China's germanium embargo and its consequences for German industry: Price explosion of 165% – This metal becomes a nightmare – Image: Xpert.Digital

Following China's export ban: Price shock and chaos – is the Congo now Germany's salvation?

Price explosion of 165%: Tanks without night vision? How China's germanium ban is plunging the German armed forces into crisis

An almost unknown metal called germanium is plunging German industry into a full-blown crisis and revealing its dangerous dependence on China. When Beijing drastically restricted its exports of this strategically important raw material in August 2023, it was more than just an economic measure – it was the deployment of a geopolitical weapon in the global technology conflict. The consequences are dramatic: The price of the silvery-white metalloid has more than doubled within two years and is approaching €4,000 per kilogram.

Germany's key technological and military sectors are particularly affected. Without germanium, neither modern night-vision devices for tanks like the Leopard 2 nor highly efficient fiber optic cables for broadband expansion will function. The defense industry is alarmed, NATO is concerned, and companies are having to "pay almost any price" to maintain production. The dependency is sobering: Over 60 percent of Germany's needs have traditionally come from China, which controls around 85 percent of global production. Now Germany faces the pressing question: How can this critical supply gap be closed? What alternatives, from domestic mining to deliveries from the Congo, are truly viable? And what lessons must policymakers learn from this raw materials crisis?

Why is the entire German industry suddenly preoccupied with a metal called germanium? China has drastically reduced its germanium exports to Germany, creating a problem that extends far beyond the raw materials markets. As an expert in strategic materials and industrial dependencies, I explain the most important aspects of this development.

Related to this:

The basics of the germanium problem

What exactly is germanium and why is it so important?

Germanium is a silvery-white, lustrous metalloid with atomic number 32 in the periodic table. It was discovered in 1886 by the German chemist Clemens Winkler in Freiberg and named after Germania, the Latin name for Germany. Ironically, this "German" element is now primarily produced in China.

What makes germanium special are its unique physical properties. It exhibits excellent semiconductor properties, has good thermal conductivity, and is transparent to infrared light. These properties make it virtually indispensable for modern technologies. With a melting point of 937.4°C and its semiconductor properties, germanium finds application in various high-tech fields.

In which areas is germanium actually used?

The use of germanium is concentrated in three main areas. In infrared optics, it accounts for 72 percent of consumption, in fiber optic cables 19 percent, and in other applications 9 percent. These figures illustrate how specialized the applications are.

Specifically, germanium is used in fiber optic cables, where it improves the efficiency of light transmission. In semiconductor technology, it is used for specialized applications such as high-frequency and infrared technologies. Its role in the defense industry is particularly critical: germanium is essential for night vision devices, thermal imaging cameras, sensors, and high-tech lenses, for example, in drones and satellites. It is also used in X-ray detectors and as a catalyst for PET plastic production.

How dependent is Germany on Chinese germanium?

The figures are sobering. Until China imposed export restrictions in August 2023, around 60 percent of the germanium imported into Germany came from China. China controls approximately 80 to 85 percent of global germanium production. This extreme concentration makes the global supply extremely vulnerable.

German import statistics clearly illustrate the extent of this dependence: Germany imported 10.5 tons of germanium in 2022, 8.3 tons in 2023, and only 5.3 tons in 2024. Of all the germanium imported into Germany in 2024, almost 45 percent came from China, 23 percent from Denmark, 15 percent from South Korea, and 11 percent from Belgium. However, it remains unclear whether the imports from Denmark or Belgium are re-exports of Chinese germanium.

China's strategic raw materials policy

Why has China restricted germanium exports?

China introduced export controls on gallium and germanium in August 2023, officially citing national security. These raw materials are so-called dual-use goods, meaning they can be used for both civilian and military purposes. The measure was a direct response to US restrictions on the Chinese semiconductor industry.

Export controls operate through a licensing system: Chinese companies must apply for a permit to export germanium, and the processing officially takes 45 working days. In practice, this led to a drastic decline in exports. In December 2024, China then imposed a complete export ban on germanium to the USA.

How drastic is the decline in exports, really?

The figures speak for themselves. According to raw materials expert Justus Brinkmann, while China exported 28 tons of germanium in the first half of 2023, this figure dropped to just 12.4 tons for the entire year of 2024. In the first half of 2025, it was a mere 5 tons.

The decline is particularly drastic for Germany: Germany's share of Chinese exports fell from around half in 2024 to less than a fifth recently. Specifically, Germany has received only 902 kilograms from China so far in 2025. Compared to the same period last year, exports from China to Europe plummeted by almost 60 percent in the first half of the year.

What other raw materials are affected by Chinese export restrictions?

Germanium is part of a broader Chinese strategy. Since August 2023, gallium has also been subject to similar export controls, followed by graphite in December 2023. Restrictions on antimony followed in September 2024. At the beginning of 2025, China announced further export restrictions on tungsten, tellurium, bismuth, indium, and molybdenum.

These raw materials are all critical for future technologies: Gallium is used in semiconductor production and solar cells, graphite is a key raw material for lithium-ion batteries, and antimony plays an important role in the solar industry and for military applications. China systematically uses its dominant position in these materials as a geopolitical weapon.

The impact on German industry

How significant are the price increases?

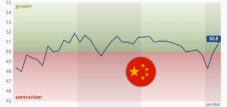

The price of germanium has developed dramatically. While the price per kilogram of 99.99% pure germanium was around €1,500 in 2023, by October 2025 it was already approaching the €4,000 mark – specifically, €3,983.70. This represents an increase of more than 165 percent.

The price trend illustrates the dramatic nature of the situation: from around €2,600 per kilogram in 2022 to over €3,400 in 2024. In the first months of 2025, total imports already averaged almost €3,800 per kilogram. World market prices for high-purity germanium have more than doubled within two years.

Which industries are particularly affected?

The defense industry is particularly alarmed. Germanium is essential for numerous military applications: night vision devices, infrared systems, sensors, high-tech lenses for drones, satellites, and specialized electronics. NATO is concerned about the supply shortages, as modern weapons systems are inoperable without these materials.

The telecommunications industry is also heavily affected. Germanium is used in fiber optic cables to improve the efficiency of light transmission. The semiconductor industry uses germanium for specialized applications, even though the majority of production is silicon-based. However, the German electrical and digital industries remain relatively unconcerned: germanium is not among the metalloids widely used by industry.

What specific problems arise in production?

So far, companies haven't had to reduce production, according to the consulting firm Inverto. Instead, purchasing teams are working intensively on individual solutions to procure the material – they simply have to accept the drastically rising prices. Companies are showing themselves to be prepared to "pay almost any price," as germanium expert Christian Hell from Tradium reports.

The problem lies not only in the higher costs, but also in the uncertainty of supply. The lengthy processing times for Chinese export licenses, up to 45 working days, significantly complicate planning. Companies with large germanium stockpiles are holding onto them and waiting to see how the market develops, which is driving prices even higher.

Alternative supply sources and their limitations

Which other countries produce germanium?

Besides China, other supplier countries include Belgium, Finland, Canada, and the USA. However, these Western alternatives face the same problems and needs as Germany. Available quantities are limited and cannot compensate for the disruption of Chinese deliveries.

An interesting development is taking place in the Democratic Republic of Congo. Since 2024, the Belgian plant of the raw materials company Umicore has been supplied from there. The germanium comes from the recycling of mining waste – specifically from the "Big Hill" spoil heap in Lubumbashi, which contains an estimated 14 million tons of metal-bearing slag. STL, a subsidiary of Gecamines, aims for an annual germanium production of 30 tons.

How realistic is a diversification of supply sources?

Diversification is difficult because germanium is mostly obtained as a byproduct. As raw materials expert Justus Brinkmann explains: "Germanium is generally obtained as a byproduct of zinc production. Extraction from lignite ash or copper production is also technically possible." This means that germanium availability depends on the production of these main raw materials.

Peter Buchholz, head of the German Mineral Resources Agency, warns: "With germanium, we're not as flexible as with gallium – there are few alternative sources of supply, even in the medium term." The markets are "highly concentrated," and industry urgently needs to develop other sources of supply. Other countries can only step in to a limited extent, as China has established a quasi-monopoly on critical raw materials.

What role does the Congo play as an alternative?

The Congo is developing into an important alternative source. The agreement between Umicore and STL was welcomed by the Minerals Security Partnership (MSP), which comprises 14 nations as well as the European Union and aims to connect industrialized countries with resource-rich states. The first test quantities of germanium concentrates were refined by Umicore in the last quarter of 2024.

However, the German Federal Ministry for Economic Cooperation and Development (BMZ) warns against the Congo: "Rich raw material deposits, poor business climate." The country is politically unstable and its infrastructure is inadequate. A recent analysis shows that Chinese companies have already secured access to Africa's most important raw material sources. Furthermore, Congolese imports cannot fully compensate for the losses incurred by China.

Related to this:

Germanium in the German arms industry

Why is germanium so critical for the German Armed Forces?

Germanium is indispensable for modern weapon systems. The metal is used in various systems of Leopard tanks and Eurofighter fighter jets. The German Armed Forces use germanium in third-generation thermal imaging devices, which offer high-resolution vision even at night and in adverse weather conditions.

Specifically, germanium is used in night vision devices, infrared systems, sensors, and high-tech lenses. Modern main battle tanks like the Leopard 2A8 are equipped with ATIA thermal imaging systems, which require germanium. Germanium-based systems are also installed in Eurofighter combat jets. NATO is concerned because a shortage of germanium could severely disrupt arms production.

What quantities does the arms industry need?

The exact quantities are mostly secret, but the amounts are considerable. A single F-35 fighter jet contains 420 kilograms of rare earth elements and critical materials. A large portion of this comes from China. Germanium is virtually indispensable for modern night vision devices and infrared systems.

The German Armed Forces recently ordered 16,041 additional night vision devices, which also require germanium. Given the planned modernization and the changing times, the demand will continue to rise. Germany is planning massive investments in new tanks, modernized infantry fighting vehicles, and armed drones – all of these systems rely on germanium.

How is NATO reacting to the supply shortages?

NATO is alarmed by the germanium shortage, as confirmed by various media reports. The scarcity of this critical raw material is causing the alliance considerable concern, as modern weapons systems are inoperable without germanium. "Germanium is currently a huge problem," n-tv quoted a manager of a German arms company as saying.

The alliance is working on solutions, but short-term alternatives are limited. Strategic stockpiling is becoming a key issue, but China is currently no longer exporting germanium for storage. NATO member states must fundamentally rethink their procurement strategies and develop alternative sources of supply.

Hub for Security and Defense - Advice and Information

Hub for Security and Defense - Image: Xpert.Digital

The Security and Defence Hub offers expert advice and up-to-date information to effectively support companies and organizations in strengthening their role in European security and defence policy. Working closely with the SME Connect Defence Working Group, it particularly promotes small and medium-sized enterprises (SMEs) that wish to further develop their innovative capacity and competitiveness in the defence sector. As a central point of contact, the Hub thus creates a crucial bridge between SMEs and European defence strategy.

Related to this:

Germanium shortage: Can Germany build its own supply? Strategies for the future – How Germany can achieve resource resilience

Possibilities of domestic production

Can Germany produce its own germanium?

Theoretically yes, but practically it's difficult. Germany has zinc, copper, and lignite deposits from which germanium could be extracted as a byproduct. Research is already underway into the feasibility of such post-mining operations. Trace metals like germanium, gallium, and indium could be recovered from residual reserves of old mines or from new deposits.

Previously, this was not economically viable, but the scarcity is shifting the economic landscape. The Federal Institute for Geosciences and Natural Resources describes significant raw material potential in Germany's geological subsurface. Several dozen exploration projects are currently underway in Saxony, including those targeting metals such as indium, silver, zinc, and other raw materials relevant to germanium.

What are the challenges facing domestic mining?

The challenges are manifold. First, significant investments are required: "Investments in raw material production and recycling are substantial and long-term," explains raw materials expert Brinkmann. Purchase guarantees are crucial, as such investments are too risky without planning certainty.

The permitting processes are lengthy and complex. Entering the raw material extraction sector in densely populated Germany is not only technically challenging but also involves extensive permitting procedures. While the EU aims to shorten these processes – reducing environmental impact assessments from one year to 90 days and permitting procedures to a maximum of two years – implementation is taking time.

What role can recycling play?

Recycling could play an important role, but is currently limited. The recycling rate for germanium in the EU is only two percent. Some of the supply already comes from factory scrap, while germanium scrap is also recovered from the windows of decommissioned tanks and other military vehicles.

However, the recyclability of germanium is limited. For most critical raw materials – such as rare earth elements, indium, or germanium – recycling rates remain negligible. This is because germanium is often present in products only in very small quantities, and recovery is technically difficult and economically unattractive.

Related to this:

Substitution options and technical alternatives

Can germanium be replaced by other materials?

In principle, both substances can be replaced, explains raw materials expert Justus Brinkmann, but this would reduce the conductivity of the products. "Germanium is difficult to substitute because of its exceptional conductivity," he confirms. In most applications, germanium cannot be replaced without significantly compromising the functionality of the products.

For some specific applications, alternatives exist: Germanium can be partially replaced with silicon, and zinc selenide is a possible alternative for infrared devices. However, this usually results in a decrease in performance. For example, germanium-free thermal imaging lenses are now available, but such innovations take time.

What are the technical challenges involved in substitution?

Substitution is a long-term strategy. Unless a company happens to be researching alternative materials and is already relatively far along in development, it cannot quickly replace germanium with less critical materials. The unique properties of germanium—its infrared transmittance, excellent thermal conductivity, and semiconductor properties—are difficult to replicate.

Barium fluoride is being discussed as an interesting alternative to germanium for use at higher temperatures. For optics larger than 100 millimeters in diameter, germanium is already viewed critically due to limited supply and high costs. Nevertheless, these alternatives cannot completely replace the unique properties of germanium.

How realistic are short-term technical solutions?

Short-term solutions are unrealistic. Developing substitute materials or alternative technologies takes years, even decades. Technical literature repeatedly points out that substitutions are associated with performance losses. Therefore, companies must live with high prices and uncertain supply in the medium term.

Industry is therefore primarily relying on proven measures: improved material efficiency, long-term supply contracts, and supplier diversification. However, more innovative measures such as recycling, as well as research and development, remain the domain of large corporations. Most companies are not prepared for short-term solutions.

The role of politics and strategic consequences

What can German politics do?

Policymakers have a responsibility to provide the raw materials sector with greater planning certainty. Raw materials expert Brinkmann sees a clear mandate here: "Purchase guarantees would be crucial, as investments in raw material production and recycling are substantial and long-term." Without government support, private investments in domestic raw material extraction are too risky.

Raw material extraction should be given legal priority to ensure that demand is met in a timely manner and that legal and planning certainty is increased. The German government has already developed a raw materials strategy, but its implementation is slow. Germany must reduce its dependence on unreliable suppliers like China and diversify its supply chains.

What European initiatives exist?

The EU has presented a strategy for 34 critical raw materials with the Critical Raw Materials Act (CRMA). Germanium and gallium are among the raw materials classified as particularly critical. The EU aims to source ten percent of these strategically important raw materials within the EU in the future – currently, it is only three percent.

The approval processes are to be significantly accelerated: environmental impact assessments from one year to 90 days, and permitting procedures to a maximum of two years. Brussels supports the promotion of domestic raw materials with investment incentives and expedited processes. The goal is to reduce dependence on individual supplier countries and promote domestic production.

How should Germany change its raw materials policy?

Germany needs a comprehensive raw materials strategy that goes beyond previous approaches. Current political initiatives provide important impetus, but they are not enough. The dependence on domestic imports for key raw materials can be reduced through the rapid development of domestic refining and processing capacities within the EU, as well as through recycling.

Germany should forge strategic partnerships with resource-rich countries and promote domestic raw material extraction. The EU should have started building strategic reserves as early as 2023, warns expert Christian Hell. Now it is too late, since China no longer exports germanium for storage. New recycling options and investments in research and development are also needed.

Related to this:

- Mega-deal nearing completion: World's largest free trade zone – The EU-Mercosur agreement

- EU-India Free Trade Agreement – Opportunities and advantages for German companies – Ambitious agreement planned for 2025

- The modernized EU-Mexico Free Trade Agreement: A comprehensive analysis of the 2025 agreement

Long-term perspectives and market development

How will the germanium market develop?

The forecasts are bleak. At the beginning of the year, the consulting firm Deloitte predicted a supply shortage for 2024, a prediction that has now been confirmed. Experts expect prices to continue rising as long as China maintains its export restrictions. The market is proving extremely volatile and sensitive to geopolitical developments.

Matthias Rüth of Tradium explains the ongoing problems: Legally mandated stockpiling of key raw materials in China has led to a shortage in the market. Additionally, global demand for germanium is rising, particularly in the infrared industry. Companies with large germanium reserves are holding onto them and waiting, which is driving prices even higher.

What geopolitical consequences can be expected?

The germanium shortage is just a taste of future geopolitical resource wars. China is using its dominant position in supplying the global market with many critical raw materials as an effective geopolitical weapon. The world is evolving from an open global economy into a multipolar world with intensified resource conflicts.

Europe and the US must learn that raw materials have long since become a tactical weapon. China systematically responds to Western technological restrictions with raw material embargoes. This strategy is likely to expand to other critical materials. The struggle for metals like germanium marks a new era of geopolitical resource wars.

What does this mean for German companies?

German companies need to fundamentally rethink their procurement strategies. The days of cheap and reliable deliveries from China are over. Companies are prepared to "pay almost any price," but this is not a sustainable solution. In the long term, they must invest in alternative sources of supply, recycling, and research into substitutions.

The primary measures currently in use are still relatively uninnovative – and even these are only implemented in half of all companies. More comprehensive preparedness seems necessary, encompassing strategic inventory management, long-term supply contracts, and the development of spare parts. Smaller companies, in particular, are often insufficiently prepared and dependent on government support.

Lessons for the future

What lessons can be learned from the germanium crisis?

The germanium crisis exposes the dangerous dependence on individual supplier countries for critical raw materials. It shows how quickly geopolitical tensions can lead to supply shortages. Germany and Europe ignored the warning signs for too long and are now in a difficult position.

The crisis makes it clear that decoupling economic growth from raw material demand is not feasible. Raw material productivity cannot be increased to such an extent that raw material imports become unnecessary. As a highly developed and export-oriented economy, Germany will continue to depend on critical raw materials in the future.

What structural changes are needed?

Germany and Europe must establish a sustainable circular economy for mineral and metallic raw materials. Domestic primary raw materials and efficient recycling must be developed as complementary sources of supply. Metals are ideal candidates for this, as they are only used, not consumed.

Diversifying supply sources is essential, but not sufficient. Germany must invest in domestic raw material extraction, even if complete self-sufficiency is unrealistic. Rather, the goal is to achieve resilience and no longer be entirely dependent on individual supplier countries. Building strategic reserves, promoting recycling technologies, and developing substitution options are indispensable.

What could a resilient raw material supply look like?

A resilient raw material supply requires a mix of different strategies. First, domestic raw material sources must be developed, even if this involves higher costs. Second, strategic partnerships must be established with reliable supplier countries outside of China. Third, recycling and the circular economy must be massively expanded.

Fourth, investments in research and development for substitute materials are needed. Fifth, strategic reserves must be built up to cushion short-term supply disruptions. All these measures require long-term planning, significant investment, and political support. The germanium crisis shows that those who react too late pay a high price.

Your global marketing and business development partner

☑️ Our business language is English or German

☑️ NEW: Correspondence in your native language!

Konrad Wolfenstein

I and my team are happy to be available to you as your personal advisor.

You can contact me by filling out the contact form here wolfenstein@xpert.digital:or simply call me at +49 7348 4088 965. My email address is

I'm looking forward to our joint project.

☑️ SME support in strategy, consulting, planning and implementation

☑️ Creation or realignment of the digital strategy and digitization

☑️ Expansion and optimization of international sales processes

☑️ Global & Digital B2B trading platforms

☑️ Pioneer Business Development / Marketing / PR / Trade Fairs

Our EU and German expertise in business development, sales and marketing

Our EU and German expertise in business development, sales and marketing - Image: Xpert.Digital

Industry focus areas: B2B, digitalization (from AI to XR), mechanical engineering, logistics, renewable energies and industry

More information here:

A thematic hub offering insights and expertise:

- Knowledge platform covering global and regional economies, innovation and industry-specific trends

- A collection of analyses, insights, and background information from our key areas of focus

- A place for expertise and information on current developments in business and technology

- A hub for companies seeking information on markets, digitalization, and industry innovations