Amazon will lose market share in Germany for the first time in 2026 – Kaufland, OTTO & eBay strike back – Image: Xpert.Digital

A quiet turnaround in e-commerce: These 3 marketplaces are now stealing market share from Amazon

The Amazon Trap: Why online retailers will fail in 2026 without a multi-channel strategy

Red alert at Amazon? What the historic fee cuts mean for sellers

For more than two decades, Amazon has been the undisputed king of German e-commerce. For countless retailers, the unwritten rule was: whoever wins on Amazon, wins the market. But in 2026, a quiet yet momentous shift is taking place in German online retail. While the giant continues to grow in absolute terms, it is structurally losing market share for the first time. Growth is being redistributed – among players that many had long since written off or significantly underestimated. Kaufland Global Marketplace, OTTO Market, and eBay are attacking with completely different but highly successful strategies, fundamentally shifting the balance of power. The aggressive low-price competition from Temu and Shein plays only a minor role in this. For online retailers, this development represents a fundamental turning point: those who continue to focus their business exclusively on Amazon are taking a dangerous concentration risk. This article analyzes the new power dynamics, explains why Amazon is suddenly reacting with historic fee reductions, and shows what a future-proof and profitable multi-channel strategy for 2026 must look like.

Three platforms, one message: Those who don't diversify today will lose tomorrow

The seemingly invincible giant and his first real moment of weakness

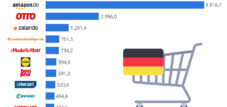

Amazon has been the dominant force in online retail in Germany for more than two decades. With a market share of around 60 percent of German e-commerce – divided into 17 percent direct sales and 43 percent marketplace revenue – the platform has remained not only the most important, but simply the only relevant sales channel for many retailers. This dependence was economically rational for a long time: No other marketplace offered comparable reach, logistics infrastructure, and customer loyalty. But in 2026, the landscape will fundamentally change.

Amazon generated sales of approximately €40.6 billion in Germany in 2025, representing growth of eight percent. In absolute terms, the company continues to grow. The crucial question, however, is not whether Amazon is growing – but whether Amazon is growing faster than the market. And this is where the picture begins to shift. While the entire German e-commerce market is expected to grow by around four percent in 2026, this growth is being distributed among an increasing number of players. For the first time in the platform's recent history, three specific marketplaces are structurally gaining ground: Kaufland Global Marketplace, OTTO Market, and eBay. None of these three will pose a threat to Amazon in the foreseeable future. Together, however, they are shifting the balance of power in German online retail to an extent that retailers now need to understand.

When market share is gained by many instead of one

What's special about the current shift lies in its structure. It's not a revolution driven by a single challenger, as Temu and Shein attempted in the low-price segment. It's a gradual, structurally underpinned diversification of German consumers' purchasing decisions and—more importantly—of the sales strategies of professional online retailers. Online marketplaces in Germany reached a sales volume of €46.2 billion in 2025, an increase of 4.9 percent compared to the previous year, and now 56 percent of all online sales in Germany are conducted via marketplaces. This growth no longer benefits Amazon exclusively.

The German Retail Federation (HDE) and the Cologne-based EHI Retail Institute measured growth of almost 3.5 percent in German e-commerce for 2024. For 2025, EHI and ECDB even predicted a nominal increase of 5.3 percent for the top 1,000 online shops. The market is therefore growing overall – but the contributions to this growth are shifting. While pure-play online retailers faced a decline of 3.6 percent in 2024 and direct sales shrank by 2.3 percent, it was precisely the online marketplace segment that was able to grow. For retailers, this means: those who continue to rely on only a single channel are missing out on structural growth potential.

The average number of active marketplace connections per retailer has already increased from 2.46 in Q1 2024 to 2.52 in Q1 2025. This may sound like a small shift, but it is a clear signal of accelerating professionalization in multi-channel sales.

Kaufland Global Marketplace: The European bet with strategic consequences

Few e-commerce players in Europe pursued expansion as consistently in 2025 as Kaufland Global Marketplace. Following its successful launch in Poland and Austria in 2024, the platform expanded to France in late summer 2025 (August) and shortly thereafter to Italy (September). Kaufland is now active in seven European markets – Germany, Austria, Poland, Czech Republic, Slovakia, France, and Italy – and potentially reaches around 140 million online customers.

What distinguishes this expansion strategy from others is the combination of institutional patience and structural backing. Kaufland belongs to the Schwarz Group, which also owns Lidl, one of the world's largest brick-and-mortar retailers. This foundation enables a platform strategy that is not geared towards quick profitability, but rather towards long-term market penetration. CEO Gerald Schönbucher has clearly articulated the ambition: Kaufland aims to become the largest European online platform and is explicitly positioning itself as an alternative to the global e-commerce giants – from Europe, for Europe.

In 2024, Kaufland Global Marketplace's Gross Merchandise Volume (GMV) grew by 7.85 percent across all marketplace countries. The most successful categories were electronics and computers with 24 percent growth, and garden and DIY with 20 percent. For comparison, Kaufland.de recorded approximately 28.5 million visits per month in March 2025, while Amazon.de reached over 360 million visits – a factor of more than 12 in favor of its American competitor. This discrepancy demonstrates that Kaufland is still far from catching up with Amazon.

For retailers, the strategic added value is obvious: with a single registration, they gain access to 13,000 existing retailers and 140 million potential customers across Europe. Kaufland offers free, automated product data translations, over 70 software interfaces, multilingual support, an automatic lowest price feature, and VAT automation. For medium-sized retailers looking to internationalize their business without the operational complexity of manual country expansion, this is an offer whose practicality is often underestimated.

The decisive differentiating factor compared to Amazon is not its current size, but rather its growth dynamics in markets where Amazon does not yet have a comparably strong position. According to Kaufland, it is experiencing particularly strong growth in Eastern Europe. And any retailer already present on Kaufland in France or Italy benefits from first-mover advantages in a market that is still developing. France is the third-largest e-commerce market in Europe, Italy the fourth-largest – together, these are markets with considerable potential for retailers who take the plunge today.

OTTO Market: Quality over quantity, and why that can be better for retailers

OTTO is perhaps the most underrated chapter in German e-commerce. Anyone still associating OTTO with the image of a traditional mail-order company has missed the platform's development over the past decade. In fiscal year 2024/25, OTTO's gross merchandise volume (GMV) grew by approximately nine percent, from €6.5 billion to over €7 billion. This growth significantly outpaced the overall market, and according to the company, OTTO gained market share. For the current fiscal year 2025/26, OTTO increased its platform revenue again by six percent to approximately €7.5 billion GMV – while German e-commerce as a whole grew by only around three percent during the same period.

OTTO's customer base is remarkable: the platform recently registered 12.6 million active buyers, a four percent increase compared to the previous year. The marketplace now boasts 6,100 partner retailers, with a nine percent GMV growth in the marketplace segment alone. Marketplace business now accounts for 40 percent of total GMV. The Fashion and Sports categories, with nine percent GMV growth, and the Home and Living categories, with seven percent, performed particularly well.

What structurally distinguishes OTTO from Amazon is the buyer profile. The average OTTO customer buys more consciously, is price-sensitive but not price-driven, and associates the platform with a promise of quality and trust that has grown historically. The Handelsblatt-exclusive NielsenIQ analysis from Black Friday 2025 demonstrated that OTTO – unlike Amazon – experienced virtually no loss in revenue due to the rise of Temu and Shein. This is a remarkable sign of platform resilience and customer loyalty.

For retailers with mid- to high-price points, especially in the home furnishings, fashion, and electronics segments, this means that price competition is less intense on OTTO than on Amazon. Depending on the product range, this can lead to better margins and a higher-quality customer base. OTTO is also investing heavily in AI-powered personalization and has developed its own AI assistant for the shopping experience. The company aims for ten billion euros in revenue by 2028 – an ambition that, if achieved, would make OTTO one of the three or four most important online marketplaces in Europe.

Strategically, OTTO is also gradually opening its marketplace internationally: initially to suppliers from the Netherlands, with Poland, Austria, France, and Spain to follow later. This internationalization will also create new cross-border opportunities for retailers in the medium term, which are currently receiving little attention.

eBay: The underestimated reach of a classic platform

In strategic discussions about e-commerce, eBay is often met with a weary smile – as a platform of the past, long since overtaken by Amazon and modern competitors. This perception is simply empirically wrong. eBay.de records around 106 million visits per month and thus remains one of the best-known trading platforms in Germany. Worldwide, 134 million buyers are active on eBay, and 18 million active sellers offer 2.4 billion items.

In the fourth quarter of 2025, eBay reported revenue of approximately three billion US dollars and a GMV of 21.2 billion US dollars – revenue grew by 15 percent and GMV by ten percent compared to the previous year. For the full year 2025, eBay reported revenue of 11.1 billion US dollars and a GMV of 79.6 billion US dollars. Almost half of this revenue came from international business outside the US. Germany is traditionally one of eBay's most important markets worldwide.

Often overlooked, but highly relevant: 40 percent of eBay's gross merchandise volume (GMV) now comes from secondhand and refurbished products. And 86 percent of users have traded used goods on the platform in the past twelve months. This is no coincidence, but rather an expression of a fundamental shift in consumer behavior towards the circular economy and recommerce. eBay has recognized this trend and is investing strategically in AI-powered sales tools and enhanced authentication options to improve the platform's quality.

What makes eBay attractive for retailers is the specificity of search intent on the platform. Those searching on eBay have a more concrete purchase intention in many categories than on a generic marketplace. Price comparisons, specific model numbers, niche segments, and offers that are simply unavailable on Amazon or don't receive sufficient visibility there perform disproportionately well on eBay. The platform continues to hold a firm position among the top five marketplaces for German e-commerce orders – directly behind Amazon and ahead of Temu.

🎯🎯🎯 Data-driven B2B industry hub as a quasi-in-house solution

The quasi-in-house solution: How Xpert.Digital closes operational gaps in B2B marketing and sales – Smart Content-Driven Business - Image: Xpert.Digital

Xpert.Digital is a data-driven B2B industry hub led by Konrad Wolfenstein . The company acts as an external, quasi-in-house solution for industrial partners, closing operational gaps in marketing, content, and sales – without requiring additional resources on the client side.

More information here:

Four-pillar strategy 2026: How retailers can secure revenue beyond Amazon – multi-channel instead of monopoly

The comparative analysis: What distinguishes the three platforms

To structure the strategic decision for retailers, a direct comparison of the key performance indicators is worthwhile:

| platform | GMV Germany/worldwide | Active buyers | Strength | Growth 2024/25 |

|---|---|---|---|---|

| Amazon.de | €51.4 billion (DE) | ~35 million (Germany, estimated) | Reach, Prime, Logistics | 8% |

| OTTO Market | €7.5 billion gross vehicle weight | 12.6 million active | Quality buyers, fashion/living | 6% GV |

| Kaufland Marketplace | Targeted gross merchandise volume (GMV) of approximately €2 billion | 140 million potential customers in the EU | Cross-border, EU expansion | 7,85% |

| eBay.de | €8.9 billion (DE) | 134 million globally | Reach, niches, recommerce | 10% GMV Q4 |

Amazon.de achieves a GMV of approximately €51.4 billion in Germany and reaches an estimated 35 million active buyers in Germany; its strengths lie in its reach, Prime services, and logistics. Growth for 2024/25 is projected at around +8%. OTTO Market has a GMV of €7.5 billion, 12.6 million active customers, and scores points with quality buyers and a focus on fashion and home decor, with GMV growth of around +6%. The Kaufland Marketplace aims for a GMV of approximately €2 billion and can draw on a potential customer base of 140 million in the EU; its strengths are cross-border trade and EU expansion, with projected growth of around +7.85%. eBay.de has a German GMV of €8.9 billion, benefits from approximately 134 million active users globally, and is characterized by its reach, niche offerings, and recommerce. In the fourth quarter, GMV growth of 10% was recorded. These figures illustrate the central argument: None of the three platforms will replace Amazon as the leading force in German e-commerce. Nevertheless, OTTO, Kaufland, and eBay each occupy areas where Amazon exhibits structural weaknesses or offers no convincing solution—for example, European data sovereignty and cross-border capabilities (Kaufland), quality buyers with a clear purchase intention (OTTO), or niche markets, recommerce, and established brand recognition (eBay). Faced with increasing competition, platforms like Amazon are responding not only with investments but also tactically, for example, by reducing fees, to signal that they want to retain merchants and are aware of merchants' willingness to switch to alternative platforms.

Amazon's response: Fee reductions as a strategic signal

The finding that Amazon will face serious pressure for the first time in 2026 is underscored by a remarkable measure taken by the company: At the end of 2025, Amazon announced one of the largest fee reductions in its corporate history. Starting December 15, 2025, FBA shipping fees were reduced by an average of €0.32 per shipment in Germany, France, Italy, Spain, and the UK. At the same time, referral fees (sales fees) in the clothing and accessories category were reduced from eight to five percent for products up to €15 and from 15 to ten percent for products in the €15 to €20 range. Further categories, such as home products, pet food, and groceries and vitamins, followed suit in February 2026.

These fee reductions are not an expression of corporate generosity. They are a direct response to increasing competition and the evident tendency of sellers to migrate to alternative platforms. When Amazon undertakes something as unusual as a systematic fee reduction, it sends a strong market signal: The company knows that its negotiating position as the only relevant alternative is dwindling. For sellers, this is a historic opportunity to leverage their dependence to negotiate better terms while simultaneously developing alternatives – without abandoning their Amazon business.

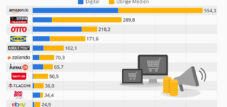

At the same time, Amazon's strategy must be viewed in a broader context. In the German advertising market, Google, Amazon, and Meta will further expand their dominance in 2026 – Amazon will increase its advertising business by ten percent to €2.97 billion net. Retail media will thus become an independent profit engine, making the platform increasingly independent of pure transaction revenues. Amazon is not finished – but it needs to reposition itself.

The Temu Shein Trap: Why cheap competition isn't a permanent issue

An important contextual factor for assessing the current market shifts is the rise and partial collapse of the Chinese platforms Temu and Shein. Since 2023, these platforms have shaken up German e-commerce with their aggressive low-price strategies. At their peak, five percent of orders in German online retail were placed on these two platforms – a figure that more than doubled within a year. An analysis by NielsenIQ based on electronic purchase receipts for Black Friday 2025 showed that Temu customers spent an average of only 38 percent of their shopping budget on Amazon – compared to 45 percent for non-Temu customers.

But the market is correcting. Despite brand awareness of 96 percent for Temu and 93 percent for Shein in Germany, only around 50 percent of those familiar with the brands actually shop there regularly. Customer loyalty is stagnating: Temu's share of buyers remained at 45 percent, while Shein's share even fell from 49 to 45 percent. At the same time, European providers are regaining ground. The fear that Temu and Shein would permanently push German e-commerce into the budget segment has not materialized to the extent feared. What remains is sustained price pressure in the lowest market segment – but no structural displacement of the established players.

The real risk: concentration risk and the illusion of scaling

The central problem addressed in this article is not technical, but strategic. Concentrating roughly 80 percent of sales on a single marketplace was an economically sound decision for many retailers between 2015 and 2022: Amazon grew faster than any alternative, and FBA's operating cost model rewarded concentration. Today, this concentration represents a significant risk that should no longer be accepted uncritically in any professional business model.

The structural risks of Amazon dependency include fee changes that recalibrate the market at short intervals, algorithmic visibility changes that can redistribute organic traffic at any time, and increasing direct competition from Amazon itself in the form of its own-brand products. Added to this are regulatory risks: The European Commission has repeatedly investigated Amazon's marketplace practices from an antitrust perspective. And last but not least, there is the shift in consumer preferences themselves, which, while slow, is inevitably generating more purchases on alternative platforms.

The alternative model – a diversified multi-channel strategy – is not a departure from Amazon. It's a complementary approach that reduces operational risks, opens up new target groups, and ultimately improves the negotiating position with each individual marketplace. According to Destatis, by 2025, 86 percent of 16- to 74-year-olds in Germany would have shopped online, with 70 percent having done so within the previous three months. The customers are there – they're simply spread across more platforms than ever before.

The four-pillar strategy for 2026 and beyond

A structurally sound marketplace strategy for 2026 doesn't involve abandoning Amazon. It involves replacing dependence with diversification. Specifically, the following positioning is recommended:

Amazon remains the anchor. The platform continues to offer the greatest reach, the most sophisticated fulfillment network, and the strongest customer loyalty through Prime. No ambitious retailer in Germany can afford to ignore Amazon. What needs to change is the proportion of total revenue concentrated on this platform.

Kaufland Global Marketplace is the growth channel for Europe. The platform is currently in its development phase, which means that entry costs are low, first-mover advantages are real, and competition is still manageable for retailers. Those who invest now in Kaufland.fr and Kaufland.it are placing their product catalogs in markets that will be significantly more expensive and competitive in two to three years.

OTTO Market is the premium channel for high-spending target groups. For retailers in the home, furnishings, fashion, household appliances, and sporting goods segments, OTTO offers a target group that buys more consciously, returns less frequently, and is less price-driven. This requires a curated assortment strategy – but in the right categories, it translates into better margins.

eBay is the channel for both reach and niche markets. With 106 million monthly visits in Germany, eBay is far larger than most retailers realize. For specialty products, rare category items, recommerce strategies, and discontinued inventory, eBay is not just relevant—it's often the best option. AI-powered sales tools, which eBay is actively developing, will further lower the barrier to entry for professional retailers.

Structural change without attention: Why 2026 is a turning point year

In e-commerce, there are always years that only become apparent in retrospect as turning points. The year 2020 was such a moment – the pandemic-driven boom accelerated the digitalization of retail by years. The year 2026 could be a similar moment, only quieter, more structural, and therefore harder to grasp.

Amazon is still growing. But the platform's relative increase in importance within German e-commerce is slowing. The combination of Kaufland's expansion in France and Italy, OTTO's growth significantly above the market average, eBay's rebound with strong Q4 figures, and a demonstrably growing multi-channel readiness among professional retailers results in a shift that has so far barely made headlines – but will be considered a structural turning point in three years.

The German online marketplace revenue of €46.2 billion projected for 2025 is no longer just an Amazon phenomenon. It's a general marketplace phenomenon. And anyone seriously analyzing the future of e-commerce must accept that the post-Amazon world isn't necessarily one without Amazon – but one in which Amazon is just one among several relevant players. For retailers starting to build alternative channels today, this isn't a threat. It's the strategic opportunity of the decade.

Your global marketing and business development partner

☑️ Our business language is English or German

☑️ NEW: Correspondence in your native language!

Konrad Wolfenstein

I and my team are happy to be available to you as your personal advisor.

You can contact me by filling out the contact form here wolfenstein@xpert.digital:or simply call me at +49 7348 4088 965. My email address is

I'm looking forward to our joint project.

☑️ SME support in strategy, consulting, planning and implementation

☑️ Creation or realignment of the digital strategy and digitization

☑️ Expansion and optimization of international sales processes

☑️ Global & Digital B2B trading platforms

☑️ Pioneer Business Development / Marketing / PR / Trade Fairs

📈🔵 Ambidexterity or doom: The only management concept that still works in the triple crisis💡

When proven strategies fail: Organizational adaptability in the digital transformation of ambidexterity - Image: Xpert.Digital

We are currently experiencing a period of economic turmoil that differs fundamentally from previous recessions. A deceptive silence prevails in the boardrooms of European and international companies – broken only by the sound of failing strategies that were considered a guarantee of success just yesterday. This is not merely a cyclical downturn, but a profound structural break. The tools with which companies achieved growth for over two decades simply no longer work.

More information here:

📈🔵 Market knowledge vs. marketing knowledge: Why SMEs block their own growth 💡

Market vs. Marketing Knowledge: Why SMEs Block Their Own Growth - Image: Xpert.Digital

A persistent, pragmatic misconception exists among small and medium-sized enterprises (SMEs): that those who know their customers and the market also know how marketing works. However, this very equation is increasingly becoming a strategic trap for many SMEs.

The following article analyzes the often overlooked tension between operational market knowledge (looking in the rearview mirror) and strategic marketing knowledge (the high beam for future market share). Learn why a sole focus on sales targets leads to interchangeability in the long run and how SMEs can mature from "short-distance runners" to distinctive brands by consciously separating and realigning these two disciplines. Because those who understand marketing merely as "colorful pictures for sales" surrender 95 percent of tomorrow's potential customers to the competition without a fight.

More information here: