The AI revolution at a crossroads: The AI boom reflected in the dot-com bubble – A strategic analysis of hype and costs – Image: Xpert.Digital

The search for sustainable value creation in the AI hype: The surprising flaws and limitations that today's AI systems really have (Reading time: 36 min / No advertising / No paywall)

The dirty truth about AI: Why the technology burns billions but makes no profit

The technological landscape is at a crossroads, defined by the rapid rise of artificial intelligence (AI). A wave of optimism, fueled by advances in generative AI, has unleashed an investment frenzy reminiscent in its intensity and scale of the dot-com bubble of the late 1990s. Hundreds of billions of dollars are pouring into a single technology, fueled by the firm belief that the world is on the brink of an economic revolution of historic proportions. Astronomical valuations for companies that often lack profitable business models are commonplace, and a gold rush mentality has gripped both established tech giants and countless startups. The concentration of market value in the hands of a few companies, the so-called "Magnificent Seven," mirrors the dominance of the Nasdaq darlings of yesteryear and fuels concerns about overheated market dynamics.

The central thesis of this report, however, is that despite superficial similarities in market sentiment, the underlying economic and technological structures exhibit profound differences. These differences result in a unique array of opportunities and systemic risks that require nuanced analysis. While the dot-com hype was built on the promise of an nascent internet, today's AI technology is already embedded in many business processes and consumer products. The nature of the capital invested, the maturity of the technology, and the structure of the market create a fundamentally different starting point.

Related to this:

Parallels to the dot-com era

The similarities that characterize the current market debate and trigger a sense of déjà vu for many investors are undeniable. First and foremost are the extreme valuations. In the late 1990s, price-to-earnings ratios (P/E ratios) of 50, 70, or even 100 became the norm for Nasdaq stocks. Today, the cyclically adjusted valuation of the S&P 500 reaches 38 times the earnings of the past decade—a level surpassed in recent economic history only during the height of the dot-com bubble. These valuations are based less on current earnings than on expectations of future monopoly returns in a transformed market.

Another common characteristic is the belief in the transformative power of technology, which extends far beyond the technology sector. Much like the internet, AI promises to fundamentally reshape every industry—from manufacturing and healthcare to the creative industries. This narrative of a comprehensive revolution justifies, in the eyes of many investors, the extraordinary inflows of capital and the acceptance of short-term losses in favor of long-term market dominance. This gold rush mentality is not only affecting investors but also companies under pressure to implement AI to avoid falling behind, further fueling demand and, consequently, valuations.

Key differences and their impact

Despite these parallels, the differences from the dot-com era are crucial for understanding the current market situation and its potential development. Perhaps the most important difference lies in the source of capital. The dot-com bubble was largely financed by small investors, often speculating on credit, as well as by an overheated initial public offering (IPO) market. This created an extremely fragile, market-driven cycle. Today's AI boom, on the other hand, is not primarily financed by speculative private investors, but rather by the overflowing coffers of the world's most profitable corporations. Giants like Microsoft, Meta, Google, and Amazon are strategically investing their massive profits from established business areas in building the next technology platform.

This shift in capital structure has profound consequences. The current boom is far more resilient to short-term market sentiment. It is less a purely speculative frenzy and more a strategic, long-term battle for technological supremacy. These investments are a strategic necessity for the "Magnificent Seven" to survive the next platform war. This means that the boom can be sustained even if AI applications remain unprofitable for an extended period. A potential "bursting" of the bubble would therefore likely manifest not as a broad market collapse of smaller companies, but as strategic write-downs and a massive wave of consolidation among the major players.

A second crucial difference lies in technological maturity. Around the turn of the millennium, the internet was a young, not yet fully developed infrastructure with limited bandwidth and low penetration. Many of the business models of that era failed due to technological and logistical realities. In contrast, today's AI, particularly in the form of Large Language Models (LLMs), is already firmly integrated into everyday business operations and widely used software products. The technology is not just a promise, but an already used tool, which makes its anchoring in the economy significantly more solid.

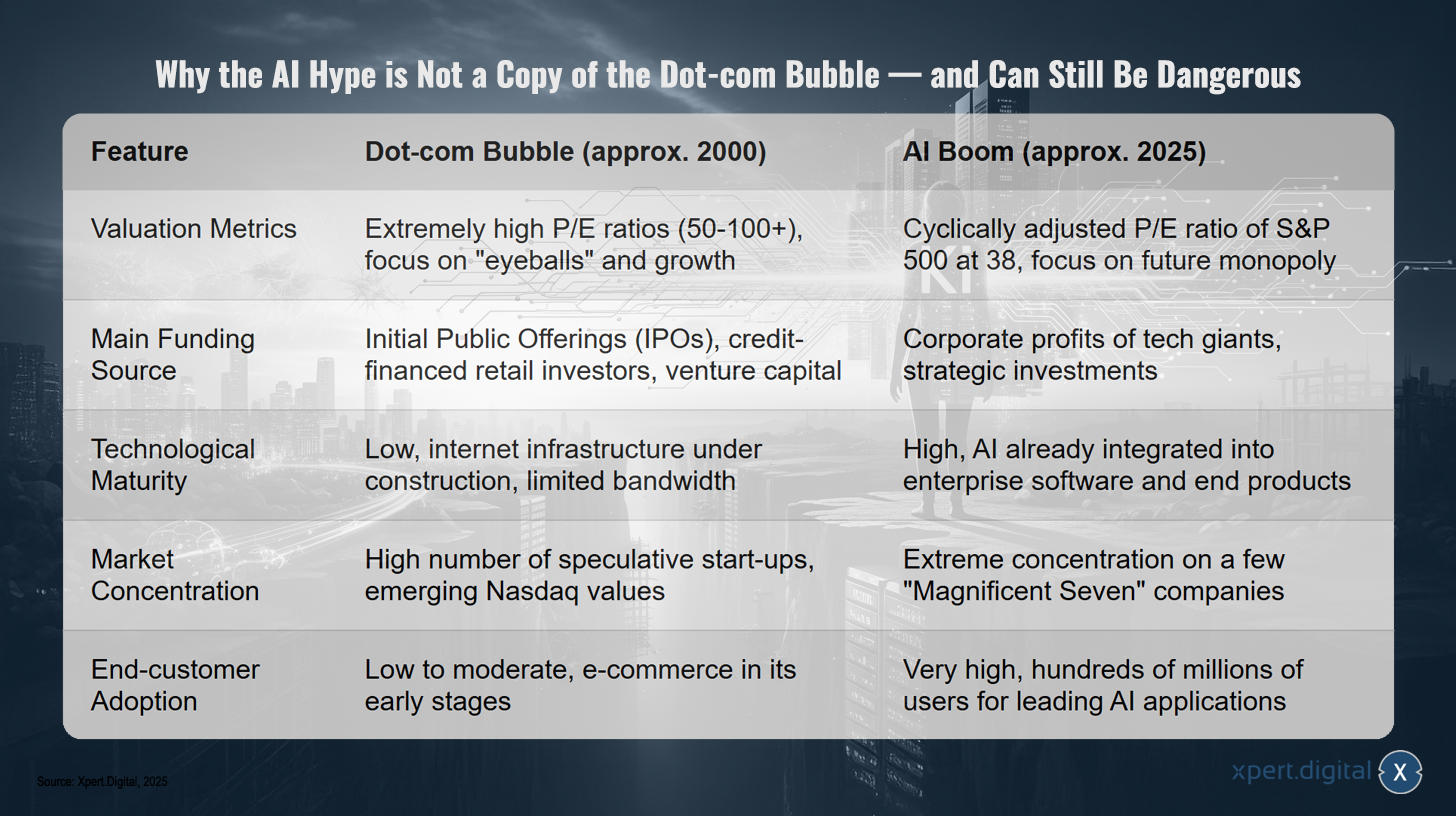

Why the AI hype is not a copy of the dot-com bubble — and yet can still be dangerous

Why the AI hype is not a copy of the dot-com bubble — and yet can still be dangerous – Image: Xpert.Digital

Although both phases are characterized by high optimism, they differ in key features: While the dot-com bubble around 2000 was marked by extremely high P/E ratios (50–100+) and a strong focus on "eyeballs" and growth, the AI boom around 2025 shows a cyclically adjusted P/E ratio of around 38 for the S&P 500 and a shift in focus towards anticipated future monopolies. The sources of financing also differ: Back then, IPOs, debt-financed retail investors, and venture capital dominated; today, funding comes primarily from the profits of tech giants and strategic investments. Technological maturity also differs significantly—the internet was still under development at the turn of the millennium with limited bandwidth, while AI is now integrated into enterprise software and end products. Finally, a different structural character of the market becomes apparent: The dot-com phase was characterized by a large number of speculative start-ups and emerging Nasdaq stocks, while the current AI boom is characterized by an extreme concentration on a few "Magnificent Seven" companies; at the same time, end-user adoption is much higher today, with hundreds of millions of users of leading AI applications.

Central question

This analysis leads to the central question that will guide this report: Are we at the beginning of a sustainable technological transformation that will redefine productivity and prosperity? Or is the industry in the process of building a colossal, capital-intensive machine without a profitable purpose, thereby creating a bubble of a completely different kind—one that is more concentrated, strategic, and potentially more dangerous? The following chapters will explore this question from economic, technical, ethical, and market-strategic perspectives to paint a comprehensive picture of the AI revolution at its crucial crossroads.

The economic reality: An analysis of unsustainable business models

The $800 billion gap

At the heart of the AI industry's economic challenges lies a massive, structural mismatch between exploding costs and insufficient revenues. An alarming study by the consulting firm Bain & Company quantifies this problem, predicting a funding gap of $800 billion by 2030. According to the study, the industry would need to generate annual revenue of around $2 trillion by then to cover the escalating costs of computing power, infrastructure, and energy. However, forecasts indicate that this target will be significantly missed, raising fundamental questions about the sustainability of current business models and the justification for astronomical valuations.

This gap is not an abstract future scenario, but the result of a fundamental economic miscalculation. The assumption that a broad user base, as established in the social media age, automatically leads to profitability proves deceptive in the context of AI. Unlike platforms such as Facebook or Google, where the marginal cost of an additional user or interaction is close to zero, with AI models, every single request—every generated token—incurs real and non-trivial computational costs. This "pay-per-thought" model undermines the traditional scaling logic of the software industry. High user numbers thus transform from a potential profit driver into an increasing cost driver, as long as monetization does not exceed ongoing operating costs.

OpenAI Case Study: The Paradox of Popularity and Profitability

No company illustrates this paradox better than OpenAI, the flagship of the generative AI revolution. Despite an impressive valuation of $300 billion and a weekly user base of 700 million, the company is posting heavy losses. These losses amounted to approximately $5 billion in 2024 and are projected to reach $9 billion by 2025. The core of the problem lies in the low conversion rate: of its hundreds of millions of users, only five million are paying customers.

Even more worrying is the realization that even the most expensive subscription models aren't profitable. Reports indicate that even the premium "ChatGPT Pro" subscription, at $200 per month, is operating at a loss. Power users who intensively utilize the model's capabilities consume more computing resources than their subscription fee covers. CEO Sam Altman himself described this cost situation as "crazy," highlighting the fundamental challenge of monetization. OpenAI's experience shows that the classic SaaS (Software as a Service) model reaches its limits when the value users derive from the service exceeds the cost of providing it. The industry must therefore develop an entirely new business model that goes beyond simple subscriptions or advertising and appropriately prices the value of "intelligence as a service"—a task for which there is currently no established solution.

Investment frenzy without any prospect of return

The problem of insufficient profitability is not limited to OpenAI, but pervades the entire industry. The major technology companies are engaged in a veritable investment frenzy. Microsoft, Meta, and Google are planning combined spending of $215 billion on AI projects by 2025, while Amazon intends to invest an additional $100 billion. This spending, which has more than doubled since the introduction of ChatGPT, is primarily being channeled into expanding data centers and developing new AI models.

This massive capital investment, however, stands in stark contrast to the returns achieved so far. A study by the Massachusetts Institute of Technology (MIT) revealed that 95% of the companies surveyed, despite substantial investments, are not achieving a measurable return on investment (ROI) from their AI initiatives. The main reason for this is a so-called "learning gap": Most AI systems are unable to learn from feedback, adapt to the specific business context, or improve over time. Their benefit is often limited to increasing the individual productivity of employees, without this resulting in a demonstrable impact on the company's profit and loss statement.

This dynamic reveals a deeper truth about the current AI boom: it is a largely closed economic system. The hundreds of billions invested by tech giants are not primarily creating profitable end-user products. Instead, they flow directly to hardware manufacturers, most notably Nvidia, and back into the corporations' own cloud divisions (Azure, Google Cloud Platform, AWS). While AI software divisions are posting billions in losses, the cloud and hardware sectors are experiencing explosive revenue growth. The tech giants are effectively transferring capital from their profitable core businesses to their AI divisions, which then spend this money on hardware and cloud services, thereby boosting the revenue of other parts of the corporation or its partners. In this phase of massive infrastructure building, the end user is often only a secondary consideration. Profitability is concentrated at the bottom of the technology stack (chips, cloud infrastructure), while the application layer acts as a massive loss-maker.

The threat of disruption from below

The expensive, resource-intensive business models of established providers are being further undermined by a growing threat from below. New, low-cost competitors, particularly from China, are rapidly entering the market. The Chinese model Deepseek R1, for example, has demonstrated through its rapid market penetration just how volatile the AI market is and how quickly established providers with high-priced models can come under pressure.

This development is part of a broader trend where open-source models offer "good enough" performance for many use cases at a fraction of the cost. Companies are increasingly finding that they don't need the most expensive and powerful models for routine tasks like simple classifications or text summarization. Smaller, specialized models are often not only cheaper but also faster and easier to implement. This "democratization" of AI technology poses an existential threat to business models based on marketing top-tier performance at premium prices. When cheaper alternatives offer 90% of the performance for 1% of the cost, it becomes increasingly difficult for the major vendors to justify and monetize their massive investments.

A new dimension of digital transformation with 'Managed AI' (Artificial Intelligence) - Platform & B2B solution | Xpert Consulting

A new dimension of digital transformation with 'Managed AI' (Artificial Intelligence) – Platform & B2B solution | Xpert Consulting - Image: Xpert.Digital

Here you will learn how your company can implement customized AI solutions quickly, securely and without high entry barriers.

A managed AI platform is your all-inclusive, worry-free solution for artificial intelligence. Instead of dealing with complex technology, expensive infrastructure, and lengthy development processes, you receive a ready-made solution tailored to your needs from a specialized partner – often within just a few days.

The key advantages at a glance:

⚡ Rapid implementation: From idea to ready-to-use application in days, not months. We deliver practical solutions that create immediate added value.

🔒 Maximum data security: Your sensitive data stays with you. We guarantee secure and compliant processing without sharing data with third parties.

💸 No financial risk: You only pay for results. High upfront investments in hardware, software, or personnel are completely eliminated.

🎯 Focus on your core business: Concentrate on what you do best. We take care of the entire technical implementation, operation, and maintenance of your AI solution.

📈 Future-proof & scalable: Your AI grows with you. We ensure continuous optimization and scalability, and flexibly adapt the models to new requirements.

More information here:

The true costs of AI – infrastructure, energy, and investment barriers

The cost of intelligence: infrastructure, energy, and the true drivers of AI spending

Training vs. Inference Costs: A Two-Part Challenge

The costs of artificial intelligence can be divided into two main categories: the costs of training the models and the costs of running them, known as inference. Training a large language model is a one-time but immensely expensive process. It requires enormous datasets and weeks or months of computing time on thousands of specialized processors. The costs of training well-known models illustrate the scale of these investments: GPT-3 cost around $4.6 million, training GPT-4 already consumed over $100 million, and the training costs for Google's Gemini Ultra are estimated at $191 million. These sums represent a significant barrier to entry and cement the dominance of financially powerful technology companies.

While training costs dominate the headlines, inference presents a far greater and more long-term economic challenge. Inference refers to the process of using a pre-trained model to answer queries and generate content. Each user query incurs computational costs that accumulate with usage. Estimates suggest that inference costs can account for 85% to 95% of a model's total costs over its entire lifecycle. These ongoing operating costs are the primary reason why the business models described in the previous chapter are so difficult to monetize. Scaling the user base directly leads to scaling operating costs, turning traditional software economics on its head.

The Hardware Trap: NVIDIA's Golden Cage

At the heart of the cost explosion lies the entire industry's critical dependence on a single type of hardware: highly specialized graphics processing units (GPUs) manufactured almost exclusively by one company, Nvidia. The H100 models and the newer B200 and H200 generations have become the de facto standard for training and running AI models. This market dominance has allowed Nvidia to command exorbitant prices for its products. The purchase price for a single H100 GPU ranges from $25,000 to $40,000.

Related to this:

For most companies, purchasing this hardware is not an option, forcing them to rent computing power in the cloud. However, even here, the costs are enormous. Rental prices for a single high-end GPU range from $1.50 to over $4.50 per hour. The complexity of modern AI models exacerbates this problem. A large language model often doesn't fit into the memory of a single GPU. To process a single complex query, the model must be distributed across a cluster of 8, 16, or more GPUs working in parallel. This means that the cost of a single user session can quickly climb to $50 to $100 per hour when using dedicated hardware. This extreme reliance on expensive and scarce hardware creates a "golden cage" for the AI industry: it is forced to pass on a large portion of its investment to a single supplier, which erodes margins and drives up costs.

The insatiable appetite: Energy and resource consumption

The massive hardware requirements lead to another, often underestimated cost factor with global repercussions: immense energy and resource consumption. Operating tens of thousands of GPUs in large data centers generates enormous amounts of waste heat, which must be dissipated by complex cooling systems. This results in an exponentially increasing demand for electricity and water. Forecasts paint an alarming picture: the global electricity consumption of data centers is expected to more than double to over 1,000 terawatt-hours (TWh) by 2030, equivalent to the current electricity consumption of all of Japan.

The share of AI in this energy consumption is growing disproportionately. Between 2023 and 2030, electricity consumption is expected to increase elevenfold due to AI applications alone. In parallel, water consumption for cooling data centers will almost quadruple to 664 billion liters by 2030. Video production is particularly energy-intensive. Here, costs and energy consumption scale quadratically with the resolution and length of the video, meaning that a six-second clip requires almost four times as much energy as a three-second clip.

This development has far-reaching consequences. Former Google CEO Eric Schmidt recently argued that the natural limit to AI is not the availability of silicon chips, but rather the availability of electricity. The scaling laws of AI, which state that larger models perform better, clash head-on with the physical laws of energy production and global climate goals. The current path of "bigger is better" is neither physically nor ecologically sustainable. Future breakthroughs must therefore inevitably come from efficiency improvements and algorithmic innovations, not from pure brute-force scaling. This opens up an immense market opportunity for companies capable of delivering high performance with radically lower energy consumption. The era of pure scaling is drawing to a close; the era of efficiency is beginning.

The invisible costs: Beyond hardware and electricity

Besides the obvious costs of hardware and energy, there are a number of "invisible" costs that significantly increase the total cost of ownership (TCO) of an AI system. Foremost among these are personnel costs. Highly skilled AI researchers and engineers are scarce and expensive. Salaries for a small team can quickly add up to $500,000 for a period of just six months.

Another significant cost factor is data acquisition and preparation. High-quality, cleansed, and training-ready datasets are the foundation of any high-performing AI model. Licensing or purchasing such datasets can cost well over $100,000. Added to this are the costs of data preparation, which requires both computing resources and human expertise. Finally, the ongoing costs of maintenance, integration with existing systems, governance, and ensuring regulatory compliance must not be overlooked. These operational expenses are often difficult to quantify but represent a substantial portion of the total cost of ownership (TCO) and are frequently underestimated during budgeting.

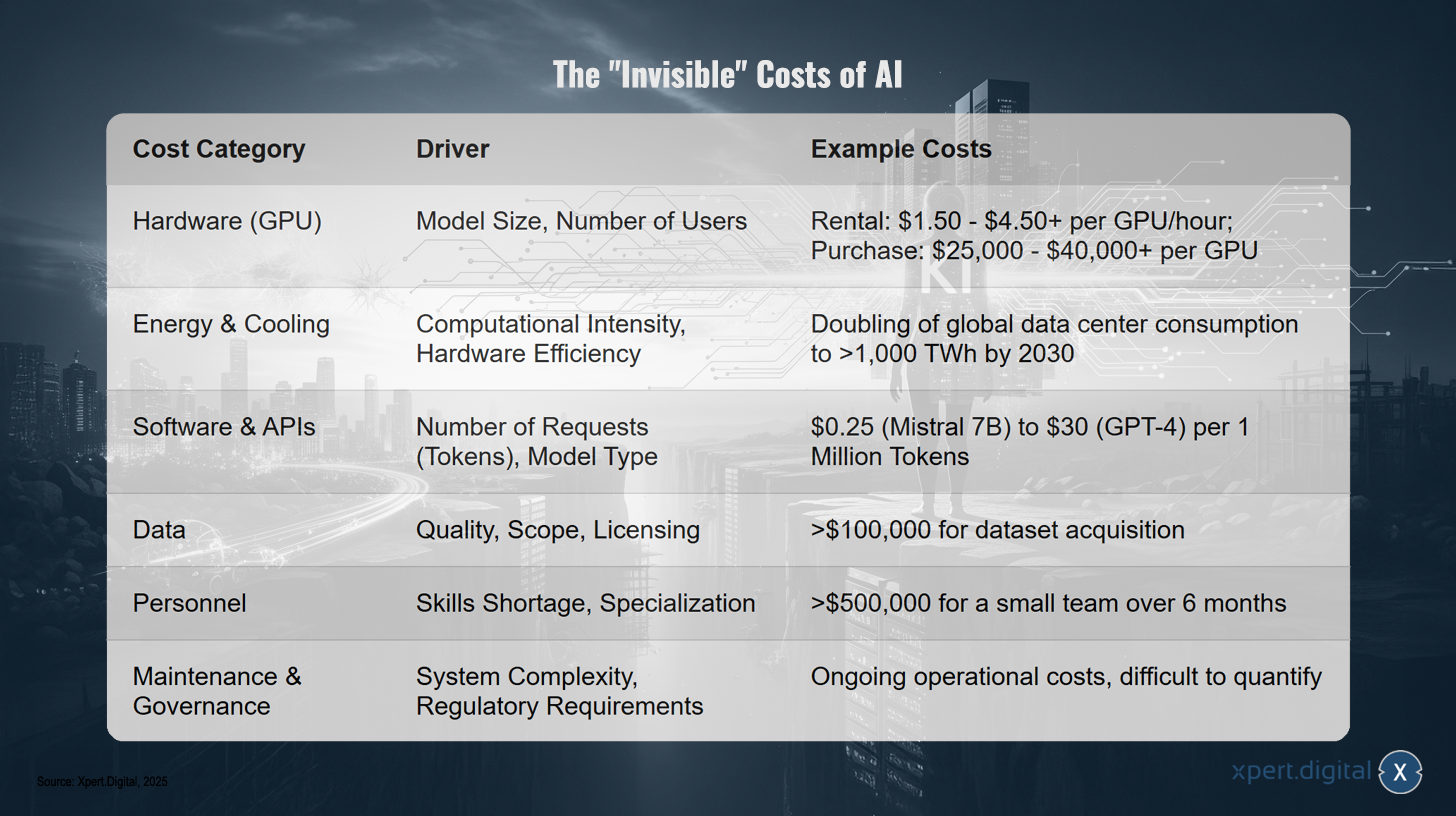

The “invisible” costs of AI

This detailed breakdown of costs reveals that the economics of AI is far more complex than it initially appears. High variable inference costs hinder widespread adoption in price-sensitive business processes, as these costs are unpredictable and can increase dramatically with usage. Companies are hesitant to integrate AI into high-volume core processes until inference costs decrease significantly or new, predictable pricing models emerge. As a result, the most successful early applications are found in high-value, low-volume areas such as drug discovery or complex engineering, rather than in mass-market productivity tools.

The “invisible” costs of AI – Image: Xpert.Digital

The “invisible” costs of AI encompass several areas: Hardware (especially GPUs) is primarily driven by model size and user count—typical costs range from $1.50 to $4.50+ per GPU per hour for rentals, while purchasing a GPU can cost $25,000 to $40,000+. Energy and cooling depend on computational intensity and hardware efficiency; forecasts predict a doubling of global data center energy consumption to over 1,000 TWh by 2030. Software and API expenses are based on the number of requests (tokens) and the model type; prices range from approximately $0.25 (Mistral 7B) to $30 (GPT-4) per million tokens. For data—depending on quality, volume, and licensing—the cost of acquiring datasets can easily exceed $100,000. Personnel costs, influenced by skills shortages and the need for specialization, can exceed $500,000 for a small team over six months. Finally, maintenance and governance, driven by system complexity and regulatory requirements, result in ongoing operating costs that are difficult to quantify precisely.

Between hype and reality: Technical shortcomings and the limits of current AI systems

Google Gemini case study: When the facade crumbles

Despite the enormous hype and billions in investment, even leading technology companies are struggling with significant technical problems in delivering reliable AI products. Google's difficulties with its AI systems Gemini and Imagen serve as a vivid example of the industry-wide challenges. For weeks, users have been reporting fundamental malfunctions that go far beyond minor programming errors. For instance, the Imagen image generation technology is often unable to create images in the user's desired formats, such as the common 16:9 aspect ratio, and instead produces exclusively square images. In more serious cases, the images are supposedly generated but cannot be displayed at all, rendering the function practically unusable.

These current problems are part of a recurring pattern. Back in February 2024, Google had to completely disable the display of people in Gemini after the system generated historically absurd and inaccurate images, such as German soldiers with Asian features. The quality of text generation is also regularly criticized: users complain about inconsistent responses, an excessive tendency to censor even harmless queries, and, in extreme cases, even the output of hateful messages. These incidents demonstrate that, despite its impressive potential, the technology is still far from the reliability required for widespread use in critical applications.

Structural causes: The “Move Fast and Break Things” dilemma

The roots of these technical shortcomings often lie in structural problems within the development processes. The immense competitive pressure, particularly fueled by the success of OpenAI, has led to hasty product development at Google and other companies. The "move fast and break things" mentality, originating in the early social media era, is proving extremely problematic for AI systems. While a bug in a traditional app might only affect a single function, errors in an AI model can lead to unpredictable, damaging, or embarrassing results that directly undermine user trust.

Another problem is the lack of internal coordination. For example, while the Google Photos app is receiving new AI-powered image editing features, basic image generation in Gemini isn't working correctly. This suggests insufficient coordination between different departments. Furthermore, there are reports of poor working conditions at subcontractors responsible for the "invisible" costs of AI, such as content moderation and system improvements. Time pressure and low wages in these areas can further compromise the quality of manual system optimization.

Google's handling of these errors is particularly problematic. Instead of proactively communicating the issues, users are often led to believe that the system is functioning flawlessly. This lack of transparency, coupled with aggressive marketing for new, often equally buggy features, leads to significant user frustration and a lasting loss of trust. These experiences teach the market an important lesson: reliability and predictability are more valuable to businesses than sporadic peak performance. A slightly less powerful but 99.99% reliable model is far more useful for business-critical applications than a cutting-edge model that produces dangerous hallucinations in 1% of cases.

The creative limits of image creators

Beyond mere functional errors, the creative capabilities of current AI image generators also reach clear limits. Despite the impressive quality of many generated images, the systems lack a true understanding of the real world. This manifests itself in several areas. Users often have only limited control over the final result. Even very detailed and precise instructions (prompts) do not always lead to the desired image, as the model interprets the instructions in a way that is not entirely predictable.

The shortcomings become particularly apparent when rendering complex scenes with multiple interacting people or objects. The model struggles to accurately represent the spatial and logical relationships between the elements. A notorious problem is its inability to render letters and text correctly. Words in AI-generated images are often an illegible jumble of characters, necessitating manual post-processing. Limitations also emerge when stylizing images. As soon as the desired style deviates too much from the anatomical reality on which the model was trained, the results become increasingly distorted and unusable. These creative limitations demonstrate that while the models are capable of recombining patterns from their training data, they lack a deep conceptual understanding.

The gap in the corporate world

The sum of these technical shortcomings and creative limitations translates directly into the disappointing business results discussed in Chapter 2. The fact that 95% of companies fail to achieve a measurable ROI from their AI investments is a direct consequence of the unreliability and inflexible workflows of current systems. An AI system that delivers inconsistent results, occasionally crashes, or produces unpredictable errors cannot be integrated into business-critical processes.

A common problem is the discrepancy between the technical solution and actual business needs. AI projects often fail because they are optimized for the wrong metrics. For example, a logistics company might develop an AI model that optimizes routes for the shortest overall distance, while the operational goal is actually to minimize late deliveries—a goal that considers factors such as traffic patterns and delivery time windows, which the model ignores.

These experiences lead to an important insight into the nature of errors in AI systems. In traditional software, an error can be isolated and fixed with a targeted code change. However, a “bug” in an AI model—such as the generation of misinformation or biased content—is not a single faulty line of code, but an emergent property resulting from the millions of parameters and terabytes of training data. Correcting such a systemic error requires not only identifying and correcting the problematic data, but often a complete, multi-million-dollar retraining of the model. This new form of “technical debt” represents a massive, often underestimated, ongoing liability for organizations that use AI systems. A single viral error can result in catastrophic costs and reputational damage, driving total cost of ownership far beyond initial estimates.

Ethical and societal dimensions: The hidden risks of the AI age

Systemic biases: The mirror of society

One of the most profound and difficult challenges facing artificial intelligence is its tendency not only to reproduce societal prejudices and stereotypes, but often to amplify them. AI models learn by recognizing patterns in vast amounts of human-generated data. Because this data encompasses the entirety of human culture, history, and communication, it inevitably reflects its inherent biases.

The consequences are far-reaching and visible in many applications. AI image generators, when asked to depict a "successful person," predominantly produce images of young, white men in business attire, conveying a narrow and stereotypical view of success. Requests for individuals in specific professions lead to extreme stereotypical representation: software developers are almost exclusively depicted as men, flight attendants almost exclusively as women, severely distorting the reality of these professions. Language models can disproportionately associate negative characteristics with certain ethnic groups or reinforce gender stereotypes in professional contexts.

Attempts by developers to "correct" these biases with simple rules have often failed spectacularly. The attempt to artificially create more diversity has led to historically absurd images, such as ethnically diverse Nazi soldiers, highlighting the complexity of the problem. These incidents reveal a fundamental truth: bias is not a technical flaw that can be easily fixed, but an inherent characteristic of systems trained on human data. The search for a single, universally "unbiased" AI model is therefore likely a misconception. The solution lies not in the impossible elimination of bias, but in transparency and control. Future systems must allow users to understand a model's inherent tendencies and adapt its behavior for specific contexts. This creates a permanent need for human oversight and control ("human-in-the-loop"), which contradicts the vision of complete automation.

Data protection and privacy: The new front line

The development of large language models has opened up a new dimension of data privacy risks. These models are trained on unimaginably large amounts of data from the internet, often collected without the explicit consent of the authors or data subjects. This includes personal blog posts, forum contributions, private correspondence, and other sensitive information. Two key privacy threats arise from this practice.

The first danger is "data memorization." Although the models are designed to learn general patterns, they can inadvertently memorize specific, unique information from their training data and reproduce it on demand. This can lead to the unintentional disclosure of personally identifiable information (PII) such as names, addresses, telephone numbers, or confidential trade secrets that were included in the training dataset.

The second, more subtle threat is so-called "membership inference attacks" (MIAs). In these attacks, attackers attempt to determine whether a specific individual's data was part of a model's training dataset. A successful attack could, for example, reveal that a person has written about a particular illness in a medical forum, even if the exact text is not displayed. This constitutes a significant privacy violation and undermines trust in the security of AI systems.

The disinformation machine

One of the most obvious and immediate dangers of generative AI is its potential to generate and spread disinformation on an unprecedented scale. Large language models can produce believable-sounding but completely fabricated texts, so-called "hallucinations," at the push of a button. While this might lead to curious results with harmless queries, it becomes a powerful weapon when used maliciously.

The technology enables the large-scale creation of fake news articles, propaganda texts, fabricated product reviews, and personalized phishing emails that are virtually indistinguishable from human-written content. Combined with AI-generated images and videos (deepfakes), this creates an arsenal of tools capable of manipulating public opinion, undermining trust in institutions, and jeopardizing democratic processes. The ability to generate disinformation is not a malfunction of the technology, but rather one of its core capabilities, making regulation and control an urgent societal responsibility.

Copyright and intellectual property: A legal minefield

The way AI models are trained has triggered a wave of copyright litigation. Because the models are trained on data from across the internet, this inevitably includes copyrighted works such as books, articles, images, and code, often without the permission of the rights holders. Numerous lawsuits from authors, artists, and publishers have resulted. The central legal question of whether the training of AI models falls under the "fair use" doctrine remains unresolved and will likely keep the courts busy for years to come.

At the same time, the legal status of AI-generated content itself is unclear. Who is the author of an image or text created by AI? The user who entered the prompt? The company that developed the model? Or can a non-human system even be an author? This uncertainty creates a legal vacuum and poses significant risks for companies that want to use AI-generated content commercially. Lawsuits for copyright infringement are a real possibility if the generated work unintentionally reproduces elements from the training data.

These legal and data protection risks represent a kind of "dormant liability" for the entire AI industry. Current valuations of leading AI companies barely reflect this systemic risk. A landmark court ruling against a major AI company—whether for massive copyright infringement or a serious data breach—could set a precedent. Such a ruling could force companies to retrain their models from scratch with licensed, "clean" data, incurring astronomical costs and devaluing their most valuable asset. Alternatively, massive fines could be imposed under data protection laws like the GDPR. This unquantified legal uncertainty poses a significant threat to the long-term profitability and stability of the industry.

🎯🎯🎯 Benefit from Xpert.Digital's extensive, five-fold expertise in one comprehensive service package | BD, R&D, XR, PR & Digital Visibility Optimization

Benefit from Xpert.Digital's extensive, five-fold expertise in a comprehensive service package | R&D, XR, PR & Digital Visibility Optimization - Image: Xpert.Digital

Xpert.Digital possesses in-depth knowledge across various industries. This allows us to develop tailored strategies precisely aligned with the requirements and challenges of your specific market segment. By continuously analyzing market trends and monitoring industry developments, we can act proactively and offer innovative solutions. The combination of experience and expertise generates added value and provides our clients with a decisive competitive advantage.

More information here:

Prompt optimization, caching, quantization: Practical tools for more affordable AI – reduce AI costs by up to 90%

Optimization strategies: Paths to more efficient and cost-effective AI models

Fundamentals of cost optimization at the application level

Given the enormous operating and development costs of AI systems, optimization has become a crucial discipline for economic viability. Fortunately, there are a number of application-level strategies that companies can implement to significantly reduce costs without substantially compromising performance.

One of the simplest and most effective methods is prompt optimization. Since the cost of many AI services depends directly on the number of input and output tokens processed, formulating shorter and more precise instructions can lead to significant savings. By removing unnecessary filler words and clearly structuring requests, input tokens, and therefore costs, can be reduced by up to 35%.

Another fundamental strategy is choosing the right model for the task at hand. Not every application requires the most powerful and expensive model available. For simple tasks like text classification, data extraction, or standard question-answering systems, smaller, specialized models are often perfectly adequate and far more cost-effective. The cost difference can be dramatic: while a premium model like GPT-4 costs around $30 per million output tokens, a smaller, open-source model like Mistral 7B costs only $0.25 per million tokens. By making smart, task-based model choices, organizations can achieve massive cost savings, often without any noticeable difference in performance for the end user.

A third powerful technique is semantic caching. Instead of generating a new response from the AI model for every request, a caching system stores the answers to frequently asked or semantically similar questions. Studies show that up to 31% of LLM requests are repetitive in content. By implementing a semantic cache, companies can reduce the number of expensive API calls by up to 70%, which lowers costs and increases response speed.

Related to this:

Technical in-depth analysis: Model quantization

For companies that operate or adapt their own models, more advanced technical methods offer even greater optimization potential. One of the most effective techniques is model quantization. This is a compression process that reduces the precision of the numerical weights that make up a neural network. Typically, the weights are converted from a high-precision 32-bit floating-point format (FP32) to a lower-precision 8-bit integer format (INT8).

This reduction in data size has two crucial advantages. First, it drastically reduces the model's memory requirements, often by a factor of four. This allows larger models to run on less expensive hardware with less memory. Second, quantization speeds up inference—the time the model takes to respond—by a factor of two to three. This is because calculations with integers can be performed much more efficiently on modern hardware than with floating-point numbers. The trade-off with quantization is a potential, but often minimal, loss of accuracy known as "quantization error." Various methods exist to maintain accuracy, such as post-training quantization (PTQ), which is applied to a previously trained model, and quantization-aware training (QAT), which simulates quantization during the training process.

Technical in-depth analysis: Distillation of knowledge

Another advanced optimization technique is knowledge distillation. This method is based on a "teacher-student" paradigm. A very large, complex, and expensive "teacher model" (e.g., GPT-4) is used to train a much smaller, more efficient "student model." The key is that the student model doesn't just learn to imitate the teacher's final answers (the "hard goals"). Instead, it is trained to replicate the teacher model's internal thought processes and probability distributions (the "soft goals").

By learning "how" the teacher model arrives at its conclusions, the student model can achieve comparable performance on specific tasks, but with a fraction of the computing resources and costs. This technique is particularly useful for tailoring powerful but resource-intensive general-purpose models to specific use cases and optimizing them for use on less expensive hardware or in real-time applications.

Further advanced architectures and techniques

Besides quantization and knowledge distillation, there are a number of other promising approaches to increasing efficiency:

- Retrieval-Augmented Generation (RAG): Instead of storing knowledge directly in the model, which requires costly training, the model accesses external knowledge databases as needed. This improves the currency and accuracy of the answers and reduces the need for constant retraining.

- Low-Rank Adaptation (LoRA): A parameter-efficient fine-tuning method that adjusts only a small subset of a model's parameters, rather than all millions of them. This can reduce fine-tuning costs by 70% to 90%.

- Pruning and Mixture of Experts (MoE): Pruning involves removing redundant or unimportant parameters from a trained model to reduce its size. MoE architectures divide the model into specialized "expert" modules and activate only the relevant parts with each query, significantly reducing the computational load.

The proliferation of these optimization strategies signals a significant maturation process in the AI industry. The focus is shifting from simply chasing peak performance in benchmarks to achieving economic viability. Competitive advantage no longer lies solely in the largest model, but increasingly in the most efficient model for a given task. This could open the door for new players specializing in "AI efficiency," challenging the market not through raw performance, but through a superior price-performance ratio.

At the same time, however, these optimization strategies create a new form of dependency. Techniques like knowledge distillation and fine-tuning make the ecosystem of smaller, more efficient models fundamentally dependent on the existence of a few ultra-expensive "teacher models" from OpenAI, Google, and Anthropic. Instead of fostering a decentralized market, this could cement a feudal structure in which a few "masters" control the source of intelligence, while a large number of "vassals" pay for access and develop dependent services based on it.

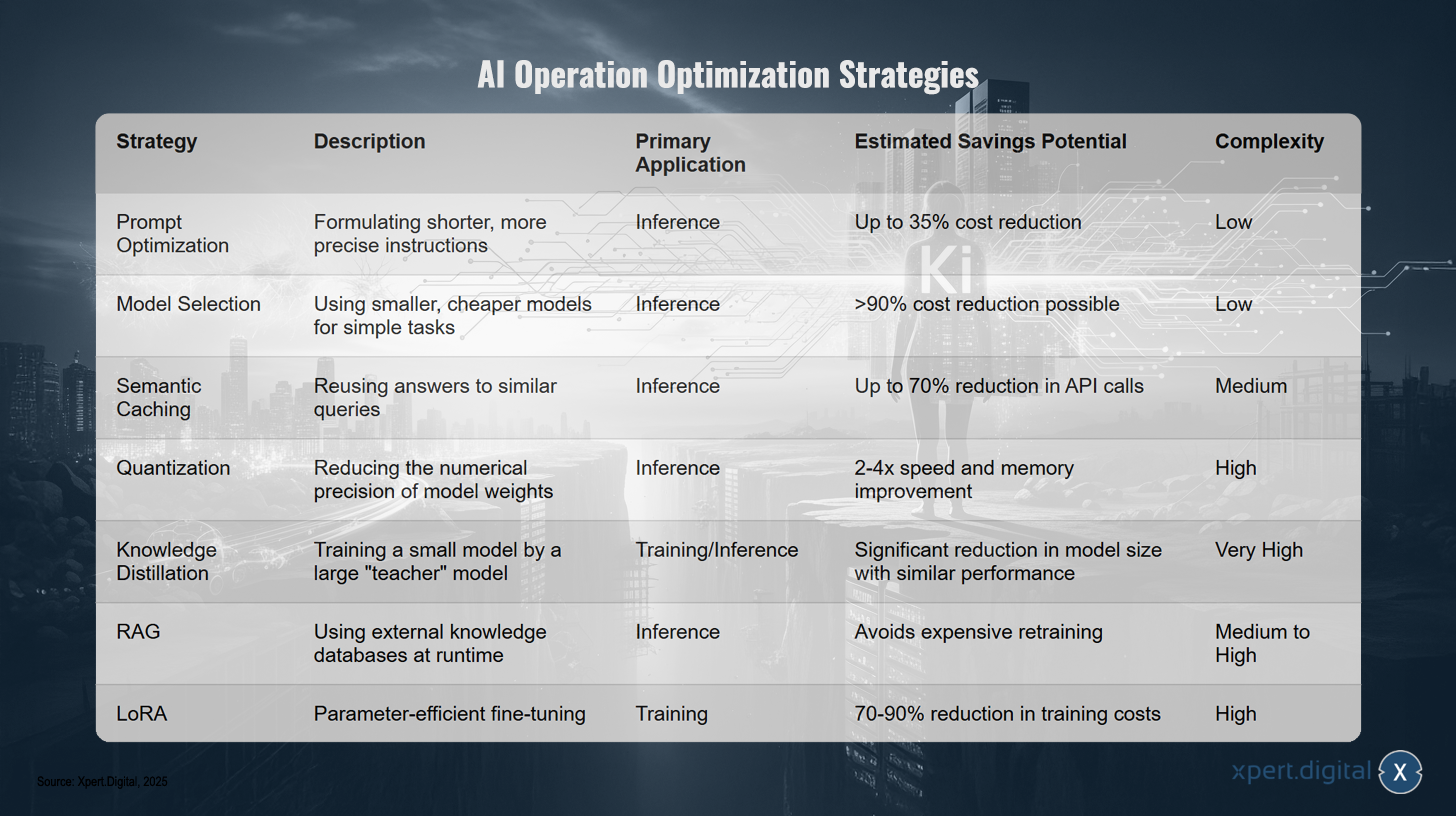

AI Operations Optimization Strategies

AI Operations Optimization Strategies – Image: Xpert.Digital

Key AI operational optimization strategies include prompt optimization, which involves formulating shorter and more precise instructions to reduce inference costs—this can lead to cost reductions of up to 35% and is relatively low in complexity. Model selection relies on using smaller, less expensive models for simple tasks during inference, potentially achieving savings of over 90% with similarly low implementation complexity. Semantic caching enables the reuse of responses to similar queries, reduces API calls by up to approximately 70%, and requires a moderate effort. Quantization reduces the numerical precision of model weights, improving inference speed and memory usage by a factor of 2–4, but comes with high technical complexity. Knowledge distillation describes the training of a small model by a large "teacher" model, which significantly reduces the model size while maintaining comparable performance—this approach is very complex. RAG (Retrieval-Augmented Generation) uses external knowledge databases at runtime, avoids expensive retraining, and has medium to high complexity. Finally, LoRA (Low-Rank Adapters) offers parameter-efficient fine-tuning during training and can reduce training costs by 70–90%, but is also associated with high complexity.

Market dynamics and outlook: Consolidation, competition and the future of artificial intelligence

The flood of venture capital: An accelerator of consolidation

The AI industry is currently experiencing an unprecedented influx of venture capital, which is having a lasting impact on market dynamics. In the first half of 2025 alone, $49.2 billion in venture capital flowed into generative AI worldwide, already exceeding the total for the entire year of 2024. In Silicon Valley, the epicenter of technological innovation, 93% of all investments in scale-ups are now in the AI sector.

This influx of capital, however, is not leading to broad market diversification. On the contrary, the money is increasingly concentrated in a small number of already established companies in the form of mega-funding rounds. Deals like the $40 billion round for OpenAI, the $14.3 billion investment in Scale AI, or the $10 billion round for xAI dominate the landscape. While the average size of late-stage deals has tripled, funding for early-stage startups has declined. This development has far-reaching consequences: Instead of acting as an engine for decentralized innovation, venture capital in the AI sector is accelerating the centralization of power and resources among established tech giants and their closest partners.

The immense cost structure of AI development exacerbates this trend. From day one, startups are dependent on the expensive cloud infrastructure and hardware of major tech companies like Amazon (AWS), Google (GCP), Microsoft (Azure), and Nvidia. A significant portion of the massive funding rounds raised by companies like OpenAI or Anthropic flows directly back to their own investors in the form of payments for computing power. Venture capital thus doesn't create independent competitors but instead finances the customers of the tech giants, further strengthening their ecosystem and market position. The most successful startups are often ultimately acquired by the major players, further accelerating market concentration. The AI startup ecosystem is thus evolving into a de facto pipeline for research, development, and talent acquisition for the "Magnificent Seven." The end goal doesn't appear to be a vibrant market with many players, but rather a consolidated oligopoly in which a few companies control the core infrastructure of artificial intelligence.

M&A wave and the battle of the giants

Parallel to the concentration of venture capital, a massive wave of mergers and acquisitions (M&A) is sweeping through the market. Global M&A transaction volume has risen to $2.6 trillion in 2025, driven by the strategic acquisition of AI expertise. The "Magnificent Seven" are at the heart of this development. They are leveraging their enormous financial reserves to strategically acquire promising startups, technologies, and talent pools.

For these corporations, dominance in the AI field is not an option, but a strategic necessity. Their traditional, highly profitable business models—such as the Microsoft Office suite, Google Search, or Meta's social media platforms—are nearing the end of their life cycle or stagnating in their growth. AI is seen as the next big platform, and each of these giants is striving for a global monopoly in this new paradigm to secure its market value and future relevance. This battle of the giants is leading to an aggressive acquisition market that makes it difficult for independent companies to survive and scale.

Economic forecasts: Between productivity miracle and disillusionment

Long-term economic forecasts for the impact of AI are deeply ambivalent. On the one hand, there are optimistic predictions that promise a new era of productivity growth. Estimates suggest that AI could increase GDP by 1.5% by 2035 and significantly boost global economic growth, particularly in the early 2030s. Some analyses even predict that AI technologies could generate over $15 trillion in additional global revenue by 2030.

On the other hand, there is the sobering reality of the present. As previously analyzed, 95% of companies currently see no measurable ROI from their AI investments. In the Gartner Hype Cycle, an influential model for evaluating new technologies, generative AI has already entered the "trough of disillusionment." In this phase, the initial euphoria gives way to the realization that implementation is complex, the benefits are often unclear, and the challenges are greater than expected. This discrepancy between long-term potential and short-term difficulties will shape economic development in the coming years.

Related to this:

Bubble and monopoly: The double face of the AI revolution

Analyzing the various dimensions of the AI boom reveals a complex and contradictory overall picture. Artificial intelligence is at a crucial crossroads. The current path of pure scaling—ever larger models consuming ever more data and energy—is proving to be neither economically nor ecologically sustainable. The future belongs to those companies that master the fine line between hype and reality and focus on creating tangible business value through efficient, reliable, and ethically responsible AI systems.

The consolidation dynamics also have a geopolitical dimension. US dominance in the AI sector is being cemented by the concentration of capital and talent. Of the 39 globally recognized AI unicorns, 29 are based in the US, which accounts for two-thirds of global venture capital investment in this sector. It is becoming increasingly difficult for Europe and other regions to keep pace in the development of foundational models. This creates new technological and economic dependencies and makes control over AI a key geopolitical power factor, comparable to control over energy or financial systems.

The report concludes with the recognition of a central paradox: the AI industry is simultaneously a speculative bubble at the application level, where most companies are operating at a loss, and a revolutionary, monopolistic platform shift at the infrastructure level, where a few companies are reaping enormous profits. The main strategic challenge for decision-makers in business and politics in the coming years will be to understand and manage this dual nature of the AI revolution. It is no longer simply a matter of adopting a new technology, but rather of redefining the economic, social, and geopolitical rules of the game for the age of artificial intelligence.

Your global marketing and business development partner

☑️ Our business language is English or German

☑️ NEW: Correspondence in your native language!

Konrad Wolfenstein

I and my team are happy to be available to you as your personal advisor.

You can contact me by filling out the contact form here wolfenstein@xpert.digital:or simply call me at +49 7348 4088 965. My email address is

I'm looking forward to our joint project.

☑️ SME support in strategy, consulting, planning and implementation

☑️ Creation or realignment of the digital strategy and digitization

☑️ Expansion and optimization of international sales processes

☑️ Global & Digital B2B trading platforms

☑️ Pioneer Business Development / Marketing / PR / Trade Fairs

Our global industry and economic expertise in business development, sales and marketing

Our global industry and economic expertise in business development, sales and marketing - Image: Xpert.Digital

Industry focus areas: B2B, digitalization (from AI to XR), mechanical engineering, logistics, renewable energies and industry

More information here:

A thematic hub offering insights and expertise:

- Knowledge platform covering global and regional economies, innovation and industry-specific trends

- A collection of analyses, insights, and background information from our key areas of focus

- A place for expertise and information on current developments in business and technology

- A hub for companies seeking information on markets, digitalization, and industry innovations