The invisible bottleneck: Why the future of arms manufacturing will be decided in supply chains – Image: Xpert.Digital

The true Achilles' heel of our defense: It's not the tanks

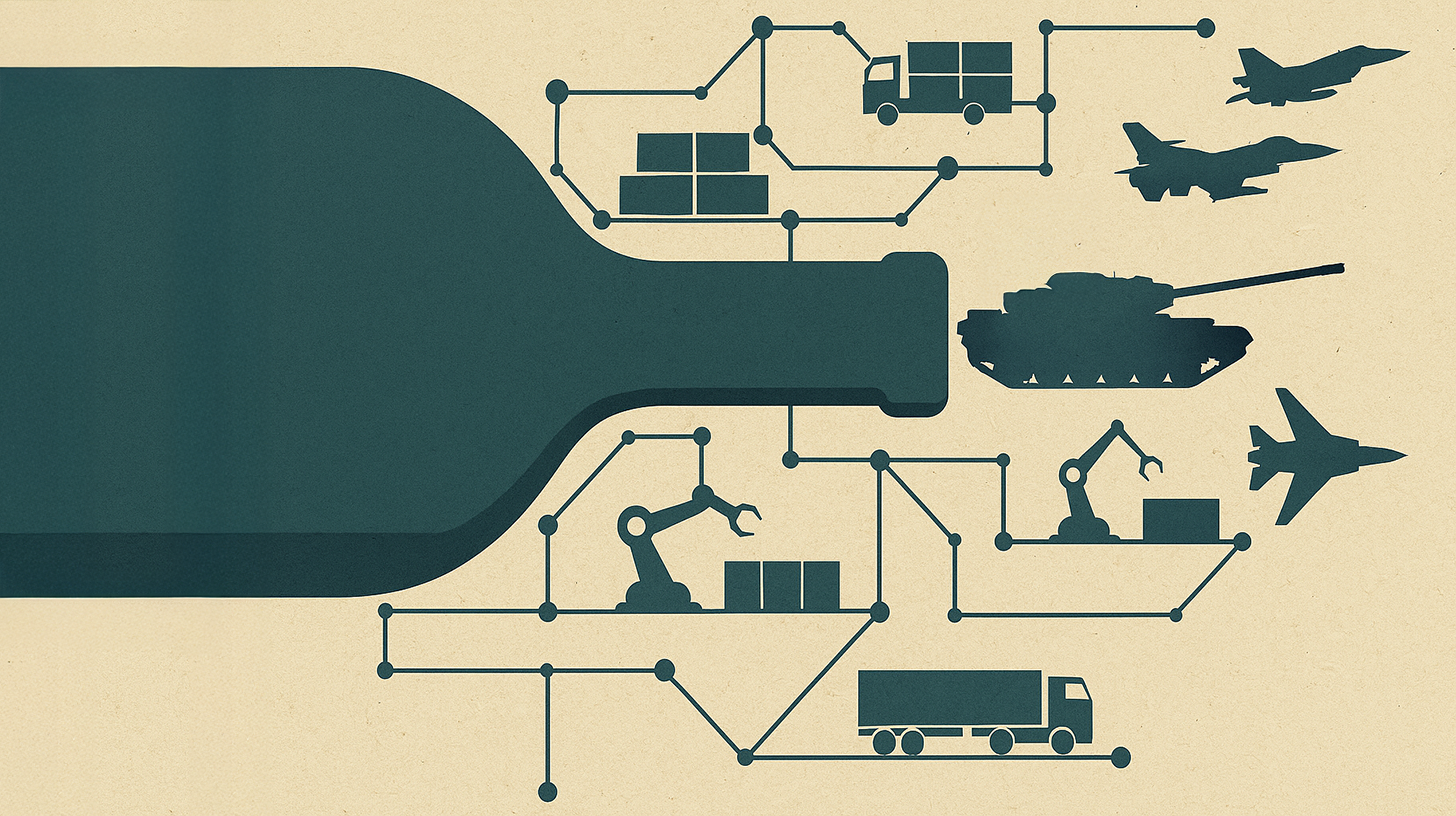

If the bottleneck is not at the top, but in the foundation

The German defense industry is facing a historic turning point. While billions are flowing into new production lines and order books are overflowing, the true success of this paradigm shift will not be decided at the workbenches of the large system houses. Rather, it will be decided in the small, specialized companies at the lower supply chain levels – where precision parts, seals, and brackets are manufactured. Anyone discussing production increases today must understand that speed is not achieved through more machines, but through the way companies collaborate along the entire value chain.

From prototype to production: How the industry is reaching its structural limits

The roots of the current challenge reach far back. For decades, the German defense industry focused on small production runs, prototypes, and highly specialized, one-off solutions. After the end of the Cold War, defense budgets shrank continuously, manufacturing capacities were reduced, and an industrial base for mass production was deemed dispensable. The result was a specialization geared towards low production volumes and long development cycles.

With the turning point in 2022, the situation changed fundamentally. Russia's war of aggression against Ukraine made it clear that Europe urgently needed to strengthen its defense capabilities. Germany announced a special fund of 100 billion euros, and NATO called for an increase in defense spending to at least two percent of gross domestic product. For 2026, Germany is planning a defense budget of over 108 billion euros – a historic figure corresponding to approximately 2.2 to 2.3 percent of GDP.

This sudden surge in demand hit an industry that was structurally unprepared for it. While large companies like Rheinmetall, KNDS, or Hensoldt have sufficient resources, stable processes, and the necessary expertise, the real bottleneck lies further down the supply chain. It lies with the highly specialized Tier 2 and Tier 3 suppliers – those often family-run, medium-sized businesses that manufacture add-on parts, fasteners, or high-precision optical components.

These companies possess specialized knowledge and individual manufacturing processes developed over decades that cannot be replicated quickly. Establishing a second source, i.e., an alternative supplier, is often neither technically nor economically feasible in the short term. The combination of dependency, know-how monopoly, and lack of scalability makes these companies critical, yet difficult to replace, links in the industrial chain. If even one of these companies cannot expand its capacity or reaches its quality limits, the entire production process comes to a standstill.

In addition, there are structural bottlenecks in raw materials. Tank steel must be ordered at least a year in advance. Delivery times for stainless steel and special alloys have increased dramatically in recent years, and prices have risen to record highs. China has also tightened its export regulations for rare earth elements, which poses further challenges for the German defense industry.

The anatomy of modern defense supply chains: Complexity as a systemic risk

Modern defense supply chains follow a hierarchical structure divided into several levels. At the top are the OEMs (Original Equipment Manufacturers) – the large system houses such as Rheinmetall, KNDS, Thyssenkrupp Marine Systems, or Hensoldt. These companies develop and integrate complete weapon systems and deliver them directly to the German Armed Forces or other armed forces.

Directly below are the Tier 1 suppliers, who deliver complex modules and systems to the OEMs – such as drive systems, electronic modules, or weapon control systems. These companies often have a close development and production partnership with the system integrators.

Tier 2 suppliers are component suppliers who deliver individual assemblies to Tier 1 suppliers – for example, electronic components, hydraulic components, or steel components. At the lowest level, Tier 3 suppliers are parts suppliers who provide raw materials or standard components such as screws, seals, or fasteners.

This structure is highly interconnected and interdependent. A failure at the lowest level can have cascading effects on the entire chain. The complexity is exacerbated by the fact that many Tier 2 and Tier 3 suppliers do not work exclusively for the defense industry, but also for the automotive, mechanical engineering, or aerospace sectors. This leads to competition for limited capacity, especially during periods when several industries are experiencing simultaneous growth.

The defense industry also has specific requirements for quality, documentation, and traceability that go beyond civilian standards. Every component must be fully documented, and supply chains must be transparent and originate from NATO member states for security reasons. This significantly increases the demands on suppliers and makes it difficult for smaller companies to enter the defense industry without support.

A turning point under pressure: The current situation between boom and shortage

The German arms industry is currently experiencing an unprecedented boom. Rheinmetall's revenue increased by ten percent in 2023, and the company's share price has multiplied since the Russian attack on Ukraine. Hensoldt, the radar specialist from Ulm, plans to increase its production capacity for radar systems fivefold to approximately 1,000 units per year by 2027, creating up to 200 new jobs in the process.

Satellite images across Europe paint a similar picture: since the start of the war in Ukraine, over seven million square meters of new industrial space for arms production have been developed. This expansion is being promoted by public subsidies, particularly through the EU's ASAP (Act in Support of Ammunition Production) program, which has a funding volume of €500 million. The new European Defence Industry Programme (EDIP) will provide a further €1.5 billion until 2027.

But behind these impressive figures lie structural challenges. Production capacities cannot be ramped up as quickly as politicians demand. Rheinmetall plans to increase its artillery ammunition production twentyfold by 2026 – from 70,000 rounds in 2022 to 1.1 million rounds annually by 2027. But even this massive increase would not cover half of Ukraine's estimated demand of two to 2.4 million rounds per year.

The problem doesn't primarily lie with the large system integrators, but with their suppliers. Sebastian Schaubeck, Managing Director at ACS Armoured Car Systems, explains: If you can rely on existing supply chains and utilize shift work models, expansion can be relatively quick – in less than twelve months. However, if new halls need to be built, permits obtained, and machinery procured, such an expansion can easily take more than 24 months.

Added to this is the shortage of skilled workers. Rheinmetall is looking for more than 3,500 new employees, and the German Armed Forces are competing with industry for qualified personnel. While the simultaneous crisis in the automotive industry offers opportunities for the defense sector – Hensoldt CEO Oliver Dörre reports talks with Continental and Bosch about taking over employees – the transferability of skills is limited and requires training measures.

Supply chain resilience is another critical issue. Many suppliers rely on components from China, which poses a significant risk given geopolitical tensions. Peter Wambsganß of etatronix emphasizes the importance of resilient supply chains: Recent crises have demonstrated the crucial importance of keeping the value chain as closed as possible within NATO member states. His company develops and manufactures military products entirely in Germany and consistently uses components from NATO member states.

From practice: Success models and learning areas

A look at practical examples shows that successful approaches already exist, but have not yet been implemented across the board. The automotive industry offers valuable experience in this area, particularly regarding the transition to electromobility. Systematic supplier development programs were established there to prepare Tier 2 and Tier 3 suppliers for new requirements. Technical training, maturity models, co-investments, and long-term development agreements helped to raise highly specialized micro-enterprises to the necessary level of quality and processes.

Rheinmetall has introduced a digital procurement portal that streamlines collaboration with suppliers. The platform gives suppliers access to relevant documents, creates transparency in business processes, and offers a direct communication channel. From onboarding and sourcing to contract management, all processes are centralized in one place, increasing efficiency and effectiveness.

In its corporate strategy, KNDS emphasizes the importance of a stable supplier network comprised of renowned component and subsystem manufacturers. Consistent demand guarantees long-term supply and provides planning security for suppliers. This is a crucial factor, as many companies hesitate to invest in capacity expansion until it is clear whether demand will be sustainable.

Another example is the ZEBEL project (Central Bundeswehr Spare Parts Logistics), one of the most successful public-private partnerships of the German Armed Forces. ESG, together with DB Schenker, manages a central warehouse of 17,000 square meters, thus representing a positive example of effective cooperation between a public client and industry to increase effectiveness and efficiency.

However, there are also challenges. Ukraine demonstrates that even massive investments do not automatically lead to full capacity utilization. Despite a tenfold increase in production value from 2021 to 2024, reaching over ten billion euros, capacity utilization is only around 40 percent. Reasons for this include inadequate protection of production facilities, a lack of financing, and shortages of raw materials such as gunpowder.

Hub for Security and Defense - Advice and Information

Hub for Security and Defense - Image: Xpert.Digital

The Security and Defence Hub offers expert advice and up-to-date information to effectively support companies and organizations in strengthening their role in European security and defence policy. Working closely with the SME Connect Defence Working Group, it particularly promotes small and medium-sized enterprises (SMEs) that wish to further develop their innovative capacity and competitiveness in the defence sector. As a central point of contact, the Hub thus creates a crucial bridge between SMEs and European defence strategy.

Related to this:

The invisible backbone: Why Tier-2 and Tier-3 decide on security

System failure or system change? A critical examination

Despite the boom and political declarations of intent, there are significant criticisms of the supply chain management in the German arms industry. One of the central criticisms is that supplier management is still widely understood as a mere purchasing discipline and not as a strategic task of corporate management.

A study commissioned by the German Federal Ministry of Defense uncovered numerous risks in central procurement processes. Criticism focuses primarily on a lack of transparency, excessive bureaucracy, and insufficient planning certainty. Klaus-Heiner Röhl of the German Economic Institute emphasizes: Industry needs long-term perspectives backed by orders. Discussions about increased defense spending don't benefit manufacturers much.

A structural problem is the lack of systematic development of supplier structures, particularly at the lower levels of the value chain. While large Tier 1 suppliers are generally well-positioned, smaller Tier 2 and Tier 3 companies often lack the necessary resources for qualification, certification, and capacity expansion.

The automotive industry demonstrates that Tier 3 suppliers are often smaller and less diversified – both in terms of their customers and their production facilities. Their biggest challenge is rapidly rising energy and material prices. Furthermore, they are bound by annual price agreements with their customers and lack a unique selling proposition. This limits their ability to pass on cost increases in the short term.

Another point of criticism concerns the lack of transparency along the supply chain. A study by Forrester Consulting found that only 13 percent of the companies surveyed rate their supplier management as leading-edge – with formal programs that are consistently applied across their entire supply base. Without robust supplier management programs, companies risk disrupted supply chains, compliance issues, and missed opportunities for cost savings or innovation.

The arms industry also faces ethical questions. The sudden shift of industrial capacity from civilian to military production raises questions about Germany's long-term economic strategy. Critics warn that an excessive focus on arms production could lead to a structural dependence on conflict-driven demand.

Finally, there are concerns regarding the timeline. Leading generals indicate that a further Russian escalation could occur between 2027 and 2030 at the latest. By then, the German armed forces would need to be ready for combat. The question is whether the defense industry and its supply chains can be ramped up quickly enough to meet this deadline. Experience shows that building up capacity at suppliers takes at least 12 to 24 months – and that's assuming that permits, financing, and skilled personnel are available.

Digitalization, AI and autonomous systems: The next stage of evolution

The future of arms supply chains will be significantly shaped by technological innovations. Artificial intelligence, digital platforms, and autonomous systems offer enormous potential for increasing efficiency and minimizing risk. China, with its strategy of "intelligentization," has built a lead in this area that is forcing Europe to rethink its approach.

The integration of AI into all facets of military operations, including logistics, is a central element of Chinese modernization. AI is being used for predictive logistics, autonomous resupply, and optimized resource allocation in dynamic environments. Studies indicate efficiency gains of 20 percent or more.

Europe and Germany need to catch up in this area. Rheinmetall has taken a first step towards networked, digitized warfare with its Battlesuite software solution. The platform aims to improve military communication and data analysis by linking all relevant information and connecting all users relevant on the battlefield.

Digital platforms offer significant advantages in supply chain management. Establishing systems for recording and monitoring delivery status, risks, quality indicators, and capacities along the entire value chain creates the necessary transparency for effective control. Cloud technologies, collaborative platforms, and common standards for data exchange promote transparent, real-time communication.

Blockchain technology could provide decentralized, transparent, and tamper-proof documentation of transactions. This offers significant potential, particularly in the defense sector, where traceability and compliance are paramount.

The introduction of AI for predictive maintenance is another important trend. By predicting component failure before it occurs, unplanned downtime can be reduced, costs saved, and operational reliability increased.

Autonomous supply systems – UAVs for critical air support and robots for warehousing and transport in hazardous environments – are already under development. Rheinmetall already has systems in its portfolio in this area, including the HERO series of loitering munitions and the LUNA NG reconnaissance drone.

The challenge lies in implementation. Europe needs a committed, well-equipped strategy for smart logistics, not just isolated projects. This requires, first and foremost, the availability of standardized, accessible, and secure data – a fundamental prerequisite for the effective use of AI at the coalition level.

The European Defence Agency and NATO are working on common standards and interoperability. The European Defence Industry Programme (EDIP) explicitly provides funding for digital transformation and technological innovation.

However, there are also risks. The excessive dependence on a few global providers in the field of software and AI technologies is a warning sign. Technological sovereignty – the ability to develop and manufacture key technologies in Europe – is increasingly becoming a strategic imperative.

Digital transformation is not an end in itself, but a necessity to remain competitive in the global market. Those who invest in digital supply chain technologies today are laying the foundation for tomorrow – both in defense and in the civilian economy.

The foundation of resilience: Why supply chains determine security

The analysis clearly shows that the German and European defense industry is at a turning point. This paradigm shift is not just a political platitude, but an industrial reality. The challenge lies less in technological expertise or financial resources than in the systematic development and management of supplier structures.

The bottleneck isn't with the large system integrators, but with the highly specialized companies at the lower supply chains. These Tier 2 and Tier 3 suppliers are the backbone of the industry – irreplaceable, but often invisible. Their ability to scale determines whether political announcements actually translate into deliveries.

The solution lies in a fundamental paradigm shift. Supplier management must no longer be understood as a mere purchasing discipline, but must be anchored as a strategic task of corporate and governmental leadership. This encompasses five key areas of action:

First, capacity building and redundancy management. Expanding additional production capacity must be done jointly with key suppliers across all stages. At the same time, redundancies must be created to reduce dependence on individual suppliers.

Secondly, qualification and development programs. Lower supply chain levels require targeted support through technical training, maturity models, co-investments, and long-term development agreements. The automotive industry has achieved significant success with similar programs during the transition to electromobility.

Thirdly, transparency and real-time control. The development of digital platforms for recording and monitoring delivery statuses, risks, quality indicators, and capacities along the entire value chain is essential. Only those who understand their supplier landscape through data can manage it effectively.

Fourth, cooperative value creation and incentive systems. The development of long-term partnerships through joint development initiatives, technology partnerships, and performance-based incentive systems replaces short-term purchasing thinking.

Fifth, institutionalized governance. Anchoring supplier management not only in the purchasing strategy, but also in strategic corporate management – with clear roles, competencies and responsibilities, regular audits and reporting obligations across all hierarchies.

The greatest potential lies not in new technologies, but in new connections. Those who understand cooperation as a strategic capability will ensure speed, quality, and reliability in the long term. Competitiveness is not determined at the top of the supply chain, but at its foundation.

Supply capability is no accident. It is the result of transparency, systematic development, and a shared commitment to shaping the future. The European defense industry can continue in a mode of individual optimization – or it can seize this turning point to jointly redesign its industrial base. The decision is being made today. The consequences will shape European security for decades to come.

Consulting - Planning - Implementation

Markus Becker

I would be happy to serve as your personal advisor.

Head of Business Development

Chairman SME Connect Defense Working Group

Consulting - Planning - Implementation

Konrad Wolfenstein

I would be happy to serve as your personal advisor.

You can contact me at wolfenstein∂xpert.digital or

Just call me on +49 7348 4088 965 .

Your dual-use logistics experts

Dual-use logistics experts - Image: Xpert.Digital

The global economy is currently undergoing a fundamental transformation, a watershed moment that is shaking the foundations of global logistics. The era of hyper-globalization, characterized by the relentless pursuit of maximum efficiency and the "just-in-time" principle, is giving way to a new reality. This new reality is marked by profound structural breaks, geopolitical power shifts, and increasing fragmentation of economic policy. The once taken-for-granted predictability of international markets and supply chains is dissolving and being replaced by a period of growing uncertainty.

Related to this: