How is the mechanical engineering sector structured in the various EU countries and outside of them in the USA, BRIC, MIST, China and Japan? – Image: Xpert.Digital

Industrial value creation: The mechanical engineering sector in global comparison

Mechanical engineering and globalization: New perspectives and markets

Mechanical engineering is a key pillar of industrial value creation in many countries and is characterized by diverse structures, specializations, and economic developments. This article provides a comprehensive overview of the mechanical engineering sector in the European Union as well as in key international markets such as the USA, the BRIC countries, China, and Japan.

Related to this:

Mechanical engineering in the European Union

Leading countries and export quotas

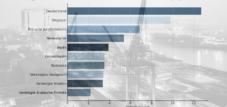

Germany is the undisputed leader in European mechanical engineering and makes a significant contribution to the EU's industrial performance. The distribution of production shares demonstrates Germany's dominance:

- Germany: 27% of total mechanical engineering production in the EU

- Italy: 14%

- France: 12%

- Spain: 8%

- Poland: 6%

Export markets within the EU are particularly important for German machine manufacturers. The main buyers of German machines in the EU are:

- France: 16%

- Italy: 11%

- Poland: 10%

- Netherlands: 10%

- Austria: 9.5%

Overall, 45% of all German machinery exports go to the EU. This close economic integration demonstrates the central importance of the EU's single market for the industry.

Related to this:

- Successful mechanical engineering companies in Germany include Bosch, CLAAS, Dürr, Exyte, Festo, Krones, Voith, Zeiss and others

- Uncertainty surrounding investments in mechanical engineering? What role does digital transformation play in investment security?

Company structure

The mechanical engineering sector in the EU is largely comprised of medium-sized companies. This is particularly true for Germany:

- 95% of the approximately 6,600 mechanical engineering companies have fewer than 500 employees.

The distribution of company sizes in Germany:

- 62.6% micro-enterprises (up to €2 million in revenue)

- 22.7% small businesses (up to €10 million in revenue)

- 10.6% Medium-sized companies (up to €50 million in revenue)

- 4.1% Large companies (over €50 million in revenue)

This structure is typical for mechanical engineering in many EU countries, with a high proportion of specialized companies that are often world market leaders in niche markets.

Specialization and competitiveness

Specialization within the EU varies greatly between member states:

- Luxembourg, Belgium, France and Ireland: Strong specialization in high-tech products and highly skilled workers.

- Germany, Netherlands, Great Britain: Broad and balanced portfolio with high technological expertise.

- Denmark, Sweden, Finland: Focus on medium to low qualification requirements in production.

- Hungary, Italy, Portugal: Focus on areas with low to medium qualifications.

Growth and challenges

Despite challenges, the European mechanical engineering industry is growing steadily:

- 95% of EU countries report stable or increasing market shares.

- Investments in transport infrastructure, sustainable technologies and energy supply are driving growth.

However, challenges remain:

- Profitability: The average operating profit is 10% in Europe, while it reaches 14% in North America.

- Cost increases: Rising labor and material costs, as well as supply chain bottlenecks, are putting companies under pressure.

To remain competitive, European machine manufacturers are increasingly focusing on digitalization, automation and sustainable production methods.

Mechanical engineering outside the EU

China

China has developed into one of the leading players in global mechanical engineering over the last few decades:

China is the EU's most important trading partner in mechanical engineering:

- 11.4% of machinery imports into the EU came from China (2022).

Between 2010 and 2020, exports grew rapidly in many segments:

- Packaging machines: +206.9%

- Paper machines: +266.8%

- Semiconductor manufacturing machines: +167.5%

China is investing heavily in research and development and is increasingly relying on its own innovations to be less dependent on Western technology.

USA

The USA is one of the most important export markets for German machinery:

- The US market has a high demand for German high-tech machines.

- Germany is among the five largest suppliers of machinery to the USA.

Furthermore, US companies are increasingly investing in local production to minimize supply chain risks.

BRIC countries (Brazil, Russia, India, China)

The BRIC countries are significant growth regions:

- 13.9% of German machinery exports go to these countries.

- India and Russia are showing rising industrial production, while Brazil is weakening.

- China's influence continues to grow, while Russia is losing importance due to geopolitical challenges.

MIST countries (Mexico, Indonesia, South Korea, Türkiye)

This group of countries is becoming increasingly important for mechanical engineering:

- 5.6% of German machinery exports go to these countries.

- Indonesia and Turkey have high growth rates in industrial production.

- However, the export quota of German machines to these countries has stagnated at around 6% in recent years.

Japan

Japan remains an important market for European machine manufacturers:

- 13.8% of German machinery exports go to Japan and the USA.

- Japan is heavily investing in automation and robotics, which offers opportunities for European machine manufacturers.

Eastern Europe (non-EU countries)

Countries like Georgia, Moldova and Ukraine are gaining importance for mechanical engineering:

- They benefit from free trade agreements with the EU, which reduce tariffs and facilitate trade processes.

- The machine industry is growing particularly in Ukraine, which will increasingly rely on modern production technologies after reconstruction.

Innovations in mechanical engineering: The trends of tomorrow

The future of mechanical engineering depends significantly on technological developments and economic conditions:

- Digitalization and Industry 4.0 will increase efficiency and competitiveness.

- Sustainability is playing an increasingly important role, especially through the use of energy-efficient machines.

- New markets in Asia, Africa and South America offer potential for long-term growth.

European machine manufacturers must adapt to remain internationally competitive. Key measures include:

- Investments in research and development, particularly in the field of artificial intelligence and automation.

- Optimizing supply chains to reduce dependence on individual markets.

- A stronger focus on sustainable technologies and environmentally friendly production processes.

These strategic measures will enable mechanical engineering to continue playing a key role in the global economy in the future.

Our recommendation: 🌍 Limitless reach 🔗 Connected 🌐 Multilingual 💪 Sales power: 💡 Authentic with strategy 🚀 Innovation meets 🧠 Intuition

From local to global: SMEs conquer the world market with a clever strategy - Image: Xpert.Digital

In an era where a company's digital presence determines its success, the challenge lies in creating an authentic, personalized, and far-reaching presence. Xpert.Digital offers an innovative solution that positions itself as the intersection of an industry hub, a blog, and a brand ambassador. It combines the advantages of communication and sales channels in a single platform and enables publication in 18 different languages. Cooperation with partner portals and the ability to publish articles on Google News and a press distribution list with approximately 8,000 journalists and readers maximize the reach and visibility of the content. This represents a crucial factor in external sales and marketing (SMarketing).

More information here:

Mechanical engineering in focus: Europe's diversity and global power dynamics - background analysis

Insider view: Germany's key role in global mechanical engineering

Mechanical engineering, as the backbone of the European and global economy, manifests itself in diverse structures and forms across the world. Within the European Union (EU), a complex picture emerges, ranging from Germany's dominance to specialized niches in smaller member states. Outside the EU, the USA, the BRIC countries, and above all China and Japan, shape the global balance of power in mechanical engineering.

Mechanical engineering in the European Union: A complex structure

The EU represents one of the world's most important economic areas, and mechanical engineering plays a key role within it. It is not only a major employer but also a driver of innovation and a crucial factor in the overall competitiveness of European industry. However, the structure of mechanical engineering within the EU is by no means homogeneous, but rather reflects the diverse economic and industrial traditions of the individual member states.

Related to this:

Germany: The undisputed leader

When discussing European mechanical engineering, Germany is unavoidable. The country is the undisputed center of the industry in the EU and one of the global leaders. Germany generates more than a quarter of total mechanical engineering production within the EU, specifically 27 percent. This dominance has developed historically and is based on a combination of factors: a long industrial tradition, a strong focus on engineering and innovation, an excellent educational infrastructure, and a close-knit network of suppliers and research institutions.

The export strength of the German mechanical engineering sector is impressive. A significant portion of production is destined for export, underscoring the global competitiveness of German companies. Within the EU, the most important export markets for German machinery are France (16%), Italy (11%), Poland and the Netherlands (10%), and Austria (9.5%). Overall, 45% of all German machinery exports go to the EU, with the aforementioned top five countries and five other EU member states alone accounting for 84% of these EU exports. These figures illustrate the close integration of the German mechanical engineering sector with other European economies and its central role in the European single market.

Italy, France, Spain and Poland: The pursuers in the European field

Following Germany, at some distance, are Italy with 14 percent, France with 12 percent, Spain with 8 percent, and Poland with 6 percent of EU-wide mechanical engineering production. These countries represent important pillars of European mechanical engineering, even though they differ in their structure and specialization.

Italy

Italian mechanical engineering is characterized by a high degree of specialization in specific niches, particularly in automation technology, packaging machinery, textile machinery, and agricultural machinery. Italian companies are often family-run businesses, distinguished by their flexibility and customer focus. The Emilia-Romagna and Lombardy regions are considered centers of Italian mechanical engineering.

France

French mechanical engineering is more heavily geared towards large companies and corporations, and traditionally strong in the aerospace, defense, energy, and automotive sectors. French machine manufacturers are often leaders in high-tech fields and place a high value on research and development. The Île-de-France and Auvergne-Rhône-Alpes regions are key locations.

Spain

Spanish mechanical engineering has experienced considerable growth in recent decades, establishing itself particularly in the renewable energy, machine tool, and automotive supply sectors. Spain benefits from its geographical location as a bridge to Latin America and from comparatively lower labor costs within the EU. The Basque Country and Catalonia are key regions.

Poland

Since joining the EU, Poland has developed into a key production location for European mechanical engineering. The country benefits from its proximity to Germany, lower labor costs, and a growing pool of skilled workers. Poland is particularly strong in supplying components to the automotive industry and in plant engineering. Regions such as Silesia and Greater Poland play a central role.

The corporate structure: SMEs as the backbone

A defining characteristic of European mechanical engineering, particularly in Germany and Italy, is the dominance of medium-sized enterprises. These companies, often second- or third-generation family businesses, form the backbone of the industry. In Germany, for example, 95 percent of the approximately 6,600 mechanical engineering companies are medium-sized enterprises with fewer than 500 employees.

The industry structure in Germany illustrates this prevalence of small and medium-sized enterprises (SMEs) even more clearly: 62.6 percent are micro-enterprises with a turnover of up to €2 million, 22.7 percent are small enterprises with a turnover of up to €10 million, 10.6 percent are medium-sized enterprises with a turnover of up to €50 million, and only 4.1 percent are large enterprises with a turnover exceeding €50 million. These figures demonstrate that the German mechanical engineering sector, and similarly the Italian sector, is characterized by a large number of specialized, flexible, and innovative SMEs. This structure enables a high degree of adaptability to changing market demands and a strong customer focus.

Related to this:

Specialization and competitiveness: diversity and niches

Within the EU, there are significant differences in the sectoral specialization of individual countries. Smaller EU states such as Malta, Luxembourg, and Finland often exhibit a stronger concentration on specific niche areas. Larger countries such as Germany, the UK, Italy, and France, on the other hand, have more diversified and balanced production structures.

Looking at specialization by qualification level also reveals interesting country groups. Countries like Luxembourg, Belgium, France, and Ireland are more specialized in activities requiring high qualifications, for example, in research and development, high technology, and specialized services. Germany, the Netherlands, and the United Kingdom show a balanced profile across various qualification levels. Denmark, Sweden, and Finland exhibit greater specialization in medium to low qualifications, indicating their strengths in manufacturing and traditional mechanical engineering. Hungary, Italy, and Portugal tend toward low to medium qualifications, reflecting their role as manufacturing hubs and suppliers.

These specializations are not accidental, but rather the result of historical developments, industrial policy decisions, and the respective strengths and weaknesses of individual countries. They lead to a complementary structure within European mechanical engineering, in which the countries complement each other at different stages of the value chain and in niche areas.

Related to this:

Growth and challenges: Between optimism and headwinds

The European mechanical engineering sector is showing overall positive growth trends. A large majority of companies, namely 95 percent, report stable or growing markets. Key growth drivers are investments in transport infrastructure, climate adaptation, and energy infrastructure. In particular, the need for modern and efficient technologies in these areas is fueling demand for machinery and equipment.

Despite these positive prospects, the European mechanical engineering sector also faces significant challenges. A key issue is profitability. European machine manufacturers achieve an average operating profit margin of around 10 percent, which lags behind their North American competitors, who reach approximately 14 percent. This difference is concerning and suggests structural disadvantages or lower efficiency in Europe.

Other contributing factors include rising labor and material costs, as well as persistent supply chain problems. In particular, the sharp increase in energy prices in Europe and the global scarcity of certain raw materials and components are putting companies under pressure. Geopolitical uncertainty and increasing trade conflicts are also contributing to a more challenging economic environment.

Future prospects: Transformation and innovation as the key to success

Despite the challenges, significant opportunities also exist for European mechanical engineering. In particular, the transformation of key customer sectors, especially the automotive industry, opens up new growth potential. The transition to electromobility, the development of autonomous vehicles, and the digitalization of production require new technologies and machinery. The market volume for battery production alone is estimated at €300 billion by 2030. This offers European mechanical engineering companies enormous opportunities to position themselves in this future market.

To remain competitive and seize these opportunities, European machine manufacturers must take proactive steps. Key areas for action include:

Optimization and diversification of supply chains

Dependence on individual suppliers and regions must be reduced to increase resilience to disruptions. Greater regional diversification and the development of alternative supply chains are necessary.

Consistent focus on sustainability

The demand for environmentally friendly and resource-saving technologies is constantly increasing. European mechanical engineering companies must make their products and production processes more sustainable and develop innovative solutions for a circular economy.

Investments in research and development

Innovation is key to competitiveness. European companies must continue to invest in research and development to create new technologies and products and position themselves in future-oriented fields. Digitalization and the application of artificial intelligence play a central role in this.

Securing skilled workers

The shortage of skilled workers is a growing challenge. European mechanical engineering companies must create attractive working conditions and invest in the training and further education of their employees in order to meet the demand for skilled workers.

Overall, European mechanical engineering remains a significant economic factor with promising future prospects. However, this is contingent on companies actively addressing current challenges, adapting to changes, and consistently seizing emerging opportunities. Innovation, sustainability, and flexibility will be the decisive factors for success.

Mechanical engineering outside the EU: Global dynamics and new power relations

Outside the European Union, mechanical engineering presents itself in an even more diverse and dynamic form. Developments in Asia, particularly in China, have fundamentally altered the global balance of power in recent decades. But interesting developments and specific structures also exist in the USA, the BRIC countries, and other regions.

China: Rise to global machine-building power

China has experienced an unprecedented rise in mechanical engineering over the past few decades, transforming itself from a mere production location into a global power in this sector. China is now the most important trading partner for Germany and the EU in terms of machinery imports. In 2022, 11.4 percent of machinery imports into the EU already originated from China. This figure underscores China's growing importance as both a supplier and a competitor for European machine manufacturers.

Chinese machinery manufacturing has experienced tremendous growth in many segments. Between 2010 and 2020, numerous sectors saw triple-digit export growth. Examples include liquid pumps (124.6 percent), plastics machinery (146.3 percent), textile machinery (132.5 percent), semiconductor manufacturing equipment (167.5 percent), woodworking machinery (184 percent), packaging machinery (206.9 percent), and paper machines (a remarkable 266.8 percent). These impressive growth rates demonstrate the dynamism and enormous potential of Chinese machinery manufacturing.

This rise can be attributed to several factors:

Government support

The Chinese government has strategically promoted mechanical engineering and supported it through industrial policy, subsidies, and investments in research and development. Initiatives such as "Made in China 2025" aim to develop China into a leading industrial nation and make mechanical engineering a key sector.

Enormous domestic demand

China's rapid economic growth has led to enormous domestic demand for machinery and equipment. Infrastructure expansion, industrial modernization, and rising consumption have boosted the Chinese mechanical engineering sector.

Low production costs

Comparatively low labor costs and a high availability of workers have long made China an attractive production location. This cost advantage has helped Chinese companies to be competitive in the global market.

Technological catch-up

In recent years, China has invested heavily in technological development and closed the gap with Western industrialized nations in many areas. Chinese companies are increasingly able to produce high-quality and technologically advanced machinery.

The challenges and opportunities of Chinese mechanical engineering

However, the Chinese mechanical engineering sector also faces challenges. These include rising labor costs, increasing competition both domestically and globally, environmental regulations, and the need to evolve from pure mass production to higher-value products and services. Despite these challenges, China will continue to expand its role as a global player in mechanical engineering and transform the competitive landscape.

USA: An established market with innovative strength

The USA has long been an important market for German and European mechanical engineering and is traditionally among the top five export countries. The US market is characterized by stable demand for high-quality and technologically advanced machinery. American companies are investing heavily in automation, digitalization, and Industry 4.0, which increases the need for corresponding machinery and equipment.

The US mechanical engineering sector itself is also a significant economic industry, characterized by its innovative strength and specialization in high-tech fields. Its strengths lie particularly in aerospace, medical technology, robotics, and software for mechanical engineering. The US boasts an excellent innovation ecosystem with world-leading universities, research institutions, and venture capital firms.

However, the US mechanical engineering sector also faces challenges. These include increasing competition from Asia, a shortage of skilled workers, rising healthcare costs, and the question of how to strengthen the domestic industrial base. Initiatives to strengthen domestic production and to bring production capacity back to the US ("reshoring") could play a greater role in the future.

BRIC countries: Different dynamics and potentials

The BRIC countries (Brazil, Russia, India, China) were long considered the growth engines of the global economy and important sales markets for mechanical engineering. In 2022, the BRIC countries accounted for 13.9 percent of all machinery exports from Germany. However, the dynamics within the BRIC group have developed differently in recent years.

Brazil

Brazilian mechanical engineering is heavily influenced by the raw materials sector and agriculture. The country has a large domestic market and growth potential in various sectors, but also structural problems such as political instability, bureaucracy, and infrastructure deficits.

Russia

Russian mechanical engineering was long heavily focused on the energy and defense industries. The geopolitical situation and international sanctions have significantly impacted its development in recent years, leading to an economic slowdown. Future prospects are uncertain.

India

India is an emerging market with great potential for mechanical engineering. The country benefits from a young population growth, an expanding middle class, and infrastructure investment. However, it also faces challenges such as poverty, bureaucracy, and inadequate infrastructure. The Indian government's "Make in India" initiative aims to strengthen domestic production and promote mechanical engineering.

China

As already explained in detail, China is the most dynamic and important BRIC country in mechanical engineering.

Self-sufficiency of the BRIC countries: A challenge for German mechanical engineering companies

Overall, the export share of German machinery to the BRIC countries has decreased since 2012, even though industrial production in India and Russia has increased. This suggests that the BRIC countries are increasingly able to meet their machinery needs themselves or to rely on other suppliers.

MIST countries: Emerging markets in focus

The so-called MIST countries (Mexico, Indonesia, South Korea, Turkey) are gaining importance as emerging markets for mechanical engineering. In 2022, they accounted for 5.6 percent of German machinery exports. Indonesia and Turkey, in particular, are experiencing strong growth in industrial production.

Mexico

Mexico benefits from its geographical proximity to the US and its role as a production hub for North American industry. The country is strong in automotive supply and other manufacturing sectors. The USMCA free trade agreement (successor to NAFTA) secures access to the North American market.

Indonesia

Indonesia is a populous island nation in Southeast Asia with a growing domestic market and potential for further growth. The country is investing in infrastructure and industrialization, with mechanical engineering playing a key role in this development.

South Korea

South Korea is a highly developed industrial nation with a strong focus on technology and innovation. South Korean mechanical engineering is competitive in various sectors, particularly in the automotive, electronics, and shipbuilding industries.

Türkiye

Turkey is an important manufacturing hub in the region and benefits from its geographical location as a bridge between Europe and Asia. Turkish industry is diversified and encompasses various sectors of mechanical engineering. However, it also faces economic and political challenges.

MIST countries: New opportunities for German mechanical engineering?

The export share of German machinery to the MIST countries rose to 6.5 percent by 2013, but has stagnated at around 6 percent since then. Nevertheless, the MIST countries remain important growth markets with potential for mechanical engineering.

Japan: Traditional strength and technological excellence

Japan, along with the USA, is a traditionally important buyer of German machinery. Together, the two countries accounted for 13.8 percent of German machinery exports in 2022. Japanese mechanical engineering is characterized by the highest precision, quality, and technological excellence. Japanese companies are leaders in fields such as robotics, automation technology, machine tools, and precision instruments.

However, the Japanese mechanical engineering sector also faces challenges. These include an aging population, a shrinking domestic market, and increasing competition from Asia, particularly from China and South Korea. Japanese companies must adapt and develop new growth areas, such as renewable energy, medical technology, and services.

Eastern Europe (non-EU countries): Emerging markets with potential

Several Eastern European countries outside the EU, such as Georgia, Moldova, and Ukraine, are gaining importance as emerging markets for mechanical engineering. These countries have concluded free trade agreements with the EU, which have led to the elimination of most tariffs and more efficient customs procedures. Machinery and equipment are particularly important export goods for Georgia and Moldova.

These countries offer potential as production locations and sales markets for European machine manufacturers. However, there are also risks and challenges, particularly regarding political stability, corruption, and infrastructure. Furthermore, Ukraine has been severely affected by the consequences of the war, which significantly impacts economic development and the prospects for the machine manufacturing sector.

Global relocation and increasing competitive intensity

In summary, the mechanical engineering sector outside the EU is characterized by increasing dynamism and a global shift in the balance of power. Asia, and China in particular, has gained enormous importance in recent decades and has become a major competitor for European and Western mechanical engineering companies. While traditional markets such as the USA and Japan remain important, the balance of power is increasingly shifting towards emerging economies.

This development presents the global mechanical engineering sector with major challenges. Competition is intensifying, technological demands are increasing, and geopolitical uncertainty is on the rise. Companies must be flexible, innovative, and internationally positioned to succeed in this dynamic environment. The ability to adapt to changing market conditions, develop new technologies, and manage global value chains will be crucial for future competitiveness in the mechanical engineering sector.

We are here for you - Consulting - Planning - Implementation - Project Management

☑️ SME support in strategy, consulting, planning and implementation

☑️ Creation or realignment of the digital strategy and digitization

☑️ Expansion and optimization of international sales processes

☑️ Global & Digital B2B trading platforms

☑️ Pioneer Business Development

Konrad Wolfenstein

I would be happy to serve as your personal advisor.

You can contact me by filling out the contact form below or simply call me on +49 7348 4088 965 .

I'm looking forward to our joint project.

Write to me

Xpert.Digital - Konrad Wolfenstein

Xpert.Digital is a hub for industry focusing on digitalization, mechanical engineering, logistics/intralogistics and photovoltaics.

With our 360° Business Development solution, we support renowned companies from new business to after-sales.

Market intelligence, smarketing, marketing automation, content development, PR, mail campaigns, personalized social media and lead nurturing are part of our digital tools.

You can find more information at: www.xpert.digital - www.xpert.solar - www.xpert.plus

Keep in touch