Understanding the USA better: A mosaic comparing US states and EU countries – analysis of economic structures – Image: Xpert.Digital

Economic Analogies: A Comparative Analysis of the Economic Structures of US States and EU Nations

Introduction: The USA as a mosaic of economies

For European business and political leaders, a deep understanding of the US economy is of crucial strategic importance. However, a widespread misconception is to view the United States as a single, homogeneous economic unit. This perspective overlooks the fundamental reality: the US is a federation of 50 distinct, often competing and complementary economic regions, each with its own strengths, specializations, and regulatory frameworks. The true economic power and dynamism of the US only become apparent when analyzed at the state level. Some of these states have gross domestic products (GDPs) that exceed those of major nation-states and effectively operate as independent global economic powers.

This article aims to demystify this complexity for a European audience. The methodology deliberately goes beyond a simple comparison of GDP figures. Instead, a multidimensional, comparative analysis is conducted, taking the following aspects into account:

- Sectoral composition of GDP: The relative importance of services, industry and agriculture.

- Specialization in key industries: Focusing on sectors such as technology, energy, finance, or advanced manufacturing.

- Structure of the industrial base: The relationship between global corporations and a robust medium-sized business sector.

- Logistics infrastructure and trade orientation: The role as a trade hub, the quality of ports, airports and land transport.

- Regulatory and tax framework: The specific political and legal factors that shape the business climate.

This approach avoids the illusion of a direct one-to-one correspondence. It is rare for a US state to be an exact mirror image of a single EU country. Rather, the states are analyzed as economic hybrids that can combine characteristics of several European nations. California, for example, combines Germany's technological innovation and industrial scale with France's excellence in agricultural and wine production and Italy's global dominance in the cultural and entertainment industry. Texas, in turn, reflects the Netherlands' role as an energy and logistics hub, but also shows parallels to Poland's industrial rise as an attractive investment location.

This multi-perspective approach aims to paint a nuanced and strategically useful picture of the US economic landscape. Understanding these subnational ecosystems is key to accurately identifying the opportunities and challenges presented by the American market and to developing effective strategies for investment, expansion, and policy cooperation.

The global giants – California and Texas in the European mirror

At the forefront of the US economy are two states whose sheer size and global influence dwarf entire continents: California and Texas. Together, they generate almost a quarter of total US GDP and embody two distinct yet equally powerful models of American capitalism. Analyzing them in comparison to their European counterparts reveals fundamental structural similarities and profound differences that are essential for understanding the global economic architecture.

California: A nation within a nation

With a gross domestic product of $4.1 trillion in 2024, California, if it were an independent state, would be the fourth-largest economy in the world, closely following nations like Germany and Japan. This figure alone illustrates that the "Golden State" is not just a state, but a global economic and cultural giant. Its economic structure is highly developed, post-industrial, and strongly service-oriented.

Economic profile and sectoral composition

The Californian economy is dominated by a few, but extremely powerful, sectors. Finance and real estate lead the way, providing a stable foundation with an 18% share of GDP. However, the professional and business services sector (16%) and the information sector (14%) are far more dynamic and have a greater impact on the state's global image. These are largely driven by the technology and entertainment industries and are the primary sources of the state's impressive growth.

Although the manufacturing sector's share of GDP appears relatively small at 11%, this is a misleading metric. In absolute terms, this represents an industrial value added of over USD 400 billion, exceeding the industrial production of many industrialized nations. This manufacturing is highly technological and closely linked to the country's innovation clusters.

Industrial and Cultural Clusters: The Three Pillars of Power

California's unique economic strength is based on the concentration of three world-leading clusters:

Technology (Silicon Valley)

As the undisputed epicenter of the global digital economy, Silicon Valley is more than just an industrial cluster; it is an ecosystem that generates innovation at a pace that challenges the rest of the world. Companies like Apple, Google (Alphabet), Meta, and countless startups are defining the future of software, artificial intelligence, biotechnology, and digital platforms here. This sector is the primary driver behind the GDP contributions of "professional and business services" and the "information sector.".

Entertainment (Hollywood)

The film and entertainment industry, centered in Los Angeles, is another pillar of California's dominance. It is not only a direct economic driver, bringing an estimated $30 billion to California and directly supporting over 200,000 jobs, but also a source of immense soft power. Hollywood shapes global culture, sets trends, and is a massive tourist magnet. Government incentives, such as the film and television tax credit program, which has more than doubled to $750 million annually, cement this position. Sixteen recently funded television projects alone are expected to generate an economic impact of $1.1 billion.

Agriculture (Central Valley)

Often overshadowed by tech and entertainment, California agriculture is a global giant in its own right. With annual revenues of around $59 billion, the state is a powerhouse of food production, supplying over a third of the vegetables grown in the U.S. and three-quarters of the fruits and nuts. For certain products like almonds, California holds a de facto monopoly, supplying 100% of the U.S. commercial harvest and 80% of global production. This astonishing productivity, however, comes at a high price: The agricultural sector consumes about 40% of the state's total available water, making it extremely vulnerable in the face of climate change and recurring droughts.

Comparative analysis with the EU

California cannot be understood by comparing it to a single EU country. It is a hybrid, combining characteristics of several European heavyweights:

vs. Germany

The analogy to Germany lies in sheer economic power, technological leadership, and global export orientation. Both are centers of innovation. The crucial difference lies in the focus: While German strength traditionally stems from optimizing the physical world—automotive engineering, mechanical engineering, and the chemical industry—California draws its power from disruption and mastery of the digital world, i.e., from software, platforms, and data-driven business models.

vs. France

The parallel to France is striking when one considers the combination of a highly productive, value-added agricultural sector and a globally influential cultural industry. California's Central Valley, with its wine and specialty food production, is the American equivalent of the French wine regions. At the same time, Hollywood, with its global reach, reflects the cultural and economic significance of the French luxury goods and tourism industries.

vs. Italy

Similarities with Italy can be found in the strong regional specialization of industrial clusters. Just as Silicon Valley is synonymous with technology, northern Italian regions are known for mechanical engineering, fashion, and design. Both economies are characterized by a strong emphasis on design, branding, and high-quality consumer goods.

Comparative economic profile: California vs. Germany & France

Comparative economic profile: California vs. Germany & France – Image: Xpert.Digital

The comparative economic profile between California, Germany, and France reveals significant differences in the economic structure and orientation of the three regions. California has a nominal gross domestic product of approximately USD 4.103 billion, which falls between Germany's GDP of USD 4.745 billion and France's of USD 3.211 billion.

California's economic structure is heavily service-oriented, with the service sector accounting for an estimated 74 percent of GDP, while industry and agriculture have significantly smaller shares of 11 and 2 percent, respectively. Germany exhibits a more balanced structure with 70 percent services, but a considerably higher industrial share of 29 percent and an agricultural share of 1 percent. France has a similar distribution to Germany, with 69 percent services, 19 percent industry, and 2 percent agriculture.

California's main industries are dominated by technology (software and hardware), entertainment, financial services, agriculture, and biotechnology. Germany focuses on traditional industries such as automotive, mechanical engineering, chemicals, and electrical engineering. France, on the other hand, is characterized by aerospace, tourism, luxury goods, agriculture (with a focus on wine and dairy products), and the pharmaceutical industry.

The export structure reflects these industrial priorities. California primarily exports computers and electronics, transportation equipment, and agricultural products such as almonds, pistachios, and wine. Germany leads in motor vehicles and parts, machinery, and chemical products. France mainly exports aerospace technology, vehicles, pharmaceuticals, and luxury goods.

Particularly striking are the differing approaches to technology versus traditional industry. California is dominated by digital disruption, with traditional industries being redefined by technology. Germany has a strong traditional industrial base that uses digital technologies for optimization. France combines a strong traditional industry in sectors such as aviation and luxury goods with a growing technology sector.

Insights and strategic implications

The analysis of the Californian economy reveals two crucial insights for European actors.

First, the “scale trap” of perception. A sector like agriculture, which accounts for only about 2% of California’s GDP, is often underestimated in its global significance. However, the absolute value of this sector, amounting to between 50 and 80 billion USD, far exceeds the total agricultural production of many EU nations. For comparison, the entire Greek agricultural sector generates a GDP of approximately 16 billion USD. This means that even a niche sector in California can be a global market leader. European companies and policymakers must therefore not confuse percentage shares with absolute market size and power.

Second, the symbiosis and competition with Europe. California's economic model presents both a threat and an opportunity for Europe. The tech industry directly challenges traditional European sectors like the automotive industry, as demonstrated by the rise of Tesla, while German manufacturers lose market share. At the same time, these same European companies rely on Californian software, cloud infrastructure, and AI research to remain competitive. Similarly, the French luxury and cultural industries compete with Hollywood for global attention and budgets, while simultaneously leveraging Californian social media platforms as essential marketing channels. A purely confrontational or purely cooperative strategy toward California is therefore doomed to failure. European players must develop a hybrid strategy of "co-opetition"—a blend of cooperation and competition—to thrive in this complex environment.

Texas: The Energy and Trade Center

Texas, the "Lone Star State," represents a different, but no less impressive, American economic model. With a GDP of $2.7 trillion, it is the second-largest economy in the US and, as an independent nation, would be the eighth-largest in the world, ahead of countries like Canada, Russia, or Italy. While California draws its strength from the digital and cultural spheres, Texan power is based on control of physical resources and trade flows.

Economic profile and sectoral composition

Texas' economy has traditionally relied on its vast oil and natural gas reserves, which have made the state a global energy hub. Oil and gas exports alone reached $140 billion in 2023, supplemented by $70 billion from refined petroleum and coal products. Closely linked to this is the manufacturing sector, a cornerstone of the economy, contributing $241 billion to GDP (approximately 13% of total economic output). This sector is dominated by the petrochemical industry, but the manufacture of computers and electronic components is also enormously important, with exports worth $53 billion.

In recent years, Texas has undergone remarkable diversification. Its economy is increasingly expanding into sectors such as information technology, aerospace, defense, biomedical research, and renewable energy, particularly wind power.

Infrastructure, trade and regulatory environment

Texas is the undisputed export champion of the United States. With exports exceeding $440 billion in 2023, the state exports more than the next two largest states combined. This dominance is made possible by a world-class logistics infrastructure. The Port of Houston is the largest U.S. port by tonnage handled, and Dallas/Fort Worth International Airport is ranked among the best air freight hubs in the world. Texas's geographic location makes it a natural gateway for trade with Latin America, with Mexico being by far its largest trading partner.

A key factor in Texas' economic success is its regulatory environment. The state levies no income tax on individuals and maintains a decidedly business-friendly climate with minimal regulation. This has made Texas a magnet for companies relocating from other states and for new businesses, reflected in the highest number of Fortune 500 headquarters in the United States.

Comparative analysis with the EU

vs. Netherlands

This is the most apt European analogy. Both function as central energy and logistics hubs for their respective economies. Just as Texas supplies the US energy market with oil and gas and handles global trade through the Port of Houston, the Netherlands was historically Europe's gas hub and, with the Port of Rotterdam, the continent's largest, is the most important gateway for European trade. Both economies are extremely open and dependent on global trade. The Dutch trade ratio (exports plus imports as a percentage of GDP) of 166% underscores this extreme specialization in trade and logistics, a characteristic also found in the Texas economy.

vs. Poland

There are structural parallels regarding Poland's rise as an attractive location for foreign direct investment (FDI) in the manufacturing sector. Similar to Texas, Poland has attracted companies from more expensive and heavily regulated regions due to a favorable business climate, a large and skilled workforce, and a strategic location within its economic area (the EU). Both are experiencing dynamic economic growth, largely based on their success as competitive manufacturing locations.

Insights and strategic implications

The analysis of the Texas economy provides two fundamental insights for European strategy.

First, energy as a geopolitical tool and economic advantage. Texas' dominance in oil and gas production has helped the US achieve relative energy independence and become a net energy exporter. This contrasts sharply with the situation of many EU countries, particularly Germany, whose economies and geopolitical capabilities depend heavily on energy imports. The resulting lower energy costs in Texas represent a significant competitive advantage. For European energy-intensive industries (e.g., chemicals, steel), Texas is therefore not only a sales market but also increasingly a potential production location, offering protection against geopolitical energy risks and the opportunity to benefit from cost advantages.

Second, the “low-tax, low-regulation” model poses a direct challenge to the European social model. Texas’s immense success in attracting businesses and capital is based on an economic model diametrically opposed to the European approach. While EU countries like Germany and France finance their comprehensive social welfare systems through high taxes and dense regulation, Texas offers the opposite. The exodus of investment and corporate headquarters from Europe or other US states to Texas is a microcosm of global competition between economic systems. This represents a fundamental threat to the funding base of the European welfare state. European political and business leaders face the challenge of finding ways to maintain competitiveness without abandoning the social and environmental standards that define their societies.

🎯🎯🎯 Benefit from Xpert.Digital's extensive, five-fold expertise in one comprehensive service package | BD, R&D, XR, PR & Digital Visibility Optimization

Benefit from Xpert.Digital's extensive, five-fold expertise in a comprehensive service package | R&D, XR, PR & Digital Visibility Optimization - Image: Xpert.Digital

Xpert.Digital possesses in-depth knowledge across various industries. This allows us to develop tailored strategies precisely aligned with the requirements and challenges of your specific market segment. By continuously analyzing market trends and monitoring industry developments, we can act proactively and offer innovative solutions. The combination of experience and expertise generates added value and provides our clients with a decisive competitive advantage.

More information here:

From heavy industry to high-tech: America's structural transformation as a model for Europe?

Financial and service centers – New York and Florida

While California and Texas derive their global significance from technology, energy, and trade, the economies of New York and Florida are based on other, but equally powerful, pillars: the concentration of global capital and the attraction of people and services. They represent the vanguard of the American service economy and, compared with Europe, offer insightful perspectives on the workings of financial markets and demographically driven growth.

New York: Global Financial Capital

With a GDP of nearly $2.3 trillion, New York State is the third-largest economy in the United States and one of the largest in the world. The economy is overwhelmingly dominated by the New York City metropolitan area, and especially Manhattan, which is considered the undisputed global center for banking, finance, and communications.

Economic profile and sectoral composition

New York's economic structure is a prime example of a highly developed service economy. The financial and insurance sector is by far the most important sector, contributing over $315 billion to the state's GDP, which is roughly 29% of total economic output. While this sector does not employ the most people, it generates the highest value. Other massive service sectors follow: real estate and leasing at nearly $250 billion, the information sector at $195 billion, professional and technical services at $176 billion, and healthcare at $149 billion. Manufacturing plays a subordinate, but still substantial, role, contributing around $70 billion.

Structural duality: NYC vs. Upstate

The state's economy is characterized by a remarkable duality. On one side is the globalized, hyper-dynamic, and extremely service-oriented economy of New York City. On the other is the rest of the state, often referred to as "Upstate New York." These regions are economically more heavily reliant on traditional manufacturing, agriculture (particularly dairy, apples, and wine production in the Finger Lakes), and, more recently, investments in renewable energy sources such as solar and wind power. This division results in distinct economic realities and political priorities within the same state.

Comparative analysis with the EU

vs. Ireland / Luxembourg

The most obvious European analogy for New York's economic model can be found in the financial centers of Ireland and Luxembourg. All three have heavily relied on the financial sector as their central engine for economic growth. The crucial difference, however, lies in the source of their appeal. While Ireland and Luxembourg base their success as European financial hubs largely on highly favorable tax environments for multinational corporations, New York's dominance stems from the sheer size, depth, and liquidity of its capital markets. The New York Stock Exchange (NYSE) and the NASDAQ are the two largest stock exchanges in the world, both by market capitalization and trading activity. The scale is unparalleled: New York's financial and insurance sector alone (US$315 billion) generates almost as much as the entire gross domestic product of Ireland.

vs. Germany (Frankfurt) / France (Paris)

Although Frankfurt and Paris are important continental financial centers, they operate within a polycentric European financial system. Neither center possesses the singular global dominance of New York City. Wall Street is not just an American, but the global financial center, as evidenced by investment banking fees of approximately USD 55 billion in 2018.

Insights and strategic implications

Analyzing the New York economy leads to a key insight: the concentration of capital as a global power factor. The unprecedented concentration of capital, financial institutions, and specialized services in New York City gives the United States enormous, often underestimated control over global financial flows. Decisions about capital allocation, risk assessment, company valuations, and the development of new financial products made on Wall Street have direct and immediate repercussions for European companies, investors, and markets. European companies are not only clients of the New York financial system; they are also subject to its cycles, rules, and sentiments. This creates a strategic imperative for Europe to deepen and strengthen its own capital markets union. Only by creating a sufficiently large, liquid, and integrated European capital market can this structural dependence on a single non-European financial center be reduced in the long term.

Florida: Tourism, trade and demographic change

Florida, the "Sunshine State," has become the fourth-largest economy in the US, with a GDP exceeding $1.7 trillion. Its economic model is based on an attractive mix of services, trade, and relentless population growth, which serves as the primary engine of economic growth.

Economic profile and sectoral composition

Florida's economy rests on several strong pillars. The largest sectors are real estate and leasing (US$265.5 billion), professional and business services (US$208.3 billion), and health and social services (US$126.2 billion). However, tourism plays a prominent and defining role. In 2023, this sector contributed US$127.7 billion directly and indirectly to the state's economic output and supported over 2.1 million jobs, representing 14% of total non-agricultural employment. Visitor spending reached a record high of US$131 billion.

Other important economic sectors include international trade and banking. Miami, in particular, has established itself as the "gateway to Latin America" and is home to the largest concentration of international banks in the US, making it a major financial and trade center for the Western Hemisphere. Agriculture, especially the cultivation of citrus fruits and vegetables, also remains a significant economic factor.

Growth driver: The demographic factor

One of the most fundamental drivers of Florida's economic miracle is its strong and steady population growth. Unlike in many other regions of the Western world, this growth is fueled almost entirely by immigration—both from other US states and from abroad. This constant influx of new residents, workers, and retirees fuels dynamic domestic demand, particularly in the construction and real estate sectors, retail, and healthcare.

Comparative analysis with the EU

vs. Spain / Greece

The strongest analogy for Florida can be found in the major tourism nations of Southern Europe. The paramount importance of tourism to the overall economy is a common characteristic and a shared vulnerability. In Spain, tourism contributed approximately 15.6% to GDP in 2024. In Greece, the direct contribution was 13%, but the indirect and induced contribution is estimated at up to 33.7% of GDP. Similar to Florida, these economies are highly dependent on external shocks (such as pandemics, economic crises, or geopolitical uncertainties) that disrupt international travel. All three benefit from a warm climate, extensive coastlines, and highly developed tourism infrastructure.

vs. Cyprus / Malta

Smaller EU island states share parallels with Florida's role as a magnet for international capital, wealthy retirees, and service-oriented businesses. They attract visitors with a pleasant lifestyle, a favorable climate, and often advantageous tax conditions, making them popular destinations for a similar clientele to Florida.

Insights and strategic implications

The analysis of Florida highlights a crucial structural dynamic: demographics as the primary economic driver. While many European countries and even some traditional industrialized nations in the American Rust Belt face the challenges of a stagnant or shrinking population, Florida's economic growth is inextricably linked to its population growth. This process of "internal migration" within a large, integrated economic area like the USA acts as a powerful and self-reinforcing economic engine. New residents require housing, consume goods and services, and establish businesses, which in turn creates jobs and attracts even more people.

For Europe, where linguistic, cultural, and administrative barriers to intra-European migration are higher and mobility between member states is comparatively lower, this represents a structural disadvantage. Florida is a case study of how an attractive climate and a favorable business environment within a large single market can unleash demographic dynamics that lead to sustainable economic growth. Investors who invest in Florida are therefore implicitly betting on the continuation of this fundamental demographic trend.

America's Industrial Heart – The Rust Belt in Transition

The region in the northeastern and midwestern United States known as the "Rust Belt" was once the undisputed industrial center of the world. Shaped by coal, steel, and mass production, this region has undergone a profound and often painful structural transformation. However, states like Illinois, Pennsylvania, Michigan, and Ohio are far from being mere relics of a bygone era. They have transformed into highly diversified and technologically advanced industrial hubs whose economic structures and challenges bear remarkable parallels to the industrial heartlands of Europe.

Illinois & Pennsylvania: Diversified Industrial Powers in Structural Change

Illinois and Pennsylvania embody the successful, though not yet complete, transition from old heavy industry to a modern, knowledge-based economy. They are now diversified power centers that have maintained their industrial base while developing new strengths in services and technology.

Economic Profile of Illinois

With a GDP exceeding $1.1 trillion, Illinois is the fifth-largest economy in the United States. The economy is highly diversified and dominated by the Chicago metropolitan area, a global financial center and home to the world's largest futures exchange, the Chicago Mercantile Exchange. Beyond the financial sector, key pillars of the economy include manufacturing, agriculture, and a wide range of business services. Industry, encompassing sectors such as mechanical engineering, food processing, and chemicals, remains a central pillar, contributing approximately $137 billion to GDP. Outside of Chicago, the Corn Belt dominates the landscape, with corn and soybeans being the primary agricultural crops.

Economic profile of Pennsylvania

Pennsylvania's economy, the sixth largest in the US with a GDP of around $1 trillion, is a mosaic of modern and traditional sectors. The biggest drivers today are healthcare, real estate and leasing, and manufacturing. The latter remains an economic cornerstone, contributing over $113 billion (approximately 13% of GDP) and providing more than 562,000 jobs. Historically, the name Pennsylvania was synonymous with steel. While the dominance of the steel industry has waned, it remains a significant factor, contributing $8.5 billion directly to the value chain. However, the industrial base has broadened considerably and now includes chemicals, food processing, and advanced engineering.

Comparative analysis with the EU

vs. Germany (especially North Rhine-Westphalia)

The analogy between the American Rust Belt and Germany's Ruhr region is particularly apt. Both regions were the heartland of their nations' industrial revolutions, based on coal and steel. Both have undergone a profound structural transformation from heavy industry to a diversified economic landscape that now includes strong service, technology, and logistics components. Metropolises like Chicago and the Rhine-Ruhr region (Düsseldorf, Cologne) function as highly developed service and financial centers for their industrial hinterland. Both regions grapple with the demographic and environmental legacy of their industrial past but possess an immense industrial backlog, dense infrastructure, and a highly skilled workforce. One difference remains: the higher industrial density in Germany, where manufacturing accounts for approximately 18.5% of the national GDP, compared to about 12-14% in Illinois and Pennsylvania.

vs. Italy (especially Lombardy)

Another parallel can be found in comparison with Northern Italy. The combination of a strong financial center (Chicago or Milan) and a diverse industrial hinterland is a common characteristic. Italian industry is known for its clusters of highly specialized small and medium-sized enterprises (SMEs), which shows similarities to the diversified and often mid-sized manufacturing landscape in Pennsylvania and Illinois, which differs from the large-corporation-dominated states like Michigan.

Insights and strategic implications

The analysis of these states reveals a crucial development path: the journey from deindustrialization to re-industrialization. Illinois and Pennsylvania vividly demonstrate that the decline of traditional heavy industry need not spell the end of industrial significance. The successful shift toward advanced manufacturing, medical technology, logistics, and industry-related services is a model of high relevance for many of Europe's old industrial regions. This process shows that industrial strength can be maintained by shifting the focus from the mass production of basic materials to the manufacture of highly complex, knowledge-intensive goods. For European investors, this means that these states are not "rusting" relics, but rather markets in an advanced stage of economic transformation. The greatest opportunities no longer lie in the old heavy industry itself, but in the technologies and services that enable and drive this transformation—including automation, industrial software, advanced materials, and specialized logistics solutions.

Michigan & Ohio: The Automotive Axis and its Transformation

Michigan and Ohio form the historical and current center of the North American automotive industry. Their economies are so heavily reliant on this single sector that in Europe only the core automotive nations are comparable. Today, they stand at the heart of the greatest transformation in their history: the transition to electric mobility and autonomous driving.

Economic Profile of Michigan

Michigan's economy, with a GDP of approximately $719 billion, is inextricably linked to the automotive industry. The sector is not just a part of the economy; it's its very DNA. It is estimated that the automotive industry contributes up to $304 billion directly and indirectly to the state's economic output. The three major U.S. automakers—General Motors, Ford, and Stellantis (formerly Chrysler)—have their global headquarters here. Manufacturing is the largest sector by employment and contributes a substantial $99 billion to GDP. Crucially, Michigan is not just a factory, but also the brain of the U.S. auto industry: The state is the leading center for automotive research and development (R&D) in the U.S.

Ohio Economic Profile

Ohio's economy (GDP: $928 billion) is also heavily industrialized and closely linked to the automotive axis. Manufacturing is the largest single sector, contributing nearly one-fifth to the state's GDP. Within this sector, the production of motor vehicles and parts is one of the main activities, making Ohio an essential part of the North American automotive supply chain.

Comparative analysis with the EU

vs. Germany (especially Baden-Württemberg/Bavaria)

This is the most direct and powerful analogy in the entire report. The economic regions of Michigan/Ohio and Southern Germany are global twin clusters of the automotive industry. Both are characterized by the presence of world-renowned original equipment manufacturers (OEMs) and an extremely dense, highly specialized network of suppliers. Both are leaders in automotive R&D and face the absolutely identical, existential challenge of the transformation from the internal combustion engine to electromobility and autonomous driving. The sector's importance is comparable: In Germany, the automotive industry contributes around 5% to the national GDP, underscoring its immense economic role.

vs. Czech Republic / Slovakia

These countries can be considered the "workshops" of the European automotive industry. Their economies are extremely reliant on automobile production for foreign, mostly German, corporations. This reflects the dependency of many suppliers in Michigan and Ohio on the decisions of the "Big Three" in Detroit. Czech industry, for example, accounts for 37% of GDP, with the automotive industry being by far the largest and most important subsector.

Insights and strategic implications

The analysis of these automotive clusters leads to a profound realization: a shared destiny in the global transformation. The future of the economic regions of Michigan/Ohio on the one hand and Southern Germany/Czech Republic on the other hinges on the answer to the same question: Who will win the technological race for the future of mobility? Success or failure in one of these clusters will have direct and unavoidable repercussions for the other. The rise of new competitors like Tesla in the US or Chinese manufacturers in Europe threatens the established players in both regions equally.

This is not simply a competitive situation, but a global race with distributed fronts and complex interconnections. A breakthrough in battery technology in Michigan could have been developed by a German supplier. A failure by German OEMs to develop competitive software for their vehicles could pave the way for US tech companies to become either indispensable partners or overwhelming competitors. For European investors and companies, this means that a strategy focused solely on one region is risky. Instead, they must focus on the technological winners along the entire global value chain, regardless of their geographical origin. Cross-Atlantic cooperation, for example between German mechanical engineering companies and American software startups, is not a sign of weakness, but a strategic necessity to survive in this global battle for transformation.

Our recommendation: 🌍 Limitless reach 🔗 Connected 🌐 Multilingual 💪 Sales power: 💡 Authentic with strategy 🚀 Innovation meets 🧠 Intuition

From local to global: SMEs conquer the world market with a clever strategy - Image: Xpert.Digital

In an era where a company's digital presence determines its success, the challenge lies in creating an authentic, personalized, and far-reaching presence. Xpert.Digital offers an innovative solution that positions itself as the intersection of an industry hub, a blog, and a brand ambassador. It combines the advantages of communication and sales channels in a single platform and enables publication in 18 different languages. Cooperation with partner portals and the ability to publish articles on Google News and a press distribution list with approximately 8,000 journalists and readers maximize the reach and visibility of the content. This represents a crucial factor in external sales and marketing (SMarketing).

More information here:

Why European investors are focusing on the wrong American states

Agriculture and Specialized Manufacturing – The Midwest & the Pacific Northwest

Beyond the global financial, tech, and industrial centers lie economic regions whose strength rests on deep specialization in agriculture or a unique combination of high technology and traditional industry. Midwestern states like Iowa and Nebraska form the breadbasket of America and a center of food processing, while Washington State in the Pacific Northwest represents a fascinating dual powerhouse of software and aerospace.

Iowa & Nebraska: The Breadbasket and its Processing

Iowa and Nebraska are the heart of the American "Corn Belt." Their economies are a prime example of highly efficient, industrialized agriculture that extends far beyond primary production and reaches deep into the manufacturing and financial sectors.

Iowa Economic Profile

Iowa's economy (GDP: $261 billion) is fundamentally shaped by agriculture and related industries. Although agriculture itself contributes "only" 6.8% to direct GDP, its indirect impact is enormous: Together with upstream and downstream sectors, agriculture generates over 22% of the state's total economic output and provides nearly one in five jobs. The largest single sector by GDP contribution is manufacturing, at 17.2%, which consists largely of food processing, agricultural machinery manufacturing, and agrochemicals. Iowa is one of the leading U.S. producers of corn, soybeans, pork, and eggs, and a center for ethanol production.

Economic Profile of Nebraska

Nebraska's economy (GDP: $141 billion) follows a similar pattern. Agriculture is the dominant economic sector, providing more than 40% of jobs in over half of the 93 counties. The most important agricultural products are beef, corn, and soybeans. Interestingly, however, as in Iowa, agriculture itself is not the largest contributor to GDP, but rather the financial and insurance sector at $19.3 billion, closely followed by manufacturing at $17.8 billion.

Comparative analysis with the EU

vs. France (agricultural sector)

France is considered the agricultural powerhouse of the European Union, much like the Midwest is for the USA. Both regions produce enormous quantities of staple foods such as grain and have a strong livestock industry. A significant difference, however, lies in their relative importance to the overall economy: while agriculture forms the foundation of the entire economic structure in Iowa and Nebraska, the French agricultural sector contributes only 1.9% to the national GDP, highlighting the considerably greater diversification of the French economy as a whole. The absolute production value of French agriculture in 2023 was €95.5 billion, illustrating the scale of this industry.

vs. Denmark

A fitting analogy can be found in Denmark. Both economic regions combine a highly efficient, technology-driven and export-oriented agriculture (especially in pig production) with a strong industry for agricultural machinery, food processing and agricultural biotechnology.

Insights and strategic implications

The analysis of Iowa and Nebraska reveals an often overlooked but crucial economic structure: the invisible interrelationship between the primary and tertiary sectors. At first glance, it seems paradoxical that in these agrarian states, the financial and insurance sectors are among the leading contributors to GDP. However, this is not a sign of diversification away from agriculture, but rather a symptom of their extreme modernization and complexity.

Modern, industrialized agriculture is a highly capital-intensive and high-risk business. It requires specialized financial products to insure against crop failures (crop insurance), the volatility of commodity prices (commodity futures exchanges like those in Chicago), the financing of expensive agricultural machinery, and investment in biotechnology. The strong financial and insurance clusters that have developed in cities like Des Moines, Iowa, and Omaha, Nebraska, are a direct response to this need. Their strength is inextricably linked to the strength and capital requirements of the agricultural sector. For European actors, this means that engaging in these countries requires a deep understanding of the entire agricultural value chain—from seed to harvest and processing, and on to financing and insurance.

Washington: A dual powerhouse of technology and traditional industry

The state of Washington (GDP: USD 847 billion) on the Pacific coast is a fascinating economic hybrid that combines two seemingly opposing worlds: the digital future and traditional heavy industry.

Economic profile

Washington's economy is dominated by two global giants from two different eras. On one side are the tech companies of the Seattle metropolitan area, most notably Microsoft and Amazon. They are the driving force behind the strong information sector and professional services, making Washington one of the world's leading centers for software development, cloud computing, and e-commerce. On the other side is the legacy of the industrial aerospace sector, embodied by Boeing. Although the company faces challenges, the region remains a global center for aircraft manufacturing and its associated highly specialized supply chain. This dual structure is complemented by significant sectors such as agriculture (apples, wine), forestry, and one of the most important ports on the US West Coast (Port of Seattle/Tacoma), which is a crucial gateway for trade with Asia.

Comparative analysis with the EU

vs. Ireland

The strongest European parallel to Washington's tech sector can be found in Ireland. The Irish economy is exceptionally dominated by a handful of large, global US-based technology companies that maintain their European headquarters there. The technology sector contributes around 13% to Ireland's GDP, making the country extremely export-oriented. Both Washington and Ireland are heavily dependent on the global strategies and success of these few multinational corporations for their economic development and stability. This creates enormous growth and highly skilled jobs, but also significant structural dependency.

vs. Finland

Another interesting analogy can be found in Finland. Similar to Washington, Finland combines a strong, internationally oriented technology and ICT sector (historically shaped by Nokia) with traditionally important, resource-based industries such as forestry and paper. Both economies have proven their ability to build world-class capabilities in both digital and physical goods production.

The economy of Washington State demonstrates how a region can simultaneously be at the forefront of the digital revolution and a leader in a traditional, capital-intensive industry. This dual strength makes the economy resilient, but it also creates complex dependencies and requires policies that can balance the needs of very different sectors.

Synthesis and strategic conclusions for European actors

A detailed analysis of individual US states and their European counterparts paints a picture of a US economy that is far more complex, diverse, and dynamic than a purely national perspective would suggest. Instead of a monolithic block, a mosaic of highly specialized, sometimes competing, sometimes complementary economic regions emerges. This granular perspective yields crucial strategic conclusions for European companies, investors, and policymakers.

Summary of analogies and divergences

The comparison has shown that the US economy is characterized by three main features:

- Extreme scale: States like California and Texas, with their trillion-dollar economies, operate on a scale that surpasses that of most nation-states. Even their niche sectors can overshadow the overall economies of smaller EU countries.

- Deep specialization: States such as Michigan (automotive), Iowa (agriculture) or New York (finance) exhibit an extreme concentration on specific industries, leading to deep value chains and highly specialized ecosystems.

- High dynamism: Driven by factors such as demographic growth (Florida) or a business-friendly regulatory environment (Texas), many US states exhibit growth dynamics that are less common in the more mature economies of Europe.

In comparison, while the economy of the European Union is of a similar size overall, its structure is different. It is more polycentric, more fragmented by national borders, more comprehensively regulated, and characterized by welfare state models. Its strength lies less in the disruptive power of individual giants than in the excellence of highly specialized, often medium-sized, niche sectors, such as German mechanical engineering, northern Italian manufacturing, or the French luxury goods industry.

Identifying overarching trends and their implications

The analysis reveals three overarching trends that define the relationship between the US and European economies:

- Regulatory arbitrage and domestic competition: Within the US, companies can choose locations based on very different regulatory and tax frameworks. A company can leverage California's high talent density and innovative capacity while simultaneously relocating production facilities to tax-friendly Texas. This intense domestic competition is a form of "regulatory arbitrage" that does not exist in the EU due to the more harmonized, though not identical, frameworks and the lower mobility of companies and workers. This gives the US economy as a whole greater flexibility and adaptability.

- Energy independence versus energy dependence: The fundamental contrast between energy-self-sufficient states like Texas and industrialized nations like Germany, which are heavily dependent on energy imports, represents a crucial strategic difference. The availability of cheap and abundant energy in parts of the USA is not only a cost factor but also a geopolitical advantage that increasingly influences investment decisions. For European companies in energy-intensive industries, relocating production capacity to the USA is becoming a strategic option for minimizing risk.

- Technological disruption and dependency: The concentration of global digital disruptive power in a few US states, primarily California and Washington, poses a systemic challenge for Europe's traditional industries. Whether in automotive, mechanical engineering, or the media sector, European companies face a dual reality: They compete with the new digital giants while simultaneously being dependent on their platforms, software, and infrastructure. This "co-opetition" requires complex strategies that go beyond simple partnership or competition models.

Strategic Recommendations

Based on these findings, concrete strategic recommendations can be derived for European actors:

- For investors: Instead of investing indiscriminately "in the USA," portfolios should be based on a granular, country-specific analysis. For example, an investment in the established German automotive supplier industry could be diversified and hedged by targeted investments in the emerging ecosystem for electromobility and battery technology in Michigan or in the Southern "Auto Belt." Similarly, an exposure to the European luxury goods sector could be complemented by investments in the Californian entertainment and media industry, which helps shape global trends and distribution channels.

- For businesses: Location decisions in the US must be based on a thorough analysis of state and regional ecosystems. A logistics company will assess the conditions in Texas, Illinois, or Ohio differently than a biotech company, for which proximity to research clusters in Massachusetts or California is crucial. An agrotechnology company will find an ideal environment in Iowa or Nebraska. A one-size-fits-all US strategy is doomed to failure.

- For policymakers: The European Union and its member states should not treat the US as a monolithic bloc, but rather pursue a differentiated foreign economic policy. This means seeking targeted economic, technology, and research partnerships with individual states or regional clusters that possess complementary strengths. A dialogue on regulatory standards in the field of AI might be more fruitful with California than with the federal government in Washington, D.C. Cooperation in the area of advanced manufacturing could be specifically sought with the governors of the Rust Belt.

In summary, understanding the United States as a mosaic of economies is not merely an academic exercise, but a strategic necessity. Only those who know the specific strengths, weaknesses, and economic logics of California, Texas, New York, and their counterparts can fully exploit the opportunities of the American market and effectively manage its risks.

Detailed comparison tables

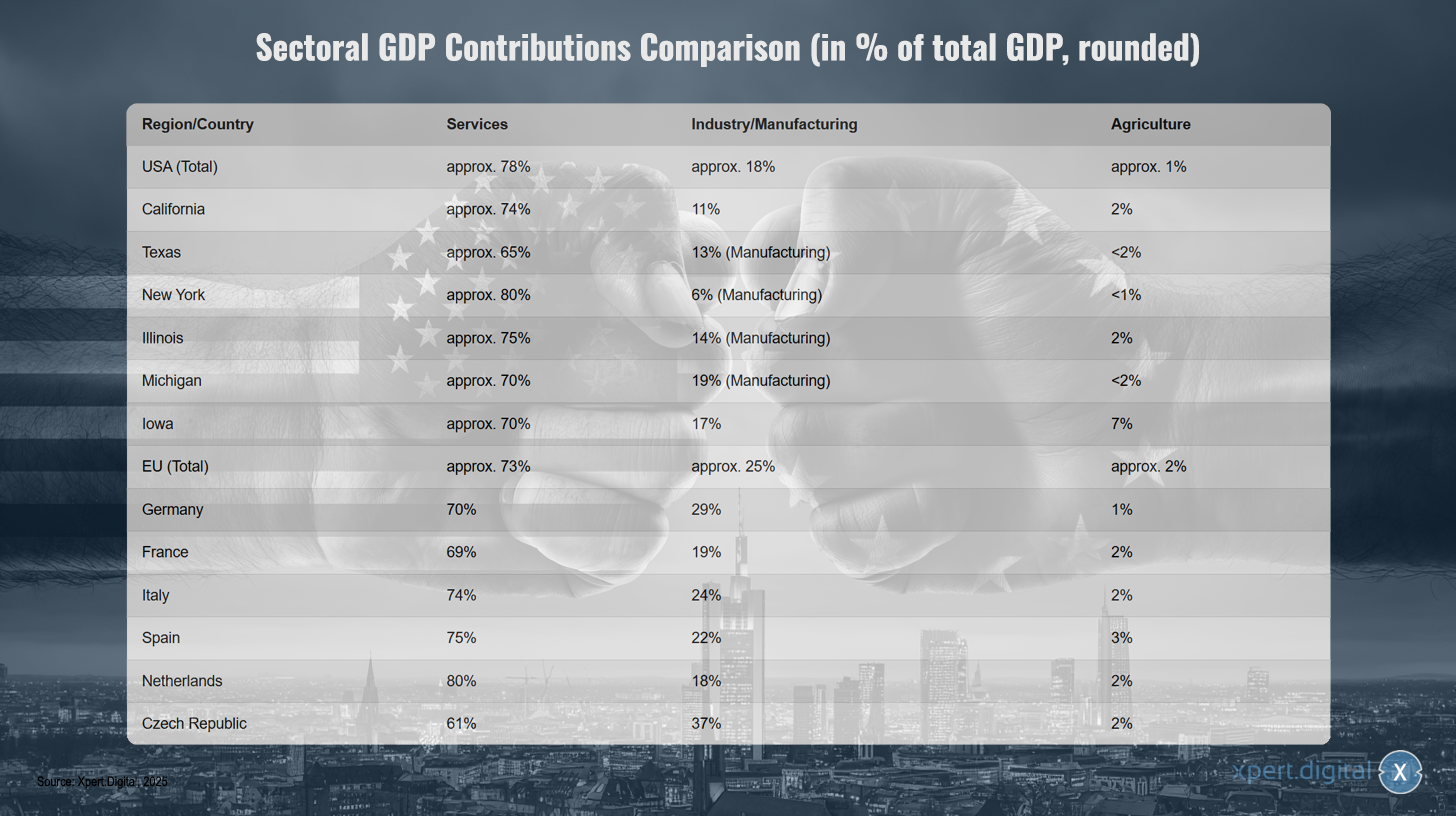

Comparison of sectoral GDP contributions (in % of total GDP, rounded)

Sectoral GDP contributions in comparison (in % of total GDP, rounded) – Image: Xpert.Digital

The sectoral GDP contributions reveal significant regional differences in economic structure. In the US, the service sector dominates, contributing approximately 78% of total GDP, while industry and manufacturing account for roughly 18%, and agriculture only about 1%. California exhibits a similar structure, with services accounting for 74%, industry for 11%, and agriculture for 2%. Texas shows a slightly stronger industrial focus, with services accounting for 65%, manufacturing for 13%, and agriculture for less than 2%. New York is particularly service-oriented, with 80% of its GDP coming from this sector, manufacturing for only 6%, and agriculture for less than 1%. Illinois achieves 75% from services, 14% from manufacturing, and 2% from agriculture, while Michigan has an above-average industrial share, with 70% from services and 19% from manufacturing. Iowa differs significantly from other US states, with 70% from services, 17% from industry, and a remarkable 7% from agriculture.

In the EU, services account for approximately 73% of the economy, industry around 25%, and agriculture about 2%. Germany demonstrates a strong industrial base with 70% services, 29% industry, and 1% agriculture. France achieves 69% services, 19% industry, and 2% agriculture. Italy has 74% services, 24% industry, and 2% agriculture, while Spain shows a similar structure with 75% services, 22% industry, and 3% agriculture. The Netherlands is particularly service-oriented with 80% services, 18% industry, and 2% agriculture. The Czech Republic stands out with the highest share of industry of all the listed countries, at 61% services, 37% industry, and 2% agriculture.

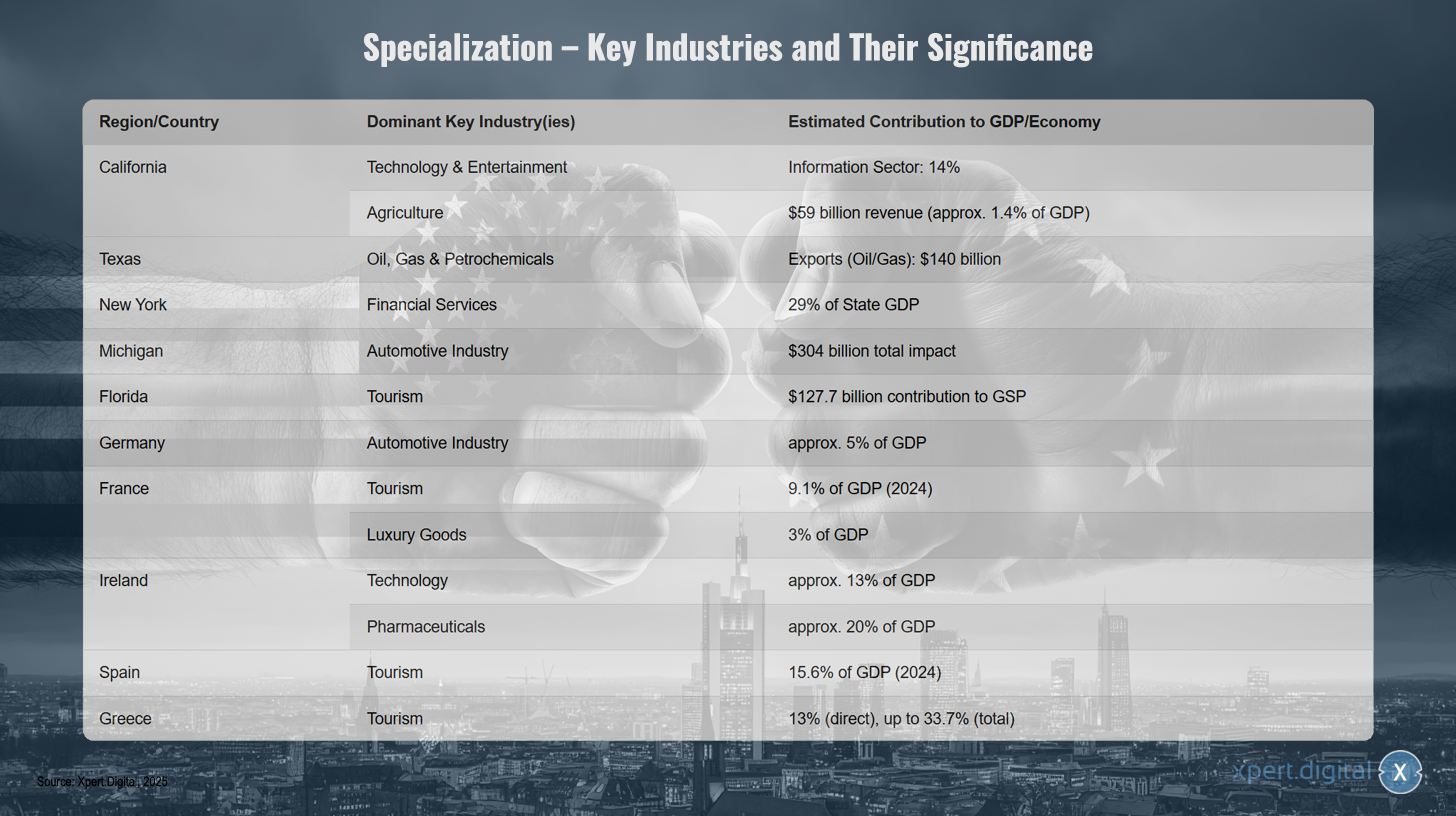

Specialization – Key Industries and Their Importance

Specialization – Key Industries and Their Importance

The specialization of different regions and countries in specific key industries reveals distinct economic strengths. California dominates with technology and entertainment, with the information sector contributing 14% to GDP, while agriculture generates $59 billion in revenue, representing approximately 1.4% of GDP. Texas focuses on oil, gas, and petrochemicals, with exports worth $140 billion. New York is heavily reliant on financial services, which account for 29% of the state's GDP. Michigan is synonymous with the automotive industry, generating a total impact of $304 billion, while Florida benefits from tourism, which contributes $127.7 billion to its GDP.

At the international level, Germany also has a strong presence in the automotive industry, which accounts for approximately 5% of its GDP. France relies on tourism, with 9.1% of its GDP projected for 2024, and luxury goods, with 3%. Ireland specializes in both technology, with approximately 13% of its GDP, and pharmaceuticals, with about 20%. Spain is heavily dependent on tourism, with 15.6% of its GDP projected for 2024. Greece shows the greatest dependence on tourism, with a direct contribution of 13% to its GDP, rising to as much as 33.7% when considering the overall impact.

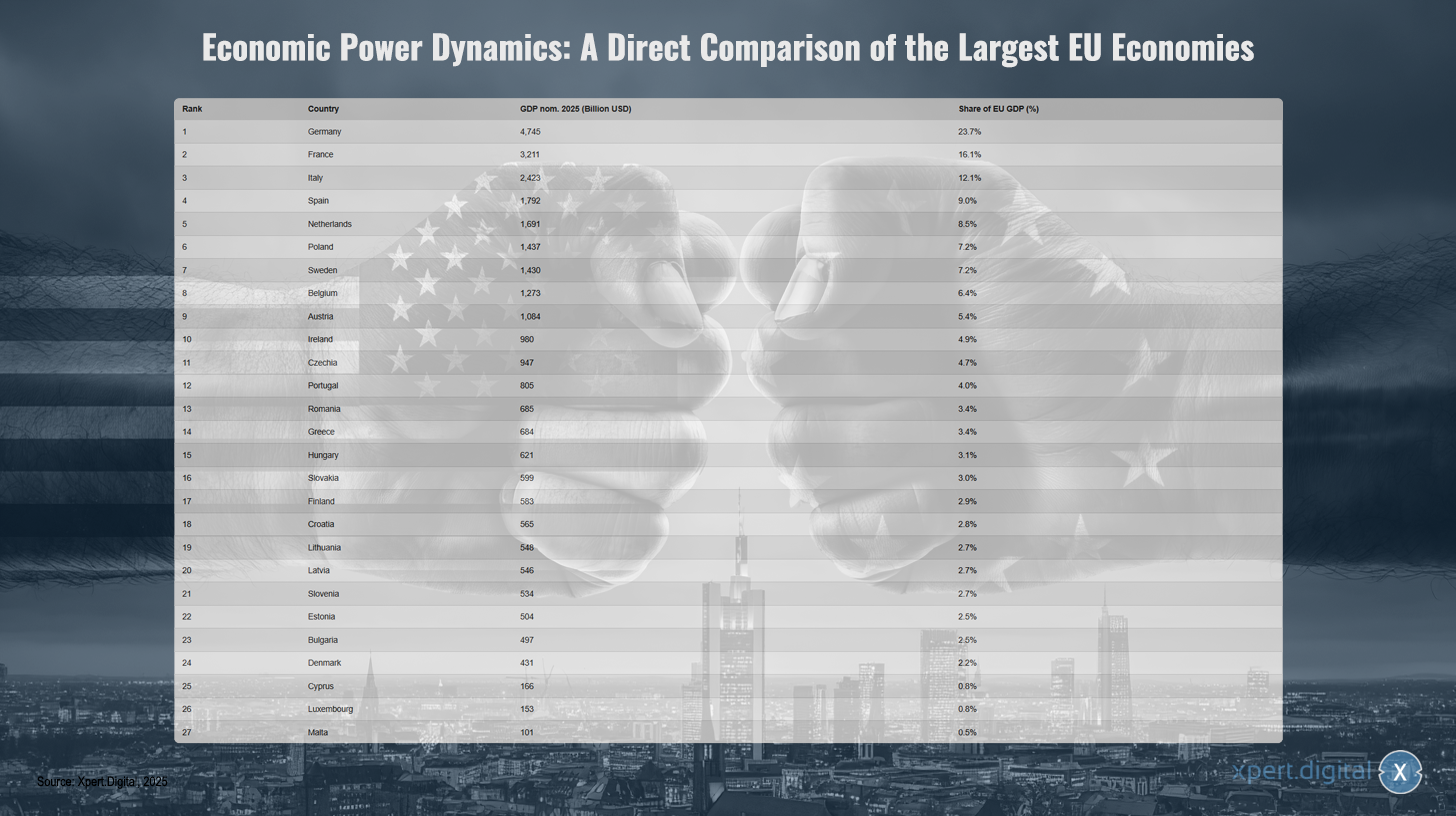

Economic power dynamics: A direct comparison of the largest EU economies

Economic power dynamics: A direct comparison of the largest EU economies – Image: Xpert.Digital

The economic balance of power within the European Union is largely determined by a few countries. With a nominal gross domestic product (GDP) of US$4,745 billion in 2025, Germany is clearly the strongest economy in the EU, contributing 23.7 percent to the total EU GDP. France follows with a GDP of US$3,211 billion and a share of 16.1 percent. Italy ranks third with US$2,423 billion and a share of 12.1 percent, followed by Spain (US$1,792 billion; 9.0 percent) and the Netherlands (US$1,691 billion; 8.5 percent). Poland, Sweden, and Belgium also make significant contributions to European economic output, each with a GDP exceeding US$1,200 billion and shares between 6.4 and 7.2 percent. Austria, Ireland, and the Czech Republic occupy the middle ground with GDPs between US$947 billion and US$1.084 trillion and shares between 4.7% and 5.4%. The remaining countries, including Portugal, Romania, Greece, Hungary, Slovakia, Finland, Croatia, Lithuania, Latvia, Slovenia, Estonia, Bulgaria, and Denmark, each have GDP shares below 4.5%. The smaller economies of Cyprus, Luxembourg, and Malta together account for less than two percent of total EU GDP. This distribution underscores the significant economic heterogeneity within the European Union, with the six largest economies already representing more than two-thirds of total economic output.

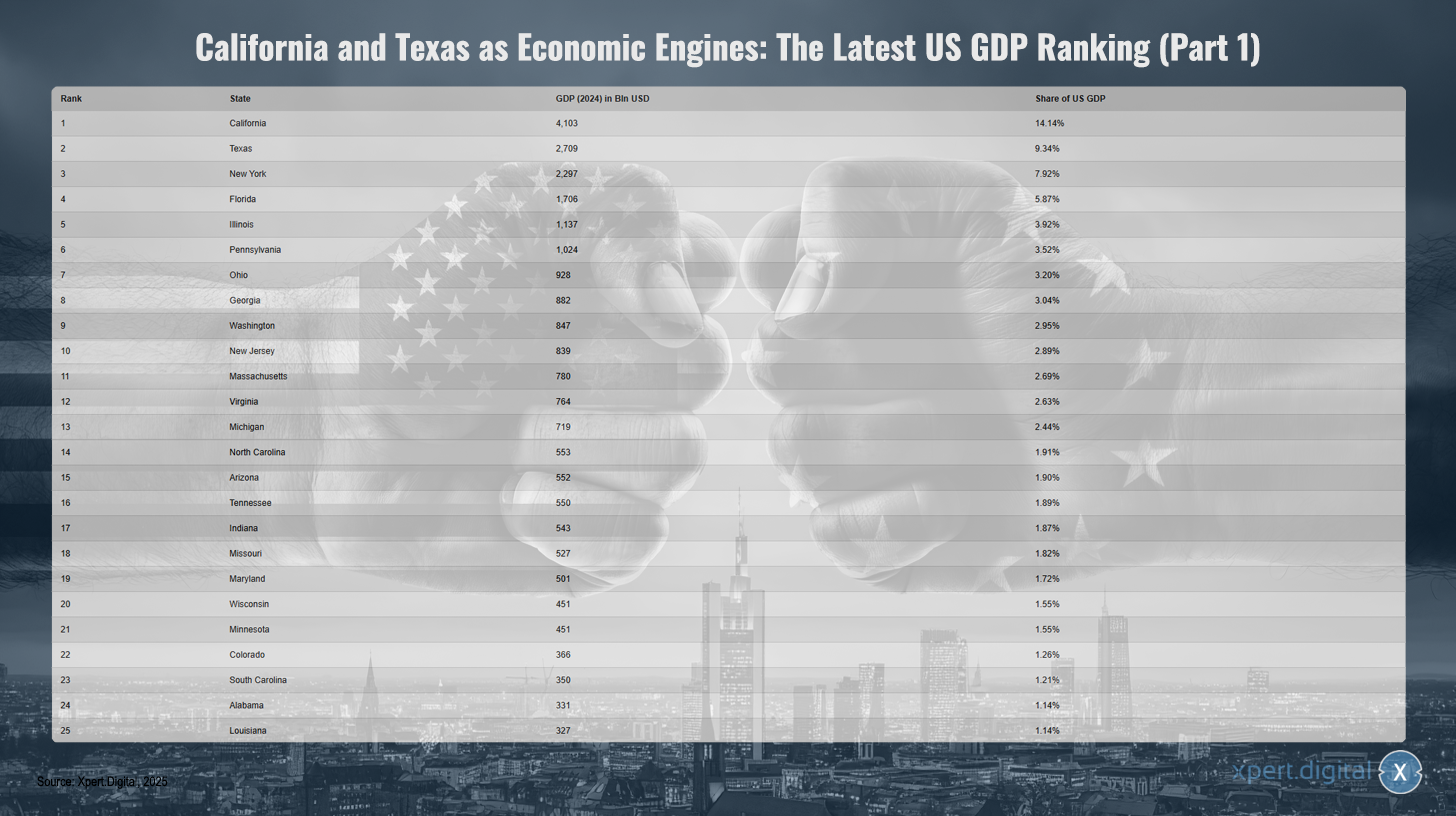

California and Texas as economic engines: The current US GDP ranking

California and Texas as economic engines: The current US GDP ranking (Part 1) – Image: Xpert.Digital

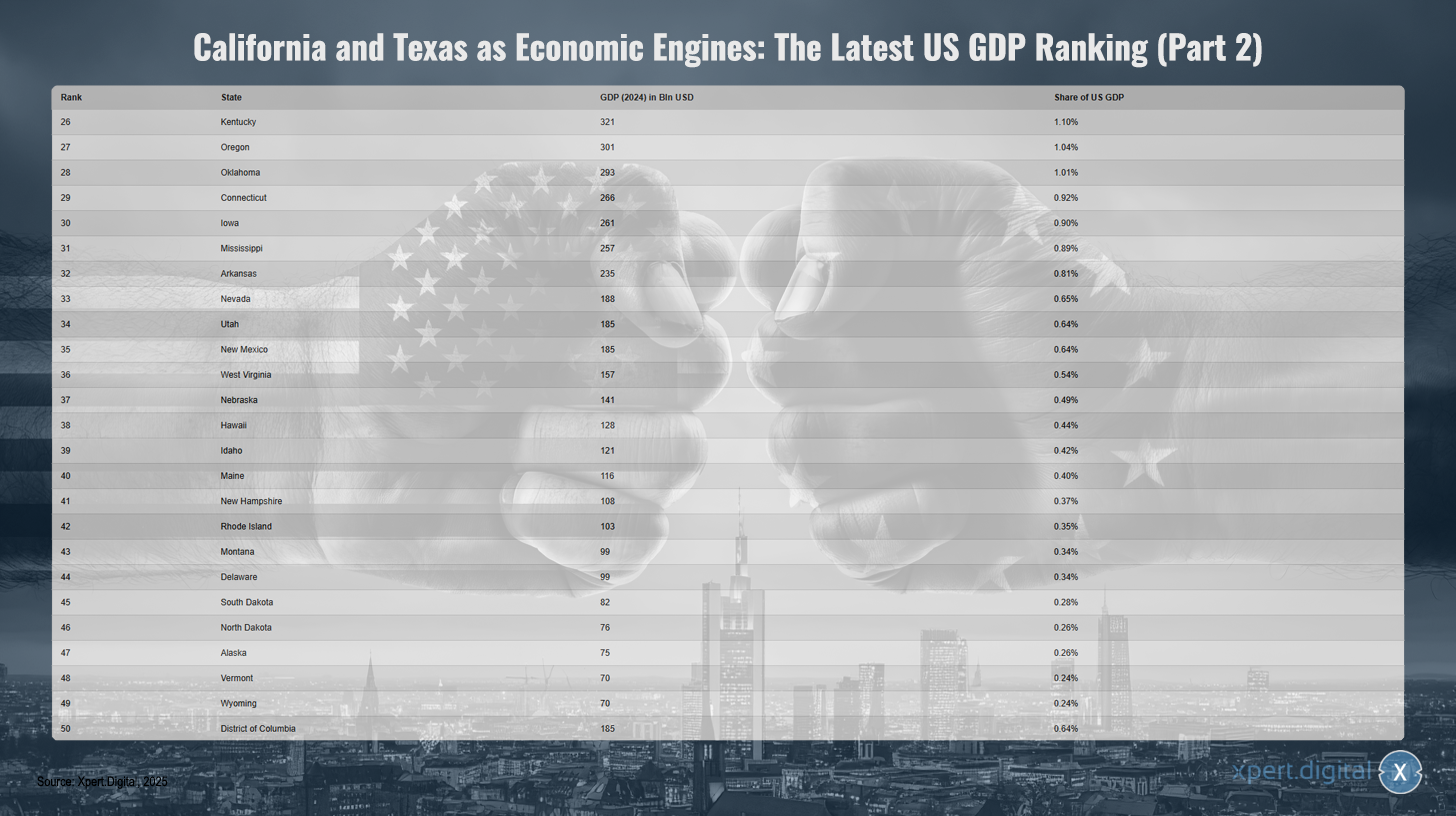

California and Texas are considered the most important economic engines of the USA. In the current GDP ranking of US states for 2024, California takes first place with a gross domestic product of $4.103 trillion, contributing 14.14% to the total economic output of the United States. Texas follows with $2.709 trillion and a share of 9.34%. New York is in third place with $2.297 trillion and 7.92%. Florida follows with $1.706 trillion (5.87%) and Illinois with $1.137 trillion (3.92%). Other economically strong states are Pennsylvania, Ohio, Georgia, Washington, and New Jersey, each contributing between $780 trillion and $1.024 trillion to US GDP. The remaining positions are occupied by states such as Massachusetts, Virginia, Michigan, and North Carolina. The GDP of the remaining states is sometimes significantly lower, although even at the bottom of the list – such as Vermont or Wyoming – respectable economic output is still achieved despite a small share of the total GDP. The enormous economic weight of the leading states compared to the numerous smaller states is striking, underscoring the strong concentration of economic power within the USA.

California and Texas as economic engines: The current US GDP ranking (Part 2) – Image: Xpert.Digital

XPaper AIS - R&D for Business Development, Marketing, PR and Content Hub

XPaper AIS application possibilities for business development, marketing, PR and our industry hub (content) - Image: Xpert.Digital

This article was handwritten. I used my self-developed R&D research tool, 'XPaper,' which I primarily use for global business development in a total of 23 languages. Stylistic and grammatical refinements were made to make the text clearer and more fluid. Topic selection, drafting, and the collection of sources and materials are all handled by an editorial team.

XPaper News is based on AIS (Artificial Intelligence Search) and differs fundamentally from SEO technology. However, both approaches share the goal of making relevant information accessible to users – AIS on the search technology side and SEO on the content side.

Every night, XPaper sifts through the latest news from around the world with continuous, round-the-clock updates. Instead of investing thousands of euros monthly in cumbersome and generic tools, I've created my own tool to stay up-to-date in my work in Business Development (BD). The XPaper system is similar to tools used in the financial sector, which collect and analyze tens of millions of data points every hour. At the same time, XPaper isn't just for business development; it's also used in marketing and PR – whether as a source of inspiration for the content factory or for article research. The tool allows you to evaluate and analyze all sources worldwide. No matter what language the data source speaks, it's no problem for the AI. Various AI models are available for this purpose. The AI analysis quickly and clearly generates summaries that show what's currently happening and where the latest trends lie – and XPaper offers this in 18 languages. XPaper allows for the analysis of independent subject areas – from general to specific niche topics, in which data can be compared and analyzed with past periods, among other things.

We are here for you - Consulting - Planning - Implementation - Project Management

☑️ Our business language is English or German

☑️ NEW: Correspondence in your native language!

Konrad Wolfenstein

I and my team are happy to be available to you as your personal advisor.

You can contact me by filling out the contact form here wolfenstein@xpert.digital:or simply call me at +49 7348 4088 965. My email address is

I'm looking forward to our joint project.