Amazon capitulates to the China offensive: The fee reduction as a strategic survival maneuver – Image: Xpert.Digital

Historic fee cut: What Amazon sellers absolutely need to know starting in December

The great fee illusion: How Amazon recoups the gifted money elsewhere.

It's a shockwave running through the world of e-commerce – and the epicenter isn't in Seattle, but in the factories of China.

For years, Amazon was considered the undisputed ruler of Western online retail. Its dominance seemed unassailable, its pricing power absolute. But that era of security is over. With the announcement of massive fee cuts for European retailers, the tech giant is currently executing one of the most radical strategic U-turns in its history. What at first glance appears to be an early Christmas present for struggling retailers, on closer inspection reveals itself to be a ruthlessly calculated defensive maneuver against an existential threat: the aggressive expansion of Temu and Shein.

The challengers from the Far East, with their ultra-fast fashion and discount models, have not only conquered market share but have also reshaped the consumer behavior of entire generations. Amazon now finds itself forced to fundamentally recalibrate its business model, which for a long time was based on steadily increasing fees. But caution is advised: While logistics costs are falling, advertising expenditures are exploding. We are not seeing a reduction in overall costs, but rather a complex reallocation of revenue streams – away from logistics and towards the media budget.

The following analysis reveals what's really happening behind the scenes of this economic thriller. It sheds light on how Amazon is trying to stem the Chinese tide, the role new customs laws play in this, and why retailers shouldn't be celebrating but urgently rethinking their strategies. Welcome to the new reality of digital commerce.

Related to this:

When the giant trembles: Why Amazon's supposed generosity is an admission of vulnerability

Amazon's announcement of one of the largest fee cuts in its history for European sellers, starting in December 2025 and February 2026, marks a tectonic shift in the global e-commerce ecosystem. With average savings of €0.17 per unit sold in Europe, reduced FBA package fees of around €0.32, and referral fees partially halved in high-growth categories, the platform giant is signaling a fundamental recalibration of its business model. These measures, however, are by no means an expression of corporate philanthropy, but rather a calculated response to an existential threat emanating from Chinese factories, via the smartphones of Western consumers, and directly into the heart of the Amazon ecosystem.

The dynamics unfolding in global online retail deserve in-depth economic analysis, as they reveal nothing less than the reshaping of the digital commerce architecture. Within just a few years, Temu and Shein have conquered market positions that were traditionally considered unassailable. The competitive pressure forcing Amazon to take this step is merely the visible tip of an iceberg encompassing changing consumer preferences, disruptive business models, and geopolitical upheavals, the full impact of which will only become apparent in the coming years.

The erosion of market dominance: How Chinese platforms are changing the rules of the game

The rise of Temu and Shein is not simply a gradual shift in market share, but rather the foundation of an alternative paradigm for digital commerce. The numbers speak for themselves: Among consumers who shop at both Amazon and Shein, Amazon's share of orders fell by 34 percent in just 18 months. While Amazon still accounted for 71 percent of orders from this customer group in January 2023, this figure had dropped to just 47 percent by June 2024. This development signals a fundamental shift in consumer behavior that goes far beyond temporary market fluctuations.

In Germany, Temu nearly quadrupled its gross trading volume within a year, reaching €3.4 billion in 2024, which propelled it from eleventh to fifth place among online marketplaces. Shein improved its ranking of the largest German online shops from 18th to seventh place, with an 18 percent increase in revenue to €1.1 billion. Net purchase intent for Shein and Temu is on average 18 percentage points higher than that of established competitors, indicating further growth potential.

The global success of these platforms is based on a radically different business model. Temu operates on a consignment model, where manufacturers send products to Chinese warehouses without Temu purchasing them upfront. The platform acts as a reseller without actually owning the products, with unsold goods being returned to the factories. This model virtually eliminates all capital tied-up risks and allows for pricing that can be 70 percent lower than comparable products on Amazon. Temu's global gross merchandise volume exploded from $14 billion in 2023 to $70.8 billion in 2024.

The reaction of European consumers to these offerings is clear: According to the Bank of England-McKinsey State of Fashion 2024 consumer survey, 40 percent of US consumers have already shopped at Shein or Temu in the last 12 months. In the United Kingdom, this figure is 26 percent. For the German market, current analyses show that foreign online marketplaces now account for 10 percent of total e-commerce volume, with Temu and Shein together generating revenues of between €2.7 and €3.3 billion. Temu's reach has already encompassed 27 percent of German online shoppers in a very short time.

Anatomy of the fee reductions: What Amazon is specifically reducing

The technical details of the announced fee reductions clarify the strategic thrust of Amazon's counter-offensive. From December 15, 2025, FBA fulfillment fees for parcels in Germany, Great Britain, France, Italy, and Spain will be reduced by an average of €0.32 per shipment. This measure builds on parcel fee reductions already introduced in 2025 and signals a deliberate cost-cutting effort in its core business.

Referral fees, or sales commissions, are being drastically reduced in strategically relevant categories. For clothing and accessories, the fees will decrease from 8 to 5 percent for items up to €15 and from 15 to 10 percent for items between €15 and €20. From February 2026, referral fees for home products will be reduced from 15 to 8 percent for items up to €20, for pet clothing and food from 15 to 5 percent for items up to €10, and for groceries and gourmet products as well as vitamins, minerals and supplements from 8 to 5 percent for items up to €10.

Particularly significant is the expansion of low-price FBA rates to products with a selling price of up to €20, which translates to an additional average saving of €0.40 to €0.45 per unit. This measure directly targets the price segment where Temu and Shein excel. Amazon's official communication emphasizes that these reductions reflect its own cost reductions through operational efficiency improvements and represent an alignment of European fee structures with changes in other markets, including the US.

However, the fee reductions are not across the board. Selective increases in monthly storage fees, return-to-seller fees, and liquidation fees result in an average increase of €0.02 per FBA-sold unit. This asymmetrical structure illustrates Amazon's strategic calculation: The platform optimizes the cost structure for fast-moving, low-margin products, while charging higher fees for slower-moving or more problematic assortments. This promotes a more efficient network and simultaneously discourages the storage of slow-moving inventory.

The advertising ecosystem as a monetary compensation mechanism

The fee reductions for fulfillment and commissions represent only one side of the economic equation. The other, far more profitable side is Amazon's explosively growing advertising business. In the third quarter of 2025, advertising revenue reached a new record of $17.7 billion, an increase of 24 percent compared to the same quarter of the previous year. This sum surpasses the total annual advertising revenue of holding companies like IPG or Omnicom and is on par with Publicis.

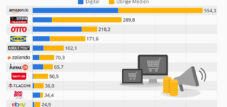

The strategic importance of advertising for Amazon can hardly be overstated. In 2024, Amazon generated $56.2 billion in advertising revenue globally, a 20 percent increase over the previous year. In Germany, advertising revenue reached a record-breaking €3.62 billion, representing growth of 23.6 percent, while the company's total revenue in the country rose by only 8.7 percent. Advertising now accounts for over 9 percent of Amazon's revenue in Germany, approaching the total revenue of Otto, its traditional main competitor in German e-commerce.

This development has far-reaching consequences for Amazon sellers. The average cost per click (CPC) for Amazon Ads will be $1.04 in 2025, a slight increase compared to the previous year. The advertising cost per sale (ACoS) varies considerably by category and level of competition, with averages of around 16 percent for Sponsored Products, 17 percent for Sponsored Brands, and 23 percent for Sponsored Display. A common rule of thumb recommends that sellers budget for advertising costs between 10 and 20 percent of their revenue.

The mechanics of this system create a self-reinforcing cycle: more advertising leads to more orders, which in turn lead to higher organic rankings, generating even more orders and a larger advertising budget. This feedback loop makes Amazon advertising virtually unavoidable for any seller who wants to remain visible on the platform. A study by Marketplace Pulse shows that the average percentage Amazon takes from each sale has increased from one-third in 2016 to over 50 percent in 2022, with advertising accounting for an increasing share of these costs.

The economics of platform dependency: A systemic risk for retailers

The economic reality for Amazon sellers has fundamentally changed. In 2014, Amazon retained 19 percent of seller revenue; by the first half of 2023, this share had risen to 45 percent. Total revenue from third-party fees reached an astronomical $140 billion in 2023 and exceeded $150 billion in 2024. If this revenue stream were a standalone company, it would rank among the Fortune 25.

The cost structure of a typical Amazon seller is as follows: a 15 percent transaction fee (referral fee), 20 to 35 percent for Fulfillment by Amazon including storage and other fees, and up to 15 percent for advertising and promotions. Some sellers report paying Amazon a total of 60 to 70 percent of their revenue, and then still have to cover inventory, shipping, staff, and other expenses.

FBA fees for standard products have increased by 96 percent since their introduction, and for oversized products by 74 percent. Removal fees, the cost of removing inventory from Amazon's warehouses, have skyrocketed by 460 percent. In 2024, additional fees were introduced, including a low inventory fee of $0.32 to $1.11 for inventory holdings of less than one month, an inbound placement fee for receiving stock, and fees of $3 to $5 for products with high return rates.

This systematic increase in fees creates a classic lock-in effect. The platform offers merchants advantages such as access to a huge customer base, optimized logistics, and simplified payment processing. At the same time, proprietary technologies, contractual obligations, and the need to become accustomed to certain processes result in significant switching costs. Merchants are familiar with the platform, know they can find almost any product, and save themselves the hassle of registering with multiple providers. These factors significantly reduce the likelihood of switching to alternative sales channels.

🎯🎯🎯 Benefit from Xpert.Digital's extensive, five-fold expertise in one comprehensive service package | BD, R&D, XR, PR & Digital Visibility Optimization

Benefit from Xpert.Digital's extensive, five-fold expertise in a comprehensive service package | R&D, XR, PR & Digital Visibility Optimization - Image: Xpert.Digital

Xpert.Digital possesses in-depth knowledge across various industries. This allows us to develop tailored strategies precisely aligned with the requirements and challenges of your specific market segment. By continuously analyzing market trends and monitoring industry developments, we can act proactively and offer innovative solutions. The combination of experience and expertise generates added value and provides our clients with a decisive competitive advantage.

More information here:

How tariffs and the end of the de minimis rule will be a game changer for Temu, Shein and Amazon Haul

Geopolitical dimension: Customs policy as a game changer

The competitive landscape between Amazon and Chinese platforms is significantly influenced by geopolitical developments. On May 2, 2025, the US government revoked the de minimis exemption for shipments from China, Hong Kong, and Macau, which had previously allowed duty-free imports of goods under US$800. This regulation was a cornerstone of the business model of Temu and Shein, which were able to achieve extreme price advantages through direct shipping from China without customs duties.

As of August 29, 2025, the de minimis exemption was lifted worldwide for all imports into the US, resulting in tariffs on all imports regardless of value or country of origin. For China, significant tariffs remain in place following a temporary reduction from 145 to 30 percent under a 90-day trade agreement, fundamentally impacting the pricing structure of Chinese platforms.

The effects were immediately noticeable. In April 2025, Temu and Shein raised prices on numerous products and temporarily suspended direct shipping from China to the US. The companies reduced their advertising spending in the US and shifted their focus more strongly to Europe. Analyses by Tech Buzz China show that Temu loses part of its competitive advantage if tariffs exceed 50 percent.

The European Union is also planning adjustments. The de minimis threshold of €150 is to be abolished as an early result of the customs code reform as early as the first quarter of 2026. This development would curb the flood of parcels from foreign online retailers and create greater fairness in customs duties, but at the same time significantly worsen the cost structure for Chinese direct shippers.

Despite these regulatory hurdles, the Chinese platforms are proving resilient. Temu has adapted its strategy, increasingly relying on local US warehouses where import duties have already been paid. Temu's EU GMV is projected to exceed $15 billion by 2025, with potential growth to over $20 billion by the end of 2026. Shein is expanding in the UK, with revenues exceeding £2 billion and growth of 32 percent.

Related to this:

Amazon Haul: The Cheap Offensive as a Defensive Strategy

In direct response to Temu and Shein, Amazon launched its own discount platform called Amazon Haul in November 2024. Accessible exclusively through its mobile app, it offers products for under $20. The majority of products cost less than $10, with some available for as little as $1 or $2. Unlike regular Amazon orders, Amazon Haul customers should expect delivery times of one to two weeks, as the products are shipped directly from Chinese warehouses.

This model deliberately copies the strategy of its Chinese competitors: low prices through direct shipping from China at the expense of delivery speed. Shipping is free for orders over US$25, orders over US$50 receive a 5% discount, and orders over US$75 receive a 10% discount. Items under US$3 cannot be returned.

The strategic logic behind Amazon Haul is defensive in nature. Neil Saunders of GlobalData describes the initiative as Amazon's response to the emerging Chinese marketplaces that have gained a foothold among price-conscious consumers. He argues that it's better for Amazon to cannibalize its own sales than to lose market share to the competition. Furthermore, Amazon Haul could resonate with younger consumers who frequently shop on competing platforms.

Amazon Haul initially benefited from the de minimis rule as well. After its abolition, the platform expanded into the UK and Saudi Arabia, while its US business faces higher costs. The future of Amazon Haul is therefore closely tied to developments in US-China trade relations and global customs regimes.

Market consolidation: Winners and losers

Despite disruption from Chinese providers, the German e-commerce market is showing remarkable growth momentum. The top 1,000 B2C online shops increased their net e-commerce revenue from €77.5 billion in 2023 to €80.4 billion in 2024, a nominal growth of 3.8 percent. Further growth of 5.3 percent is projected for 2025, with the German Retail Federation (HDE) expecting a total market size of €92.4 billion.

Market concentration is increasing significantly. The ten highest-grossing shops grew by 8 percent, while the remaining 990 shops only increased by 1.3 percent. The market share of the top 10 is 38.8 percent, and the top 100 generate 70.7 percent of total revenue. Amazon dominates German e-commerce with an estimated market share of approximately 60 percent of online retail.

The impact of this consolidation on smaller retailers is significant. An analysis by Marketplace Pulse shows that while the number of Amazon sellers is declining, successful sellers are generating higher revenues than ever before. In 2024, 5,700 sellers achieved annual sales of at least $10 million on a single Amazon marketplace for the first time, compared to 3,600 in 2021. The number of sellers with at least $100 million in annual sales increased from 50 in 2021 to 230.

This development points to a professionalization and scaling of the Amazon ecosystem. Those who adapt to the numerous requirements, rising fees, and high margin pressure can achieve disproportionate profits. At the same time, Amazon is evolving from a platform for entrepreneurial experimentation into a professional infrastructure for established retailers. Traffic per seller increased by almost a third, suggesting that successful sellers have less to compete for customer attention.

Strategic options: Diversification as a survival principle

The structural dependence on Amazon poses a systemic risk for retailers, which can be mitigated through strategic diversification. The direct-to-consumer (D2C) channel is gaining importance, with US D2C e-commerce sales projected to reach $239.75 billion in 2025, representing 19.2 percent of total retail e-commerce. Owning the checkout experience and first-party data is increasingly becoming a prerequisite for growth.

Multichannel strategies offer significant advantages: increased reach and visibility, risk minimization through diversification of sales channels, improved customer experience through freedom of choice, higher revenue potential, and valuable data insights from various sources. Studies show that customers who shop across multiple sales channels spend an average of 30 percent more than customers who use only one channel. A personalized multichannel strategy can lead to a 5 to 15 percent higher conversion rate and 10 to 30 percent higher customer satisfaction.

The combination of Vendor Central and Seller Central on Amazon, the so-called hybrid model, allows for a more flexible and broader distribution of risk. Bestsellers or core products with high sales volume can be sold via Vendor Central, while products with lower volume or lower margins are offered in Seller Central. New products can be tested in Seller Central and, after an evaluation phase, potentially transferred to the Vendor program.

Retail media beyond Amazon is developing into a significant growth area. Walmart Connect is increasingly becoming a competitor for Amazon, with 46 percent of advertisers using Walmart Connect in 2024, compared to 24 percent in 2023. Walmart's advertising business grew by almost 30 percent in 2024, a pace that surpasses Amazon's. In Germany, platforms such as Zalando, Otto, Douglas, and Rewe are also massively expanding their advertising systems.

The platform dilemma: Between dependence and autonomy

The economic analysis of Amazon's fee reductions reveals a fundamental paradox of platform capitalism. Merchants benefit in the short term from reduced fulfillment and commission costs, but at the same time, they are more deeply integrated into Amazon's advertising ecosystem. Amazon compensates for the relief from traditional fees through accelerated growth in its highly profitable advertising segment, which operates with margins that significantly exceed those of its core business.

Amazon's business model has evolved from a pure marketplace into an integrated ecosystem that combines e-commerce, fulfillment, advertising, and digital services. Its multiple revenue streams include third-party fees, fulfillment services, advertising, Prime memberships, and AWS, each with different profitability profiles. Prime membership, with over 200 million paying members worldwide and an annual fee of $139, generates approximately $30 billion in recurring revenue.

This diversification makes Amazon resilient to market fluctuations. Even if retail sales decline, Prime subscriptions, advertising, and AWS ensure stable profits. For merchants, however, this resilience of the platform means increased dependence, as alternative channels generally do not achieve Amazon's reach or conversion rates.

The consequence for retailers is a constant balancing act between the advantages of the platform's reach and the risks of dependence. Amazon offers access to millions of customers, standardized payment processing, efficient logistics, and established customer trust. At the same time, the platform controls the rules of the game, can adjust fees and algorithms at any time, and collects data that can potentially be used to develop competing private-label brands.

The reorganization of digital commerce

Amazon's fee reductions mark a turning point with long-term implications extending beyond the immediate competitive landscape. Chinese platforms have demonstrated that alternative business models can put even established e-commerce giants under pressure. This disruption is forcing Amazon to recalibrate its pricing and fee structures, which will benefit retailers in the short term.

The development of tariff policies in the US and Europe will significantly determine the future competitiveness of Temu and Shein. The elimination of de minimis exemptions considerably increases the cost base of the Chinese platforms and could partially erode their price advantages. At the same time, the companies are demonstrating remarkable adaptability by shifting to local warehousing and expanding into markets with more favorable regulatory environments.

This dynamic creates clear strategic imperatives for retailers. Leveraging the current fee reductions to optimize product ranges and pricing makes sense in the short term. At the same time, dependence on the Amazon advertising ecosystem should be critically evaluated. Developing alternative sales channels, whether through their own D2C shops, a presence on other marketplaces, or retail media partnerships beyond Amazon, will be crucial for long-term profitability and entrepreneurial autonomy.

Whether Amazon can maintain its market dominance in the long term will not be decided solely by its fee structure. The company's future position will be determined by its willingness to adapt to changing consumer preferences, its capacity for technological innovation, and its ability to respond to geopolitical upheavals. The recent fee reductions demonstrate that Amazon is taking these challenges seriously and is prepared to accept short-term margin sacrifices for long-term market share.

The profound transformation of global e-commerce is by no means complete. Rather, we are at the beginning of a phase of intensified competition, in which established players and disruptive newcomers are vying for consumers' favor. For retailers, this development presents both risks and opportunities. Those who understand the structural changes and navigate them strategically can profit from the new competitive intensity. Conversely, those who passively rely on platform mechanisms risk being crushed between the millstones of the price war.

Your global marketing and business development partner

☑️ Our business language is English or German

☑️ NEW: Correspondence in your native language!

Konrad Wolfenstein

I and my team are happy to be available to you as your personal advisor.

You can contact me by filling out the contact form here wolfenstein@xpert.digital:or simply call me at +49 7348 4088 965. My email address is

I'm looking forward to our joint project.

☑️ SME support in strategy, consulting, planning and implementation

☑️ Creation or realignment of the digital strategy and digitization

☑️ Expansion and optimization of international sales processes

☑️ Global & Digital B2B trading platforms

☑️ Pioneer Business Development / Marketing / PR / Trade Fairs

Our global industry and economic expertise in business development, sales and marketing

Our global industry and economic expertise in business development, sales and marketing - Image: Xpert.Digital

Industry focus areas: B2B, digitalization (from AI to XR), mechanical engineering, logistics, renewable energies and industry

More information here:

A thematic hub offering insights and expertise:

- Knowledge platform covering global and regional economies, innovation and industry-specific trends

- A collection of analyses, insights, and background information from our key areas of focus

- A place for expertise and information on current developments in business and technology

- A hub for companies seeking information on markets, digitalization, and industry innovations