China's silent access to our power grid: Why the EU is now pulling the plug – Image: Xpert.Digital

Getting out of the China trap: How Europe's electricity grid can finally become independent

Why China could remotely control the European power grid – and how Europe can free itself

The expansion of renewable energies in Europe is breaking records – but behind the scenes of these glowing success stories, concerns are growing about the resilience of our critical infrastructure. While millions of households and businesses produce their own electricity with solar panels, these systems often rely on an electronic heart from China: the inverter. The risk that foreign actors could destabilize European power grids remotely has jolted policymakers out of their complacency and led to drastic funding cuts. But technological independence is only one piece of the energy transition puzzle. To unleash the full economic and ecological potential of wind and solar power, gigantic storage capacities are lacking. While the hesitant expansion of battery storage costs the economy billions annually, researchers are already working on the next revolution: iron powder as a seasonal long-term storage solution. This is an in-depth look at an interconnected system where geopolitics, billions in savings, and groundbreaking innovations converge – and where the costs of hesitation have long since outweighed the costs of action.

Europe's energy transition: between dependency, savings potential and new storage technologies

Anyone operating a photovoltaic system in Germany, Poland, or Spain today is highly likely using an inverter manufactured in China. These devices—largely unnoticed by the public—are the electronic heart of every solar power system. They convert the direct current generated by the modules into grid-compatible alternating current and are typically permanently connected to the internet to transmit operating data, receive firmware updates, and provide grid services. It is precisely this internet connection that has increasingly worried security experts for several years.

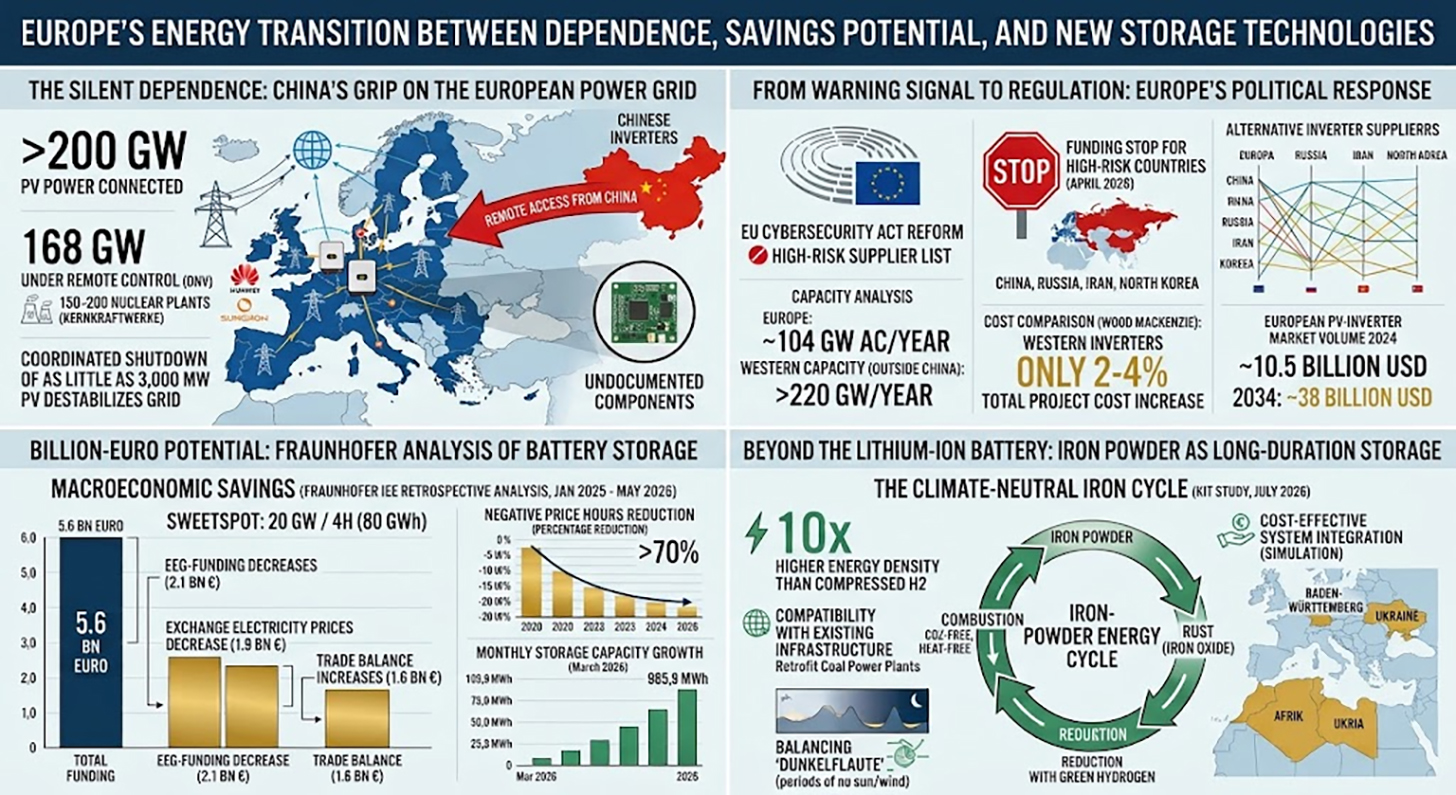

The figures are both impressive and alarming: Over 200 gigawatts of photovoltaic capacity in Europe are currently connected to Chinese inverters. According to a report by the Norwegian testing and quality institute DNV, the two dominant providers, Huawei and Sungrow, already remotely control 168 gigawatts of PV capacity on the continent. DNV predicts this figure could rise to over 400 gigawatts by 2030 – equivalent to the combined output of 150 to 200 nuclear power plants. In such a scenario, Europe would effectively have relinquished remote control over a significant and growing portion of its electricity generation infrastructure to foreign manufacturers.

What sounds like an abstract risk in theory has already been given initial practical evidence. According to media reports, US investigators have discovered undocumented radio modules in imported inverters that fall outside the official technical specifications. In Denmark, the industry association Green Power Denmark encountered unexplained electronic components during the inspection of imported circuit boards. The DNV report shows in simulations that a coordinated shutdown of just 3,000 megawatts of PV capacity – a small fraction of the installed capacity – could have significant, destabilizing effects on the European power grid. Given that market-dominating manufacturers each have access to more than 10,000 megawatts of installed inverter capacity, the potential for attack is structurally considerable.

From warning signal to regulation: Europe's political reaction

Europe's political response to this situation was hesitant for a long time, but has gained considerable momentum since the beginning of 2026. In January 2026, Henna Virkkunen, Executive Vice-President of the European Commission for Technological Sovereignty, Security and Democracy, made it clear in the European Parliament that dependence on a very limited number of inverter manufacturers poses a significant security risk. The ongoing reform of the European Cybersecurity Law envisages the introduction of a so-called high-risk manufacturer list, modeled on the 5G Toolbox.

In April 2026, the EU significantly escalated its measures: The European Commission halted funding for all energy projects using inverters from four so-called high-risk countries. These are China, Russia, Iran, and North Korea – but in practice, this measure amounts to a ban on subsidies for Huawei and Sungrow devices. The funding freeze applies immediately to new projects and has an enormous reach: In 2025, the European Investment Bank financed around one-fifth of all solar projects in the EU, and most of these projects had previously used Chinese inverters. The regulation also affects projects in neighboring EU regions such as North Africa and the Balkans, provided they are connected to the European grid.

Lithuania acted earlier than the European Commission: Since May 1, 2025, a Lithuanian law has prohibited Chinese manufacturers from remotely accessing the country's solar, wind, and battery storage systems via software. The law applies to new installations and mandates a technical upgrade for existing installations with a capacity of 100 kilowatts or more during a transition period until May 2026. The ESMC considers this approach a blueprint and is calling for its adoption by all EU member states. In parallel, the revised EU Radio Equipment Directive came into force in August 2025, stipulating that only internet-connected devices that meet basic cybersecurity requirements and do not contain undocumented remote access functions may be sold on the internal market.

Inverters excluding China: What capacity analyses really show

The most obvious objection to a consistent displacement of Chinese inverters is: Who will meet the demand? Can European and other Western manufacturers fill the resulting gap without the expansion of solar power stalling or costs exploding?

In a survey conducted in February 2026 among Western manufacturers, and based on data from S&P Global Commodity Insights, ESMC presented the first comprehensive capacity analysis, the results of which significantly alleviate these concerns. The analysis quantifies European inverter production capacity at approximately 104 gigawatts of AC power per year. In addition, there are more than 120 gigawatts of manufacturing capacity from manufacturers in North and South America, as well as in the Asia-Pacific region outside of China. Specifically for the European market, according to S&P Global, more than 53 gigawatts of production capacity are available – a figure that corresponds almost exactly to the total newly installed photovoltaic capacity in the European Union in 2025.

The ESMC survey specifically questioned six Western manufacturers about their presence in Eastern Europe and yielded a clear result: A combined installed capacity of approximately 14 gigawatts was identified in eight eastern EU markets, with a market presence dating back to around 2010 and approximately 330 sales and service employees working on-site or remotely. The manufacturers also indicated their ability to significantly expand sales and support within about six months. Poland stands out in particular: All six companies surveyed are active there, with a total installed capacity of 4,430 megawatts and approximately 74 permanently assigned employees.

These figures suggest that the often-cited supply chain dependency on China for inverters is structurally less compelling than the current market share would suggest. The high Chinese market share – in 2023, 70 percent of all newly installed inverters in Europe came from Chinese suppliers – is primarily due to massive cost advantages and aggressive pricing, not to a capacity gap among alternative manufacturers.

The question of cost: How much more expensive is security of supply?

Security of supply and technological sovereignty come at a price – but how high is it really? An analysis by the market research company Wood Mackenzie provides revealing data: Using a Western inverter instead of a Chinese one increases the overall costs of a commercial or ground-mounted project by only about two percent. For string inverters in residential buildings, the price premium is around three to four percent.

Measured against the total investment costs of a solar power plant, where module prices, installation costs, grid connection, and planning costs are the dominant factors, the inverter, at approximately ten to fifteen percent of the plant costs, already represents a mid-range cost segment. Two percent additional costs at the project level—that is an economically manageable figure, especially when compared to the risks posed by uncontrolled remote access to critical infrastructure. The ESMC points out that coordinated manipulation of inverters leading to the failure of significant generation capacity would cause economic damage far exceeding the cost savings.

Despite the intense competitive pressure of recent years, European manufacturers like SMA Solar from Kassel have maintained and modernized their technical capabilities. In 2025, SMA achieved a turnover of €1.27 billion in its large-scale project business, with an EBIT margin of 16.6 percent, and expects a significant improvement in earnings for 2026 – also benefiting from the EU subsidy freeze. The European PV inverter market had a volume of approximately US$10.5 billion in 2024 and, according to Global Market Insights, is projected to grow to nearly US$38 billion by 2034. The subsidy freeze thus acts not only as a security policy measure but also as an industrial policy that structurally benefits European manufacturers.

The billion-dollar potential of battery storage: The Fraunhofer analysis in detail

While the debate surrounding inverters primarily revolves around security of supply and risks of dependency, a new analysis by the Fraunhofer Institute for Energy Economics and Energy System Technology reveals a complementary dimension of the electricity system: the significant potential for macroeconomic savings through the accelerated expansion of battery storage. The study was commissioned by the German Renewable Energy Federation (BEE), the German Solar Association (BSW), and the German Wind Energy Association (BWE) and presented in Berlin in July 2026.

In a backward analysis, researchers simulated the cost effects of a hypothetical earlier deployment of battery storage in the German electricity system. Specifically, they retrospectively added battery storage capacities of 10 to 40 gigawatts and storage durations of two to eight hours to the system model for the period from January 2025 to the end of May 2026. The result boils down to one key figure: Had 20 gigawatts of additional storage capacity with four hours of storage per hour – totaling 80 gigawatt-hours – been available during this 17-month period, it would have resulted in economic savings of €5.6 billion. Extrapolated to an annual figure, this equates to approximately €3.9 billion.

The study precisely identifies the sources of these savings: First, the costs of feed-in tariffs decrease because the market value of the generated electricity increases when oversupply situations are smoothed out by storage – by €2.1 billion during the period under review. Second, end customers benefit from lower wholesale electricity prices: a relief effect of approximately €1.9 billion over the period. Third, the trade balance with other countries improves by around €1.6 billion because, with sufficient storage capacity, Germany would have to export less extreme surplus electricity at negative prices.

The effect on so-called negative electricity prices on the exchange is particularly striking; these are the hours when electricity supply so far exceeds demand that producers effectively have to pay to get rid of their electricity. In the baseline scenario without additional storage, 845 hours with negative prices were identified. With 20 gigawatts of storage capacity, this number would drop to 276 hours – a reduction of over 70 percent. At the same time, market-driven curtailment of renewables could be reduced by around 3.3 terawatt-hours, or about 55 percent. The researchers describe the 20-gigawatt mark with four hours of storage duration as the sweet spot and recommend an annual addition of around 8,000 megawatts of storage capacity, each with four hours of storage, for a practical continuation of the model.

Reality versus potential: The current state of storage expansion

The contrast between the potential calculated in the Fraunhofer study and the actual state of battery storage expansion in Germany is sobering. Germany currently has a large-scale storage capacity of around six gigawatts, with an average storage duration of one to two hours. This is far from the 20 gigawatts with four hours of capacity that the Fraunhofer analysis describes as the sweet spot. The total capacity of all stationary battery storage systems in Germany – including residential and commercial storage – amounted to approximately 27.23 gigawatt-hours at the end of March 2026, distributed across more than 2.4 million installations.

Growth is dynamic, however. In the first quarter of 2026, more than 2.2 gigawatt-hours of new battery storage capacity were commissioned in Germany – an increase of around 38 percent compared to the same period of the previous year. This growth was driven almost exclusively by large-scale storage systems, whose segment grew by around 120 percent year-on-year, thus reaching parity with the residential storage segment for the first time in terms of capacity growth. In March 2026 alone, 985.9 megawatt-hours of new capacity were commissioned – the highest monthly rate since records began.

Up to 5.7 gigawatts are projected for the end of 2026, with delays in grid connection considered a major obstacle. The grid application pipeline is enormous: applications for battery storage totaling more than 700,000 megawatts have been submitted. The permitting system represents the real bottleneck, not investor interest or the technology itself. At the same time, the Federal Ministry for Economic Affairs and Energy, with its planned Flexibility Acceleration Act, has primarily targeted accelerated permits for natural gas power plants, a move criticized in expert circles as a systematic misprioritization.

Innovative photovoltaic solution for cost reduction (up to 30%) and time savings (up to 40%)

Innovative photovoltaic solution for cost reduction and time savings - Image: Xpert.Digital

More information here:

Why flexibility is the true currency of the energy transition

The economics of electricity: systems thinking instead of component optimization

The Fraunhofer study draws attention to a structural imbalance in the energy policy debate that extends beyond technical details. Those who generate, store, transport, or consume electricity do so within a highly interconnected system where every decision creates externalities for all other participants. Expanding renewable energy sources without adequate storage capacity leads to the same systemic problems that could be avoided by reducing the expansion – except that the path of inflexibility is more costly for the economy as a whole.

Specifically, the study shows that if roughly 30 percent less photovoltaic and 20 percent less wind power capacity had been installed since the beginning of 2025, the burden of feed-in tariffs would indeed have decreased. However, wholesale electricity prices would have increased because more expensive electricity from fossil fuels would have been added more frequently. On balance, the actual expansion of renewables, considering all effects, was approximately €300 million more cost-effective for the economy – without a single storage system contributing to this result. With the storage sweet spot, this effect would be many times greater. Investments in flexibility are therefore not a cost driver of the energy transition, but rather a prerequisite for it and, at the same time, a cost-saving measure.

Beyond the lithium-ion battery: Why long-term storage is a chapter unto itself

The Fraunhofer study focuses on short-term storage systems with capacities of two to eight hours, i.e., battery systems that typically operate on a daily basis. This technology is commercially mature, and the cost curve for lithium iron phosphate systems has been declining sharply for years. However, what the study structurally leaves open is a fundamental challenge of the energy transition: the seasonal fluctuation of renewable electricity generation.

In Germany, wind and solar power provide significantly more energy in summer than in winter, and within each season there are periods of low wind and solar output lasting several days – the so-called "dark doldrums" – during which neither sun nor wind generates sufficient electricity. A lithium-ion battery can smooth out fluctuations for four hours, but not for four weeks. For storage on this scale, other technologies are needed: chemical energy carriers such as hydrogen, ammonia, or methanol; physical storage systems such as pumped-storage hydroelectric plants; or something that might seem surprising at first glance: iron.

A new Iron Age: KIT and energy storage with metal powder

In July 2026, researchers at the Karlsruhe Institute of Technology (KIT) published a study in the journal Chem Circularity that systematically investigated the potential of iron powder as a long-term energy storage medium for a climate-neutral European energy system. The basic idea is simple and physically elegant: iron powder can be burned, i.e., oxidized. This releases heat without producing carbon dioxide, because iron contains no carbon. What remains is iron oxide, ordinary rust. This can then be reduced back to metallic iron using green hydrogen, which is available for the next combustion. The cycle is completely closed, CO2-neutral, and, in principle, repeatable indefinitely.

The energy-economic potential of this principle is considerable, as the KIT team led by Julia Schuler from the Institute for Industrial Production and Management has quantified using the PERSEUS-PtX energy system model. Iron has a volumetric energy density approximately ten times higher than that of compressed hydrogen. It is abundantly available worldwide, non-toxic, and stable in solid form at room temperature – no high-pressure tank, no deep-freeze system, and no complex infrastructure are required. The material can be transported on existing shipping, rail, and road routes, making iron powder particularly attractive for importing renewable energy from coastal and desert regions.

The KIT study also realistically highlights the limitations: iron does not replace hydrogen in the energy system, but can complement it effectively in certain niche applications. Iron is particularly attractive as a long-term storage medium in countries or regions with limited hydropower potential or underground hydrogen storage facilities. In simulations of various scenarios for a climate-neutral European energy system, iron powder-fired power plants proved to be a component of the cost-minimal system across all scenarios – an encouraging sign from the researchers' perspective.

Old power plants, new function: The industrial policy dimension of iron storage

A particularly relevant aspect of iron technology is its compatibility with existing infrastructure. Coal-fired power plants that have been decommissioned or are slated for decommissioning as part of the energy transition could, in principle, be converted to run on iron powder. Turbines, generators, cooling systems, and grid connections would be largely reusable; only the combustion chamber and material feed would need to be adapted – making the conversion significantly more cost-effective than building a new plant.

This aspect has considerable regional economic importance for regions structurally characterized by coal mining and coal-based power generation. The Clean Circles research project, in which KIT, TU Darmstadt, Darmstadt University of Applied Sciences, DLR, and the University of Mainz participated, has demonstrated the technical feasibility at a demonstration power plant site. The parallel DLR project IronCircle is working on making the technology ready for implementation in larger plants. The current KIT study was funded by the Baden-Württemberg Energy Research Foundation, which underscores the regional industrial policy dimension.

System integration: How inverters, battery storage and long-term storage work together

The three topics – inverter safety, short-term storage, and long-term storage – are not isolated issues. They describe three layers of the same system: the transformation of the European energy supply from a centralized, fossil fuel-based architecture to a decentralized, volatile, and digitally networked infrastructure.

Inverters are the digital interfaces of this new energy infrastructure. They translate physical energy flows into marketable transactions and communicate with grid operators, energy management systems, and trading platforms. Whoever controls the inverters, to a certain extent, controls the pulse of the grid. Short-term battery storage acts as an economic buffer, balancing volatile generation and demand over time, thereby mitigating price spikes, reducing grid costs, and conserving subsidies. Finally, long-term storage solutions like hydrogen or iron powder provide seasonal reserves, guaranteeing security of supply even when short-term storage is depleted and the wind doesn't blow for days.

A climate-neutral energy system requires all three levels. And at all three levels, structural decisions are currently pending that are not primarily technical, but rather economic policy-related: Which manufacturers should be allowed to participate in critical infrastructure? Which market designs create sufficient incentives for storage investments? What research funding will secure the technological sovereignty of tomorrow?

Geopolitical Economics of Electricity: What's at Stake

It would be analytically insufficient to treat the inverter debate solely as a technical safety issue. It is embedded in a broader shift in geopolitical economics, which has gained considerable importance in European energy policy since the Russian attack on Ukraine. Europe's dependence on Russian gas has taught it a bitter lesson about the costs of excessive specialization in cheap imports when the supplier ceases to be a reliable trading partner. The structural parallel to dependence on Chinese inverter technology is obvious.

This is not about fundamentally questioning bilateral trade with China or advocating technological nationalism. By using the term "derisking" instead of "decoupling," the EU Commission signals its intention to pursue a differentiated policy: minimizing risks to critical infrastructure without abandoning trade diversification. Inverters that communicate directly with the grid and can theoretically be remotely shut down fall under any reasonable definition of critical infrastructure. Modules, cables, or mounting rails, on the other hand, do not. The suspension of subsidies will put diplomatic pressure on Beijing, but at the same time, it should give European manufacturers like SMA and Fronius a structural competitive advantage, enabling new investments in production capacity.

Regulatory gaps and open issues

Despite the progress described, significant regulatory gaps remain. The EU Commission's announced ban on subsidies for high-risk inverters has not yet been accompanied by an officially published legal act – an unusually informal approach by EU standards, creating legal uncertainty for investors and project developers. An official press release or legislative text was still lacking months after the measure came into force.

The regulatory situation regarding battery storage is no less complex. Grid connections for storage projects are considered the most significant bottleneck in their expansion, and fast, standardized procedures are lacking. The Federal Ministry for Economic Affairs and Energy's planned Flexibility Acceleration Act has so far omitted this area, focusing instead on simplifying permitting processes for new gas-fired power plants. From the perspective of the storage industry, this represents a systematic misallocation of regulatory resources: gas-fired power plants can provide systemic flexibility in extreme cases, but in the long term, they pave the way to further import dependency.

For iron technology, despite promising research results, the path from demonstration to commercial scaling is still considerable. The Clean Circles project formally ended in March 2025, and the newly published KIT study is an analytical follow-up, showing where the technology could be meaningfully integrated into the overall system. Concrete investment frameworks, industrial-scale pilot projects, and regulatory definitions regarding how iron powder is treated under energy law are still pending.

Consequences of hesitation: The cost of waiting

The three thematic strands examined – inverter sovereignty, battery storage savings potential and iron storage research – converge on a common message: Europe's energy transition has reached a point where the costs of hesitation outweigh the costs of action.

The suspension of subsidies for high-risk Chinese inverters comes late, but it is long overdue. ESMC's capacity analysis shows that supplying energy from alternative sources is feasible with acceptable additional costs of two to four percent. The Fraunhofer IEE estimates the economic damage caused by insufficient storage investments at almost four billion euros per year – money that the federal budget, consumers, and the renewable energy sector collectively lose. And KIT demonstrates that research into tomorrow – into seasonal long-term storage using iron powder – should not be treated as a pipe dream, but rather as a viable technology option that already appears cost-efficient in simulation models of climate-neutral energy systems.

What's lacking isn't better knowledge. What's lacking is the political resolve to swiftly translate available findings into actionable decisions: clearer legislation instead of informal funding freezes, rapid grid connections for storage facilities instead of bureaucratic waiting lists, and sufficient research funding for long-term storage technologies that are not yet commercially viable but are already systemically important. The energy transition is technically feasible and economically sound – especially if we consistently rely on European components. The question is no longer whether, but whether action will be taken quickly enough.

🎯🎯🎯 Data-driven B2B industry hub as a quasi-in-house solution

The quasi-in-house solution: How Xpert.Digital closes operational gaps in B2B marketing and sales – Smart Content-Driven Business - Image: Xpert.Digital

Xpert.Digital is a data-driven B2B industry hub led by Konrad Wolfenstein . The company acts as an external, quasi-in-house solution for industrial partners, closing operational gaps in marketing, content, and sales – without requiring additional resources on the client side.

More information here:

Your global marketing and business development partner

☑️ Our business language is English or German

☑️ NEW: Correspondence in your native language!

Konrad Wolfenstein

I and my team are happy to be available to you as your personal advisor.

You can contact me by filling out the contact form here wolfenstein@xpert.digital:or simply call me at +49 7348 4088 965. My email address is

I'm looking forward to our joint project.