Today's Amazon Web Services (AWS) outage and the cloud trap: When digital infrastructure becomes a geopolitical weapon – Image: Xpert.Digital

Besides Amazon itself, major platforms such as Slack, Zoom, Signal, Snapchat, Canva, Fortnite, Roblox, as well as government and banking services were also massively affected by the AWS outage at times

Problem outline and relevance: Recognizing a new form of dependency

Today, October 20, 2025, at 12:11 UTC (Coordinated Universal Time), the modern internet came to a standstill. Not due to a cyberattack, not due to a natural disaster, but due to a technical failure in a single data center in Northern Virginia. Amazon Web Services, the world's dominant cloud provider with a 30 percent market share, reported increased error rates in its US-EAST-1 region. What followed was a global blackout of digital services of unprecedented scope.

Signal and Slack, the communication backbones of modern businesses, fell silent. Canva, the design tool of millions of creatives, froze. Snapchat, Fortnite, Roblox – an entire generation of digital users lost access to their virtual worlds. Financial platforms like Coinbase and Venmo experienced outages, and banks in the UK could no longer provide their services. Even Amazon's own products – Prime Video, Alexa, Ring's smart doorbells – failed, exposing the vulnerability of an interconnected ecosystem.

The outage affected 28 AWS services and lasted several hours before a full recovery was achieved. The source was Amazon DynamoDB, a NoSQL database platform that serves as a fundamental building block for countless applications. What technically appeared to be a local DNS problem turned out to be a systemic vulnerability of the globalized digital economy: its structural dependence on a handful of American hyperscalers.

This incident is far more than a technical glitch. It is a symptom of a deeper economic and geopolitical problem. While Europe has spent the last few years painstakingly discussing its energy dependence on Russian gas and developing diversification strategies, a far more dangerous dependence has taken root: that on digital infrastructure from the USA. The comparison with Gazprom is not an exaggeration – it is precise. In both cases, we are dealing with critical infrastructure, in both cases with monopolistic structures, in both cases with geopolitical leverage.

The crucial difference: While gas deliveries flow visibly through pipelines and are politically controllable, data migration occurs invisibly, in real time, and under the jurisdiction of foreign legal systems. The US Cloud Act of 2018 grants American authorities extraterritorial access to all data managed by US companies—regardless of where the servers are physically located. European companies that store their data with AWS, Microsoft Azure, or Google Cloud are thus effectively subject to American jurisdiction. This directly conflicts with the European General Data Protection Regulation (GDPR) and systematically erodes the continent's digital sovereignty.

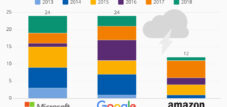

The scale of this dependency becomes tangible through numbers: AWS controls 30 percent of the global cloud market, Microsoft Azure 20 percent, and Google Cloud 12 percent. Together, these three US corporations control 62 percent of the world's cloud infrastructure. The situation is even more dramatic in Europe. While the German federal government officially promotes a multi-cloud strategy and digital sovereignty, it actually uses 32 cloud services – the vast majority from Microsoft, AWS, Google, and Oracle. The planned sovereign cloud for the federal administration is based on none other than Microsoft Azure.

This analysis examines the economic, geopolitical, and strategic dimensions of this dependency. It traces its historical development, analyzes current market mechanisms, compares different national strategies, and assesses the risks as well as potential development paths. The central thesis is that Europe's cloud dependency poses a greater strategic threat than its former energy dependency because it affects the entire digital value chain, national sovereignty, and social communication—and because Europe has yet to develop a convincing response.

Services widely affected

Amazon's own services

- Amazon.com

- Prime Video

- Alexa

- Amazon Music

- ring

- IMDB

Communication and AI services

- signal

- Slack

- zoom

- Perplexity AI

- WhatsApp (occasionally)

Gaming and Entertainment

- Fortnite

- Roblox

- Epic Games Store

- PlayStation Network

- Steam

- Duolingo

- Clash of Clans / Clash Royale

- Pokémon Go

- Rocket League

Social Media and Lifestyle

- Snapchat

- Strava

- Peloton

- Tinder

Productivity and cloud tools

- Canva

- Atlassian

- Jira

- Asana

- Smartsheet

Financial and crypto services

- Coinbase

- Venmo (PayPal)

- Lloyds Bank

- Halifax

- Square

- Xero

Other institutional systems

- British Government Gateway Services (gov.uk and HMRC)

- Cloudflare

- BT, EE, Vodafone, Sky Mobile

The Rise of a Digital Empire: How Silicon Valley Conquered the Infrastructure of the Global Economy

The dominance of American cloud providers is no accident, but rather the result of strategic decisions, technological pioneering achievements, and targeted investment policies over more than a decade and a half. The story begins in 2006, when Amazon Web Services was founded as a subsidiary of the online retailer Amazon. What was initially conceived as an internal solution for handling peak loads in e-commerce evolved into a revolutionary business idea: offering computing capacity as a service, scalable, billed on a usage basis, and without upfront investment.

The Infrastructure-as-a-Service (IaaS) business model revolutionized traditional IT economics. Companies no longer had to invest millions in their own data centers, procure hardware, or hire administrators. They could rent servers by the minute, scale as needed, and expand globally—all without capital risk. For startups, this was revolutionary: with a credit card and an idea, one could build a globally scalable business. Dropbox, Netflix, Airbnb, Reddit—the most successful digital business models of the 2010s were built on AWS infrastructure.

Microsoft followed suit in 2010 with Azure, initially hesitantly, then with the full force of the corporation. The advantage: deep integration into the existing Microsoft ecosystem of Windows, Office, and Active Directory. For companies already using Microsoft products, the transition to the Azure cloud was virtually seamless. Google Cloud Platform launched in 2011, initially positioned primarily for developers and data-intensive applications, later with an increasing focus on artificial intelligence.

The competitive advantage of the American hyperscalers was based on several factors. First, timing. They entered the market years before their European or Asian competitors and were able to build network effects, economies of scale, and ecosystems. Second, enormous investments. AWS alone invested billions in building data centers, network infrastructure, and product development—financed by Amazon's profitable e-commerce division. Microsoft mobilized its gigantic cash reserves, and Google used its dominance in the search engine market for cross-financing.

Third: Innovation in breadth and depth. AWS now offers over 200 fully featured services – from simple virtual machines to specialized databases and machine learning platforms. This product portfolio was created through aggressive product development, strategic acquisitions, and continuous expansion. No European provider has been able to match this pace and breadth.

Fourth: aggressive pricing. Hyperscalers, due to their size, were able to achieve economies of scale that undercut smaller competitors. At the same time, the usage-based billing model enabled low barriers to entry. Companies experimented with cloud services without making large upfront commitments – and then became trapped in technological dependencies that made switching prohibitively expensive.

Europe systematically missed this shift. While cloud computing became a national technology strategy in the US, European governments and companies remained entrenched in traditional IT structures. Telecommunications providers, the natural candidates for cloud infrastructure, were preoccupied with acquisitions, regulatory issues, and expanding mobile networks. Software providers like SAP focused on their classic business models. By the time the strategic relevance of cloud infrastructure became apparent, the market was already saturated.

The breakthrough for cloud dominance came with the COVID-19 pandemic in 2020. Within a few weeks, millions of companies had to send their employees to work from home, implement digital collaboration tools, and ramp up e-commerce capacity. The hyperscalers were the only ones able to meet this explosive demand. Companies migrated to the cloud at a breathtaking pace – often hastily, without strategy, and without regard for the risks of dependency.

The result is today's market structure: AWS generates $124 billion in annual revenue and is growing at 17 percent, Microsoft Azure is growing even faster at 21 percent and generates over $40 billion annually, and Google Cloud is expanding at 32 percent. The European alternatives – OVHcloud, IONOS, and Scaleway – operate on a completely different scale. OVHcloud, the largest European cloud provider, generates approximately three billion euros in revenue – less than three percent of AWS.

China pursued a fundamentally different path. The government recognized the strategic importance of cloud infrastructure early on and specifically promoted domestic champions. Alibaba Cloud, which emerged from the e-commerce giant Alibaba, dominates the Chinese market with 35.8 percent. Huawei Cloud, Tencent Cloud, and Baidu Cloud share further market shares. American hyperscalers are effectively excluded in China—partly due to technical barriers, partly due to regulatory hurdles, and partly due to political pressure. The result is a largely self-sufficient digital ecosystem.

The course set over the past 15 years has created a situation in which the global digital economy rests on the infrastructure of a few American corporations. These corporations control not only computing power and storage space, but increasingly also the platforms for artificial intelligence, data analytics, and cloud-native application development. They define standards, dominate ecosystems, and create lock-in effects. The consequence: Europe has lost control of its digital infrastructure – voluntarily, through inaction and strategic blindness.

The ecosystem of dependency: actors, mechanisms and economic drivers of cloud concentration

The dominance of American hyperscalers is the product of several reinforcing market mechanisms that systematically hinder any attempt to catch up. At the heart of this is the phenomenon of vendor lock-in – the technological and economic imprisonment of customers in proprietary systems.

Cloud services may appear standardized and interchangeable on the surface. However, AWS, Azure, and Google Cloud actually use different APIs, network models, security architectures, and service structures. An application developed on AWS cannot simply be migrated to Azure. Databases, storage systems, security policies, monitoring tools—everything must be reconfigured, tested, and optimized. The migration costs can exceed the original development costs.

This lock-in is not accidental, but strategically intentional. Hyperscalers are investing heavily in proprietary add-on services that make their platforms more attractive – and switching more expensive. AWS offers over 200 services, from specialized databases and machine learning tools to IoT platforms. Every service used increases dependency. Microsoft leverages integration with Office 365, Teams, and Windows to make Azure attractive – while simultaneously creating an ecosystem that is difficult to leave.

The cost structure exacerbates these mechanisms. Cloud computing initially appears cost-effective: no investment in hardware, no administrators, usage-based billing. But this calculation conceals hidden costs. Data transfer between regions is expensive. Storage costs accumulate. Complex pricing models with hundreds of options make cost forecasting impossible. Companies that started with a few thousand dollars a month end up paying millions after just a few years.

The insurance company GEICO experienced this firsthand. After ten years of cloud migration, annual costs had risen to over $300 million – 2.5 times higher than projected. The consequence: cloud repatriation, migration back to its own data centers. Dropbox also saved $74.6 million in two years after migrating from AWS to its own infrastructure. The software company 37signals estimates savings of $10 million over five years after leaving AWS.

These examples illustrate a growing trend: cloud repatriation. According to a survey by CIO magazine Barkley, 83 percent of companies plan to move workloads back to private clouds. The reasons are manifold: exploding costs, security concerns, compliance requirements, and performance issues with latency-critical applications.

Nevertheless, the majority of companies remain in the public cloud – not out of conviction, but because they have no alternative. Migrating back to their own infrastructure requires enormous investments, technical expertise, and time. Smaller companies cannot afford this. Even large corporations hesitate given the complexity.

The economic drivers of this concentration also lie on the supply side. Cloud computing is a business of extreme economies of scale. Those who operate more data centers can purchase hardware more cheaply, use electricity more efficiently, and distribute software development across more customers. AWS invests tens of billions of dollars annually in infrastructure – financed by profitable e-commerce and advertising revenues. Microsoft and Google have comparable cash reserves. European competitors cannot match these levels of investment.

Another factor is the ecosystem of developers, partners, and third-party vendors. Millions of developers worldwide have acquired expertise in AWS or Azure technologies. Thousands of software vendors have certified their products on these platforms. Consulting firms have built business models around hyperscaler migrations. This ecosystem generates network effects that smaller vendors cannot replicate.

The actors in this system pursue different, sometimes conflicting, interests. Hyperscalers maximize their market power through lock-in, ecosystems, and aggressive expansion. Companies seek cost efficiency, flexibility, and innovation—but become dependent. Governments face the dilemma between economic efficiency and strategic sovereignty. The EU has created regulatory frameworks with the GDPR and the Data Act, but these do nothing to change the de facto market power of American providers.

The market structure favors further consolidation. Smaller cloud providers are acquired or squeezed out. Specialized niche providers survive in segments like sovereign cloud or edge computing, but cannot replicate the breadth of the hyperscalers. The consequence: an oligopoly of three dominant providers controlling 62 percent of the global market – and growing.

This concentration carries systemic risks. An AWS outage, like the one on October 20, 2025, cripples a significant portion of the global internet. Dependence on a few providers creates single points of failure – technically, economically, and geopolitically. Financial market regulators have already identified concentration risks in the banking sector and are calling for diversification. But a genuine alternative does not exist.

Our EU and German expertise in business development, sales and marketing

Our EU and German expertise in business development, sales and marketing - Image: Xpert.Digital

Industry focus areas: B2B, digitalization (from AI to XR), mechanical engineering, logistics, renewable energies and industry

More information here:

A thematic hub offering insights and expertise:

- Knowledge platform covering global and regional economies, innovation and industry-specific trends

- A collection of analyses, insights, and background information from our key areas of focus

- A place for expertise and information on current developments in business and technology

- A hub for companies seeking information on markets, digitalization, and industry innovations

The dark side of the cloud: Systemic risks that no one can ignore

The current situation: A continent in a digital state of emergency

The disruption of October 20, 2025, marks a turning point in the public perception of digital dependencies. What experts had been warning about for years became a tangible reality for millions of users: modern society rests on fragile digital infrastructure, controlled by a few corporations, vulnerable to outages and extraterritorial access.

The immediate economic damage is difficult to quantify, but substantial. Studies estimate average downtime costs at $9,000 per minute. For Amazon itself, the cost is $220,000 per minute. Extrapolated over several hours of downtime and considering the global reach of the disruption, the total damage likely reaches hundreds of millions of dollars.

But the economic costs are only one aspect. More serious are the strategic implications. The outage hit critical infrastructure: Financial services like Coinbase and Venmo couldn't process transactions. Communication platforms like Signal and Slack failed. Educational platforms like Canvas and Duolingo were inaccessible. Entertainment services like Netflix, Prime Video, and dozens of games crashed.

The geographic distribution of the outage reveals the architecture of the problem. Although the technical error occurred in Northern Virginia, services worldwide were affected. This is due to the centralized architecture of cloud services: Many global services use US-EAST-1 as their primary region because that's where most of the AWS infrastructure is concentrated. Redundancy often exists only on paper.

The frequency of such outages is alarming. AWS has experienced at least seven major outages since 2011. The outage on December 7, 2021, lasted over eight hours and crippled similar services. In February 2017, operator error led to a four-hour outage that caused an estimated $150 to $160 million in damages. The recurrence rate demonstrates that these are not isolated incidents, but rather structural weaknesses in an overloaded system.

Alongside the technical fragility, the legal issues are intensifying. The US Cloud Act of 2018 obliges American companies to grant US authorities access to data upon request – regardless of where the data is stored. This directly conflicts with the European GDPR, which permits data transfers to third countries only under strict conditions. In the 2020 Schrems II ruling, the European Court of Justice declared the Privacy Shield agreement invalid because US surveillance laws are incompatible with EU fundamental rights.

The consequence is a legal gray area. European companies using AWS or Azure potentially violate GDPR – or risk having their data accessed by US authorities. This dilemma remains unresolved. Standard contractual clauses and technical safeguards offer only limited protection. The risk of industrial espionage, government surveillance, and data misuse remains real.

The political response in Europe oscillates between rhetoric and reality. The EU Commission proclaims digital sovereignty as a strategic goal. Germany officially launched its German Administrative Cloud in 2025, based on open standards and multi-cloud principles. France invested €1.8 billion in promoting domestic cloud providers, particularly OVHcloud.

The Gaia-X initiative, launched in 2019 by Germany and France, was intended to create a federated, sovereign data infrastructure for Europe. However, four years later, Gaia-X remains a paper tiger. The initiative defines standards and certification frameworks but offers no competitive infrastructure. Ironically, AWS and Microsoft are associate members of Gaia-X – which undermines the project's credibility.

The reality of German and European administrations is sobering. Despite its official sovereignty strategy, the German government uses 32 cloud services, primarily from Microsoft, AWS, Google, and Oracle. The planned sovereign cloud is based on Microsoft Azure – a US provider, of all companies. The justification: only this way can the necessary scalability and functionality be achieved. This only cements the dependency rather than reducing it.

The European cloud market is deeply fragmented. OVHcloud, the largest European provider, operates 43 data centers worldwide and generates approximately three billion euros in annual revenue. IONOS, a subsidiary of United Internet, focuses on business customers in the DACH region (Germany, Austria, and Switzerland). Scaleway, part of the French Iliad Group, positions itself as an innovative, sustainability-oriented provider for startups. Together, however, these providers barely reach five percent of the European market.

The quantitative gap is dramatic. AWS invests over $30 billion annually in infrastructure and product development. Microsoft and Google maintain similar investment levels. OVHcloud cannot raise such sums. The product range of European providers is narrower, their global presence smaller, and their ecosystem weaker. For companies with complex, global requirements, they are often not a viable alternative.

At the same time, awareness of the risks is growing. The threat of market concentration, vendor lock-in, exploding costs, and legal uncertainties are driving companies to seek alternatives. Multi-cloud strategies, in which workloads are distributed across multiple providers, are considered a solution. However, the complexity of such architectures is enormous. Companies need expertise in multiple cloud platforms, must orchestrate data flows, and harmonize security policies. Costs often rise instead of fall.

Another trend is edge computing, where data is processed closer to its point of origin rather than in central data centers. This reduces latency, improves data protection, and decreases dependence on cloud hyperscalers. However, here too, American providers dominate technological development. European initiatives such as the 8ra initiative within the IPCEI-CIS program are attempting to build a federated edge cloud continuum – with 150 partners and three billion euros in funding. Whether this will be enough to become competitive with the hyperscalers is questionable.

The current situation can be summarized as follows: Europe is digitally dependent, legally vulnerable, and strategically incapable of action. The AWS outage of October 2025 was a wake-up call – but an effective remedy is lacking.

Germany, France and China: Three approaches to digital sovereignty

A comparison of national strategies highlights the different approaches and their prospects for success in the struggle for digital sovereignty. Germany, France, and China represent three fundamentally different philosophies – each with its own strengths and weaknesses.

Since 2020, Germany has officially pursued a strategy to strengthen digital sovereignty in public administration. At its core is the German Administrative Cloud, which was symbolically launched in March 2025. The concept is based on open standards, interoperability, and multi-cloud principles. Public administrations should be able to use cloud services from various providers without becoming locked into a specific vendor.

The theory sounds convincing. Practice reveals fundamental contradictions. The administrative cloud initially only offers services from public IT service providers – capacities are limited, functionality restricted. To meet real-world requirements, government agencies continue to rely on commercial providers. Of the 32 cloud services currently in use, most come from Microsoft, AWS, Google, and Oracle. The planned sovereign cloud for the federal administration is based on Microsoft Azure – a US provider.

This discrepancy between aspiration and reality has structural causes. Germany lacks its own hyperscalers with global reach. Deutsche Telekom, SAP, and United Internet are too small or too specialized to compete with AWS. The federal cloud lacks the capacity to meet the needs of the administration. Open-source software, originally planned as the foundation, is only used to a limited extent. Instead, proprietary systems from American corporations dominate.

The consequences became dramatic in July 2024, when a faulty update from CrowdStrike, a US cybersecurity provider, caused worldwide IT outages. Critical infrastructure in Germany was also affected. A similar risk exists with dependence on Microsoft Azure. The German strategy is failing due to a lack of investment, fragmented responsibilities, and insufficient political will.

France is pursuing a more ambitious approach. In November 2021, the government announced a €1.8 billion program to promote the French cloud industry. The goal: to create national champions that can compete with AWS. At the heart of this program is OVHcloud, the largest European cloud company, which went public in 2021.

The French strategy combines government funding, industrial policy planning, and strategic partnerships. Twenty-three research and development projects received €421 million in public funding, 85 percent of which went to SMEs, startups, and open-source projects. An additional €444 million came from EU funds and €680 million from private co-financing. The European Investment Bank supported OVHcloud with a €200 million loan for infrastructure development.

The plan has partially worked. OVHcloud has grown to become one of the top ten cloud providers worldwide, operating 43 data centers in nine countries and serving 1.6 million customers. The French government uses OVHcloud for critical applications. The European Commission has also signed contracts with the company.

Nevertheless, doubts remain. OVHcloud generates approximately three billion euros in annual revenue – less than three percent of AWS. Its product range is narrower, its global reach smaller. A serious fire in a data center in 2021 and a network outage damaged trust. Furthermore, France is making compromises: The defense contractor Thales is cooperating with Google to offer state-approved cloud services for sensitive data. This is hardly true digital sovereignty.

The French strategy demonstrates that a European cloud champion can emerge through government support, industrial policy planning, and scaling. However, the gap to the hyperscalers remains enormous. Without European coordination, economies of scale, and decisive action against US dominance, OVHcloud will remain a niche player.

China is pursuing a radically different path: digital self-sufficiency. The Chinese government recognized the strategic importance of cloud infrastructure early on and specifically created a framework for domestic providers. Alibaba Cloud, which originated from the e-commerce giant Alibaba, dominates the Chinese market with 35.8 percent. Huawei Cloud follows with 18 percent, Tencent Cloud with ten percent, and Baidu Cloud with six percent.

This dominance is no accident. The Chinese government limits market access for foreign providers through technical, regulatory, and political barriers. AWS, Microsoft Azure, and Google Cloud are marginalized or completely excluded in China. At the same time, the state is massively promoting domestic technology development. Alibaba Cloud has invested billions in data centers, AI platforms, and global expansion.

The result is a largely self-sufficient digital ecosystem. Chinese companies use Chinese cloud providers. The data remains in the country, under the control of the Chinese government. At the same time, Alibaba Cloud, Huawei Cloud, and Tencent Cloud are expanding internationally—particularly in Southeast Asia, the Middle East, and Africa. They offer lower prices, better local adaptation, and political independence from the US.

This strategy comes at a cost. The Chinese market is less innovative due to a lack of competition from global players. Dependence on the state creates risks for companies. The global expansion of Chinese cloud providers is met with suspicion, particularly in Western countries. Nevertheless, the strategy is successful: China has achieved digital sovereignty – through isolation, subsidies, and strategic planning.

The comparison highlights Europe's predicament. Germany wavers between rhetoric and pragmatism without achieving genuine sovereignty. France invests strategically but lags far behind the hyperscalers. China demonstrates that digital sovereignty is possible – if the political will exists and massive resources are mobilized. Europe lacks both – and is paying the price in increasing dependence.

The dark side of the cloud: Systemic risks and unresolved conflicts of objectives

The concentration of global cloud infrastructure in the hands of a few American corporations creates systemic risks that extend far beyond technical failures. A critical assessment must encompass economic, security policy, legal, and social dimensions.

The risk of technical single points of failure was brutally exposed once again on October 20, 2025. A DNS problem in an AWS region crippled thousands of services globally. This is not an isolated incident. AWS has experienced at least seven major outages since 2011, with Microsoft Azure and Google Cloud seeing similar frequencies. The likelihood of further disruptions is high, and the consequences become more severe with increasing dependency.

Financial market regulators have identified the risk of concentration as a systemic risk. A simultaneous failure of several banks due to a cloud provider outage could paralyze payment systems, trigger liquidity crises, and shake confidence. The Bank for International Settlements warns that dependence on a few cloud providers creates risks that traditional risk models fail to capture. Regulatory requirements for redundancy and exit strategies remain vague.

The economic risk of vendor lock-in is significant. Companies deeply integrated with AWS or Azure cannot switch without investing millions in migration, redevelopment, and testing. This lock-in gives hyperscalers pricing power. Broadcom's acquisition of VMware and the subsequent price increases of two to five times illustrate the risk: vendors use their market power to maximize profits.

The cost explosion is increasingly affecting businesses. IDC's Cloud Pulse Survey 2023 revealed that nearly half of cloud users experienced unexpected cost overruns, and 59 percent expected similar overruns in 2024. The opaque pricing structure with hundreds of options makes cost control virtually impossible. Companies start with low budgets and end up paying millions after years – with no way out.

The security risk posed by extraterritorial data access is acute. The US Cloud Act grants American authorities access to all data managed by US companies – regardless of server location. This also applies to European companies using AWS or Azure. The justification – combating terrorism and law enforcement – may be legitimate. However, the consequence is that European company data can be accessed without European judicial oversight.

The risk of industrial espionage is real. Sensitive research data, trade secrets, patents, strategic plans – all of this resides on servers under US jurisdiction. Historical revelations like the Snowden leaks have shown that US intelligence agencies collect massive amounts of data, including from allies. Technical safeguards – encryption, access control – offer only limited protection if the provider is obligated to cooperate.

The conflict with the GDPR remains unresolved. The EU General Data Protection Regulation prohibits data transfers to third countries without an adequate level of protection. In the 2020 Schrems II ruling, the European Court of Justice determined that US data protection does not meet this standard. Standard contractual clauses and certifications offer only limited relief. European companies are operating in a legal gray area – an untenable situation.

The geopolitical dimension is intensifying. In a world of increasing geopolitical tensions between the US, China, and Europe, digital infrastructure is being weaponized. In the event of a conflict, the US could use access to European data for sanctions, surveillance, and political pressure. China is already doing this: companies are required to store their data in China, under government control. Europe is caught between the blocs—without its own infrastructure and without the capacity to act.

The sustainability risk is underestimated. Data centers consume enormous amounts of energy – globally around two percent of electricity generation, and this figure is rising. Cloud providers advertise climate neutrality, but their energy demands are growing due to AI training, big data analytics, and increasing usage. Dependence on cloud hyperscalers cements energy-intensive business models. Decentralized, edge-based architectures would be more efficient – but are hampered by the market power of the hyperscalers.

Societal risks include digital exclusion. Small businesses, startups, and organizations in developing countries increasingly cannot afford the costs of hyperscalers. This exacerbates digital inequality. At the same time, dependence on American platforms fosters cultural homogenization. European values—data privacy, transparency, democratic control—are undermined by American business models.

The debate is highly controversial. Proponents of hyperscalers argue that cloud computing has democratized innovation, enabled startups, and reduced costs. They maintain that the economies of scale and technical expertise of hyperscalers are unmatched. Regional alternatives, they contend, would be more expensive, less efficient, and stifling innovation. They assert that the market functions, competition exists, and companies have freedom of choice.

Critics argue that freedom of choice is an illusion when vendor lock-in exists. Market power hinders, rather than promotes, innovation. Costs are opaque and spiraling out of control. The security and legal risks are unacceptable. Digital sovereignty is not an ideology, but a strategic necessity.

The conflict of objectives is real: efficiency versus sovereignty, innovation versus control, globalization versus localization. Europe must resolve this conflict – or bear the consequences.

🎯🎯🎯 Benefit from Xpert.Digital's extensive, five-fold expertise in one comprehensive service package | BD, R&D, XR, PR & Digital Visibility Optimization

Benefit from Xpert.Digital's extensive, five-fold expertise in a comprehensive service package | R&D, XR, PR & Digital Visibility Optimization - Image: Xpert.Digital

Xpert.Digital possesses in-depth knowledge across various industries. This allows us to develop tailored strategies precisely aligned with the requirements and challenges of your specific market segment. By continuously analyzing market trends and monitoring industry developments, we can act proactively and offer innovative solutions. The combination of experience and expertise generates added value and provides our clients with a decisive competitive advantage.

More information here:

Can Europe achieve digital sovereignty with the 8ra and billions in investments? Three future scenarios for the cloud – and what they mean for businesses

The future of the cloud: Scenarios between superpower dominance and digital emancipation

The development of global cloud infrastructure is at a crossroads. Several trends point to fundamental changes – but the direction is uncertain. Which development paths are likely? What disruptions could alter the market structure?

The baseline trend is: further growth and consolidation. The global cloud market will grow from $1.3 trillion in 2025 to $2.3 trillion in 2030 – an annual growth rate of 12.5 percent. Some forecasts are even more optimistic, predicting $1.6 trillion by 2030. Drivers include artificial intelligence, IoT, digital transformation, and growing data volumes.

Market shares will shift, but the dominance of the Big Three remains. Microsoft Azure is growing faster than AWS – driven by AI partnerships, particularly with OpenAI. In the second quarter of 2023, Azure briefly overtook AWS in new customer growth but couldn't secure the overall lead. Google Cloud benefits from its AI expertise and data analytics strength. However, AWS remains number one with a 30 percent market share.

A potential disruption: Artificial intelligence could shift the balance of power. AI training and inference require specialized hardware, enormous computing power, and new architectures. Whoever offers the best AI platforms will gain market share. Microsoft has an advantage through its OpenAI partnership, Google through its research expertise. AWS lags behind in public perception but is investing heavily.

Neoclouds, specialized cloud providers for AI workloads, could carve out niche markets. CoreWeave, Databricks, and Lambda Labs offer GPU infrastructure and AI platforms at competitive prices. While they don't reach the breadth of the hyperscalers, they excel in specialized applications. Their market share will remain limited, but they are increasing competitive pressure.

A second trend is edge computing and the cloud-edge continuum. Applications such as autonomous driving, industrial automation, smart cities, and AR/VR require low latency – data must be processed close to its point of origin. Edge infrastructure reduces dependence on central data centers, improves data privacy, and enables new business models.

The European 8ra initiative aims to build a federated edge cloud continuum – 150 partners, three billion euros in funding, and a target of 10,000 edge nodes by 2030. OpenNebula coordinates the integration, and virt8ra is the first tangible implementation. The approach is promising: federated, interoperable, and sovereign. However, its scalability and competitiveness against hyperscalers remain questionable.

Telecommunications providers like Deutsche Telekom, Orange, and Telefónica could play a role. They possess geographically distributed infrastructure, customer proximity, and network expertise. Partnerships with hyperscalers are common: Orange and Capgemini operate Bleu, an Azure-based French sovereignty cloud. But even here, hyperscaler technologies ultimately dominate.

A third trend is cloud repatriation and hybrid cloud strategies. Companies are recognizing the risks and costs of the public cloud and are moving workloads back to their own data centers or private clouds. According to the Barkley CIO Survey 2024, 83 percent of companies are planning such migrations. Reasons include cost, vendor lock-in, compliance, and performance.

Hybrid cloud models, which combine public cloud, private cloud, and on-premises infrastructure, are considered the future. By 2030, 90 percent of large enterprises and 60 percent of SMEs will be using hybrid IT. This increases complexity, requires orchestration and management tools, but offers flexibility and risk diversification.

Multi-cloud strategies, where companies use multiple providers in parallel, reduce dependence on a single provider. However, the complexity is enormous: different APIs, security models, and cost structures. Only large companies with the corresponding IT expertise can implement multi-cloud effectively.

Further disruption could arise from regulation. The EU is considering stricter rules regarding the risk of concentration, interoperability, and data portability. The Digital Markets Act targets platform power, while the Data Act focuses on data access. Stricter enforcement of the GDPR could force cloud providers to actually host data within the EU – without US access.

China and other countries are intensifying data localization. Data must be stored within the country, and foreign providers are subject to local laws. This fragments the global cloud market, creates regional ecosystems, and reduces hyperscaler dominance. The price: fewer economies of scale, higher costs, and less innovation.

Geopolitical tensions could escalate. A trade conflict between the US and the EU could affect cloud services – with tariffs, sanctions, and forced localization. A security conflict with China could drive Western cloud providers out of Asian markets. The fragmentation of the internet into geopolitical blocs – the Splinternet – is becoming more likely.

Technological innovations could bring about paradigm shifts. Quantum computing could make encryption obsolete – or enable new security models. Decentralized, blockchain-based cloud infrastructures could challenge hyperscaler dominance. But it will take years for these technologies to reach market maturity, and the hyperscalers are also investing in them.

Three scenarios seem plausible:

Scenario 1: Hyperscaler hegemony. AWS, Microsoft, and Google consolidate their dominance, achieving a 70 percent market share, integrating AI platforms, and controlling edge infrastructure. Europe remains dependent, Gaia-X fails, and sovereignty remains mere rhetoric. Regulation is ineffective because economic dependence paralyzes political action. The result: the digital colonization of Europe.

Scenario 2: Regulated Multipolarity. Stricter EU regulation, data localization, and geopolitical fragmentation create regional markets. European providers gain market share in the regulated environment, US hyperscalers remain globally dominant, and China expands its own ecosystem. The result: a fragmented but diversified cloud ecosystem with regional champions.

Scenario 3: Technological paradigm shift. Edge computing, decentralized architectures, and new AI models reduce dependence on centralized cloud data centers. Federated, interoperable infrastructures emerge, telecommunications providers play a larger role, and European initiatives like 8ra succeed. The result: a fragmented but sovereign digital infrastructure.

Which scenario unfolds depends on political decisions, investments, and geopolitical developments. Scenario 1 is likely if Europe continues to hesitate. Scenario 2 requires decisive political action and massive investments. Scenario 3 is possible, but not guaranteed – technological development is unpredictable.

The prediction is: The next five years are crucial. Either Europe succeeds in digital emancipation – or its dependence will become irreversible.

Strategic Empires: What Needs to Happen Now

The analysis leads to clear strategic imperatives for politics, business, and society. Digital sovereignty is not an ideological project, but an economic and security policy necessity. The following measures are required:

First, Europe needs a coordinated cloud strategy with massive investments. The French model of industrial policy support for domestic champions shows the way, but it is not enough. A European solution is necessary: consolidation of European providers, shared infrastructure, and harmonized standards. The 8ra initiative with three billion euros in funding is a start, but too small. Investments in the range of 50 to 100 billion euros over ten years would be necessary – comparable to the European chip program.

Secondly, regulation must show teeth. The Digital Markets Act and Data Act must be rigorously enforced, with a focus on interoperability, data portability, and anti-lock-in mechanisms. Cloud providers must be obligated to facilitate migrations, provide data in standardized formats, and offer open APIs. The risk of market concentration must be addressed through regulation, for example, by setting caps on market shares of critical infrastructure.

Thirdly: The US Cloud Act is unacceptable. Europe must insist on a transatlantic data agreement that respects EU standards and excludes extraterritorial US access. If this fails, European companies and authorities must be obligated to host sensitive data with European providers. The legal gray area must be closed.

Fourth: Public procurement must favor European providers. A “Buy European” clause for cloud infrastructure, similar to the “Buy American” rules in the US, would provide domestic providers with planning certainty and scalability. This is WTO-compliant if security interests are invoked. The German federal administration should lead by example and end its dependence on Azure.

Fifth: Education and skills development are crucial. Europe needs more cloud engineers, data scientists, and cybersecurity experts. Universities and universities of applied sciences must expand their relevant degree programs. Companies need training programs for multi-cloud management, cloud security, and vendor switching strategies.

Sixth: Companies need to rethink their cloud strategies. Blindly migrating to the public cloud was a mistake. Hybrid cloud models, which keep critical workloads in private clouds or on-premises, are less risky. Multi-cloud strategies reduce dependency but require expertise and investment. Cloud repatriation can be economically viable, as the examples of Dropbox, GEICO, and 37signals demonstrate.

Seventh: Edge computing and federated infrastructures must be promoted. The 8ra initiative is promising but needs more support. Telecommunications providers should invest more heavily in cloud and edge infrastructure, ideally in cooperation with European cloud providers. This creates regional, low-latency, sovereign infrastructure.

Eighth: Transparency and accountability must be increased. Cloud providers should be required to disclose outage statistics, security incidents, and data access by authorities. Independent audits should verify compliance with EU standards. Users have a right to know how their data is processed and who has access to it.

The lessons from the AWS outage of October 20, 2025, are clear: Digital infrastructure is critical infrastructure. Dependence on a few providers is a systemic risk. The comparison with Gazprom is apt: Both are monopolies, both are geopolitical levers, and both pose risks to European sovereignty.

But there is a crucial difference: Gas dependence was visible, politically debated, and partially reduced. Cloud dependence is invisible, technically complex, politically neglected – and increasing. Europe learned from the energy crisis, sought diversification, and built infrastructure. These lessons must be applied to digital infrastructure.

The long-term importance of this issue cannot be overstated. Whoever controls the digital infrastructure controls the economy of the future: data flows, AI applications, industrial automation, and social communication. Europe faces a choice: digital emancipation through decisive action – or digital colonization through inaction. Time is running out.

Your global marketing and business development partner

☑️ Our business language is English or German

☑️ NEW: Correspondence in your native language!

Konrad Wolfenstein

I and my team are happy to be available to you as your personal advisor.

You can contact me by filling out the contact form here wolfenstein@xpert.digital:or simply call me at +49 7348 4088 965. My email address is

I'm looking forward to our joint project.

☑️ SME support in strategy, consulting, planning and implementation

☑️ Creation or realignment of the digital strategy and digitization

☑️ Expansion and optimization of international sales processes

☑️ Global & Digital B2B trading platforms

☑️ Pioneer Business Development / Marketing / PR / Trade Fairs

🎯🎯🎯 Benefit from Xpert.Digital's extensive, five-fold expertise in one comprehensive service package | BD, R&D, XR, PR & Digital Visibility Optimization

Benefit from Xpert.Digital's extensive, five-fold expertise in a comprehensive service package | R&D, XR, PR & Digital Visibility Optimization - Image: Xpert.Digital

Xpert.Digital possesses in-depth knowledge across various industries. This allows us to develop tailored strategies precisely aligned with the requirements and challenges of your specific market segment. By continuously analyzing market trends and monitoring industry developments, we can act proactively and offer innovative solutions. The combination of experience and expertise generates added value and provides our clients with a decisive competitive advantage.

More information here: