Growth miracle instead of recession: Why Poland is overtaking crisis-ridden Europe and Germany – Image: Xpert.Digital

Europe's new powerhouse: Why looking to Poland is vital for the German economy

Ahead of China: How Poland is quietly rising to become Germany's most important partner – VW, Google & Rheinmetall and the massive capital flight to the East that nobody notices

While worries deepen in Berlin and Brussels and the Eurozone teeters on the brink of stagnation, an economic miracle is unfolding on Germany's eastern border that is far more than just a cyclical boom. Poland is not only growing faster than the rest of Europe – it is reinventing its role in the global value chain.

The days when Poland merely served as an extended production bench for cheap intermediate goods are over. Driven by massive investments in defense, digital infrastructure, and green technologies, Poland is transforming into a high-tech hub and military bulwark of the continent. German exporters now do more business with Poland than with China, and giants like Volkswagen, Microsoft, and Rheinmetall are relocating strategically crucial production capacities across the Oder River.

But this rise presents a paradox: While trade is booming, investment flows are fundamentally changing, and administrative hurdles for businesses are increasing. The following article analyzes the profound shift of European economic power eastward, highlights the opportunities and risks for German companies, and explains why Warsaw is the new center of gravity for European investment.

Poland is growing – while Europe's economy remains paralyzed

How Poland is becoming Europe's growth engine: The quiet shift of European value creation to the East

The European economy is at a turning point, largely unnoticed outside the Brussels establishment. While the Eurozone groans with barely 1.5 percent growth and Germany's export champions speak of losing their dominance, Poland is growing at over 3 percent annually and simultaneously positioning itself as a technological and industrial powerhouse. This is no longer a business cycle – it is a structural shift in European value chains, driven by geopolitics, subsidies, and a calculated reassessment of what productivity means in the 21st century.

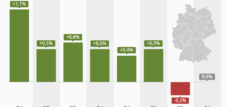

The economic data is precise. Poland's gross domestic product is projected to grow by 3.3 percent in 2025, 3.4 percent in 2026, and still reach 2.7 percent in 2027. This contrasts dramatically with the European reality: the Eurozone is effectively stagnating at one percent. Germany, long the engine of Central Europe, contracted by 0.2 percent in 2024, while Polish companies expanded their production facilities, investments flowed, and digital infrastructure was ramped up with European funding. The economic divergence is now measurable and will widen further without fundamental structural reforms in Western European economies.

Europe's trade architecture is being recalibrated

German-Polish trade reached a historic high in the first half of 2025. With a total volume of €90 billion and year-on-year growth of 5.4 percent, this development confirms a simple but often overlooked reality: Eastern Europe is no longer its economic periphery, but an integrated core of continental value creation. German exports to Poland amounted to €49.4 billion, an increase of 5.7 percent compared to the previous year – a figure that even surpasses China's import volume from Germany by €8 billion. It is noteworthy that German exports worldwide declined by 0.1 percent, while those to Poland grew explosively. This is not mere statistical noise, but proof of a massive reallocation of resources.

Poland has thus become Germany's fifth most important trading partner and has even moved up to fourth place in terms of exports – after the USA, France, and the Netherlands, but already overtaking China. At the same time, Germany imports goods from Poland worth €40.6 billion, making Poland Germany's fourth most important source of imports. This bidirectional integration is not accidental, but rather the result of a deliberate supply chain transformation that has been accelerating steadily since 2020.

The profile of these exports is particularly telling: while German-Polish trade was characterized for decades by low-value components and low-cost manufacturing, today high-quality industrial and technological products dominate. This indicates a qualitative leap in the bilateral relationship. Automotive and mechanical engineering components are flourishing, but trade in measuring instruments, semi-finished steel products, and rail vehicles is also growing disproportionately – all sectors that require advanced manufacturing capacities and a skilled workforce.

The investment paradox: More trade, less traditional FDI

Herein lies the crucial paradox that explains the misunderstanding surrounding Poland's attractiveness. While German-Polish trade is booming, measured foreign direct investment in Poland has plummeted by almost 53 percent – from approximately €27 billion in 2023 to €13.1 billion in 2024. German companies reduced their investments by eight percent to €2.1 billion. On the surface, this appears to be a warning about Poland's economic fragility. In reality, it is the opposite: an indicator of a fundamental shift in European investment behavior.

The classic narrative of foreign direct investment – Western European corporations opening low-cost factories in the East, paying subsistence-level wages, and outsourcing routine work – has become obsolete. What is happening instead is a more subtle but profound transformation. Companies are no longer investing primarily because of low wages, but because of skilled labor, stable EU funding, geographical proximity to Western European markets, and – a new development – access to future technologies and defense capabilities.

The decline in traditional FDI metrics is being overshadowed by more significant investments in future-oriented industries. The investment boom in the third quarter of 2025 was 7.1 percent year-on-year, driven by public sector investment, with defense accounting for 4.7 percent of GDP in 2025 – an investment rate among the highest in Europe. The industrial sector experienced growth of 4.9 percent, and logistics and transport by 5.3 percent. This is not a slowdown in capital formation, but rather its transformation.

The European defense strategy as an investment catalyst

Herein lies the crux of the matter: Europe is engaged in a defensive arms buildup, and Poland is the hub. In September 2025, the European Union allocated €150 billion in loans under the "Security for Europe" (SAFE) program – a new European defense financing mechanism. Poland, as a geographically exposed frontline nation on the Russian border, received €43.7 billion, the largest single allocation. These funds are not intended for traditional defense purchases – they are meant to build up the European defense industry and secure long-term capabilities.

In parallel, Poland secured an additional €59.8 billion from the EU Recovery and Resilience Facility (RRF), the European recovery financing program. Together with national funds, Poland plans to invest between €155 and €167 billion in 2025 – roughly 18 percent of its GDP, well above the EU average of 22 percent in 2023, but increasing rapidly. This level of investment is unprecedented in Polish economic history.

This public investment momentum is attracting companies like a magnet. In October 2025, the German defense company Rheinmetall signed a letter of intent with the Polish state-owned holding company Polska Grupa Zbrojeniowa (PGZ) to establish a joint venture for the production of armored support vehicles—a European production center for recovery vehicles, mine clearance vehicles, and armored bridge-laying vehicles. This is not a one-off order; it is the announcement of a long-term industrial partnership at the European level. Rheinmetall contributes technology and expertise, while PGZ provides production capacity and access to European funding. This strategic alliance implicitly states that the defense industry in Europe will not be concentrated in France or Germany, but rather decentralized and distributed across countries like Poland.

Our EU and German expertise in business development, sales and marketing

Our EU and German expertise in business development, sales and marketing - Image: Xpert.Digital

Industry focus areas: B2B, digitalization (from AI to XR), mechanical engineering, logistics, renewable energies and industry

More information here:

A thematic hub offering insights and expertise:

- Knowledge platform covering global and regional economies, innovation and industry-specific trends

- A collection of analyses, insights, and background information from our key areas of focus

- A place for expertise and information on current developments in business and technology

- A hub for companies seeking information on markets, digitalization, and industry innovations

Germany's silent exodus: How Poland is becoming Europe's new economic engine

Technological sectoralism: Volkswagen, Lufthansa, Google and Microsoft

In less publicly noticed sectors, a quiet transformation process is underway. In October 2025, Volkswagen announced the expansion of its factory in Września, Poland – an investment of approximately 1.5 billion zlotys, or 350 million euros. The company will construct two new production halls totaling 60,000 square meters, equipped with 150 new robots to produce the next generation of the all-electric e-Crafter. The foundation stone was laid in November 2025, and completion is planned for 2027. Volkswagen's commitment signals something crucial: European electromobility will be manufactured not only in Germany but also in Poland. Space is too limited in Germany, labor costs are too high, and the skilled workforce in Poland is sufficiently qualified.

In the aviation sector, the joint venture XEOS, a joint venture between GE Aerospace and Lufthansa Technik, opened a state-of-the-art maintenance, repair, and overhaul (MRO) facility in Środa Śląska, near Wrocław, in March 2025. Spanning 35,000 square meters and employing 250 people, XEOS focuses on the maintenance of CFM LEAP engines used in Boeing 737 MAX and Airbus A320neo aircraft. GE Aerospace stated that construction costs were approximately $250 million, with an additional $40 million in investment planned for 2025. This is not a second-rate repair shop—it is a world-class MRO facility with substantial capital requirements. The decision to build it in Poland, rather than in Hamburg or Toulouse, speaks to robust operational advantages and a reliable workforce.

Similar patterns are emerging in the areas of artificial intelligence and cloud infrastructure. Microsoft announced an investment of approximately €680 million in 2025 to expand its cloud and AI infrastructure in Poland. Google, Amazon, and IBM have also signaled their interest in investing in Polish tech ecosystems. The Polish IT sector already generates around 10 percent of the country's GDP, with approximately 40 percent of the country's GDP coming from the digital sector – a remarkable figure that underscores Poland's importance as a technology hub.

From Cost Play to Value Play: The Ideological Shift

Why this massive reallocation of capital? The answer lies in the fundamental paradigm shift about what “competitiveness” means in modern Europe. While the 1990s and 2000s were dominated by the search for cost savings—productivity gains through outsourcing to low-wage countries—this has reversed due to four overlapping trends.

First, Polish labor costs are no longer a differentiator. With average manufacturing wages approaching those in the western EU, the cost argument has weakened. At the same time, the available skilled labor is a real bottleneck. Poland produces over 80,000 engineering and IT graduates annually, a volume that Western Europe struggles to replicate. For companies manufacturing high-quality electronics, automotive components, or aerospace parts, access to a stable pool of skilled professionals is invaluable.

Secondly, European funding is unprecedented. The combination of the RRF, SAFE, and Polish national investments created an investment framework that does not exist in Western Europe. West German states compete with other EU regions for funding; Poland receives massive direct transfers. This is not fair competition, but a deliberate European redistribution mechanism designed to strengthen the integration and competitiveness of the eastern periphery.

Thirdly: The geopolitical security argument. With the full-scale war in Ukraine and the latent tensions on Europe's eastern border, the geographical relocation of production capacities away from globalized just-in-time logistics to regional, European supply chains has become a national security imperative. This is the concept of "nearshoring" or "friendshoring"—companies building capacities in reliable, geographically close markets. Poland, as a NATO and EU member with stable institutions, fulfills this requirement.

Fourth: The necessity of electromobility and the green transformation. The European Union has committed to the world's most aggressive decarbonization target. This requires massive investments in battery production, charging networks, and the associated digital infrastructure. Poland has positioned itself as a production hub for this transition – with Bosch investing €1.2 billion in a heat pump factory, and VW's new e-Crafter factory in Września. The green transformation cannot be carried out in Germany alone; it needs geographical diversification.

The danger: Can Germany and the Eurozone keep pace?

This leads to an uncomfortable reality for the German economy. While German industry grapples with deindustrialization issues—the outflow of capital to higher wages and a less favorable investment climate—Poland is building a new economy. A KPMG survey conducted in cooperation with the German Eastern Business Association revealed that 51 percent of German companies considering relocating production to Central and Eastern Europe cite Poland as their preferred location. Romania follows with 43 percent, and Ukraine with 41 percent. For German SMEs, the decision is simple: when it comes to a factory in the East, it's Poland. This is a vote for stability, infrastructure, and skilled workers.

And yet: 22 percent of German companies are planning such a relocation within the next year, and 56 percent within five years. This is no longer a niche strategy – it's becoming the norm. The cumulative effects of these shifts will impact Germany and Western Europe more significantly than current political debates suggest. Not through a shock, but through gradual technological and productive decline.

The downside: The challenge of cross-border complexity

German companies investing in Poland or cooperating with Polish subsidiaries face a new level of administrative complexity that is often underestimated. The Polish tax authorities have significantly intensified their auditing activities over the past five years. Between 2019 and 2024, over 45 billion zlotys – approximately 10.5 billion euros – in tax violations were uncovered, of which 27.5 billion zlotys were discovered during customs and tax audits and 18 billion zlotys during standard tax audits. The average tax violation per audit amounted to over one million zlotys. With an efficiency rate of 98 percent for tax audits and 94 percent for customs and tax audits, meticulous compliance is not optional for companies.

In addition, there are the transfer pricing requirements. The German and Polish tax authorities both follow OECD guidelines, but their practical implementation diverges. German companies with Polish subsidiaries must maintain documentation demonstrating compliance with the "arm's length principle"—that is, that all prices between group companies are at market rates. The thresholds are low: For services, the documentation requirement in Poland begins with transactions exceeding two million zlotys. For goods or financial transactions, the threshold is ten million zlotys. The documentation itself must be submitted by October 31st of each year, and the report to the authorities by November 30th.

A German-Polish manufacturing company with separate accounting in Warsaw must therefore simultaneously meet the following requirements: (1) Double-entry bookkeeping in accordance with German Commercial Code (HGB) and the Polish Tax Code; (2) Double-entry bookkeeping in accordance with Polish law; (3) Transfer pricing documentation in accordance with OECD guidelines in the local language; (4) Correct accounting of the value added by the permanent establishment; (5) Compliance with customs inspections at the German-Polish border; (6) Reporting obligations under BEPS and CRS (Common Reporting Standard); (7) Verification of supply chains under the due diligence requirements of the Supply Chain Due Diligence Act (LkSG). An error in any of these categories can lead to significant penalties – not only through back taxes, but also through fines of up to 720 daily rates per violation in Poland.

The strategic conclusion: The new Europe is taking shape

Poland's growth is not a cyclical phenomenon. It is the manifestation of a structural reorganization of the European economy. In the 1990s, the continent embraced globalization—offshoring to China, just-in-time logistics, specialization in high-value services in the West. This architecture has broken down. Supply chains are disrupted, geopolitical uncertainty is endemic, and energy realities have shifted. What is emerging is a regionalized, Eurocentric production system, with Poland acting as a pivot between the wealthier West and the uncertain, fragmented markets of Southeast Europe and Russia.

For German and Western European capital, this is both a threat and an opportunity. A threat because Germany's long industrial tradition is gradually being devalued as factories relocate eastward and skilled workers follow the west. An opportunity because this restructuring need not run counter to German interests – it can be used for modernization, for relocating low-margin production to locations with better cost structures, and for concentrating German capacity on higher-value, design-driven industries.

Volkswagen isn't choosing Poland because Germany is deindustrialized, but because the logic of modern manufacturing dictates that high-volume production of standardized electric vans must take place at geographically diversified locations. Rheinmetall isn't choosing Poland because the German defense industry is weak, but because European defense must be decentralized. Microsoft isn't choosing Poland because Germany isn't digital, but because its data center infrastructure needs to be distributed across continents.

The real risk lies in Western Europe – in Germany, France, and the Benelux countries – which are ignoring or actively hindering this change. The economic divergence between the Eurozone and Poland will worsen if Western European countries resort to protectionist or beggar-thy-neighbor fiscal policies. Poland has accepted geopolitical reality; the question is whether the West will do the same.

Your global marketing and business development partner

☑️ Our business language is English or German

☑️ NEW: Correspondence in your native language!

Konrad Wolfenstein

I and my team are happy to be available to you as your personal advisor.

You can contact me by filling out the contact form here wolfenstein@xpert.digital:or simply call me at +49 7348 4088 965. My email address is

I'm looking forward to our joint project.

☑️ SME support in strategy, consulting, planning and implementation

☑️ Creation or realignment of the digital strategy and digitization

☑️ Expansion and optimization of international sales processes

☑️ Global & Digital B2B trading platforms

☑️ Pioneer Business Development / Marketing / PR / Trade Fairs

🎯🎯🎯 Benefit from Xpert.Digital's extensive, five-fold expertise in one comprehensive service package | BD, R&D, XR, PR & Digital Visibility Optimization

Benefit from Xpert.Digital's extensive, five-fold expertise in a comprehensive service package | R&D, XR, PR & Digital Visibility Optimization - Image: Xpert.Digital

Xpert.Digital possesses in-depth knowledge across various industries. This allows us to develop tailored strategies precisely aligned with the requirements and challenges of your specific market segment. By continuously analyzing market trends and monitoring industry developments, we can act proactively and offer innovative solutions. The combination of experience and expertise generates added value and provides our clients with a decisive competitive advantage.

More information here: