Capital injection for Chinese banks: An analysis in the context of trade disputes and economic challenges – Image: Xpert.Digital

How China's government plans to save the economy with capital injections

A multi-billion dollar answer to complex problems

The Chinese government is taking a remarkable step to strengthen its financial system and boost the economy: it has injected billions of US dollars into four of its largest state-owned banks. This capital injection, totaling approximately US$71.6 billion, came amid a series of economic challenges plaguing the country. These included slowing economic growth, a struggling housing sector, persistent deflationary pressures, and increasing economic strain from US tariffs.

The capital injection was aimed at improving these banks' lending capacity. The government hoped that the strengthened capital base would enable the banks to grant more loans to businesses and individuals, which in turn would boost investment and consumption, thus stimulating the economy as a whole.

However, it is important to emphasize that this measure should not be seen as an isolated solution. The Chinese economy faced a multitude of problems, and the capital injection was only one part of a broader strategy to address these challenges. Critics expressed doubts as to whether the measure alone would be sufficient to sustainably stimulate the economy.

Related to this:

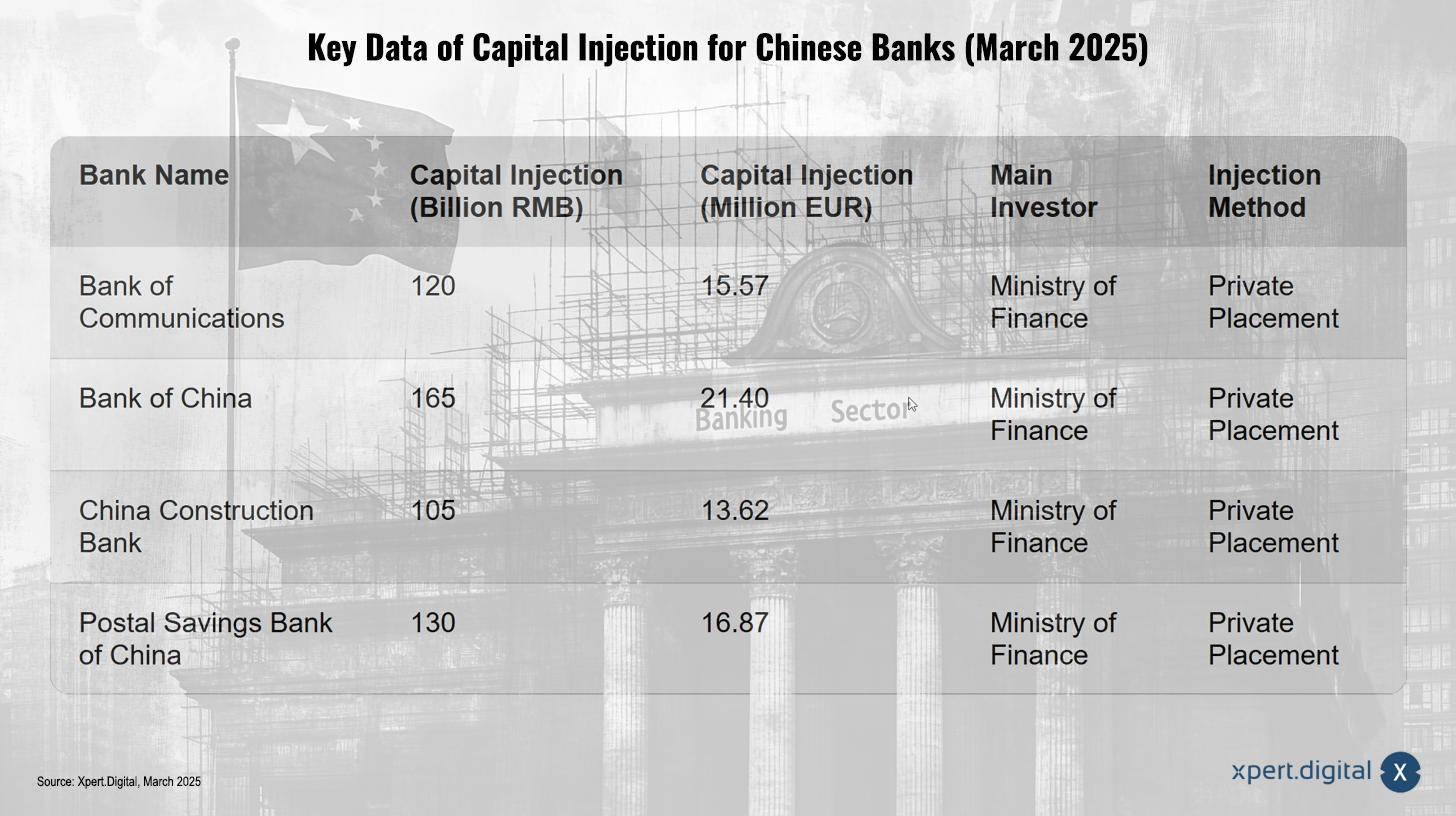

Details of the capital injection: scope, mechanism and objectives

Key data of the capital injection for Chinese banks (March 2025) – Image: Xpert.Digital

The capital injection, which was officially confirmed on March 30, 2025, affected the following four major banks:

- Bank of Communications

- Bank of China

- China Construction Bank

- Postal Savings Bank of China (PSBC)

The total sum amounted to approximately US$71.6 billion, which was roughly equivalent to 520 billion yuan. It is worth noting that the figure of €66 billion mentioned in some reports was in a similar range due to exchange rate fluctuations.

How did the capital injection work?

The capital increase was achieved through private placements of shares with investors. The Chinese Ministry of Finance played a central role as the main investor, acquiring shares worth 500 billion yuan. This measure came shortly after the government announced it would issue 500 billion yuan in special government bonds to bolster the capital of the country's largest state-owned lenders. The Ministry of Finance confirmed that the proceeds from these bonds were used to finance the capital injection.

Why was Tier 1 core capital strengthened?

The main purpose of the capital injection was to strengthen banks' capital, improve the quality of their balance sheets, and stimulate lending to keep the economy running. Particular emphasis was placed on replenishing banks' Tier 1 core capital. Tier 1 core capital is a crucial indicator of a bank's financial strength, as it comprises the highest-quality capital components, such as retained earnings and reported capital. It serves as a buffer to absorb losses and ensure the bank's stability.

The emphasis on Tier 1 core capital suggests that the government was not merely aiming to meet minimum regulatory requirements, but rather to achieve a fundamental level of financial soundness for banks. This could indicate that the government was anticipating potential future strains on the banking system due to economic uncertainties.

China's economic challenges in 2025: A multifaceted problem

The capital injection did not occur in a vacuum. It was a response to a number of economic challenges that China faced in 2025:

Slowed economic growth

The Chinese government had set a target of around five percent economic growth for 2025. However, given the weak growth, analysts had called for the rapid injection of fresh capital into the country's major banks. Although China achieved growth of approximately 5 percent in 2024, the foundation for a sustainable recovery was not yet solid, as both domestic and foreign demand were weak and the real estate sector continued to face challenges. Achieving the five percent growth target for 2025 thus presented a significant challenge, necessitating measures such as the capital injection into the banking sector to stimulate economic activity.

Real estate crisis

Chinese banks were grappling with a substantial volume of non-performing loans amid a sustained slump in the real estate sector. The capital injection was aimed at boosting lending, which in turn could support the country's struggling real estate sector. However, the situation in the real estate sector remained tense. Reports indicated that real estate continued to be a significant drag on the economy, as prices and investment had not yet bottomed out, although the rate of decline had slowed. Various outlooks for the real estate market in 2025 ranged from potential stabilization in the second half of the year to expectations of continued price declines and no broad recovery. Oversupply remained a serious challenge.

The real estate crisis was therefore a significant factor affecting the health of Chinese banks and the overall economy, making the capital injection partly a measure to minimize risk in the event of further deterioration in this sector.

Related to this:

US tariffs

Since February 2025, Chinese exports have been subject to US tariffs, which were significantly increased in March 2025. It was assumed that building up capital buffers at banks could help manage the risks to the Chinese economy amid the escalating trade conflict with the US. The US tariffs thus contributed to the economic headwinds China faced, as they potentially harmed export-oriented companies and increased the risk of loan defaults, necessitating stronger bank capitalization.

Deflationary pressure

The government attempted to combat deflationary pressures. Reports confirmed the presence of deflation in China at the beginning of 2025, with consumer inflation falling below zero and producer prices also declining. This trend had persisted for several quarters. Deflation can weaken consumer demand and business investment, thus further slowing economic growth. Deflationary pressures exacerbated the challenges of weak economic growth and the housing crisis, potentially leading to lower profitability for businesses and increased difficulties in repaying loans, thereby impacting banks.

Related to this:

How the capital injection should work: mechanism and expected effects

The capital injection should essentially work through two mechanisms:

- Strengthening banks' capital base: This would allow banks to increase their lending without jeopardizing their financial stability. A well-capitalized bank can absorb capital losses without reducing its lending.

- Boosting lending: Increased lending should help to revive the country's slowing economy. In particular, it should support the country's struggling real estate sector.

It was expected that the capital injection would enable banks to better serve the real economy and provide greater support for the country's steady and long-term economic development.

New approaches to restoring trust in households and businesses

However, policymakers still faced the challenge of restoring the confidence of households and businesses, which remained hesitant to spend. There was also the risk of a deterioration in credit quality as banks attempted to expand consumer lending.

Although the capital injection was intended to boost lending, its effectiveness in promoting economic recovery depended on whether confidence was restored and whether the increased lending actually led to spending and investment without a significant deterioration in credit quality.

The role of US tariffs in China's economic landscape: An additional burden

The US tariffs imposed on Chinese imports represented an additional burden on the Chinese economy. On March 4, 2025, tariffs on all Chinese imports were increased from 10% to 20% under the International Emergency Economic Powers Act (IEEPA). The increase was justified by China's alleged failure to adequately address the fentanyl crisis.

It is important to note that certain exceptions could apply, for example for goods that were in transit before 1 February 2025, as well as specific provisions of HTSUS Chapter 98.

The tariffs were expected to negatively impact Asia-Pacific economies, including China's. Analysts anticipated that the tariffs would dampen Chinese growth through lower exports, investment, and other ripple effects. However, there were differing assessments of the extent to which the tariffs would affect Chinese growth.

China's broader economic context at the beginning of 2025: A mixed picture

To fully understand the impact of the capital injection and the US tariffs, it is important to consider China's broader economic context at the beginning of 2025:

- Chinese industrial production rose by 5.9% year-on-year in the first two months of 2025, representing a slight slowdown compared to December.

- Real retail sales rose by 4.1% year-on-year in the first two months, showing some improvement but remaining weak compared to pre-pandemic rates.

- Chinese consumer inflation fell below zero in February 2025, indicating deflationary pressures. Producer prices also continued to decline. China had set a relatively low inflation target of around 2% for 2025, suggesting an expectation of continued low inflation.

- Real estate investment remained negative in the first two months of 2025. Prices for new and existing homes continued to fall month-on-month in February, although the decline slowed in some cities. Oversupply and weak consumer confidence continued to weigh on the housing market.

Overall, the Chinese economic outlook at the beginning of 2025 was mixed. There were some positive signs, such as growth in industrial production and retail sales. However, there were also significant challenges, such as deflation and the real estate crisis.

Expert opinions on the capital injection: A predominantly positive assessment

Analysts and economists generally expressed positive views on the capital injection:

- Analysts at Northeast Securities expected the recapitalization plans to help lenders increase their capital buffers and manage asset quality pressures. They pointed out that falling interest rates and declining profits had increased the capital pressure on banks.

- HSBC Global Research believed that the capital injection would benefit the resilience of the Chinese banking system.

- S&P Global Ratings stated that the capital injections would give major banks more options to finance the country's growth in the face of tariff headwinds and to improve their loss-absorbing buffers in the face of profit pressures. They expected that with the fresh capital, major banks would continue to prioritize areas such as inclusive finance, advanced manufacturing, and green energy.

However, some experts warned that the capital injection alone might not be enough to sustainably boost the Chinese economy. They emphasized the need to restore consumer and business confidence and address the underlying problems in the real estate sector.

Related to this:

Historical Parallels and Lessons: A Look into the Past

It is helpful to place the current capital injection in the context of historical parallels:

- China has made significant efforts in the past to restructure its banking sector, particularly in the late 1990s, to manage large volumes of non-performing loans. This included issuing special government bonds and injecting capital into the “big four” state-owned banks. The costs of these earlier restructurings were substantial, potentially reaching a significant percentage of GDP.

- During the 2008 financial crisis, governments worldwide used bank bailouts and capital injections to stabilize their financial systems. Examples include the US Troubled Asset Relief Program (TARP).

These historical examples show that government intervention in the financial sector is a common tool during times of economic stress. However, they also show that the success of these measures depends on a wide range of factors, including the general economic climate and the effectiveness of other accompanying policy measures.

A step in the right direction, but not the whole solution

The capital injection into China's four major banks represents a significant and multifaceted response to the country's current economic challenges. In the short term, it aims to improve the banks' capital base and increase their lending capacity. This could potentially help stabilize the struggling real estate sector and support a broader economic recovery.

However, significant uncertainties remain regarding the long-term effectiveness of this measure. Persistent deflationary pressures and underlying problems in the housing sector could continue to dampen the willingness of businesses and households to borrow and invest. Furthermore, the increasing pressure from US tariffs represents an external burden that could potentially diminish the positive effects of the capital injection.

Experience from previous bank recapitalizations in China and international responses to financial crises and trade wars suggests that government intervention in the financial sector is a common crisis management tool. However, the success of these measures depends on a wide range of factors, including the overall economic climate and the effectiveness of other accompanying policy measures.

The future development of the Chinese economy will be largely determined by the interaction of these factors. While the capital injection is an important measure to strengthen the financial system, it is unlikely to be a sole solution to the complex economic challenges facing China in 2025. The government's ability to restore confidence, curb deflation, and mitigate the negative effects of US tariffs will be crucial for the country's future economic performance.

Related to this:

Your global marketing and business development partner

☑️ Our business language is English or German

☑️ NEW: Correspondence in your native language!

Konrad Wolfenstein

I and my team are happy to be available to you as your personal advisor.

You can contact me by filling out the contact form here wolfenstein@xpert.digital:or simply call me at +49 7348 4088 965. My email address is

I'm looking forward to our joint project.