Advice: Independent financial planning – looking for financial advice or investment advice in Biberach, Memmingen, Kempten or Krumbach?

Language selection 📢

Published on: October 24, 2021 / update from: February 1, 2024 - Author: Konrad Wolfenstein

Independent financial planning – Image: Xpert.Digital / Rido|Shutterstock.com

Independent financial planning

In a survey, 68% of those surveyed said that they knew the Sparkasse as a wealth creation provider. However, only 33% see the Sparkasse as a suitable partner on this topic. For another 29%, none of the providers are an option. Only 22% rate their level of information on financial matters as good. Do you actually know how high the financial assets of private households in Germany or how high the advertising expenditure of the German Savings Banks and Giro Association is? How many banks are now charging negative interest rates?

You can find an independent overview here:

Free PDF download of 'Saving behavior of private households'

Important note: The PDF is password protected.

Please get in contact with me. Of course, the PDF is free of charge. Important note: The PDF is password protected. Please contact me. Of course the PDF is free of charge.

German version – To see the PDF, please click on the image below.

German Version – To view the PDF, please click on the image below.

Saving behavior of private households – PDF download

👨🏻 👩🏻 👴🏻 👵🏻 For private households

Xpert.Digital helps you choose your independent financial service provider. With our AI-supported digital know-how, we provide you with current data and figures.

Financial planning is worthwhile for everyone, regardless of income and assets. It doesn't always have to be a complete and elaborate financial plan. Depending on the situation, special topic plans such as: B. retirement provision.

📣 For entrepreneurs such as founders and start-ups

The financial plan is the basis for the business plan. It should be updated regularly. Clearly defined corporate goals help with this.

With over 1,000 specialist articles, we cannot present all topics here. Therefore, you will find a small excerpt from our work here and we would be pleased if we have piqued your interest in getting to know us better:

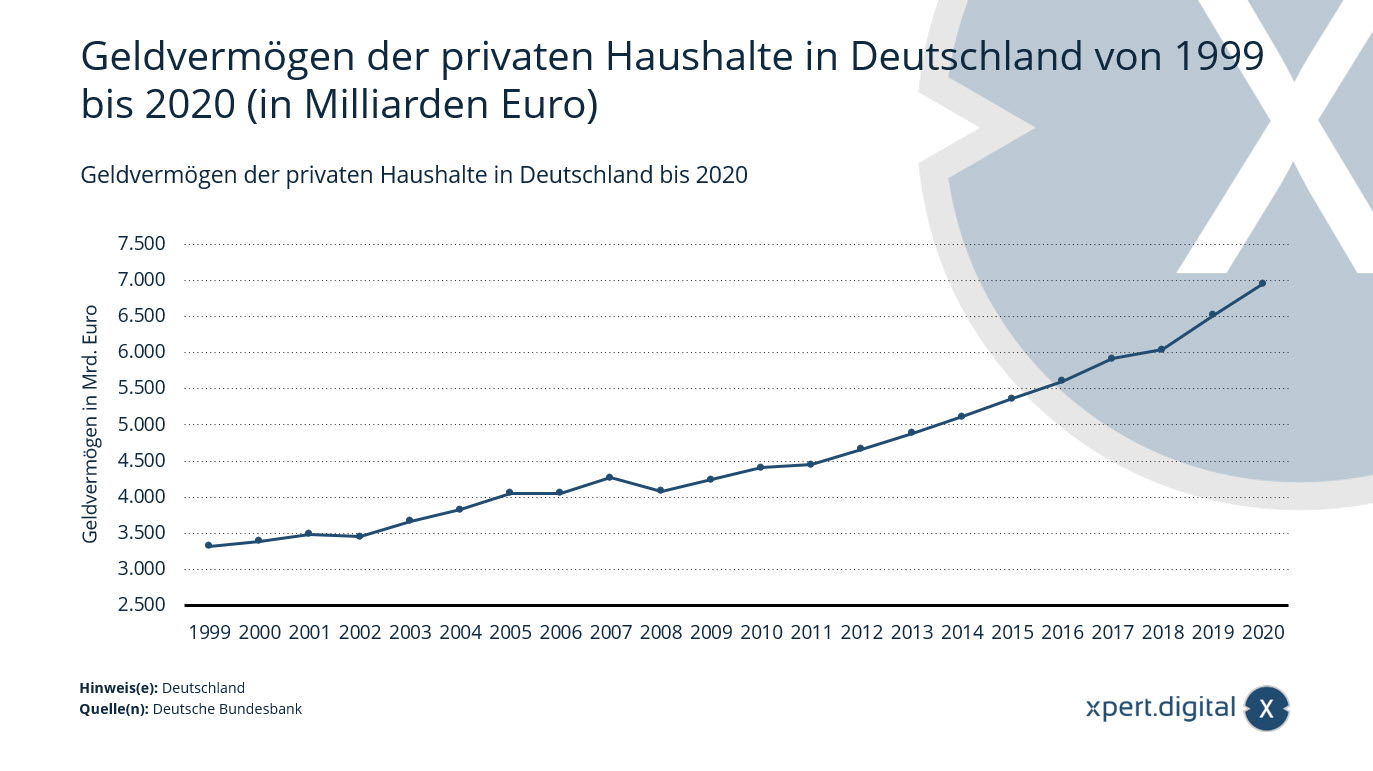

Financial assets of private households in Germany

Financial assets of private households in Germany – Image: Xpert.Digital

At the end of 2020, the financial assets of private households* in Germany reached a new record level: German citizens have now saved almost 7 trillion euros. Compared to the end of the previous year, financial assets increased by around 6.7 percent. This means that Germans' wealth has increased for the twelfth time in a row.

How are financial assets composed?

The financial assets of private households are divided into cash held, bank deposits and securities (stocks, fixed-interest securities and investment fund shares) as well as claims against insurance companies and pension institutions. Private households hold more than a third of their financial assets in cash and sight deposits.

Total assets of private households

Financial and material assets combined form the total assets of private households. The largest item of total assets is real estate assets, including land ownership. At the end of 2019, the assets of private households in Germany invested in residential buildings amounted to around 4.9 trillion euros. Total private real assets amounted to around 8.98 trillion euros.

Financial assets of private households in Germany from 1999 to 2020 (in billion euros)

- 2020 – 6,950 billion euros

- 2019 – 6511.5 billion euros

- 2018 – 6,037.7 billion euros

- 2017 – 5,913.4 billion euros

- 2016 – 5,604 billion euros

- 2015 – 5,361.8 billion euros

- 2014 – 5,111.7 billion euros

- 2013 – 4,879.6 billion euros

- 2012 – 4,659.3 billion euros

- 2011 – 4,447.8 billion euros

- 2010 – 4,407.7 billion euros

- 2009 – 4,38.7 billion euros

- 2008 – 4,077.8 billion euros

- 2007 – 4,268.7 billion euros

- 2006 – 4,050.2 billion euros

- 2005 – 4,052.7 billion euros

- 2004 – 3,822.3 billion euros

- 2003 – 3,662.2 billion euros

- 2002 – 3,452.4 billion euros

- 2001 – 3,489 billion euros

- 2000 – 3,392 billion euros

- 1999 – 3,315.8 billion euros

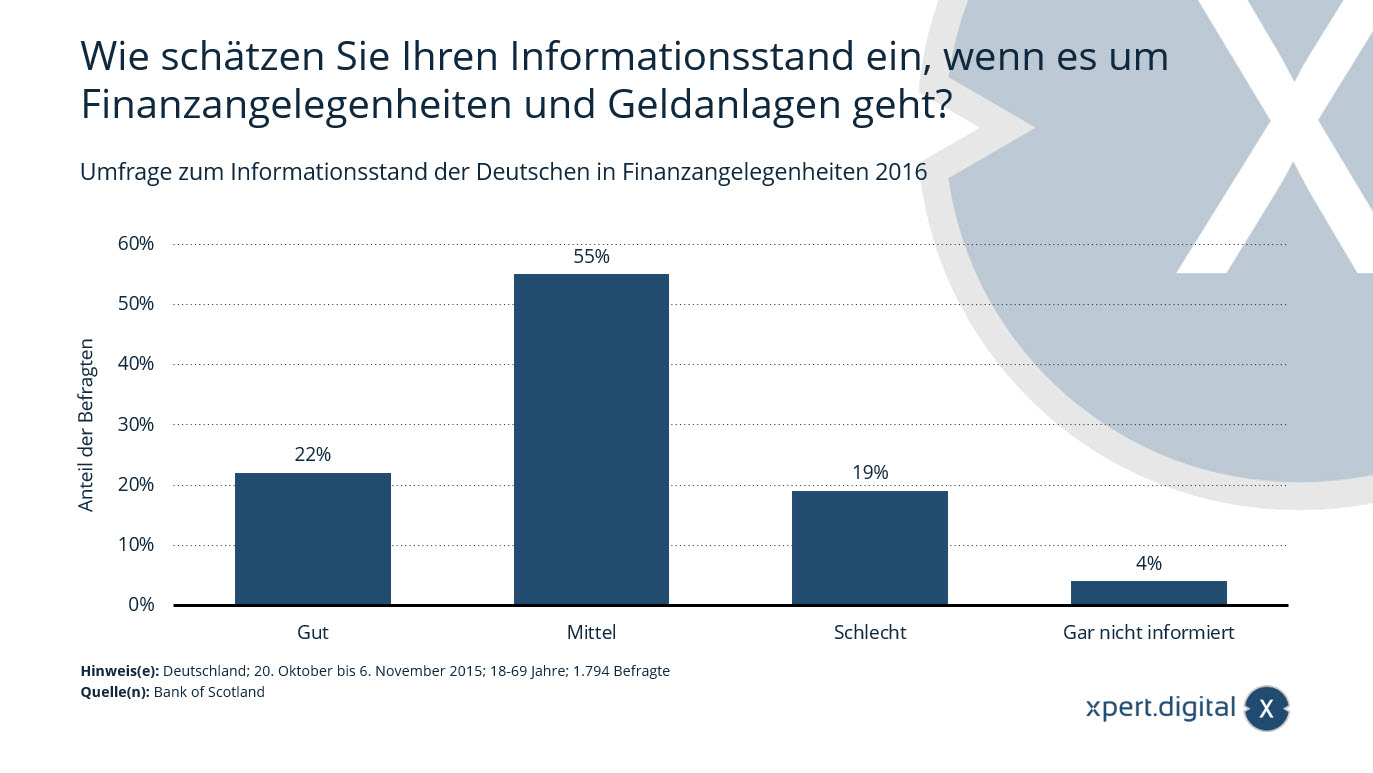

Survey on the level of information Germans have on financial matters

Survey on the level of information Germans have on financial matters – Image: Xpert.Digital

This statistic reflects the results of a survey on the level of information Germans have on financial matters. At the time of the survey, around 22 percent of those surveyed said they were well versed in the subject of finance and investments.

How do you assess your level of information when it comes to financial matters and investments?

- Good – 22%

- Medium – 55%

- Poor – 19%

- Not informed at all – 4%

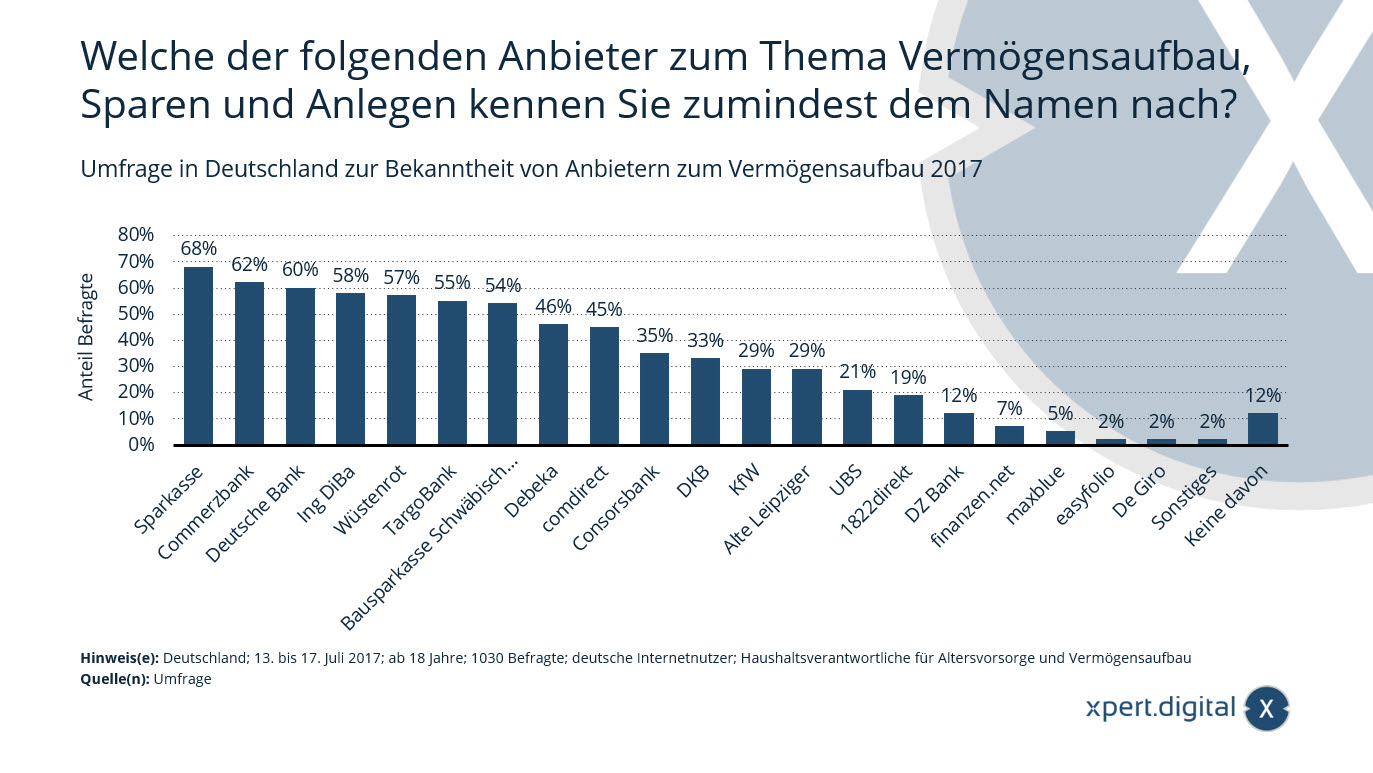

Survey in Germany on the awareness of wealth creation providers

Survey in Germany on the awareness of wealth creation providers – Image: Xpert.Digital

This data shows the results of a survey in Germany on the awareness of providers on the subject of wealth creation, saving and investing. In 2017, around 68 percent of those surveyed said they knew the savings bank at least by name.

Which of the following providers on wealth creation, saving and investing do you know at least by name?

- Sparkasse – 68%

- Commerzbank – 62%

- Deutsche Bank – 60%

- Ing DiBa – 58%

- Desert Red – 57%

- TargoBank – 55%

- Schwäbisch Hall building society – 54%

- Debeka – 46%

- comdirect – 45%

- Consorsbank – 35%

- DKB – 33%

- KfW – 29%

- Old Leipzig residents – 29%

- UBS – 21%

- 1822direct – 19%

- DZ Bank – 12%

- finanzen.net – 7%

- maxblue – 5%

- easyfolio – 2%

- De Giro – 2%

- Other – 2%

- None of these – 12%

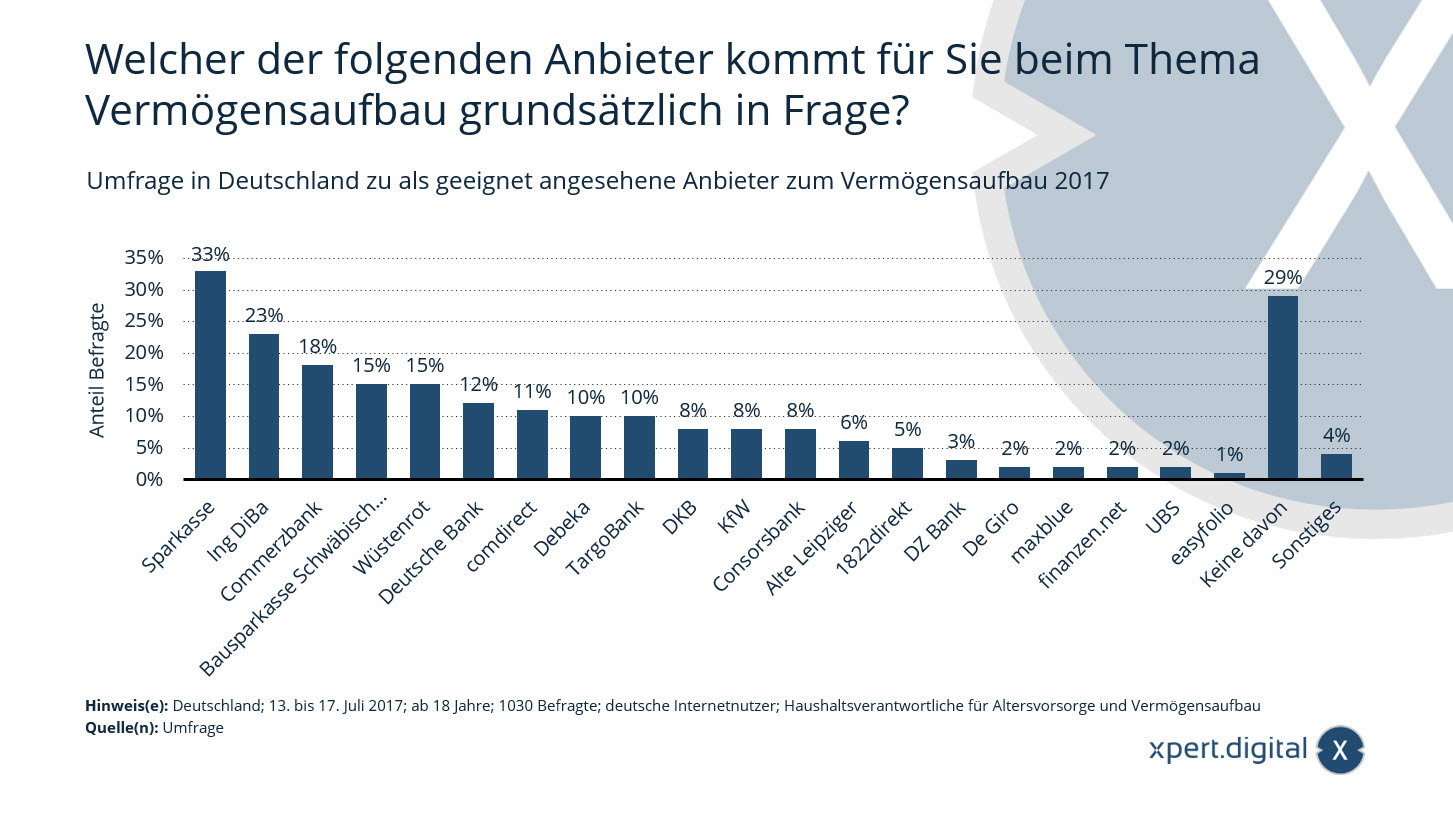

Survey in Germany on providers considered suitable for building wealth

Survey in Germany on providers considered suitable for wealth creation – Image: Xpert.Digital

This data shows the results of a survey in Germany about which providers are suitable for wealth creation. In 2017, around 33 percent of those surveyed said that the Sparkasse would be an option for this.

German internet users were surveyed. Household responsible for retirement provision and wealth creation. Several answers were possible.

Which of the following providers is generally suitable for you when it comes to building wealth?

- Sparkasse – 33%

- Ing DiBa – 23%

- Commerzbank – 18%

- Schwäbisch Hall building society – 15%

- Desert Red – 15%

- Deutsche Bank – 12%

- comdirect – 11%

- Debeka – 10%

- TargoBank – 10%

- DKB – 8%

- KfW – 8%

- Consorsbank – 8%

- Old Leipzig residents – 6%

- 1822direct – 5%

- DZ Bank – 3%

- De Giro – 2%

- maxblue – 2%

- finanzen.net – 2%

- UBS – 2%

- easyfolio – 1%

- None of these – 29%

- Other – 4%

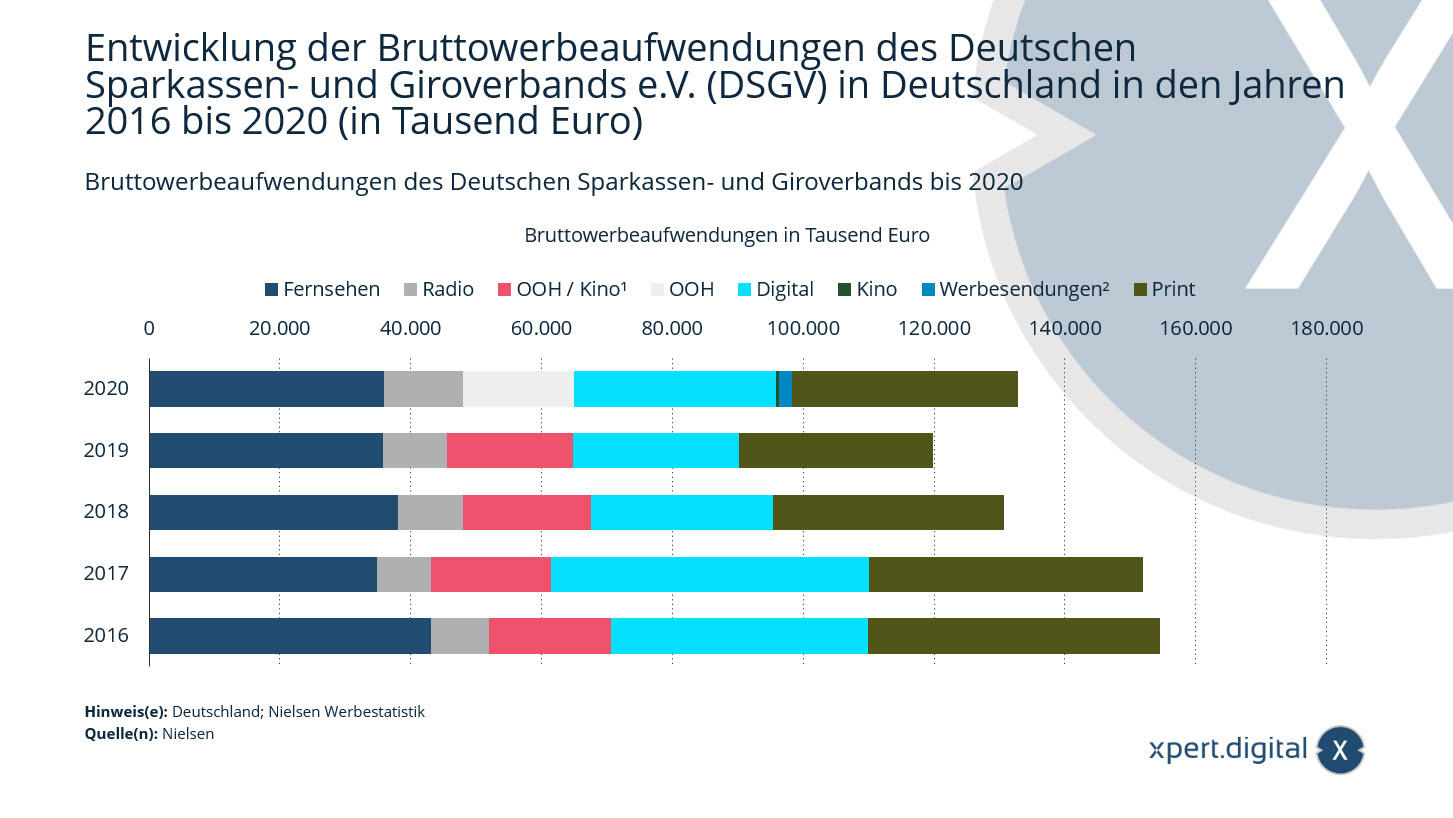

Gross advertising expenses of the German Savings Banks and Giro Association

Gross advertising expenses of the German Savings Banks and Giro Association – Image: Xpert.Digital

According to Nielsen Media Research, the German Savings Banks and Giro Association (DSGV) invested around 132.8 million euros in advertising in Germany in 2020.

¹ OOH / cinema were reported together until 2019.

² Advertising mailings have been reported since 2020. The values of previous years are only comparable to a limited extent.

OOH: Out-of-Home / outdoor advertising, e.g. B. large-format posters or whole posters.

Development of gross advertising expenses of the German Savings Banks and Giro Association (DSGV) in Germany from 2016 to 2020 (in thousands of euros)

Digital

- 2016 – 39,394 thousand euros

- 2017 – 48,676 thousand euros

- 2018 – 27,880 thousand euros

- 2019 – 25,246 thousand euros

- 2020 – 30,851 thousand euros

TV

- 2016 – 43,196 thousand euros

- 2017 – 34,999 thousand euros

- 2018 – 38,099 thousand euros

- 2019 – 35,863 thousand euros

- 2020 – 36,069 thousand euros

radio

- 2016 – 8,785 thousand euros

- 2017 – 8,144 thousand euros

- 2018 – 9,912 thousand euros

- 2019 – 9,774 thousand euros

- 2020 – 11,945 thousand euros

- 2016 – 44,429 thousand euros

- 2017 – 41,697 thousand euros

- 2018 – 35,116 thousand euros

- 2019 – 29,558 thousand euros

- 2020 – 34,421 thousand euros

OOH / Cinema¹

- 2016 – 18,665 thousand euros

- 2017 – 18,367 thousand euros

- 2018 – 19,614 thousand euros

- 2019 – 19,313 thousand euros

OOH¹

- 2020 – 17,024 thousand euros

Cinema¹

- 2020 – 483 thousand euros

Commercials²

- 2020 – 2,006 thousand euros

Negative interest rates at almost 400 banks

Negative interest rate – Image: M. Schuppich|Shutterstock.com

Update - October 24, 2021: At the end of the third quarter, a total of 392 credit institutions are charging negative interest rates from their private customers. Of these, over 200 banks and savings banks have introduced negative interest rates in the current year. In addition, more and more financial institutions are tightening their existing negative interest rate regulations by reducing allowances or pushing interest rates even further into the red. This is shown by a Verivox evaluation of around 1,300 banks.

Penalty interest for larger amounts of money in checking accounts is becoming a practice at more and more banks in Germany. According to a study by the comparison portal Verivox, the number of financial institutions that charge negative interest rates is around 349 - an increase of 171 compared to the previous year. The analysis of the price notices published on the Internet by around 1,300 banks and savings banks reveals that the exemption amount at around 102 banks is less than 50,000 euros - a few even have a limit of just 25,000 euros. Also annoying for bank customers: in around 30 cases, fees are charged on the usually free daily money account, as the Statista graphic shows.

The situation will probably continue to worsen in the future. The trigger for this development is the monetary policy of the European Central Bank (ECB). Since commercial banks currently have to pay 0.5 percent interest on excess funds deposited with the ECB, the resulting costs are passed on to bank customers in the broadest sense.

More about it here:

How many billionaires are really “self-made”?

Self-made billionaire George Soros – Image: Alexandros Michailidis|Shutterstock.com

The Forbes 400 is a ranking of the wealthiest Americans. In order to get a place on the list, you now have to have a net worth of around 2.9 billion US dollars - last year you had to have 2.1 billion. This year's ranking contains 44 new names and said goodbye to some well-known ones, such as Donald Trump. The collective wealth of these 400 people increased by a whopping 40 percent last year. What hasn't increased, however, is philanthropy. The number of list members who donate more than 20 percent of their wealth to charity has fallen from ten to eight - that's two percent of all 400 billionaires.

Among the world’s elite, many individuals proudly refer to themselves as “self-made billionaires.” But how many of them can rightly say this about themselves? Forbes analyzed the careers of all 400 entries on the list and divided them into one of ten categories.

The first six categories are occupied by people who have inherited some or all of their wealth. A distinction is also made as to whether these people continue to work or to what extent they have contributed to increasing their wealth. Around 29.5 percent of the list belongs to this category. Examples of this would be Walmart heir Jim Walton and Dolby heiress Dagmar Dolby.

Category number six is reserved for the 3.3 percent of billionaires who made their fortune as employees of a large company, such as former Microsoft CEO and Los Angeles Clippers owner Steve Ballmer.

The last four categories are those of self-made billionaires and are probably the most interesting. Overall, around 67.3 percent of the Forbes 400 fall into this category. But self-made is not the same as self-made. Around a tenth of these 269 people grew up with rich parents, another 59.5 percent come from the middle class - including the currently four richest people in the USA; Bezos, Musk, Zuckerberg and Gates. The working class has produced around 18.6 percent of self-made super-rich. Only about 28 people (10.4 percent) among the Forbes 400 live the proverbial American dream. Examples include hedge fund tycoon George Soros and talk show icon Oprah Winfrey.

More about it here:

Xpert.Digital for Biberach, Memmingen, Kempten and Krumbach. Support for your independent financial planning advice, wealth advice and investment advice

Konrad Wolfenstein

I would be happy to answer any further questions or help you may have.

You can contact me by filling out the contact form below or simply call me on 0731 550 40 117 .

I'm looking forward to our joint project.

Write to me

Xpert.Digital – Konrad Wolfenstein

Xpert.Digital is a hub for industry with a focus on digitalization, mechanical engineering, logistics/intralogistics and photovoltaics.

With our 360° business development solution, we support well-known companies from new business to after sales.

Market intelligence, smarketing, marketing automation, content development, PR, mail campaigns, personalized social media and lead nurturing are part of our digital tools.

You can find out more at: www.xpert.digital – www.xpert.solar – www.xpert.plus

Keep in touch