New logistics strategies, including digital twins and artificial intelligence (machine learning) – Image: Xpert.Digital / KeyFame|Shutterstock.com

In 2011, the German Language Society (GfdS) chose "Stresstest" as its word of the year. It refers to a test that measures resilience and the associated, increasing physical or psychological stress of a reaction to an event. It gained wider recognition through media coverage in connection with stress tests conducted at nuclear power plants, interim storage facilities, as well as at banks and the Stuttgart 21 railway project.

A crisis plan for the economy?

Interestingly, a so-called national pandemic plan for Germany was first published in 2005 and last updated in March 2017. It was the response to the SARS pandemic of 2002/2003 and the global spread of H5N1. In addition to measures against the spread of a pandemic pathogen, it was also intended to maintain the country's infrastructure.

With regard to influenza, the World Health Organization (WHO) has stipulated in its guidelines on Pandemic Influenza Risk Management, last revised in May 2017, that the Director-General of the WHO declares a pandemic – that is, the transition from an epidemic to a pandemic.

However, potential scenarios for a collapse of global supply chains, as well as a corresponding international set of measures to mitigate and bridge the global consequences, have so far failed to materialize. The COVID-19 pandemic brought to a halt the supposedly golden age of globalization, which had been driven forward with an ostrich-like approach. Even ecologically contradictory aspects were pushed into the background. Any objective stress test would have highlighted the sensitive nature of supply chains and their ecological vulnerabilities.

With growing environmental awareness (reducing greenhouse gas emissions) and the outbreak of the coronavirus pandemic, it is now clear to everyone that things cannot continue as they are. While some still hoped that the pandemic would quickly resolve itself like an annual flu season, we are now already in the second year of the pandemic, and a possible solution beyond the third year is still not in sight.

Example: steel and aluminum

Even though supply chains were temporarily disrupted here and there and raw materials for further processing were lacking, national and international logistics have so far coped quite well with the crisis. However, this has also impacted prices. Many goods and raw materials have become expensive or are experiencing long delivery times. For example, steel and aluminum prices skyrocketed, which also had a negative impact on the expansion of renewable energies. In September 2021, the price of aluminum reached its highest level in the eight-year observation period.

The steel industry has always been one of the most important key industries, upon which many other industries depend. Steel is therefore a crucial indicator of economic and cyclical developments. Even though prices are currently trending downwards, further developments and the impact of the 0micron variant of the coronavirus pandemic remain unclear.

This is not what a strategy and planning certainty look like. In short, the pandemic is exposing the fragility of our global supply chain. It is becoming increasingly clear that supply chains are the weakest link in globalization and the global economy, and we need to develop new logistics strategies. They have failed the acute stress test.

Now is the time to seize the opportunity and bring the supply chain back to Europe

Okay, production and labor costs are lower in China than in Germany. And it's obvious that products with many individual parts and work steps, such as smartphones, cannot currently be produced competitively in Germany. But what good is this advantage to me if, as is currently the case, transport costs for container ships are skyrocketing and then the goods are either delivered late or are currently unavailable?

At the latest when the 400-meter-long and 59-meter-wide freighter "Ever Given" ran aground in the Suez Canal in March 2021, it should have been clear to everyone that there was a critical point in the global supply chain. Essentially, a flaw or bug in the system. The repercussions before such a global supply chain management system gets back on track or functioning reasonably well again can take weeks. However, during the COVID-19 pandemic, disruptions in the global supply chain increased, making it difficult for supply chain management to adapt and react flexibly.

On the other hand, potential risks of a “disruption in the supply chain” were not entirely unknown. As early as 2015, DHL conducted a “Risk & Resilience” study on resilient logistics. While a potential pandemic was not explicitly mentioned, the study did address cyberattacks, protectionism, and political escalations, which represent an additional and real potential for disruption, on the same or even greater scale as the current coronavirus pandemic.

Approximately 12% of global freight and roughly 30% of the world's containers pass through the Suez Canal. This makes the Suez Canal the most important waterway in the world, ahead of the Panama Canal.

Container prices have now risen sharply, in some cases by 500% or more compared to last year. Demand for container deliveries has skyrocketed because passenger air travel, which was a primary mode of transport for some goods, has virtually ceased. It is assumed that air freight options will not recover quickly.

This, in turn, leads to congestion at American and European ports. In November, 400 to 500 container ships were anchored at their destinations, and due to high demand for containers coupled with a lack of port personnel, they could only be processed slowly. This, in turn, means that the containers are needed for longer periods, and consequently, container prices have risen again. In short: there is a container shortage.

German companies want to change their supply chains. Already 68% of the affected companies have initiated corresponding measures to get the situation under control as quickly as possible:

- 47% are looking for new or additional suppliers

- 41% want to increase storage capacity

- 22% distribute suppliers across multiple countries

- 12% are working on shortening delivery routes

- 11% are planning to relocate production to their own company

Source: DIHK, Going Global 2021

Global Logistics – Resilient Logistics

Resilient Logistics – Akintevs & Vit-Mar | Shutterstock.com

A survey conducted in March 2020 among 2,900 respondents from senior management revealed the following:

- 52% of respondents stated that changes are being made to global supply chains in the wake of global events.

- 40% are planning a reassessment

- and only 8% see no need for change.

- Nearly 40% of the companies surveyed also stated that they were planning changes to their workforce.

- 36% are planning further steps in automation,

- 41% are considering revising the current pace of their automation.

Industry 4.0 technologies will fundamentally change the supply chain

The current changes and adjustments to supply chains are based on the principle of delivery capability. Those who cannot deliver are currently not competitive. Price plays a secondary role in this.

Once the market stabilizes, costs will once again take center stage. The question then becomes whether to accept the next disruption in the global supply chain or to have switched to a flexible supply chain in time (see also above under “Global Logistics – Resilient Logistics”).

To make this sustainable and competitive, it is important to seize the opportunity and accelerate the expansion of Industry 4.0 technologies:

Internet of Things (IoT) – The new 5G mobile communications standard makes the IoT possible in the first place. It opens up new perspectives for companies and investors, especially in the area of smart factories

Competitive through cost reduction with automation and networking of warehouse systems

Electricity self-consumption optimization up to autonomous power supply

- Optimizing self-consumption of electricity

- Background information on petroleum, CO2 tax and renewable energies – energy transition

Robotics and automation in industry and logistics are already bringing supply chains back to regionally important locations. This includes buffer warehouses, local warehouses, and decentralized logistics centers such as micro-hubs.

- Germany is a leader in robotics

- Robotics & Automation in the Warehouse

- Local decentralized hubs – logistics centers

- Micro-Hub – The key to a brilliant solution?

- Buffer storage in intralogistics – The solution for ensuring supply

Use of digital twins

Use of digital twins in industry – Image: Xpert.Digital / EPStudio20|Shutterstock.com

Another important form from the Industry 4.0 world is the use of digital twins.

A digital twin is part of process automation (and belongs to the broader and emerging category of "hyperautomation").

The digital twin transforms the entire product lifecycle management process, from design and manufacturing to service and operation. Product lifecycle management is very time-consuming in terms of efficiency, manufacturing, intelligence, service phases, and sustainability in product design. A digital twin can merge the physical and virtual spaces of the product and drastically reduce the time required.

The digital twin enables companies to create a digital footprint of all their products, from design to development and throughout the entire product lifecycle.

In the manufacturing process, the digital twin is a virtual replica of real-time operations in the factory. Thousands of sensors are placed throughout the physical manufacturing process, collecting data from various dimensions, such as environmental conditions, machine behavior, and tasks performed. All this data is continuously transmitted and collected by the digital twin. Thanks to the Internet of Things, digital twins have become more affordable and could shape the future of the manufacturing industry.

This means that digital twins offer great business potential, as they predict the future instead of analyzing the past of the manufacturing process.

Another example comes from the healthcare sector: Previously, "healthy" was defined as the absence of symptoms. With a digital twin, "healthy" patients can be compared with the rest of the population to define true health.

3D Visualization: Digital Twin – Image: Xpert.Digital / Chesky|Shutterstock.com

Related to this:

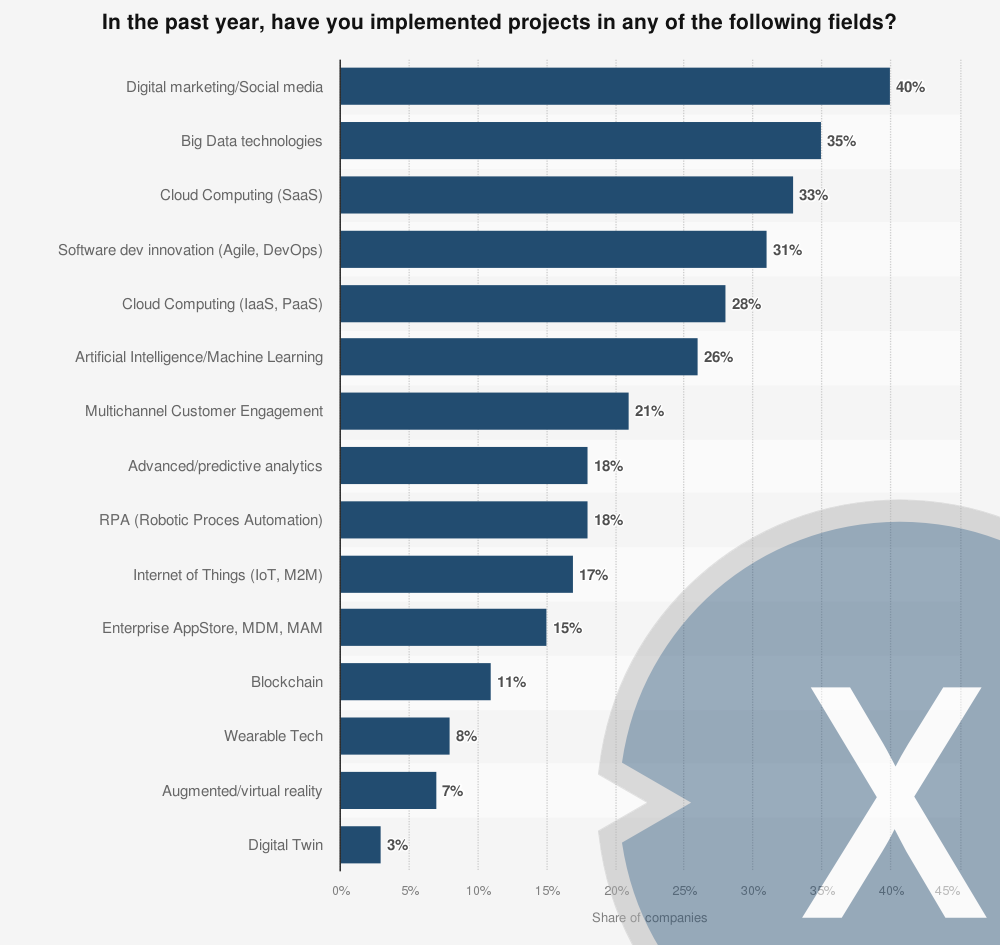

Digital Transformation - Figures from Italy

The question was phrased as follows: “If you consider all areas of your business, which of the following innovative digital projects did you already invest in in 2019 / will you invest in in 2020?”

Digital transformation projects carried out by companies in Italy in 2019 – by sector

Digital transformation projects carried out by companies in Italy in 2019 – Image: Xpert.Digital

In 2019, 40 percent of the surveyed companies in Italy implemented digital marketing or social media campaigns, while 35 percent of the companies launched projects using big data technologies. Virtual and augmented reality still appear to be a niche area for Italian companies, as only seven percent of them are implementing projects in this field.

Did you carry out any projects in any of the following areas last year?

- Digital Marketing/Social Media – 40%

- Big Data technologies – 35%

- Cloud Computing (SaaS) / Cloud Computing (SaaS) – 33%

- Software development innovation (Agile, DevOps) – 31%

- Cloud Computing (IaaS, PaaS) / Cloud Computing (IaaS, PaaS) – 28%

- Artificial Intelligence / Machine Learning – 26%

- Multichannel customer engagement – 21%

- Advanced / predictive analytics – 18%

- RPA (Robotic Process Automation) – 18%

- Internet of Things (IoT, M2M) / Internet of Things (IoT, M2M) – 17%

- Enterprise AppStore, MDM, MAM / Enterprise AppStore, MDM, MAM – 15%

- Blockchain / Blockchain – 11%

- Wearable Technology / Wearable Tech – 8%

- Augmented/Virtual Reality – 7%

- Digital Twin – 3%

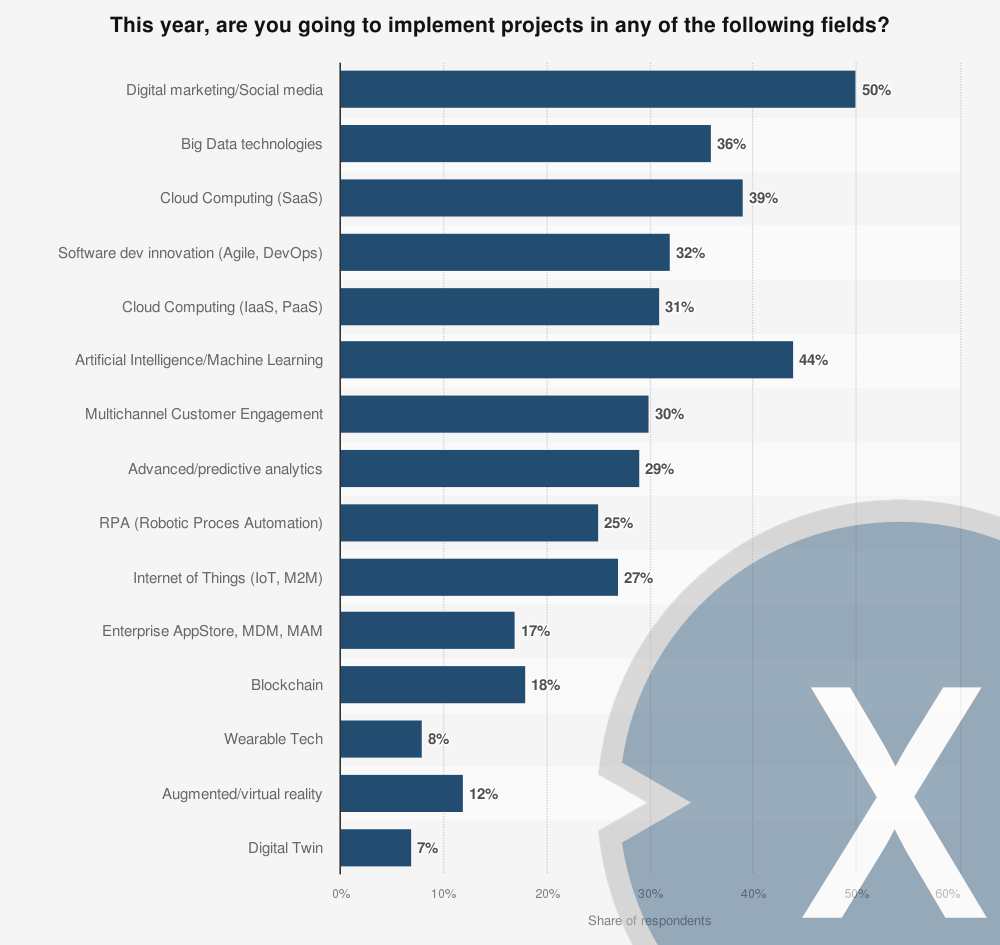

Companies implementing digital transformation processes in Italy in 2020 – by sector

Companies implementing digital transformation processes in Italy in 2020 – Image: Xpert.Digital

According to a 2019 survey, 32 percent of the companies surveyed will undertake software development innovation projects in 2020. Digital marketing and big data appear to be more attractive areas, with 50 and 36 percent of companies, respectively, planning projects in these fields. Finally, 39 percent of Italian companies planned to invest resources in cloud computing.

Will you be carrying out projects in any of the following areas this year?

- Digital Marketing / Social Media / Digital marketing/Social media – 50%

- Big Data technologies – 36%

- Cloud Computing (SaaS) / Cloud Computing (SaaS) – 39%

- Software development innovation (Agile, DevOps) – 32%

- Cloud Computing (IaaS, PaaS) / Cloud Computing (IaaS, PaaS) – 31%

- Artificial Intelligence / Machine Learning – 44%

- Multichannel customer engagement – 30%

- Advanced/predictive analytics – 29%

- RPA (Robotic Process Automation) – 25%

- Internet of Things (IoT, M2M) / Internet of Things (IoT, M2M) – 27%

- Enterprise AppStore, MDM, MAM / Enterprise AppStore, MDM, MAM – 17%

- Blockchain / Blockchain – 18%

- Wearable Technology / Wearable Tech – 8%

- Augmented/virtual reality – 12%

- Digital Twin – 7%

Smart Factory - Implementation in German companies

How far along is your company on the path to becoming a smart factory? – Image: Xpert.Digital

In 2019, 48 percent of the surveyed companies, predominantly active in mechanical and plant engineering as well as the electrical and automotive industries, stated that they were pursuing individual operational projects related to Industry 4.0. Four years earlier, this figure was 31 percent.

Approximately 70 percent of the companies surveyed are part of the mechanical and plant engineering, electrical and automotive industries.

2015: How far along is your company on the path to becoming a “Smart Factory”?

- We are pursuing individual operational projects in the area of Industry 4.0 – 31%

- The topic is currently in the observation and analysis phase for us – 36%

- The topic is currently in the planning and testing phase – 5%

- We haven't looked into it in detail yet – 19%

- Industry 4.0 is being fully implemented operationally at our company – 4%

- No answer – 5%

2017: How far along is your company on the path to becoming a “Smart Factory”?

- We are pursuing individual operational projects in the area of Industry 4.0 – 41%

- The topic is currently in the observation and analysis phase for us – 24%

- The topic is currently in the planning and testing phase – 14%

- We haven't looked into it in detail yet – 8%

- Industry 4.0 is being fully implemented operationally at our company – 7%

- No response – 6%

2019: How far along is your company on the path to becoming a “Smart Factory”?

- We are pursuing individual operational projects in the area of Industry 4.0 – 48%

- The topic is currently in the observation and analysis phase for us – 21%

- The topic is currently in the planning and testing phase – 11%

- We haven't looked into it in detail yet – 9%

- Industry 4.0 is being fully implemented operationally at our company – 8%

- No response – 3%

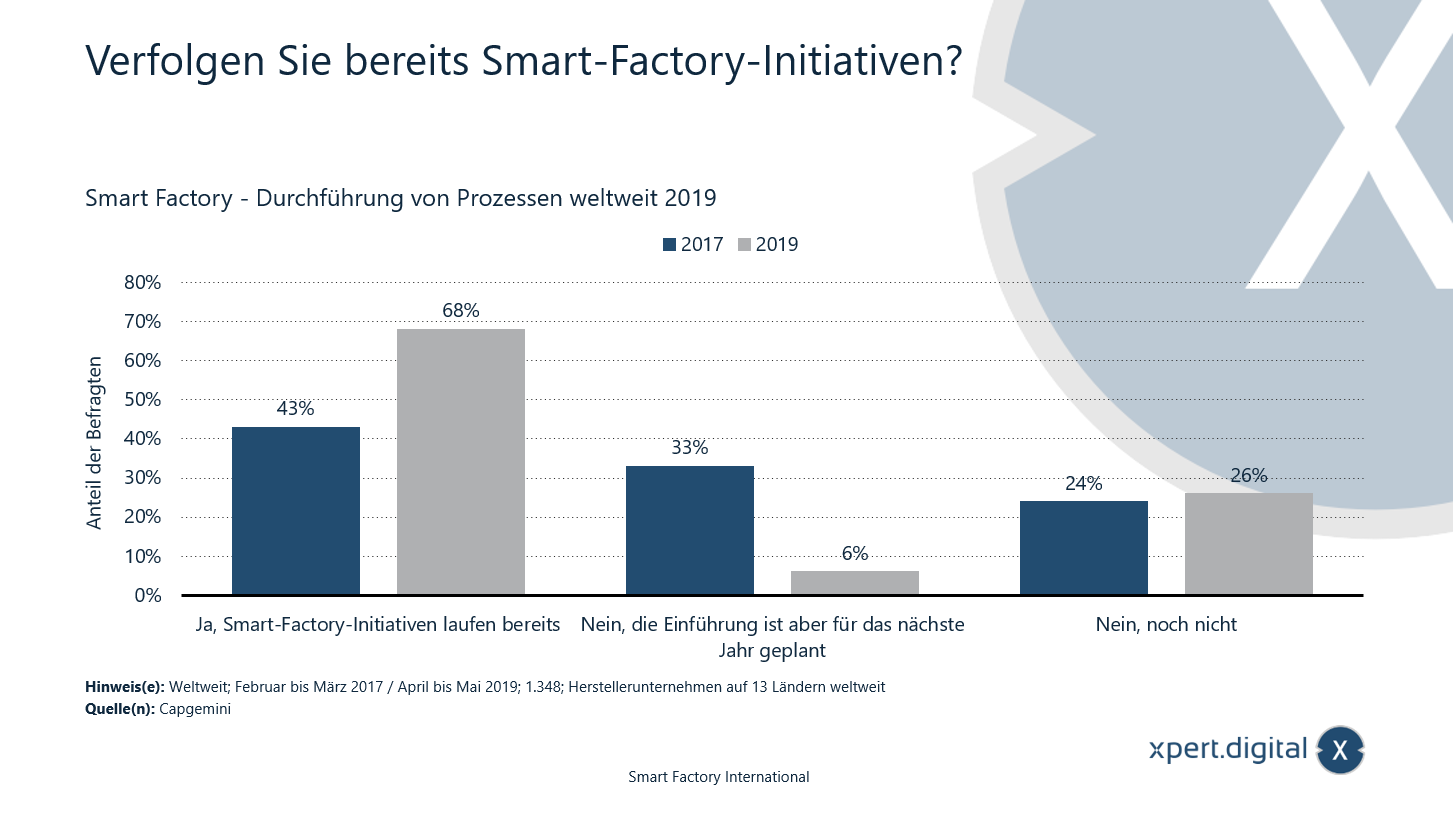

Smart Factory - Implementation of processes worldwide

Are you already pursuing smart factory initiatives? – Image: Xpert.Digital

In 2019, 68 percent of surveyed manufacturing companies worldwide stated that they were already implementing a smart factory initiative. Two years prior, this figure was 43 percent. Survey of manufacturing companies from 13 countries worldwide.

2019: Are you already pursuing smart factory initiatives?

- Yes, smart factory initiatives are already underway – 68%

- No, but the introduction is planned for next year – 6%

- No, not yet – 26%

2017: Are you already pursuing smart factory initiatives?

- Yes, smart factory initiatives are already underway – 43%

- No, but the introduction is planned for next year – 33%

- No, not yet – 24%

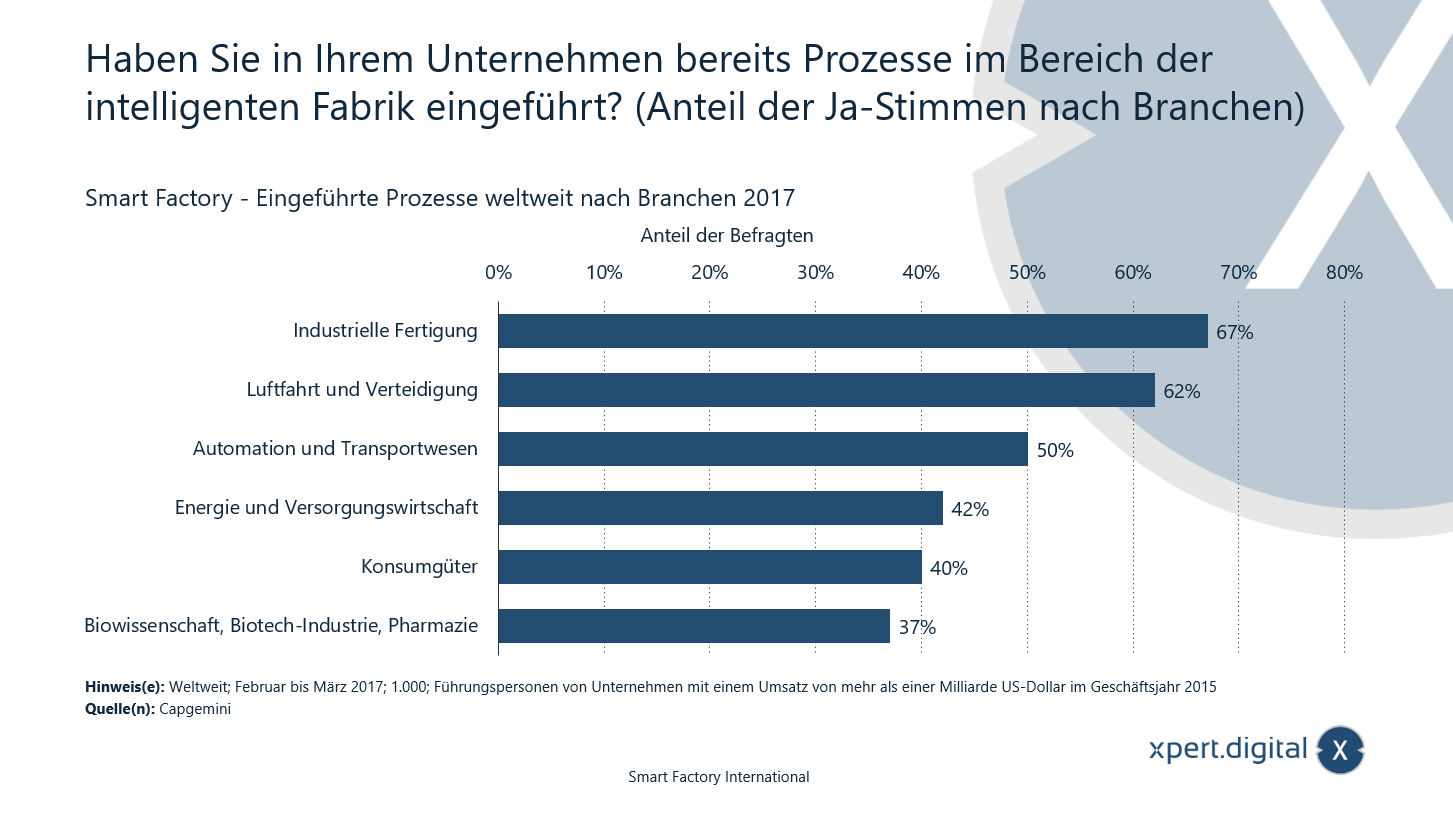

Have you already implemented smart factory processes in your company?

Have you already implemented smart factory processes in your company? – Image: Xpert.Digital

The graphic shows the results of a global survey conducted in 2017 on smart factory processes. 67 percent of the surveyed executives from the industrial manufacturing sector stated that they had already implemented smart factory processes.

Smart Factory – Implemented processes worldwide by industry

- Industrial manufacturing – 67%

- Aviation and defense – 62%

- Automation and transportation – 50%

- Energy and utilities sector – 42%

- Consumer goods – 40%

- Life sciences, biotech industry, pharmaceuticals – 37%

According to the source, the survey was conducted in eight countries (USA, United Kingdom, France, Germany, Italy, Sweden, China and India).

What are the biggest challenges in strategy planning for smart factories?

What are the biggest challenges in strategy planning for smart factories? – Image: Xpert.Digital

The graphic shows the results of a global survey conducted in 2017 on the biggest challenges in strategy planning for smart factories. 32 percent of respondents stated that the lack of coordination between different organizational units was the biggest challenge in strategy planning for smart factories.

Smart Factory – Biggest Challenges in Strategy Planning

- Lack of coordination between different organizational units – 32%

- Lack of unity in the leadership team – 28%

- Lack of clarity about business scenarios – 28%

- Lack of ownership – 23%

- Lack of imagination – 21%

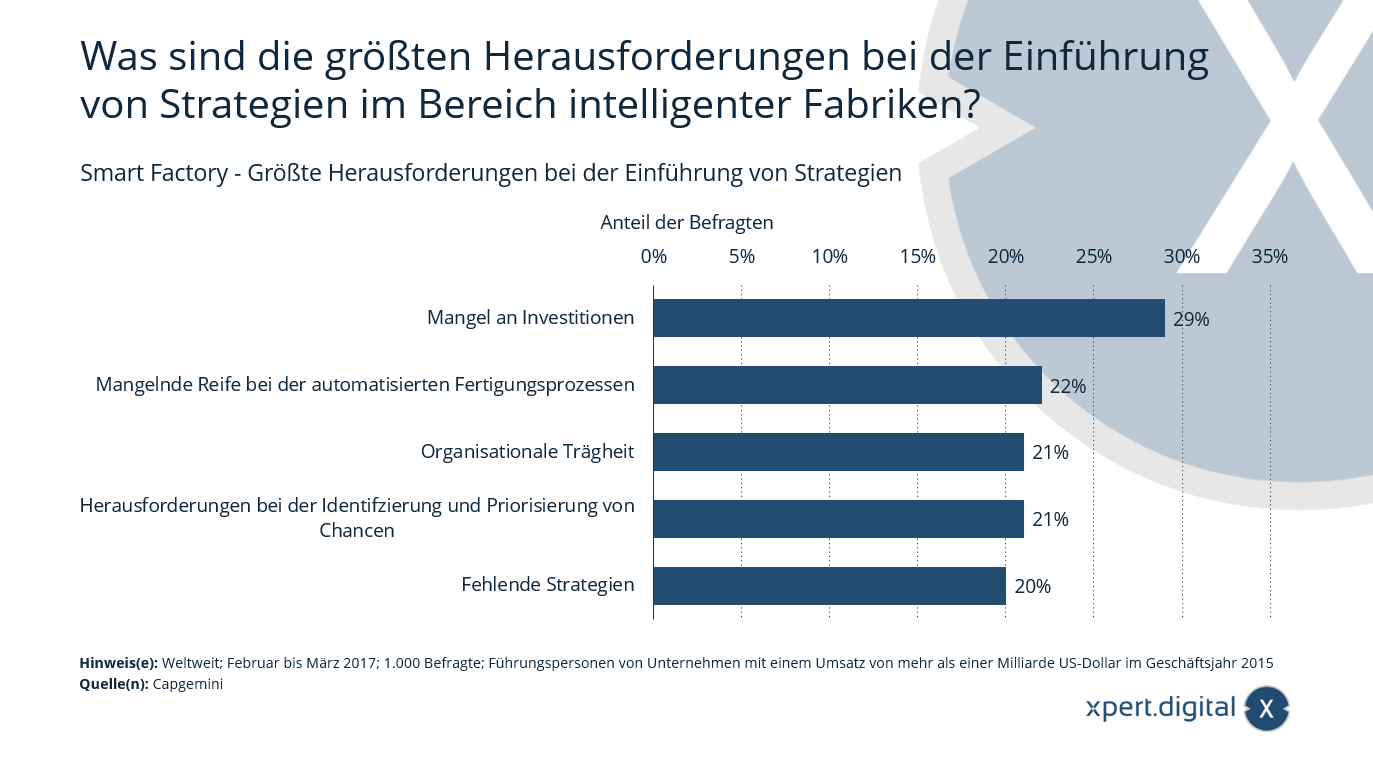

What are the biggest challenges in implementing smart factory strategies?

Smart Factory – Biggest challenges in implementing strategies – Graphic: Xpert.Digital

The graphic shows the results of a global survey conducted in 2017 on the biggest challenges in implementing smart factory strategies. 29 percent of respondents stated that a lack of investment was the biggest challenge in implementing smart factory strategies.

Smart Factory – Biggest challenges in implementing strategies

- Lack of investment – 29%

- Lack of maturity in automated manufacturing processes – 22%

- Organizational inertia – 21%

- Challenges in identifying and prioritizing opportunities – 21%

- Lack of strategies – 20%

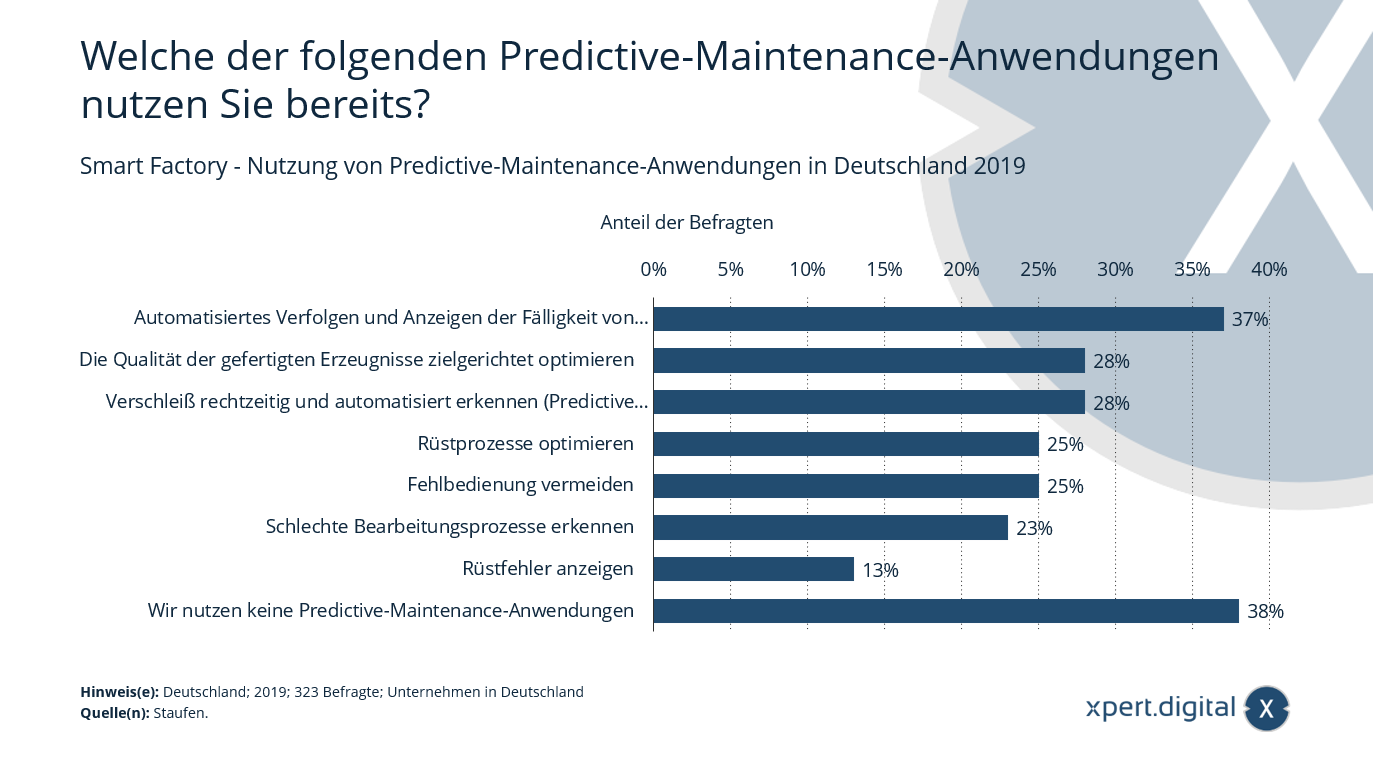

Which of the following predictive maintenance applications are you already using?

Smart Factory – Use of predictive maintenance applications in Germany – Image: Xpert.Digital

In 2019, 37 percent of the surveyed companies, primarily active in the mechanical engineering, electrical engineering, and automotive industries, stated that they use automated tracking and display of due dates for regular maintenance work. Approximately 70 percent of the surveyed companies are from the mechanical engineering, electrical engineering, and automotive industries.

Smart Factory – Use of Predictive Maintenance Applications in Germany

- Automated tracking and display of the due date of regular maintenance work – 37%

- Targeted optimization of the quality of manufactured products – 28%

- Detecting wear and tear early and automatically (Predictive Maintenance) – 28%

- Optimize setup processes – 25%

- Avoid incorrect operation – 25%

- Identifying poor processing processes – 23%

- Display setup errors – 13%

- We do not use predictive maintenance applications – 38%

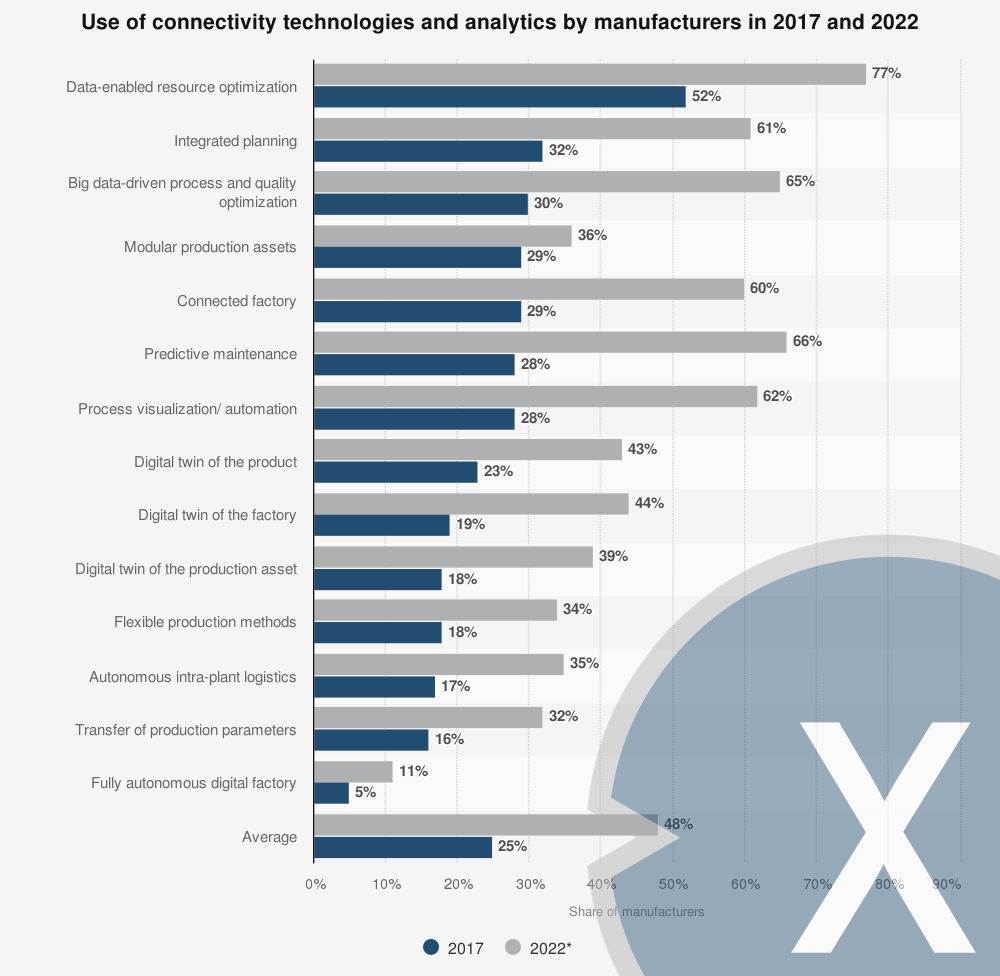

Use of connectivity technologies and analytics in manufacturing 2017-2022

Use of connectivity technologies and analytics in manufacturing – Image: Xpert.Digital

In 2017, data-driven resource optimization was the most widely used connectivity and analytics technology in manufacturing. It was predicted that this technology would remain the most widely used through 2022. However, the fastest-growing technology between 2017 and 2022 was predicted to be predictive maintenance. Forecasts indicated that by 2022, approximately 66 percent of manufacturers would have implemented predictive maintenance in their operations.

Use of connectivity technologies and analytics by manufacturers in 2017

- Data-enabled resource optimization – 77%

- Integrated planning – 61%

- Big data-driven process and quality optimization – 65%

- Modular production assets – 36%

- Networked factory / Connected factory – 60%

- Predictive maintenance – 66%

- Process visualization/automation – 62%

- Digital twin of the product – 43%

- Digital twin of the factory / Digital twin of the factory – 44%

- Digital twin of the production plant / Digital twin of the production asset – 39%

- Flexible production methods / Flexible production methods – 34%

- Autonomous intra-plant logistics – 35%

- Transfer of production parameters – 32%

- Fully autonomous digital factory – 11%

Use of connectivity technologies and analytics by manufacturers in 2022

- Data-enabled resource optimization – 52%

- Integrated planning – 32%

- Big data-driven process and quality optimization – 30%

- Modular production assets – 29%

- Networked factory / Connected factory – 29%

- Predictive maintenance – 28%

- Process visualization/automation – 28%

- Digital twin of the product – 23%

- Digital twin of the factory / Digital twin of the factory – 19%

- Digital twin of the production plant / Digital twin of the production asset – 18%

- Flexible production methods / Flexible production methods – 18%

- Autonomous intra-plant logistics – 17%

- Transfer of production parameters – 16%

- Fully autonomous digital factory – 5%

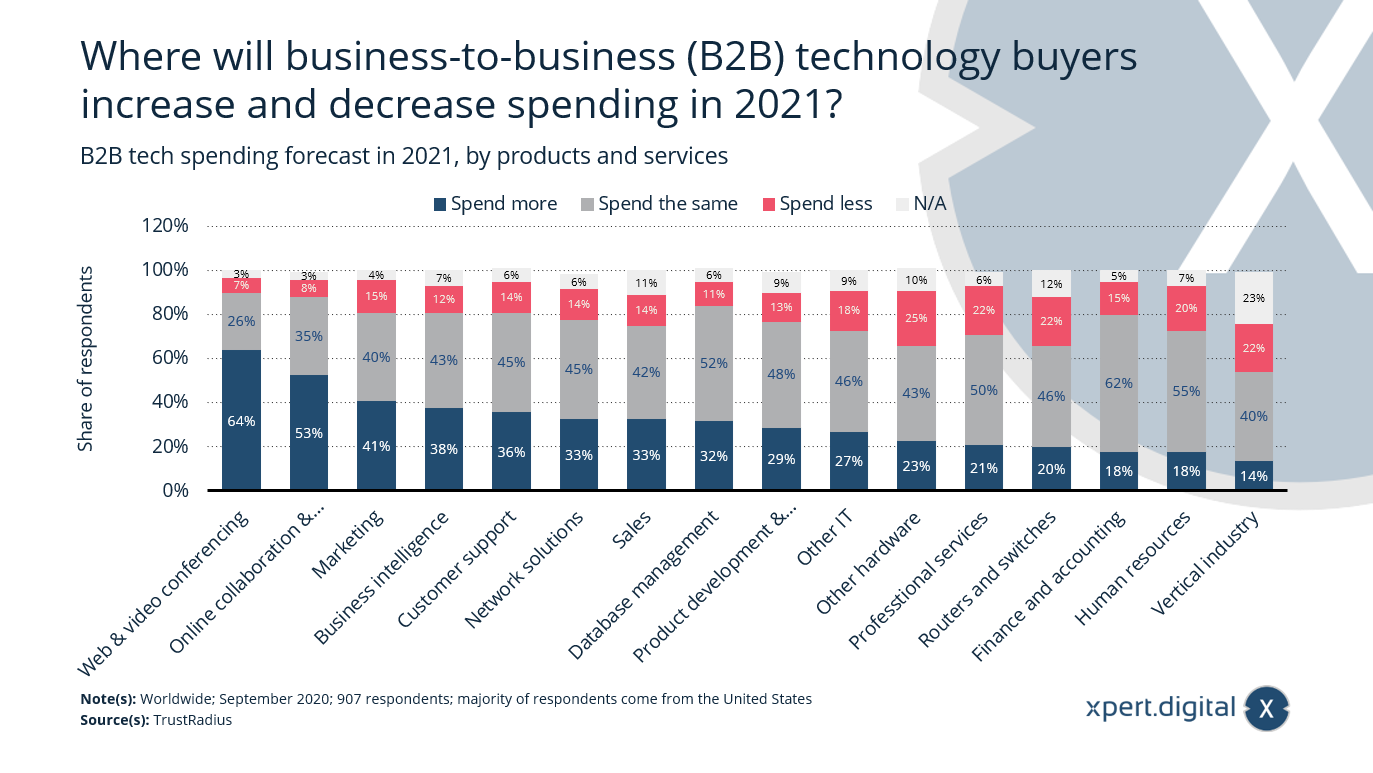

Where will buyers of business-to-business (B2B) technology spend more or less in 2021?

Spending on B2B technology in 2021 – Image: Xpert.Digital

The majority of surveyed business-to-business (B2B) technology buyers believe that spending on web and video conferencing, as well as online collaboration and project management, will increase in 2021. With the coronavirus (COVID-19) pandemic continuing into the new year and vaccines taking time to become available, remote work will remain the norm for the foreseeable future.

Forecast of B2B technology spending in 2021, by products and services

Additional expenses for:

- Web and video conferencing – 64%

- Online collaboration and project management – 53%

- Marketing – 41%

- Business intelligence / business intelligence – 38%

- Customer support – 36%

- Network solutions – 33%

- Sales – 33%

- Database management – 32%

- Product development and management – 29%

- Other IT / Other IT – 27%

- Other hardware – 23%

- Professional services – 21%

- Routers and switches – 20%

- Finance and accounting – 18%

- Human resources / Human resources – 18%

- Vertical industry / Vertical industry – 14%

Expenditure remains the same

- Web and video conferencing – 26%

- Online collaboration and project management – 35%

- Marketing – 40%

- Business intelligence / business intelligence – 43%

- Customer support – 45%

- Network solutions – 45%

- Sales – 42%

- Database management – 52%

- Product development and management – 48%

- Other IT / Other IT – 46%

- Other hardware – 43%

- Professional services – 50%

- Routers and switches – 46%

- Finance and accounting – 62%

- Human resources / Human resources – 55%

- Vertical industry / Vertical industry – 40%

Reduced spending on:

- Web and video conferencing – 7%

- Online collaboration and project management – 8%

- Marketing – 15%

- Business intelligence / business intelligence – 12%

- Customer support – 14%

- Network solutions – 14%

- Sales – 14%

- Database management – 11%

- Product development and management – 13%

- Other IT / Other IT – 18%

- Other hardware – 25%

- Professional services – 22%

- Routers and switches – 22%

- Finance and accounting – 15%

- Human resources / Human resources – 20%

- Vertical industry / Vertical industry – 22%

Not specified)

- Web and video conferencing – 3%

- Online collaboration and project management – 3%

- Marketing – 4%

- Business intelligence / business intelligence – 7%

- Customer support – 6%

- Network solutions – 6%

- Sales – 11%

- Database management – 6%

- Product development and management – 9%

- Other IT / Other IT – 9%

- Other hardware – 10%

- Professional services – 6%

- Routers and switches – 12%

- Finance and accounting – 5%

- Human resources / Human resources – 7%

- Vertical industry / Vertical industry – 23%

Looking ahead to the next few years, in which areas do you expect the shipping industry to experience the greatest boost from increasing digitalization?

Areas affected by digitalization in the shipping industry – Image: Xpert.Digital

In 2021, the surveyed suppliers, shipowners, ship operators, and shipyards expect maintenance and fleet management to be most affected by increasing digitalization in the shipping industry. While 28 percent of suppliers and 27 percent of shipyards believe that digitalization will impact the use of remotely piloted unmanned vessels, shipowners and ship operators are more skeptical.

Areas affected by digitalization in the shipping industry in 2021

Suppliers

- Maintenance/remote monitoring – 54%

- Fleet management/performance – 49%

- Assistance systems for optimized ship operation – 45%

- Communication (e.g., crew, logistics chain) – 33%

- Navigation/bridge management – 33%

- Use of unmanned ships (remotely controlled) – 28%

- Use of unmanned ships (completely autonomous) – 18%

- Digital twin – 13%

- Other areas – 2%

- Don't know / Do not know – 14%

Shipowners/ship operators – Shipowners/ship operators

- Maintenance/remote monitoring – 56%

- Fleet management/performance – 63%

- Assistance systems for optimized ship operation – 57%

- Communication (e.g., crew, logistics chain) – 49%

- Navigation/bridge management – 40%

- Use of unmanned ships (remotely controlled) – 7%

- Use of unmanned ships (completely autonomous) – 7%

- Digital twin – 8%

- Other areas – 1%

- Don't know / Do not know – 6%

Shipyards

- Maintenance/remote monitoring – 49%

- Fleet management/performance – 43%

- Assistance systems for optimized ship operation – 55%

- Communication (e.g., crew, logistics chain) – 39%

- Navigation/bridge management – 33%

- Use of unmanned ships (remotely controlled) – 27%

- Use of unmanned ships (completely autonomous) – 16%

- Digital twin – 10%

- Other areas – 2%

- Don't know / Do not know – 14%

Are you looking for technical and strategic advice for supply chain optimization or warehouse optimization? Xpert.Digital can help!

Konrad Wolfenstein

I am happy to be available to you as a personal consultant for supply chain and warehouse solutions.

You can contact me by filling out the contact form below or simply call me on +49 7348 4088 965 (Munich) .

I'm looking forward to our joint project.

Write to me

Xpert.Digital – Konrad Wolfenstein

Xpert.Digital is a hub for industry focusing on digitalization, mechanical engineering, logistics/intralogistics and photovoltaics.

With our 360° Business Development solution, we support renowned companies from new business to after-sales.

Market intelligence, smarketing, marketing automation, content development, PR, mail campaigns, personalized social media and lead nurturing are part of our digital tools.

You can find more information at: www.xpert.digital – www.xpert.solar – www.xpert.plus

Keep in touch