Intermodal transport units and the vertical terminal: When space is at a premium, logistics must think vertically – Image: Xpert.Digital

When space runs out: Why Germany's logistics sector now needs to build upwards

Truck crisis and lack of space: How silent high-bay warehouses can solve the logistics chaos

When space runs out: Why Germany's logistics sector now needs to build upwards

German freight transport is caught in a structural dilemma: While the call for a shift to climate-friendly rail is growing louder, the need for the necessary infrastructure is simultaneously increasing. Where should new transshipment hubs be built when large areas are becoming ever scarcer, politically contested, and expensive? Added to this is a chronic shortage of personnel, which is increasingly slowing down traditional, manual logistics processes. The solution to these complex challenges lies in vertical integration. Fully automated high-bay warehouses for intermodal transport units such as swap bodies promise a genuine paradigm shift in the industry. On a minimal footprint, they silently, emission-free, and completely without human intervention elevate combined transport to a new level of efficiency. Read on to discover why the vertical terminal is far more than just a fascinating technological vision – and why it represents the most sound answer to land consumption, emissions pressure, and scarce resources.

Stacking containers instead of sacrificing space: This is what the logistics terminal of tomorrow will look like

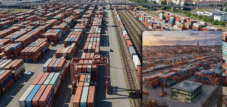

The image shows a fully automated transshipment facility where a storage and retrieval machine glides silently between rows of steel racks, precisely grips swap bodies, and transfers them—entirely without human intervention—from the freight train to the waiting truck. What seemed like a vision from an industrial film just a few years ago is now a technological reality. The high-bay warehouse, as the centerpiece of intermodal freight transport, promises a solution to several structural bottlenecks in German logistics: lack of space, labor shortage, emissions reduction, and increasing terminal pressure. However, economic analysis reveals that implementation requires bold investment thinking, political will, and a sober assessment of the framework conditions.

Structural crisis in German freight transport

Freight transport in Germany finds itself in a paradoxical situation. While overall transport volumes fell by 1.6 percent in 2024, road freight transport using German trucks even saw a decline in performance of around 1.9 percent. At the same time, the demand for logistics space continues to grow, rents are rising, and supply remains tight. This gap between declining transport volumes and increasing infrastructural pressure is not a cyclical phenomenon – it reflects structural shortcomings that have accumulated over decades.

The causes of this stagnation lie on several levels. High energy costs, increased interest rates, and growing international competition are weighing on the German export sector. Gross domestic product shrank by 0.2 percent in 2024, while industrial production even plummeted by 4.6 percent. Added to this are geopolitical uncertainties that are putting global supply chains under pressure. A further decline in transport volume of 0.4 percent is expected for 2025 – not even taking into account the effects of the current tariff escalation between the US and its trading partners. The pre-crisis level of 2019 is not expected to be reached again until 2028.

In this challenging environment, combined transport is a striking exception. While road transport is suffering and inland waterway shipping is shrinking in the long term, rail-based combined transport recorded a performance increase of 6.4 percent in 2024. In 2023, combined transport in Germany achieved a transport performance of approximately 57 billion tonne-kilometers. Rail freight thus accounts for 41.7 percent of this performance – combined transport is not a niche product, but rather the most important segment of the entire rail freight sector. Forecasts up to 2026 predict a volume increase of 6.1 percent and a performance increase of 7.0 percent for rail-based combined transport.

What an intermodal transport unit can really do

The term intermodal transport unit refers to standardized load carriers that can be exchanged between different modes of transport – road, rail, waterway – without repacking the goods. In continental Europe, the swap body is the dominant intermodal transport unit. Unlike the ISO container, it is not designed for maritime transport but is optimized for seamless interchangeability between trucks and freight wagons. Its characteristic feature is its fold-out support legs, which allow the container to be set down independently on a solid surface: The truck simply drives underneath or out of it without the need for complex crane movements.

The standardization of these containers follows a clear principle of increasing efficiency. Standardized dimensions and handling elements enable economical, fast, and cost-effective transshipment between modes of transport. In Europe, swap bodies with a width of 2,500 to 2,550 millimeters and a standard length of 13.60 meters are the most common – the 13.60-meter unit that shares the locking dimension of the 40-foot ISO container, thus ensuring direct compatibility with international container technology. It is estimated that around 300,000 of these units are in circulation in Europe.

The strength of the swap body lies in decoupling transport from the loading and unloading process. While one container is at the customer's site being unloaded, the truck driver has already picked up the next one and moved on. This principle frees up valuable driver time and reduces empty runs. It forms the logical foundation for combined transport: the loading unit remains the same, the means of transport change. This is precisely where the automated high-bay warehouse comes in – as a hub that not only manages this change but also executes it entirely automatically.

The vertical terminal: Technical architecture of a paradigm shift

If more than 150 containers or swap bodies are handled daily at a rail-connected location, the use of an automated high-bay warehouse system is recommended. This threshold marks the point at which manual handling and conventional gantry crane concepts become structurally inefficient. The solution developed by LTW for standardized containers forms the technical core of such a vertically automated terminal.

The system, in its basic configuration, consists of a loading track integrated into the warehouse building, two parallel rows of racking with storage spaces for all common containers and swap bodies, and at least two fully automated storage and retrieval machines (SRMs) that handle the transfer between the train and the racking. The unique feature of the train loading system is the EcoSlider technology: horizontal transfer devices mounted on the SRMs themselves enable the direct, horizontal movement of the transport units onto and off the freight cars – without complex vertical movements. Transfer ports in the building wall allow the containers to reach gantry cranes on the outside, which then load and unload the trucks.

The result is a system that operates simultaneously and fully automatically in its core function: While swap bodies are being loaded and unloaded on the train side, gantry cranes on the truck side receive or transfer other units. This parallel operation is the decisive operational advantage over sequential handling systems. Redundancy is structurally integrated: Since storage and retrieval machines and gantry cranes are present in at least duplicate form, operational capability remains ensured even during maintenance work or unplanned outages.

Space utilization reaches levels that are simply unattainable with conventional open-plan terminals. Within a width of just twelve meters, up to 100 of the 13.60-meter swap bodies can be stored per 100 meters of length. This allows for a redundant system for up to 500 loaded semi-trailers to be created on a footprint of approximately 9,000 square meters. By comparison, a conventional open-plan terminal of the same capacity would require many times this area – and still wouldn't achieve the level of automation offered by this vertical solution.

LTW Intralogistics from Austria is among the leading specialists for this class of fully automated intralogistics systems. The company supplies turnkey systems including stacker cranes, conveyor technology, and control software. The first LTW stacker cranes for containers were manufactured for armasuisse, the Swiss procurement agency for defense equipment – a 20-meter-high system with a payload of 18 tons. This demonstrates the technical maturity of a solution that is still considered futuristic in public discourse but has long been proven in practice.

Area productivity as an economic argument

Germany is facing a profound land crisis. Every day, around 52 to 55 hectares of land are converted into residential and transport areas – a rate that far exceeds the federal government's political targets. The sustainability strategy aims to limit land consumption to less than 30 hectares per day by 2030, and to achieve net land consumption of zero by 2050. At the same time, the greenfield reserves available for logistics in densely populated economic areas are shrinking rapidly. Municipalities bound by land consumption targets are increasingly hesitant to designate new industrial parks – especially for land-intensive logistics operations.

Logistics real estate is caught in a structural contradiction: On the one hand, demand continues to rise unabated – driven by e-commerce, just-in-time supply chains, and the restructuring of industrial production networks. On the other hand, the supply of available space is shrinking, rents are climbing, and permitting times for new facilities in Germany are significantly longer compared to other countries. While the volume of new logistics space could increase to over 4.5 million square meters per year by 2028, this is contingent on the necessary land being approved by local authorities.

In this context, the automated high-bay warehouse offers a systemically compelling solution. Its small footprint makes it possible to construct it at locations where there simply wouldn't be room for conventional terminal designs. The topographical flexibility is particularly relevant: the routes for rail and trucks don't need to be at the same level, and construction is explicitly possible even on sites with significant differences in elevation – for example, over tracks running in a cutting. This feature opens up locations in the heart of urban areas that would remain permanently inaccessible to conventional terminal projects.

The urban application as a courier, express, and parcel (CEP) city hub underscores these potentials. Since all transshipment processes take place within the building and no noise or light emissions escape to the outside, such hubs can be operated in the immediate vicinity of office or residential buildings. The loading and unloading ramps for the swap bodies are located on levels three to eight, with the handover to the trucks taking place on the lowest level. Such a system solves the previously seemingly irreconcilable requirement: logistics in the city without burdening the city.

LTW Intralogistics Solutions

LTW Intralogistics – Engineers of Flow - Image: LTW Intralogistics GmbH

LTW offers its customers not individual components, but integrated complete solutions. Consulting, planning, mechanical and electrotechnical components, control and automation technology, as well as software and service – everything is networked and precisely coordinated.

In-house production of key components is particularly advantageous. This allows for optimal control of quality, supply chains, and interfaces.

LTW stands for reliability, transparency, and collaborative partnership. Loyalty and honesty are firmly anchored in the company's philosophy – a handshake still means something here.

Related to this:

Automated intermodal terminals: How high-bay warehouses are revolutionizing climate-friendly intermodal transport

Economic calculations and funding landscape

The investment costs for fully automated intermodal terminal systems are substantial. Compared to conventional open-plan terminals, the capital expenditure requirements are higher – a factor that, considered in isolation, argues against automation. However, a complete economic evaluation requires the inclusion of several sets of factors.

On the cost side, the high initial investments are offset by significant operating cost advantages. Personnel represents a major cost factor in conventional terminal operations – and is simultaneously the greatest planning uncertainty, as qualified specialists for heavy-duty crane technology and terminal logistics are increasingly difficult to find on the job market. In contrast, a fully automated system with LTW stacker cranes is available around the clock, operates with consistent precision, and scales without the need to build up personnel capacity. The integrated self-service transfer zones are available 24/7, enabling trucks to be processed even at night and on weekends – a significant competitive advantage over operations requiring personnel.

Federal funding for combined transport transshipment facilities addresses this need. The Federal Ministry for Digital Affairs and Transport supports the construction and expansion of combined transport transshipment facilities with grants of up to 80 percent of the eligible investment costs. These eligible investment costs also include a planning cost allowance of 15 to 20 percent. The Federal Railway Authority is the approving authority for rail-road facilities. A prerequisite is a CO₂ reduction commitment: For every million euros in funding, at least 54,000 tons of CO₂ must be saved. Given the drastic differences in emissions between road and rail, this requirement is easily achievable for well-designed combined transport facilities.

Land value is another factor often underestimated in investment calculations. In key logistics locations, land costs and prices have risen sharply in recent years. A high-bay warehouse solution, which provides the same handling capacity as a conventional open-field facility on a fraction of the area, pays for itself simply through the saved land area – especially since it minimizes soil sealing, improving permitting prospects. This space efficiency is a crucial locational advantage in an environment where new logistics space is often politically contested.

Climate economics: The bill that the road is losing

Anyone transporting goods in Germany shares responsibility for one of the largest sources of emissions in the economy. In 2023, trucks emitted an average of around 119 grams of greenhouse gases per ton-kilometer. Deutsche Bahn, on the other hand, projects a figure of around 20 grams of CO₂ equivalent per ton-kilometer for its freight trains by April 2025. This represents an emissions advantage for rail of almost six times that of other modes of transport – and even more pronounced in a European comparison, where the difference is estimated at a factor of seven.

In the EU, freight transport accounts for over 30 percent of all transport-related CO₂ emissions. At the same time, more than 50 percent of goods in Europe are transported by road, and 99 percent of heavy goods vehicles on European roads are equipped with combustion engines. This situation is ecologically unsustainable – and increasingly subject to legal regulation. As part of the Green Deal, the European Commission has presented concrete measures to make freight transport more environmentally friendly and to achieve a 90 percent reduction in transport-related emissions by 2050.

A single 700-meter-long freight train can replace up to 52 trucks. Combined transport allows for a total weight of 44 tons, and the safety statistics for rail transport significantly surpass those of road transport. The automated high-bay warehouse terminal amplifies this advantage: it accelerates transshipment, increases the punctuality of train deliveries, reduces terminal-related buffer times, and thus makes combined transport operationally more competitive than direct delivery by truck. Closing precisely this gap between the climate-friendly potential and operational competitiveness of combined transport is the strategic promise of automation.

This is not an academic debate. Shippers who commit to reducing their Scope 3 emissions by 2030 – as required by the Supply Chain Due Diligence Act, the CSRD, and increasingly by customers – will have to rely more heavily on intermodal transport chains. Terminal operators who cannot offer automated, reliable, and scalable handling capacities will be forced out of these supply chains.

Proven technology meets new fields of application

The frequently expressed reservation that fully automated high-bay warehouses for intermodal transport units are still unproven technology is not empirically supported. High-bay warehouses for intermodal loading units are already in successful operation. Two reference systems demonstrate the technical maturity from very different application contexts.

The Swiss Army's material depot relies on fully automated storage and retrieval systems from LTW for handling containers under real-world operating conditions. Operations are reliable, and the redundancy concepts have proven their worth. Even more impressive is the Jungfraujoch station: located at 3,454 meters, it is the highest railway station in Europe and uses automated train loading based on the same principles. If horizontal handling technology functions reliably under these extreme climatic and logistical conditions, then the logistics realities of Central Europe truly pose no engineering challenge.

Fraunhofer SCS has evaluated various digitalization approaches in a feasibility study for the digital intermodal terminal of the future. The conclusion: Digitalization and automation of terminal processes significantly increase efficiency in the short to medium term. Greater process transparency and improved resource planning are not just convenience benefits, but measurable competitive advantages. Fully automated operation is the logical culmination of this development – not a quantum leap into the unknown, but rather the scaling of proven intralogistics principles to the requirements of intermodal freight transport.

Recent developments show that market players are also setting the course. For example, the company InterCal is focusing on fully intermodal, CO₂-free transport chains using specialized containers: Goods are transported by electric truck to the railway, then by rail to their final destination. Up to three trains, each carrying 32 containers, are planned every two weeks. This development is representative of a growing number of shippers who no longer see intermodal transport units as a niche solution, but rather as a standard tool in a sustainable supply chain strategy.

Structural barriers and political framework conditions

Despite compelling arguments, the adoption of fully automated intermodal terminals in Germany lags behind its technological potential. The reasons are structural and affect both infrastructure policy and regulatory practice.

The first obstacle is the infrastructure itself. Combined transport is under stress: infrastructure, capacity planning, and political reliability are the key bottlenecks. A high-bay warehouse terminal cannot be built without available sidings and suitable loading infrastructure. Many potential sites do have historical rail connections, but these have been unused for years and are therefore in a state that requires significant upfront investment. Reactivating disused industrial sidings is an often underestimated key to developing new terminal sites.

The second obstacle is the length of planning and approval processes. Compared internationally, these times are significantly longer in Germany. For investment decisions that have an impact for decades and tie up substantial amounts of capital, planning certainty is a fundamental requirement. Accordingly, transport associations have pointed out that important transport sectors remain without this planning certainty. Investors – whether private logistics providers or railway ancillary companies – prefer to wait for clear signals rather than invest in a regulatory environment of uncertainty.

The third obstacle is the funding landscape itself, which, despite its generosity – up to 80 percent subsidies – presents bureaucratic hurdles that pose significant challenges for small and medium-sized terminal operators. The German Association for Combined Transport and the Federal Railway Authority are available as funding institutions, but the process from application to approval is lengthy and resource-intensive. This presents an operational reform task that requires not additional budget funds, but simply a streamlining of the process.

Strategic perspective: The terminal as a system integrator

The high-bay warehouse terminal of the future is more than just a highly automated warehouse. It is a system integrator that not only makes the logistics chain more efficient but fundamentally reorganizes it. Its function goes beyond simply handling swap bodies and containers: it enables a completely new location logic for terminals, new capacity planning for rail operators, and new cost calculations for shippers.

The fact that the system can also be built on terrain with significant differences in elevation and does not require the rail and truck routes to coincide opens up locations that would be off-limits for conventional terminals: railway cuttings in metropolitan areas, abandoned industrial sites with unfavorable topography, and mixed-use suburban locations. Combined with the possibility of completely enclosing the operation, thus eliminating noise and light emissions, a terminal type emerges that integrates into the urban fabric instead of displacing it.

For decision-makers in logistics, transport planning, and urban development, this translates into a clear strategic recommendation: The vertical automation of intermodal terminals is not a luxury for large, well-capitalized operators, but rather an economically sound response to the structural bottlenecks of German freight transport. Space scarcity, labor shortages, emissions pressures, and rising infrastructure costs all point in the same direction. High-bay warehouses are not the only answer to these challenges – but they are the only answer that addresses them all simultaneously. In an industry that can hardly afford to wait and see, this is a compelling argument.

Consulting - Planning - Implementation

Konrad Wolfenstein

I would be happy to serve as your personal advisor.

You can contact me at wolfenstein∂xpert.digital or

Just call me on +49 7348 4088 965 .

Your container high-bay warehouse and container terminal experts

Container high-bay warehouses and container terminals: The logistical interplay – expert advice and solutions - Creative image: Xpert.Digital

This innovative technology promises to fundamentally change container logistics. Instead of stacking containers horizontally as before, they will be stored vertically in multi-story steel racking structures. This not only allows for a drastic increase in storage capacity within the same area, but also revolutionizes all processes at the container terminal.

More information here: