Financial planning and financial advice – Image: Xpert.Digital / Yuri Shevtsov|Shutterstock.com

Financial development and financial planning

The financial assets of German citizens amounted to almost €7 trillion at the end of 2020. This comprises private insurance and securities holdings as well as bank deposits. Despite the current low interest rate environment, household savings accounts for a significant portion of the total private assets held in German banks.

In Germany, around 42 percent of the population rate their current financial situation as good or very good. However, only 22 percent of Germans rate their level of information about financial matters and investments as good.

Do you know how the German population feels about saving money versus living a good life? Only 22% of Germans rate their financial knowledge as good. In Austria, the figure is 36%. Why is this the case, given the importance of such a topic? Do you know how much wealth is managed by private households worldwide? How does the population assess their current financial situation? What is the trend in the financial assets of private households in Germany?

You can find an independent overview here:

Free PDF download on 'Savings behavior of private households'

Important note: The PDF is password protected. Please contact me. The PDF is, of course, free of charge

.

German version – To view the PDF, please click on the image below

.

Savings behavior of private households – PDF Download

👨🏻 👩🏻 👴🏻 👵🏻 For private households

Xpert.Digital helps you choose your independent financial service provider. With our AI-powered digital expertise, we provide you with up-to-date data and figures.

Financial planning is worthwhile for everyone, regardless of income and assets. It doesn't always have to be a complete and elaborate financial plan. Depending on the situation, specific plans for certain topics, such as retirement planning, may suffice.

📣 For entrepreneurs such as founders and start-ups

The financial plan is the basis for the business plan. It should be updated regularly. Clearly defined company goals help with this.

With over 1,000 articles published, we cannot present all topics here. Therefore, you will find a small selection of our work here, and we would be delighted if we have sparked your interest in learning more about us:

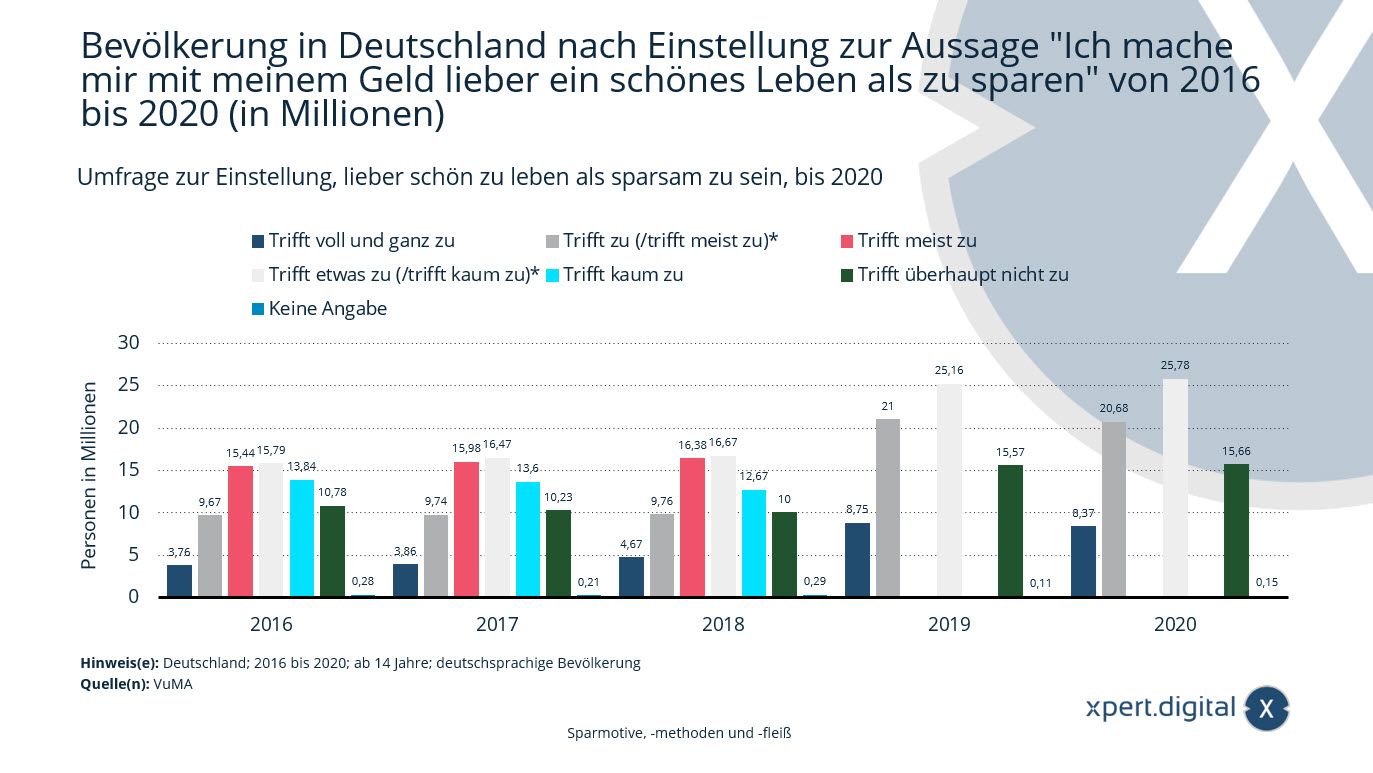

Survey on attitudes towards preferring to live well rather than being frugal

Survey on attitudes towards living well rather than being frugal – Image: Xpet.Digital

In 2020, there were approximately 8.37 million people aged 14 and over in the German-speaking population who fully agreed with the statement "I would rather spend my money on a good life than on saving it".

Population in Germany according to attitude towards the statement “I would rather spend my money on a good life than saving it” from 2016 to 2020 (in millions)

That's absolutely true

- 2016 – 3.76 million

- 2017 – 3.86 million

- 2018 – 4.67 million

- 2019 – 8.75 million

- 2020 – 8.37 million

Applies (/mostly applies)*

- 2016 – 9.67 million

- 2017 – 9.74 million

- 2018 – 9.76 million

- 2019 – 21 million

- 2020 – 20.68 million

This is usually true

- 2016 – 15.44 million

- 2017 – 15.98 million

- 2018 – 16.38 million

Does this apply (/hardly apply)*

- 2016 – 15.79 million

- 2017 – 16.47 million

- 2018 – 16.67 million

- 2019 – 25.16 million

- 2020 – 25.78 million

This hardly applies

- 2016 – 13.84 million

- 2017 – 13.60 million

- 2018 – 12.67 million

That's completely untrue

- 2016 – 10.78 million

- 2017 – 10.23 million

- 2018 – 10 million

- 2019 – 15.57 million

- 2020 – 15.66 million

Not specified

- 2016 – 0.28 million

- 2017 – 0.21 million

- 2018 – 0.29 million

- 2019 – 0.11 million

- 2020 – 0.15 million

* Change to the query: From 2019 onwards, the levels “applies” and “mostly applies” were combined, and “somewhat applies” and “hardly applies” were also combined.

Information on the target population: The basis is the German-speaking population aged 14 and over. Information on the total sample:

2016: 23,102 respondents, extrapolated to 69.56 million

respondents, extrapolated to 70.09

million people; 2018: 23,086 respondents, extrapolated to 70.45 million people;

2019: 23,120 respondents, extrapolated to 70.60 million people;

2020: 23,138 respondents, extrapolated to 70.63 million people.

The values shown refer to the following studies: 2016: VuMA 2017; 2017: VuMA 2018; 2018: VuMA 2019; 2019: VuMA 2020; 2020: VuMA 2021

Values have been rounded for better understanding of the statistics.

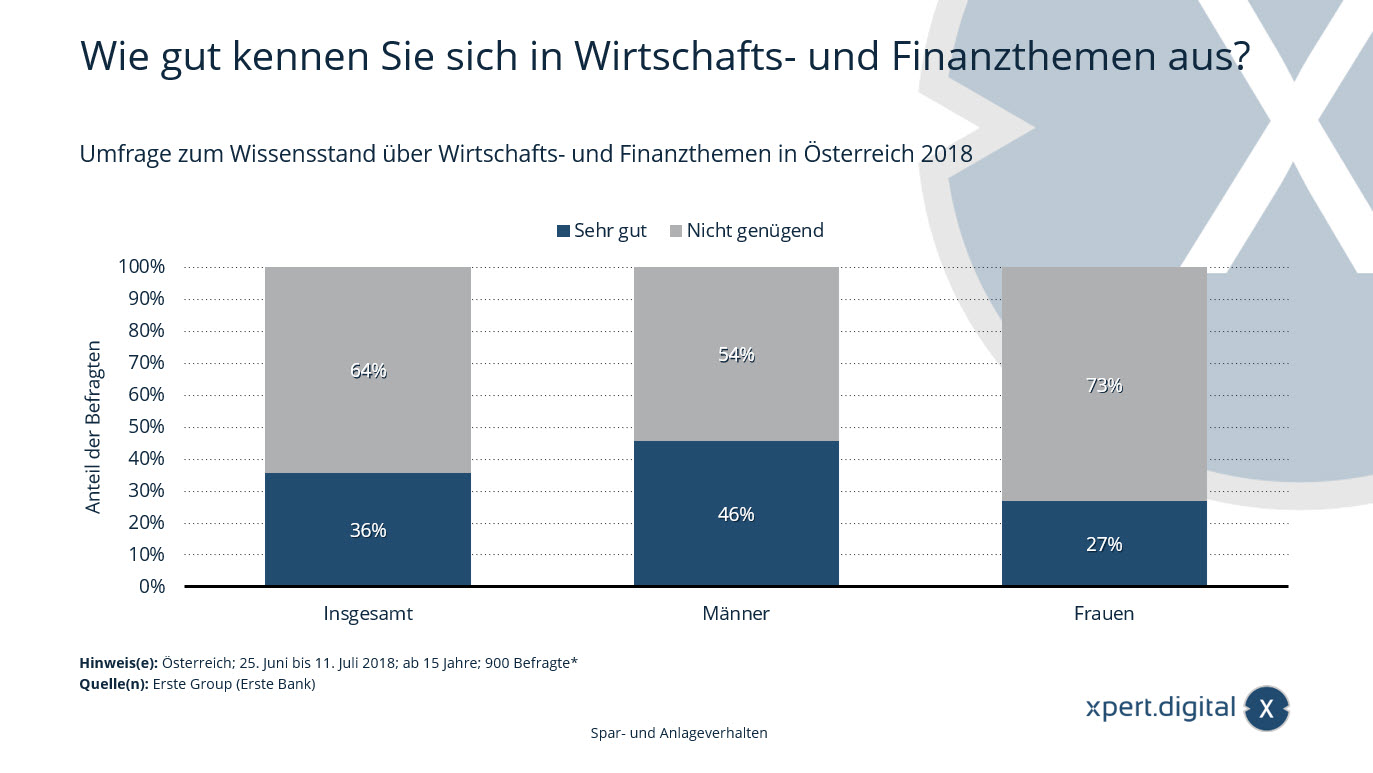

Survey on knowledge of economic and financial topics

Survey on knowledge of economic and financial topics

The statistic shows the results of a survey on the level of knowledge about economic and financial topics in Austria in 2018. 36 percent of respondents stated that they were very knowledgeable about economic and financial topics.

How well do you know your way around economic and financial topics?

Very good

- A total of 36%

- Men 46%

- Women 27%

Not enough

- A total of 64%

- Men 54%

- Women 73%

* 100 interviews were conducted per federal state to allow for separate analysis. For the overall analysis, the federal states were weighted according to their representativeness level.

The source does not provide precise details regarding the question. Therefore, the wording used here may differ slightly from the actual survey.

Type of survey: Computer-assisted telephone interviews (CATI)

Number of respondents: 900 respondents*

Household assets under management by region

Household assets under management by region – Image: Xpert.Digital

This statistic shows the globally managed assets of private households in comparison of the years 1999, 2009 and 2019, broken down by region.

In 2019, the wealth of private households in Latin America amounted to approximately US$5.6 trillion. Twenty years earlier, private wealth was only US$0.6 trillion.

Household assets under management in 1999, 2009 and 2019 by region worldwide (in trillions of US dollars)

Household assets under management by region 2019

- Worldwide – 226.40 trillion US dollars

- North America – 100 trillion US dollars

- Western Europe – 46.80 trillion US dollars

- Asia (excluding Japan) – US$42.10 trillion

- Japan – 17.60 trillion US dollars

- Latin America – 5.60 trillion US dollars

- Oceania – 4.70 trillion US dollars

- Middle East – 4.20 trillion US dollars

- Eastern Europe and Central Asia – 3.70 trillion US dollars

- Africa – 1.60 trillion US dollars

Household assets under management by region 2009

- Worldwide – 124.60 trillion US dollars

- North America – 54.40 trillion US dollars

- Western Europe – 31.90 trillion US dollars

- Asia (excluding Japan) – 15.20 trillion US dollars

- Japan – 14.40 trillion US dollars

- Latin America – 2 trillion US dollars

- Oceania – 2.40 trillion US dollars

- Middle East – 2.20 trillion US dollars

- Eastern Europe and Central Asia – 1.50 trillion US dollars

- Africa – 0.70 trillion US dollars

Household assets under management by region, 1999

- Worldwide – 80.50 trillion US dollars

- North America – 36.70 trillion US dollars

- Western Europe – 22.30 trillion US dollars

- Asia (excluding Japan) – 5.10 trillion US dollars

- Japan – 13 trillion US dollars

- Latin America – 0.60 trillion US dollars

- Oceania – 1 trillion US dollars

- Middle East – 1 trillion US dollars

- Eastern Europe and Central Asia – 0.50 trillion US dollars

- Africa – 0.30 trillion US dollars

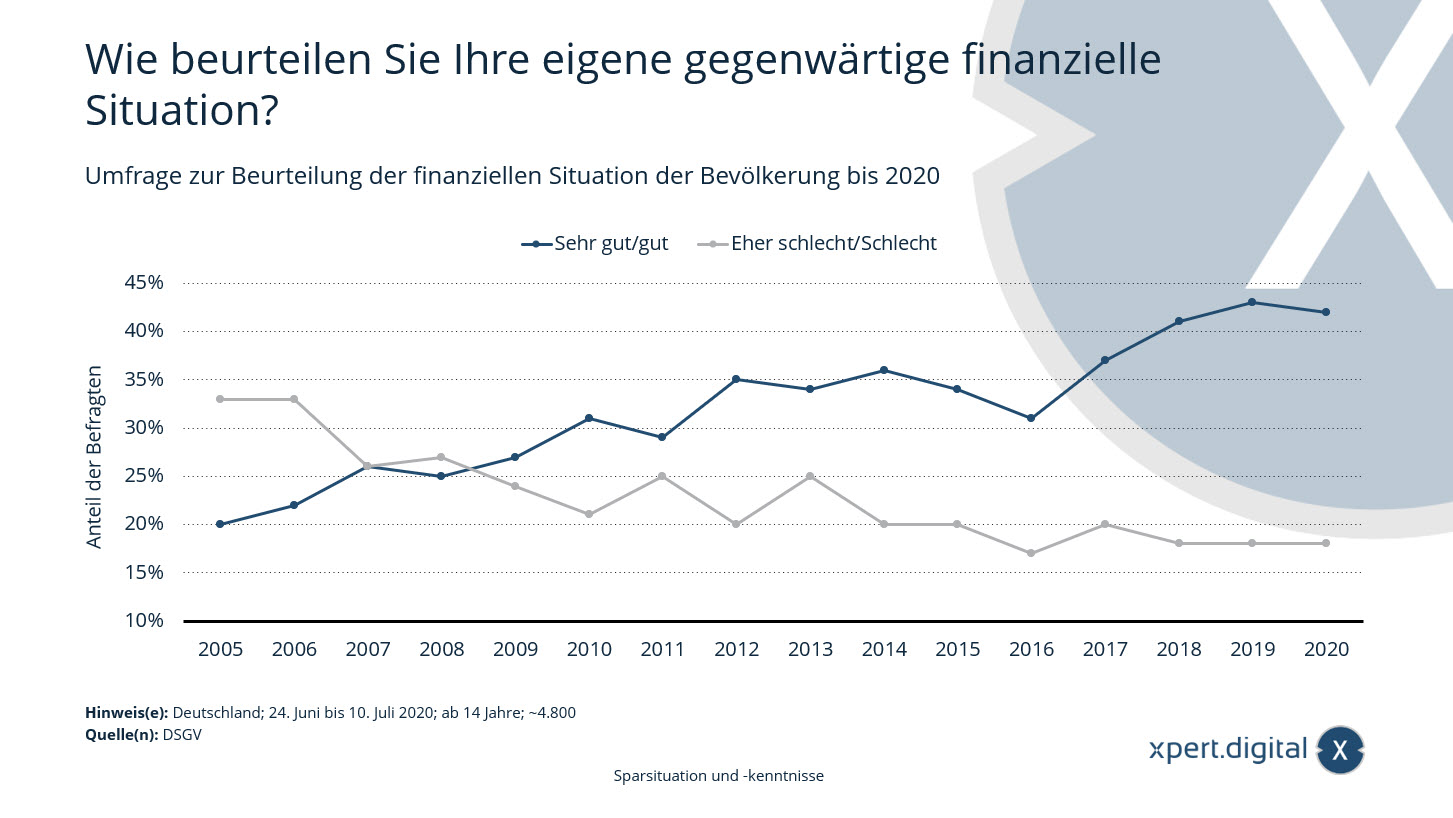

Survey on the assessment of the financial situation of the population in Germany

Survey assessing the financial situation of the population in Germany – Image: Xpert.Digital

Germans' satisfaction with their finances is declining slightly – according to the 2020 Wealth Barometer of the German Savings Banks Association, around 42 percent of German citizens rate their current financial situation as very good to good. Last year, this figure was 43 percent. Overall, however, the proportion of people satisfied with their financial situation has more than doubled in the past 15 years.

Survey on the assessment of the population's financial situation up to 2020:

How do you assess your own current financial situation?

Very good/good

- 2005 – 20 %

- 2006 – 22 %

- 2007 – 26 %

- 2008 – 25 %

- 2009 – 27 %

- 2010 – 31 %

- 2011 – 29 %

- 2012 – 35 %

- 2013 – 34 %

- 2014 – 36 %

- 2015 – 34 %

- 2016 – 31 %

- 2017 – 37 %

- 2018 – 41 %

- 2019 – 43 %

- 2020 – 42 %

Rather bad/Bad

- 2005 – 33 %

- 2006 – 33 %

- 2007 – 26 %

- 2008 – 27 %

- 2009 – 24 %

- 2010 – 21 %

- 2011 – 25 %

- 2012 – 20 %

- 2013 – 25 %

- 2014 – 20 %

- 2015 – 20 %

- 2016 – 17 %

- 2017 – 20 %

- 2018 – 18 %

- 2019 – 18 %

- 2020 – 18 %

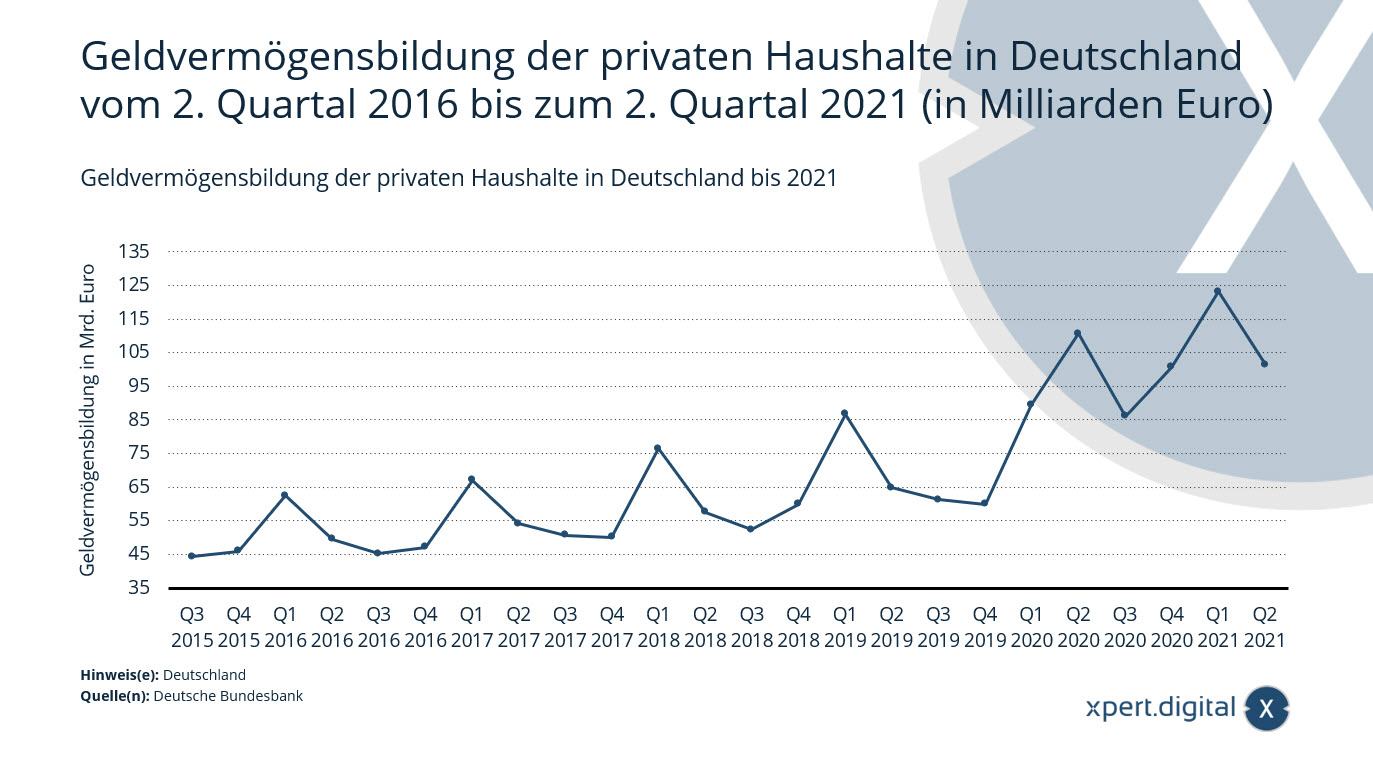

Financial wealth accumulation of private households in Germany

Financial wealth accumulation of private households in Germany – Image: Xpert.Digital

This statistic shows the development of financial asset accumulation by private households in Germany from the second quarter of 2016 to the second quarter of 2021. The net transaction-related financial asset accumulation of private households amounted to approximately 101.4 billion euros in the second quarter of 2021.

Financial wealth accumulation of private households in Germany from the 2nd quarter of 2016 to the 2nd quarter of 2021 (in billion euros)

- Q2 2021 – 101.4 billion euros

- Q1 2021 – 123.2 billion euros

- Q4 2020 – 100.7 billion euros

- Q3 2020 – 86.1 billion euros

- Q2 2020 – 110.6 billion euros

- Q1 2020 – 89.5 billion euros

- Q4 2019 – 59.9 billion euros

- Q3 2019 – 61.3 billion euros

- Q2 2019 – 64.9 billion euros

- Q1 2019 – 86.7 billion euros

- Q4 2018 – 60 billion euros

- Q3 2018 – 52.4 billion euros

- Q2 2018 – 57.6 billion euros

- Q1 2018 – 76.5 billion euros

- Q4 2017 – 50.1 billion euros

- Q3 2017 – 50.7 billion euros

- Q2 2017 – 54.1 billion euros

- Q1 2017 – 67.1 billion euros

- Q4 2016 – 47.2 billion euros

- Q3 2016 – 45.2 billion euros

- Q2 2016 – 49.5 billion euros

- Q1 2016 – 62.4 billion euros

- Q4 2015 – 46 billion euros

- Q3 2015 – 44.3 billion euros

- Q2 2015 – 47.1 billion euros

- Q1 2015 – 54.2 billion euros

- Q4 2014 – 40.8 billion euros

- Q3 2014 – 35.9 billion euros

- Q2 2014 – 37.7 billion euros

- Q1 2014 – 47.8 billion euros

- Q4 2013 – 34.3 billion euros

- Q3 2013 – 30.1 billion euros

- Q2 2013 – 35.6 billion euros

- Q1 2013 – 41.5 billion euros

- Q4 2012 – 35.5 billion euros

- Q3 2012 – 29.6 billion euros

- Q2 2012 – 37.3 billion euros

- Q1 2012 – 44.4 billion euros

- Q4 2011 – 34.6 billion euros

- Q3 2011 – 29 billion euros

- Q2 2011 – 31.7 billion euros

- Q1 2011 – 43.5 billion euros

Financial assets of private households at a new record high

Deutsche Bundesbank – Press release – 16.07.2021 – Image: bonoc|Shutterstock.com

The financial assets of private households grew by €192 billion to €7,143 billion in the first quarter of 2021. This marked the first time they exceeded the €7 trillion mark. In addition to purchases of financial assets, valuation gains on stocks and investment fund units were a major contributing factor to this increase.

The net accumulation of financial assets by private households amounted to €129 billion, significantly higher than in previous quarters. A substantial increase of €27 billion was attributable to a substantial rise in claims against insurance companies. €47 billion flowed into cash and demand deposits, less than in the previous quarter. Overall, private households continue to exhibit a strong preference for liquid or low-risk investments. At the same time, the continued increase in capital market activity indicates a heightened focus on returns. Private households purchased €25 billion worth of investment fund units – more than ever before. They also bought a net total of €3 billion worth of shares and other equity securities, primarily investing in domestic companies. Conversely, their holdings of debt securities decreased by a net €3 billion. The valuation-related increase in financial assets of €63 billion in the first quarter of 2021 resulted mainly from price gains in shares and investment fund units.

Household debt rose by €17 billion due to transaction-related factors, a smaller increase than previously. At the end of the first quarter, their liabilities stood at €1,978 billion. The household debt ratio was 59.5 percent, the highest it has been since 2010. This ratio is defined as the sum of liabilities relative to nominal gross domestic product (a rolling four-quarter total). This upward trend continues. This development can be attributed to both rising household debt and the continued year-on-year decline in nominal gross domestic product.

The net financial assets of private households amounted to 5,165 billion euros at the end of the first quarter.

Strong external financing is causing companies' debt ratios to rise significantly again

External financing for non-financial corporations reached its highest level since 2018, at €90 billion. This increase was primarily driven by other liabilities, mainly trade payables, which rose by €54 billion. Borrowing also regained importance after two weak quarters, reaching €20 billion. Shares and equity instruments worth €15 billion were issued, slightly above the average of the previous four quarters.

Due to dynamic external financing and significant valuation effects, the liabilities of non-financial corporations rose considerably. At the end of the first quarter of 2021, they amounted to €7,734 billion. The debt-to-equity ratio of non-financial corporations was 82.2 percent. This ratio is calculated as the sum of loans, debt securities, and pension provisions in relation to nominal gross domestic product (rolling four-quarter total). After increasing by only 0.3 percentage points in the fourth quarter of 2020, the rise in the reporting quarter was significantly higher at 0.9 percentage points.

The financial assets of non-financial corporations grew by €262 billion in the first quarter of 2021, taking into account all transactions and valuation effects – the strongest growth since 2015. This brought the total to €5,565 billion. Transaction-related increases in financial assets made a significant contribution of €86 billion. After four quarters of continuous unwinding, non-financial corporations significantly increased their holdings of financial derivatives and employee stock options by €22 billion. Other receivables, including trade credits and advance payments, also made a similarly significant contribution to financial asset growth. Receivables from cash and deposits also rose sharply again, increasing by €20 billion. Valuation gains, on the other hand, were primarily observed in shares and other equity securities.

However, since liabilities rose even more sharply than financial assets, net financial assets decreased more significantly than in the previous period, amounting to minus 2,169 billion euros.

Due to revisions of the national financial accounts and the national accounts that have been carried out in the meantime, the information in this press release is not comparable with that in previous press releases.

Xpert.Digital for Bellenberg, Vöhringen, Illerrieden and Illertissen. Support for your independent financial planning, wealth management and investment advice

Konrad Wolfenstein

I am happy to answer any further questions or provide assistance.

You can contact me by filling out the contact form below or simply call me on 0731 550 40 117 .

I'm looking forward to our joint project.

Write to me

Xpert.Digital – Konrad Wolfenstein

Xpert.Digital is a hub for industry focusing on digitalization, mechanical engineering, logistics/intralogistics and photovoltaics.

With our 360° Business Development solution, we support renowned companies from new business to after-sales.

Market intelligence, smarketing, marketing automation, content development, PR, mail campaigns, personalized social media and lead nurturing are part of our digital tools.

You can find more information at: www.xpert.digital – www.xpert.solar – www.xpert.plus

Keep in touch