Dangerous overproduction: China is flooding the market with robots – Is the photovoltaic scenario repeating itself? – Image: Xpert.Digital

The next wave of exports from China could already be underway

China's robot boom: Is the next major collapse looming after the 'solar miracle'?

The rapid expansion of the Chinese robotics industry shows striking parallels to the development of photovoltaics over the past decade. With billions in state aid, aggressive capacity expansion, and increasing export ambitions, a new chapter of industrial dominance from the Far East is dawning. While European companies are still debating strategies, Chinese manufacturers are already creating facts on the ground – with potentially far-reaching consequences for the global competitive landscape.

As early as 2017, the Chinese Ministry of Industry warned of overcapacity, speaking of "low-end production of high-end products" and "overcapacity in low-end products." With over 1,000 robotics companies in China, there are strong indications of a similar overproduction situation to that experienced in the solar industry.

Starting point of the technological power shift

Within just a few years, China has transformed itself from an importer of industrial automation technology into the dominant player in the global robotics industry. This transformation is taking place with a speed and systematic approach reminiscent of the success story of China's photovoltaic sector. In 2024, for the first time, Chinese companies installed more industrial robots domestically than all their foreign competitors combined – a turning point that has the industry taking notice.

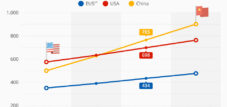

The figures speak for themselves: With 295,000 newly installed industrial robots in 2024, China accounts for 54 percent of the global market. The operational stock of over two million robots represents an international record. At the same time, the market share of domestic manufacturers is growing steadily – from 28 percent in 2014 to 57 percent in 2024.

This development is not accidental, but rather the result of a systematic industrial policy that defines robotics as a key technology for China's economic future. The €128 billion sovereign wealth fund for robotics, artificial intelligence, and cutting-edge innovation underscores the political will to achieve a dominant position in this sector as well. The parallels to the state-sponsored expansion of the solar industry are unmistakable.

Particularly noteworthy is the focus on humanoid robots, whose mass production is slated to begin as early as 2025. With over 1,000 robotics companies and an expected annual growth of ten percent until 2028, China is positioning itself as a global market leader in a technology that is only just beginning its commercial application.

Related to this:

The roots of the Chinese robotics boom

China's rise to robotics superpower didn't happen overnight, but followed a long-term strategic plan that had its roots in the early 2010s. The foundation was laid by the "Made in China 2025" program, published in 2015, which defined robotics as one of ten key industries in which Chinese companies should strive for global market leadership by 2025.

Paradoxically, the automotive industry was the initial spark for the robotics boom. Massive investments in vehicle production since 2010 have significantly boosted demand for industrial robots. China has become both the world's largest car market and the largest production base for vehicles, including electric cars. This dual role as producer and consumer created the critical mass for an independent robotics industry.

A decisive turning point occurred in 2016 when the electrical and electronics industry overtook the automotive industry as the primary customer for industrial robots. This shift reflected China's growing importance as a production hub for electronic devices, batteries, semiconductors, and microchips. The geographic concentration of production in China created optimal conditions for local robot manufacturers, enabling them to test and further develop their products directly on-site.

The years 2017 to 2019 marked a critical phase. As early as 2017, the Chinese Ministry of Industry warned of overcapacity in the robotics sector and spoke of risks arising from "low-end production of high-end products." Nevertheless, growth continued, driven by the strategic decision to use robotics as a growth engine for industrial transformation.

The COVID-19 pandemic further accelerated the trend toward automation. While other countries struggled with production losses, China increased its investments in robot-assisted manufacturing systems. The national robotics strategy published in December 2021 underscored the political will to systematically strengthen the competitiveness of the economy through automation.

In fact, current industry overviews, market studies and statements from industry associations usually estimate the number of Chinese robotics companies to be well over 1,000, making China the world's largest robotics industry in terms of the number of companies and production volume.

China is the world's largest robotics market, with its robotics industry generating revenues of over 240 billion yuan (approximately US$33.4 billion). Not only are hundreds of thousands of new robots produced and installed annually in China, but a very broad business sector also operates in the fields of industrial robotics, service robotics, and humanoid robots.

Experts and reports from industry events such as the World Robot Conference or the China Robot Industry Alliance (CRIA) repeatedly highlight that China now has more than 1,000 robotics companies. These include large corporations like Siasun, Estun, Inovance, and Geek+, as well as numerous medium-sized and small companies focusing on development, component supply, integration, and software.

Due to a national innovation strategy and high demand from numerous industrial sectors, the number of robotics companies in China continues to rise – both Chinese suppliers and international manufacturers operating factories and development labs in China are part of this growth.

Related to this:

Key elements of Chinese robotics dominance: The central mechanisms and building blocks

China's robotics offensive is based on several interconnected mechanisms that, in combination, generate exceptional power. The most important component is the industrial ecosystem that has developed over the past decades and is now considered unique. In the mechatronics industry, no other country can bring new products to market so quickly and then manufacture them to high quality and competitive prices.

A key advantage lies in the local supply chain. While European manufacturers often rely on components from various countries, Chinese companies can draw on a dense network of specialized suppliers. This prioritization of the local supply chain has led to a robust ecosystem that has now become attractive to international manufacturers as well. Even a significant portion of the hardware for the Tesla Optimus is expected to come from China.

The advantage in skilled labor represents another critical success factor. China has significantly more available skilled workers than Europe, both in development and systems integration. These human resources enable shorter product cycles and drastically lower costs for machine vision, industrial robots, and collaborative robots.

State support manifests itself not only in direct subsidies but also in strategic industrial policy. Beijing creates advantages for its own companies through protected domestic markets and cheap loans from state-owned banks. These companies are not bound by the law of profitability and can build massive production capacities, regardless of short-term profitability.

Particularly noteworthy is the crossover strategy for components. Chinese robot manufacturers benefit from the mature supply chain in the electric vehicle sector and use components from the automotive industry for their robots. These synergies reduce development costs and accelerate the market launch of new products.

Related to this:

The current market position: its significance and application in today's context

Today, China is not only the world's largest robotics market, but has also achieved technological leadership in several segments. Chinese manufacturers already hold a 90 percent market share in collaborative robots and an even higher 95 percent in mobile robots. This dominance in future-oriented segments is particularly significant, as it paves the way for the next generation of automation technology.

Robot density – a key indicator of automation levels – illustrates China's rapid catch-up process. With 470 robots per 10,000 employees, China has overtaken Germany (429 robots per 10,000 employees) and ranks third worldwide. Just five years ago, robot density in Germany was more than ten times higher than in China.

Application know-how is now frequently flowing in the opposite direction – from China to Europe. This trend is particularly evident in the electronics industry, where almost two-thirds of all industrial robots worldwide are installed in China alone. Chinese manufacturers supplied 54 percent of all units for this enormous domestic market, thus covering around 33 percent of global demand in the electronics industry.

The export strategy is beginning to change. While previously less than five percent of Chinese robots were exported, companies like Inovance and Geekplus are increasingly pushing into international markets. Inovance, the second-largest domestic robot manufacturer, is expanding into Europe, while Geekplus already generates 70 percent of its revenue outside of China.

Chinese manufacturers are showing growing ambitions, particularly in the premium segment. Traditionally, European and Japanese suppliers dominated this market segment, but customers are increasingly turning to Chinese alternatives. The strategy is to achieve 80 percent of the quality of foreign competitors while selling at 20 percent of the price.

Our China expertise in business development, sales and marketing

Our China expertise in business development, sales and marketing - Image: Xpert.Digital

Industry focus areas: B2B, digitalization (from AI to XR), mechanical engineering, logistics, renewable energies and industry

More information here:

A thematic hub offering insights and expertise:

- Knowledge platform covering global and regional economies, innovation and industry-specific trends

- A collection of analyses, insights, and background information from our key areas of focus

- A place for expertise and information on current developments in business and technology

- A hub for companies seeking information on markets, digitalization, and industry innovations

From solar panels to a flood of robots: Is Europe facing a déjà vu?

Practical examples of market conquest: Concrete use cases and illustrations

The success story of Geekplus exemplifies how Chinese robotics companies are conquering global markets. This company, specializing in warehouse robotics, only went public in Hong Kong in the summer of 2024, yet already generates 70 percent of its revenue outside of China. Its customers include international corporations such as Unilever, Walmart, and Adidas. The company's Roboshuttle series offers all-in-one picking solutions that coordinate three different robot types around a central workstation. This solution optimizes vertical storage space and eliminates the need for multiple zones.

Geekplus is also demonstrating its strategic preparation for potential trade restrictions. The company generates roughly a quarter of its revenue in the US, but produces 30 percent more cheaply than its competitors. In addition, Geekplus plans to relocate parts of its assembly to Japan to circumvent potential trade barriers. This flexibility in production strategy shows the ability of Chinese companies to learn from past trade conflicts.

The second example is Inovance, often called a "mini Huawei" because it was founded in 2003 by former Huawei engineers. The company has become the second-largest domestic manufacturer of industrial robots in China and is now systematically expanding into Europe. With its German headquarters in Pleidelsheim near Heilbronn, Inovance is building a local presence and leveraging its extensive industry expertise from China. The company has experience selling robots to major smartphone and laptop manufacturers and can benefit from the economies of scale offered by the Chinese market.

Inovance's expansion strategy reflects the typical approach of Chinese companies: first, building a local sales and service structure, then gradually increasing local value creation. In Europe, Inovance initially offers robots with payloads up to 20 kilograms, while in China, models with payloads up to 300 kilograms are available. This phased market launch allows the company to gather experience and gradually expand its product portfolio.

Problematic developments and risks: A critical analysis

The rapid expansion of the Chinese robotics industry carries structural risks reminiscent of developments in the photovoltaic sector. As early as 2017, the Chinese Ministry of Industry warned of overcapacity, speaking of "low-end production of high-end products" and "overcapacity in low-end products." With over 1,000 robotics companies in China, there are strong indications of a similar overproduction situation to that experienced in the solar industry.

The parallels to photovoltaics are striking. Just as with solar panels back then, China is building massive production capacities that far exceed domestic demand. The solution lies in exports, leading to fierce competition in international markets. Chinese robots are already 20 to 30 percent cheaper than their European competitors, a price advantage made possible by government subsidies and economies of scale.

European companies are coming under increasing pressure. The German industry association VDMA Robotics and Automation has halved its growth forecast due to intensified competition from Chinese rivals. Traditional European robot manufacturers are losing market share, while Chinese companies are systematically expanding their presence in Europe. Companies such as Dobot, Elite Robots, and Jaka Robotics have already established local service and sales structures in Germany.

Technology transfer is particularly problematic. Leading foreign companies like KUKA, ABB, and Fanuc have opened state-of-the-art production facilities in China. This knowledge transfer enables Chinese manufacturers to quickly catch up and develop their own products. German startups are already sourcing robot arms and components such as joints with integrated force sensors from China, further increasing technological dependence.

The danger of "involution"—a ruinous competition for market share at the expense of profitability—is real. China's Ministry of Industry has already initiated measures against "disorderly competition" and aggressive pricing practices. Similar warnings were issued in the solar industry before the global overproduction crisis began.

Related to this:

Future scenarios and market development: Expected trends and potential disruptions

The coming years will be crucial in determining whether the photovoltaic scenario repeats itself in robotics. Several trends indicate that China will further expand its dominance. 2025 is considered "year zero" for humanoid robots, with Chinese companies already in mass production while international competitors are still in the development phase.

Government support will continue and intensify. The €128 billion robotics fund is designed to operate for 20 years, underscoring a long-term perspective. By 2027, China aims to develop humanoid robots capable of "thinking, learning, and innovating." The market volume for humanoid robots in China is projected to reach €44 billion by 2031.

Three scenarios are conceivable for global development. In the most optimistic case, stable competition will establish itself between Chinese and international suppliers, serving different market segments. Chinese manufacturers would primarily operate in the cost-sensitive mass market, while European and Japanese companies would occupy premium segments.

The more likely scenario involves a gradual displacement of international suppliers, similar to the developments in the solar industry. Chinese companies will leverage their cost advantages to initially gain a foothold in standard applications and then successively penetrate higher-value segments. The expansion already underway into Europe and other markets will accelerate.

In the worst-case scenario, an overproduction crisis leads to a global price collapse, forcing many companies to close. Consolidation would primarily benefit Chinese manufacturers, who have larger financial reserves and access to government support. Europe could lose its technological sovereignty in yet another key sector.

The likelihood of the second or third scenario increases due to China's stated export strategy. The government has defined robot exports as a strategic goal and intends to use them as an engine of growth. This political objective, combined with domestic overcapacity, will increase export pressure.

Related to this:

Strategic Implications and Evaluation

China's robotics offensive represents one of the greatest industrial policy challenges for Europe in decades. The parallels to the development of photovoltaics are not coincidental, but rather the result of a systematic strategy that transfers proven patterns to new technological fields. China is using state support, economies of scale, and aggressive pricing to achieve market leadership in strategically important industries.

The speed of development is impressive. Within a decade, China has increased its market share in industrial robots from under 30 percent to over 50 percent. In future-oriented segments such as collaborative and mobile robots, Chinese manufacturers already dominate with market shares of 90 to 95 percent. This dominance in key technologies will impact downstream industries and fundamentally challenge Europe's competitiveness.

European companies have three strategic options. First, they can try to occupy niche markets through innovation and specialization, where technological superiority is more important than price. Second, they can form strategic partnerships with Chinese companies to gain access to their cost structures. Third, they can partially relocate their production to China to benefit from economies of scale there.

None of these options is without risk. Niche markets can erode rapidly due to technological advances. Partnerships carry the risk of technology transfer and medium-term dependency. Relocating production exacerbates the industrial decline of Europe and makes companies geopolitically vulnerable.

The challenge is structural in nature and requires a coordinated European response. Individual companies or countries cannot successfully counter Chinese systemic competition. Joint research programs, coordinated industrial policies, and potentially protectionist measures are necessary to preserve core European competencies.

Time is of the essence. While Europe is still developing strategic concepts, Chinese companies are already creating market realities. The robotics industry could become the next example of how systematic industrial policy trumps short-term market mechanisms. Europe must act quickly to avoid falling behind in this future market as well.

Your global marketing and business development partner

☑️ Our business language is English or German

☑️ NEW: Correspondence in your native language!

Konrad Wolfenstein

I and my team are happy to be available to you as your personal advisor.

You can contact me by filling out the contact form here wolfenstein@xpert.digital:or simply call me at +49 7348 4088 965. My email address is

I'm looking forward to our joint project.

☑️ SME support in strategy, consulting, planning and implementation

☑️ Creation or realignment of the digital strategy and digitization

☑️ Expansion and optimization of international sales processes

☑️ Global & Digital B2B trading platforms

☑️ Pioneer Business Development / Marketing / PR / Trade Fairs

Our recommendation: 🌍 Limitless reach 🔗 Connected 🌐 Multilingual 💪 Sales power: 💡 Authentic with strategy 🚀 Innovation meets 🧠 Intuition

From local to global: SMEs conquer the world market with a clever strategy - Image: Xpert.Digital

In an era where a company's digital presence determines its success, the challenge lies in creating an authentic, personalized, and far-reaching presence. Xpert.Digital offers an innovative solution that positions itself as the intersection of an industry hub, a blog, and a brand ambassador. It combines the advantages of communication and sales channels in a single platform and enables publication in 18 different languages. Cooperation with partner portals and the ability to publish articles on Google News and a press distribution list with approximately 8,000 journalists and readers maximize the reach and visibility of the content. This represents a crucial factor in external sales and marketing (SMarketing).

More information here: