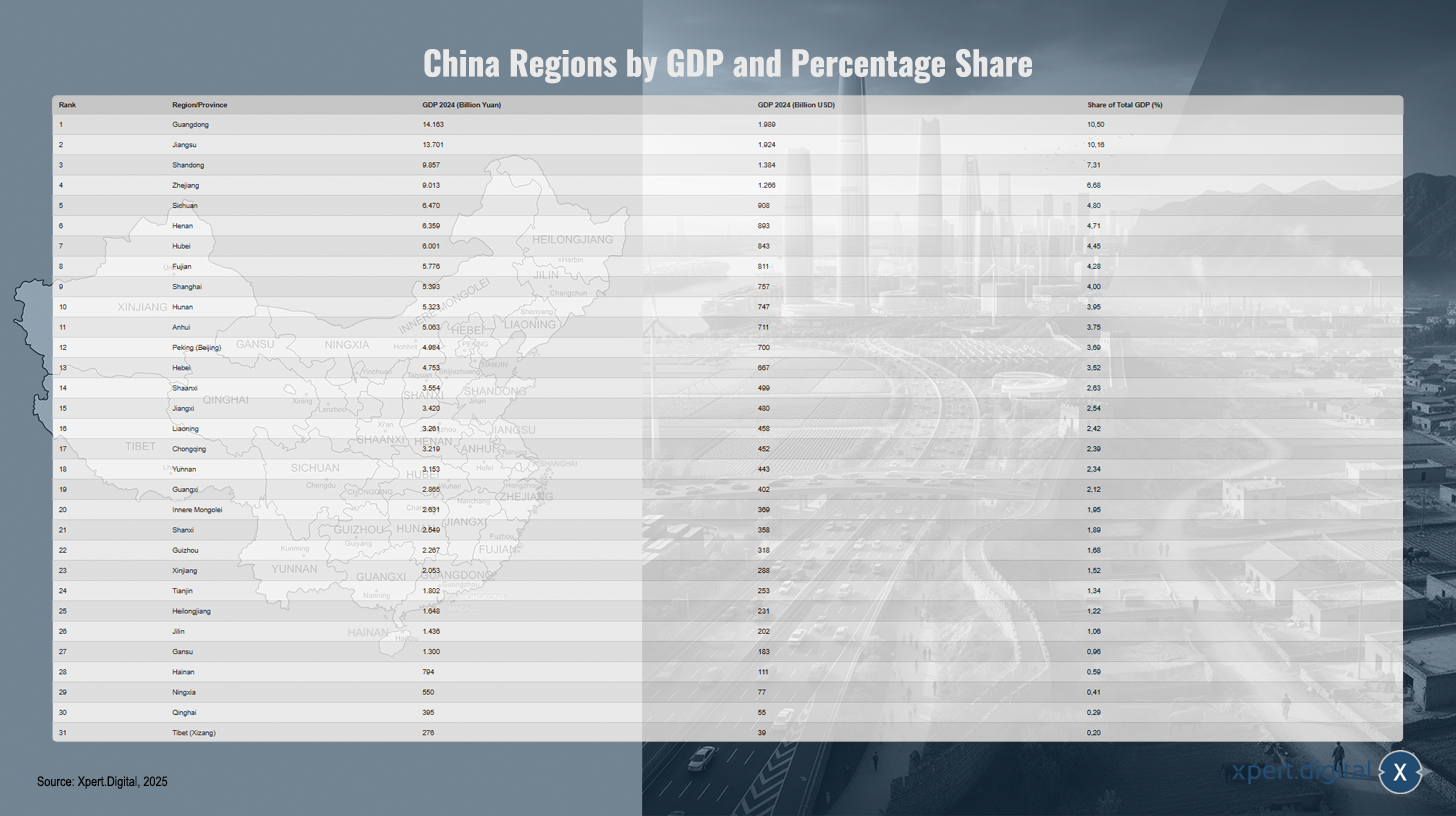

List of China's regions (Top Ten / Total list 31) by GDP and percentage share

List of China's regions (Top Ten / Total list 31) by GDP and percentage share – Image: Xpert.Digital

The complete list of all Chinese regions – comprising provinces, autonomous regions, and municipalities directly under the central government – shows their ranking by gross domestic product (GDP) for 2024, converted into yuan and US dollars, as well as their percentage share of total Chinese GDP. Guangdong leads with a GDP of 14,163 billion yuan (US$1,989 billion) and a share of 10.50%, followed by Jiangsu with 13,701 billion yuan (US$1,924 billion, 10.16%) and Shandong with 9,857 billion yuan (US$1,384 billion, 7.31%). Zhejiang ranks fourth with 9.013 billion yuan (US$1.266 billion, 6.68%), followed by Sichuan (6.470 billion yuan; US$908 billion; 4.80%) and Henan (6.359 billion yuan; US$893 billion; 4.71%). Hubei takes seventh place with 6.001 billion yuan (US$843 billion; 4.45%), while Fujian ranks eighth with 5.776 billion yuan (US$811 billion; 4.28%). Shanghai follows with 5.393 billion yuan (US$757 billion; 4.00%) and Hunan with 5.323 billion yuan (US$747 billion; 3.95%). Anhui reaches 5.063 billion yuan (US$711 billion; 3.75%), Beijing 4.984 billion yuan (US$700 billion; 3.69%), and Hebei 4.753 billion yuan (US$667 billion; 3.52%). Shaanxi follows with 3.554 billion yuan (US$499 billion; 2.63%), ahead of Jiangxi with 3.420 billion yuan (US$480 billion; 2.54%) and Liaoning with 3.261 billion yuan (US$458 billion; 2.42%). Chongqing records 3.219 billion yuan (US$452 billion; 2.39%) and Yunnan 3.153 billion yuan (US$443 billion; 2.34%). Guangxi reaches 2,865 billion yuan (US$402 billion; 2.12%) and Inner Mongolia 2,631 billion yuan (US$369 billion; 1.95%), followed by Shanxi with 2,549 billion yuan (US$358 billion; 1.89%). Guizhou comes in at 2,267 billion yuan (US$318 billion; 1.68%) and Xinjiang at 2,053 billion yuan (US$288 billion; 1.52%). Tianjin records 1,802 billion yuan (US$253 billion; 1.34%), Heilongjiang 1,648 billion yuan (US$231 billion; 1.22%) and Jilin 1,436 billion yuan (US$202 billion; 1.06%). Gansu reached 1.3 trillion yuan (US$183 billion; 0.96%), Hainan 794 billion yuan (US$111 billion; 0.59%), Ningxia 550 billion yuan (US$77 billion; 0.41%), Qinghai 395 billion yuan (US$55 billion; 0.29%), and Tibet (Xizang) 276 billion yuan (US$39 billion; 0.20%). China's total GDP for 2024 amounted to 134.908 trillion yuan, equivalent to approximately US$18.943 trillion. The percentages are based on the official exchange rates for 2024 (CNY 7.12 = US$1). Regions such as Hong Kong, Macau, and Taiwan are not included in this statistic from the cited Wikipedia source.

China's dangerous imbalance: Consumption is collapsing and nobody knows what will happen next

### China's Consumption Puzzle: Why Citizens Are Holding On to Their Money Despite Growth ### Beijing Pumps Billions into the Economy – But the Chinese Simply Aren't Buying ### The Big Fear: Why China's Weak Domestic Market Is Holding Back the Entire Economy ### More Than Just the Real Estate Crisis: The Real Problem Behind China's Weak Consumption ###

The Chinese domestic market is considered weak, especially compared to expectations and the government's long-term growth targets.

Related to this:

Causes of weakness

The most significant weakness of the domestic market lies in private consumption:

- Income growth is low, many households are saving more and spending less on leisure, education, health and consumer goods.

- The weak performance of the real estate market over the past few years has led to a loss of confidence and insecurity; as a result, many people lack the motivation to make major purchases.

- The consumption share of GDP is exceptionally low at less than 40 percent in international comparison.

Political measures and perspectives

The government is making intensive efforts to boost domestic consumption:

- In 2025, comprehensive programs to promote consumption (e.g. subsidies for purchases and interest subsidies for loans) as well as measures to increase social benefits were launched.

- Nevertheless, many analysts view the measures as insufficient or unsustainable, as structural problems such as weak social security or job insecurity remain unresolved.

Economic performance and forecasts

- According to official figures, the Chinese economy will grow by around 4.4 to 5.2 percent in 2025, with exports being a key growth driver while the domestic sector lags behind.

- Forecasts for the coming years indicate continued restraint in private consumption and slower growth.

China's domestic market is weak, despite targeted support measures. Consumption is growing less dynamically than overall GDP, and structural deficits in trust, social security systems, and the real estate sector are hindering development – a fundamental turnaround is still pending.

Details about the image (map of China): RP Chine administrative.svg: Ternoc this file: Furfur (https://commons.wikimedia.org/wiki/File:Volksrepublik_China_administrative_Gliederung.svg), “People's Republic of China administrative structure”, edited, https://creativecommons.org/licenses/by-sa/4.0/legalcode

Your global marketing and business development partner

☑️ Our business language is English or German

☑️ NEW: Correspondence in your native language!

Konrad Wolfenstein

I and my team are happy to be available to you as your personal advisor.

You can contact me by filling out the contact form here wolfenstein@xpert.digital:or simply call me at +49 7348 4088 965. My email address is

I'm looking forward to our joint project.